Quite a few of you have been asking for my views on Keppel DC REIT.

So I decided to release this FH Premium post to everyone.

This FH Premium post was written in early Feb after the FY2023 financial results and tenant default news.

However this should give you an idea of my general thought process and fundamental analysis for Keppel DC REIT.

Do sign up for FH Premium for my latest views on Keppel DC REIT.

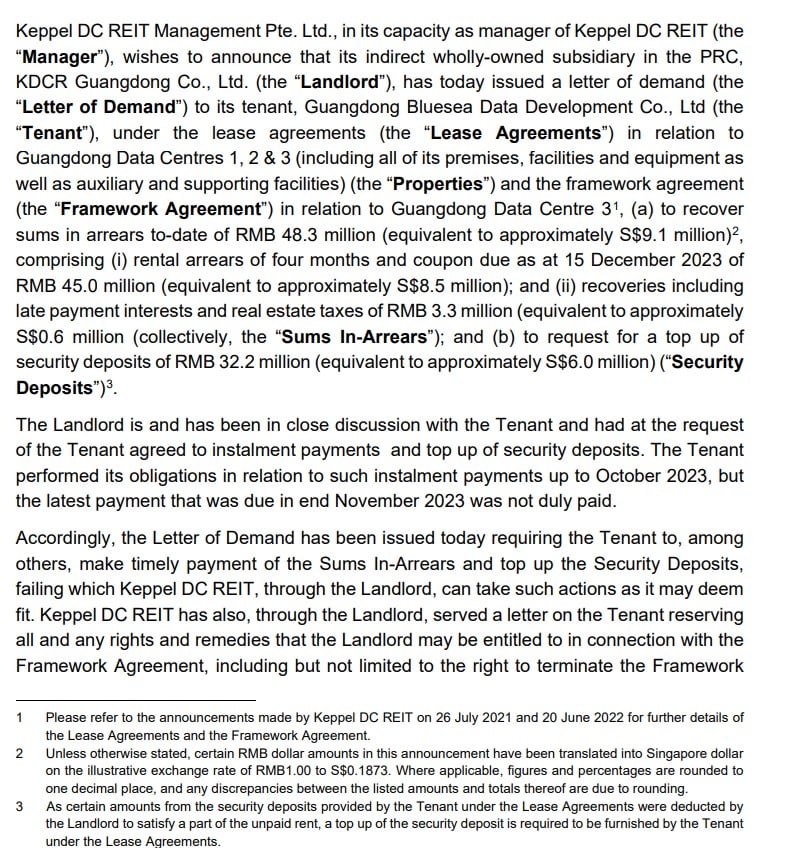

Recap of Keppel DC REIT’s Tenant default

I covered the tenant default situation in previous articles, so do check those out for a full recap.

The long and short is that:

- Tenant at the Guangdong data centre has defaulted on rent

- Total amount defaulted on to date is about 5.5 months rent

- The REIT has worked out a restructuring plan with the tenant, for them to make payments in instalments

- However the tenant has defaulted on the instalment plan in Nov 2023

- So the REIT issued a letter of demand to the tenant

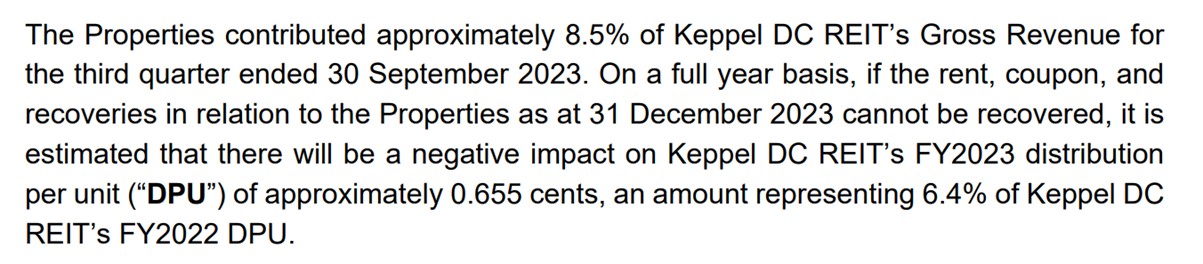

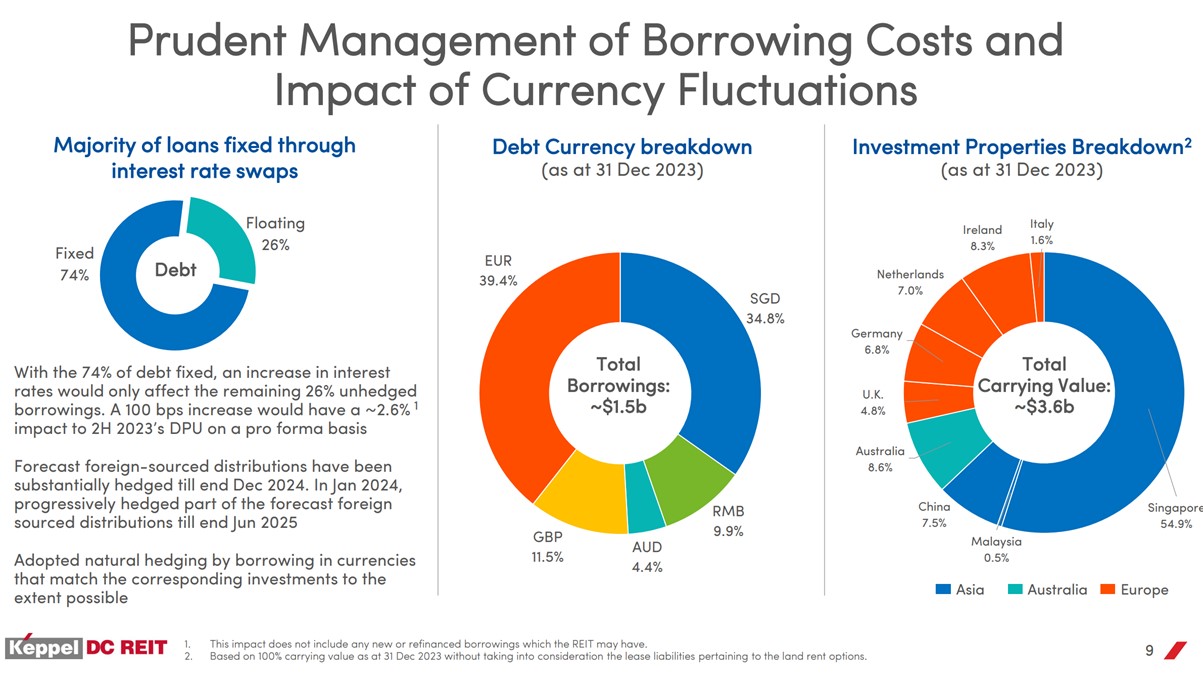

The Guangdong data centres account for 8.5% of the REIT’s gross revenue.

DPU impact is 6.4% of FY2023 DPU.

But don’t forget that is only about 5.5 months of rental in FY2023.

If you annualise it you’re probably looking at about 14% DPU impact.

DBS in an earlier report estimated DPU impact in the event of a complete default at 16% DPU loss.

So realistically you’re probably looking at 14 – 16% DPU impact from a full default.

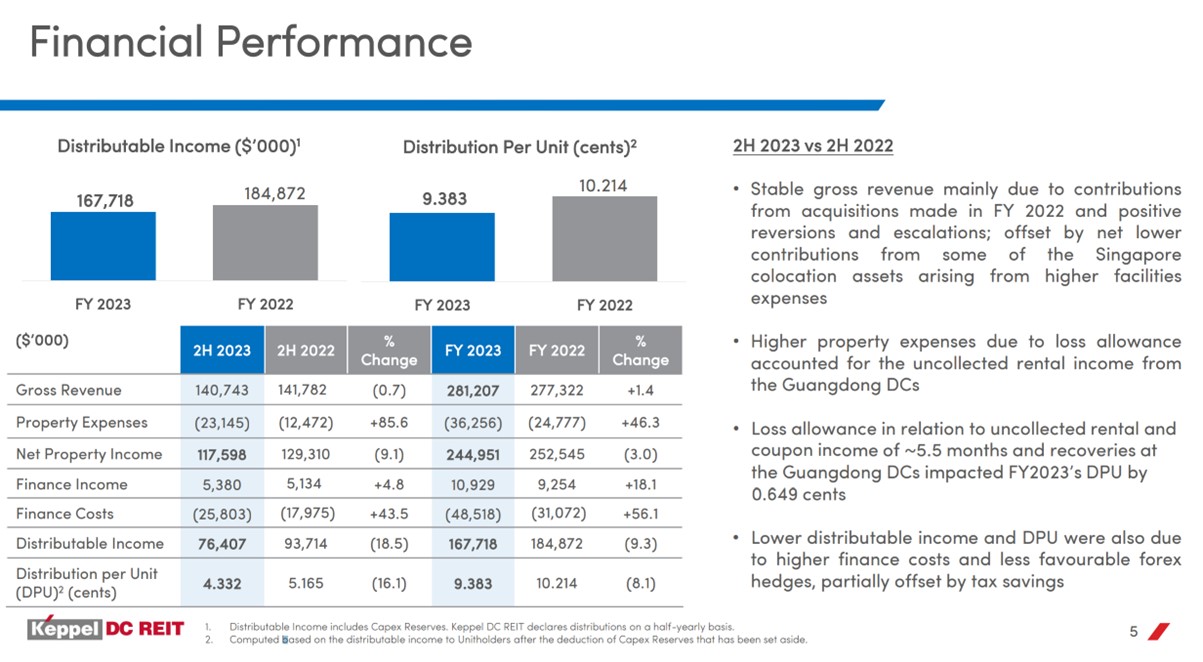

What did Keppel DC REIT announce in its 2H 2023 results?

All of the above was known to the market before this.

What did Keppel DC REIT announce in its latest 2H 2023 results?

The main change, is:

- Set aside loss allowance of 5.5 months uncollected rental from Guangdong Data Centre

In simple English – because of the uncertainty over whether they can collect the 5.5 months rental, they have “written off” the rental for now (to be added back if there is successful recovery).

What is the DPU impact for Keppel DC REIT – big drop in dividend yield?

2H 2023 DPU impact is negative 16.1% (vs 2H 2022).

To be fair 2H 2022 is not a good comparison because the interest expenses were a lot lower back then (due to lower interest rates).

So let’s dive into the numbers to make the adjustments ourselves.

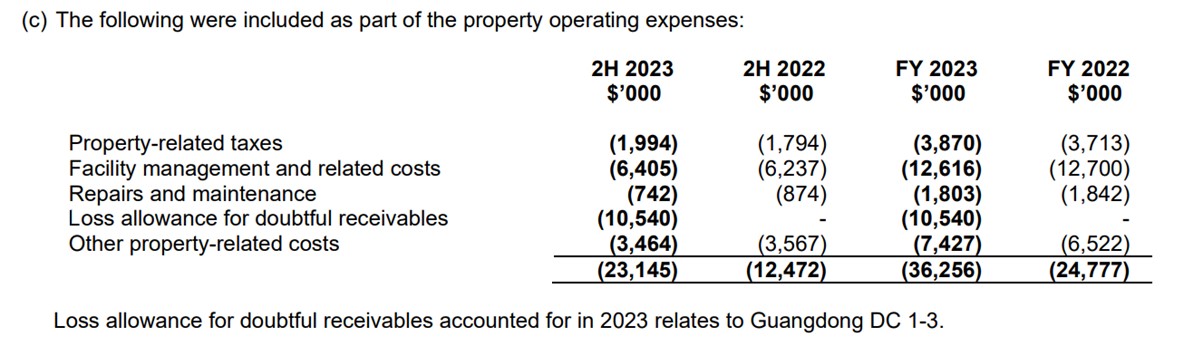

The REIT set aside $10.540 million loss allowance for the uncollected rental.

This is 5.5 months, so over a full 6-month period it would be $11.498 million.

In plain English, you can split this into 2 Scenarios:

Scenario 1 – If you assume zero contribution from the Guangdong DC for Keppel DC REIT

2H 2023 DPU would be 4.277.

Using latest unit price of $1.7, that is 5.03% dividend yield.

Scenario 2 – If you assume Guangdong DC issue will be resolved eventually (new tenant found at similar rents, or existing tenant rescued)

2H 2023 DPU would be 4.981.

Using latest unit price of $1.7, that is 5.86% dividend yield.

Which is the correct interpretation for Keppel DC REIT?

I don’t think Scenario 1 is the right way to see it if you’re a long term investor.

It is the same logic with the REITs during COVID.

When the malls were shut, and rental income dried up.

Yes the DPU for that year (or two) would be affected, and share price dropped short term.

No doubt about that.

But unless you believed that COVID would be around forever, you would realise the rental income would eventually come back once COVID went away.

Which meant this could be a buying opportunity for long term investors.

This is a temporary problem for Keppel DC REIT?

I see this broadly the same way.

Yes, no doubt the uncertainty over the DPU is going to hit short term distribution yield, and will impact share price.

But just like COVID – this doesn’t affect the competitiveness of the underlying properties.

Assuming Keppel DC REIT can find a replacement tenant or work out issues with the existing tenant, the rental is unlikely to stay at zero forever.

It’s the whole Warren Buffett analogy about the shop with renovation taking place in front of it.

Because of the renovation, number of shoppers to the shop fell.

But since the renovation would go away eventually, the sell-off could prove to be a good buying opportunity for long term investors.

What are the risks for Keppel DC REIT?

Your main risk is if the REIT defaults in the short term, or is forced into a dilutive fundraise – resulting in permanent capital loss for investors.

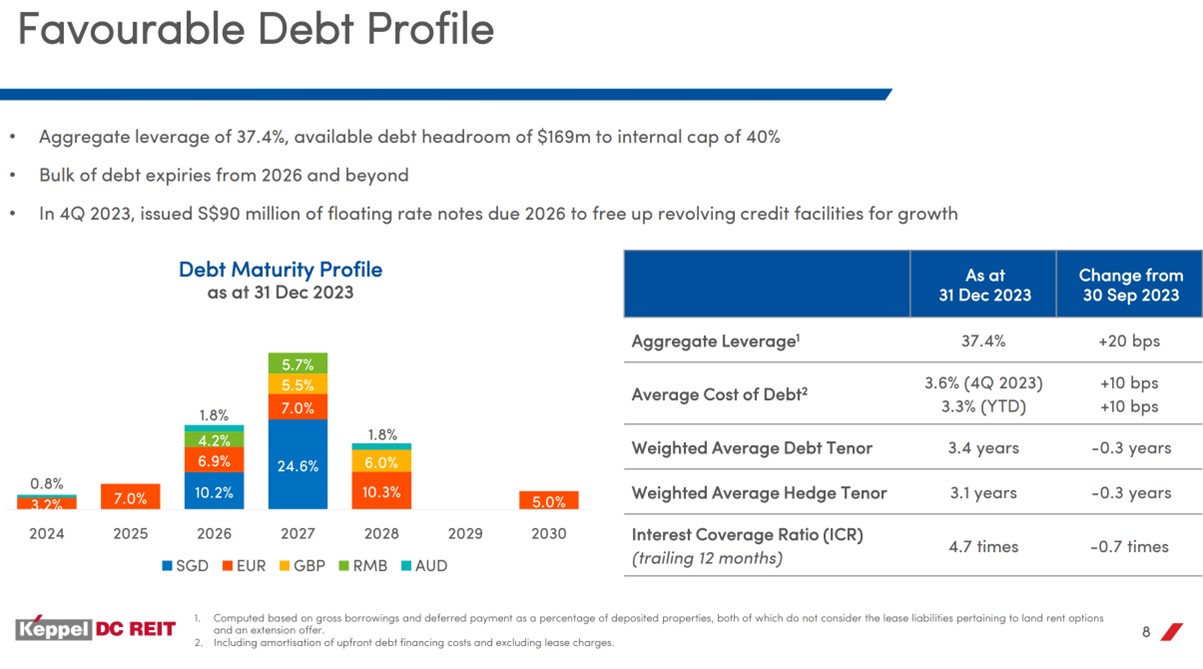

But leverage at 37.4% is acceptable and not flashing warning signs yet.

Just like with COVID, the reduced rental income will mean less distributions, but there is unlikely to be a loan default as the rest of the properties are still cash generating.

Cost of debt at 3.6% is also in line with market, and unlikely to increase materially from here.

Long story short – I think this tenant issue is a short term issue, and will eventually be resolved.

The biggest question for investors is how bad will the short term impact be?

How bad is the short term impact for Keppel DC REIT? (Fundamentals)

Unfortunately, Keppel DC REIT’s management did not provide a lot of information on the tenant during the conference call when they were grilled on this issue.

Here’s OCBC Research reporting:

“Management mentioned several times during the analyst briefing about working with the master lessee on a recovery roadmap, but details were scant and under current challenging macro and industry conditions in China, we believe the prospects remain dim. We thus expect more provisions ahead,”

Poring over the financial results, details on this tenant were indeed scant, and I could not find much information in the financial results.

More information on the tenant in question from previous reports – Neo Telemedia:

Neo Telemedia Ltd is an investment holding company principally engaged in the provision of data center services. The Company primarily operates through three business segments. The Data Center segment is engaged in the provision of data center services to its customers in Mainland China. The Others segment is engaged in the provision of system integration services, bus services and rental of properties. The Trading of Telecommunications Products segment is engaged in the provision of trading of telecommunications products.

Neo Telemedia, the master lessee of KDC REIT’s data centres made a net loss in 1HFY2023 for the six months ended June… Neo Telemedia reported a loss of HK$123.7 million or a loss per share of 1.3 HK cents for the six months to June 30. This compared with a net profit of HK$40 million in 1HFY2022. Interestingly, Neo Telemedia recorded both positive operating cash flow and free cash flow.

However, on the bank loans and debt front, Neo Telemedia has some HK$842.7 million of loans (of which HK$548 million are bank loans) categorised as current liabilities, which are generally payable within a year.

According to the financial report for 1HFY203, Neo Telemedia states that HK$500.4 million of loans were guaranteed by property, plant and equipment (PPE) with net book value of HK$161.9 million. Neo Telemedia has HK$14 million in cash and its net assets stood at HK$836 million.

Doesn’t look good, and just looking at the numbers alone you wonder why the REIT hasn’t terminated the lease and started the search for a new tenant.

I suppose the REIT here has 3 options:

- Continue to negotiate with the tenant in the hopes that something will improve (for eg. If a white knight bails them out – although I’m not sure how likely this is, as things seem to be getting worse)

- Cut losses (terminate the lease, and find a replacement tenant)

- Sell the property

Here’s JP Morgan’s view on the issue:

“While the tenant made a token RMB0.5 million ($0.1 million) payment towards its arrears, we are more positive that they are working to resolve the situation, although details of time lines remain uncertain. We see this as preferable to the vacant re-possession of the Guangdong data centres, with associated costs and downtime for leasing.

As for Guangdong DC 3, KDCREIT is reviewing options including divestment to a third party, which in our view, would be most optimal to generate cash flows for the tenant,”

Realistically, the REIT is probably going to try (1) for a while, and if things don’t get better they will have no choice but to go with (2).

So you would expect this to drag out for a while.

Not great in the short term.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

What is the downside for Keppel DC REIT (fundamentals wise)?

As shared above, in the worst case scenario where you assume no contribution from Guangdong DC going forward, you’re looking at a 5.03% dividend yield at 1.70.

If you assume the market prices the REIT at a 5.5% dividend yield.

You’re looking at $1.55 fair value.

I would say this is slightly aggressive given this is a data centre REIT with 55% exposure to Singapore data centres, and a full write off of Guangdong DC is likely to be temporary.

So fundamentals wise, $1.55 is probably the downside case.

How bad is the short term impact for Keppel DC REIT? (Technical Analysis)

Technical Analysis for Keppel DC REIT is below, but do note that the charts are as of early Feb.

Some of this may have changed since, so do update your thinking accordingly.

My latest views on Keppel DC REIT is shared on FH Premium.

Charts wise – the key support levels are 1.7, followed by 1.6.

Those are the key supports I would watch for.

That said – do note that both simple and exponential moving averages are bearish and show the REIT in a downtrend.

Price is comfortably below both 50 and 200 day simple moving average:

And exponential moving averages show a clear downtrend:

Wait for Ex-Distribution date?

In my experience with S-REITs, they usually sell off further after the REIT goes ex-distribution.

For some reason, Singapore investors like to wait to collect the distribution, before they sell the REIT.

You usually see the REIT drop an amount equivalent to the distribution amount on ex-distribution date.

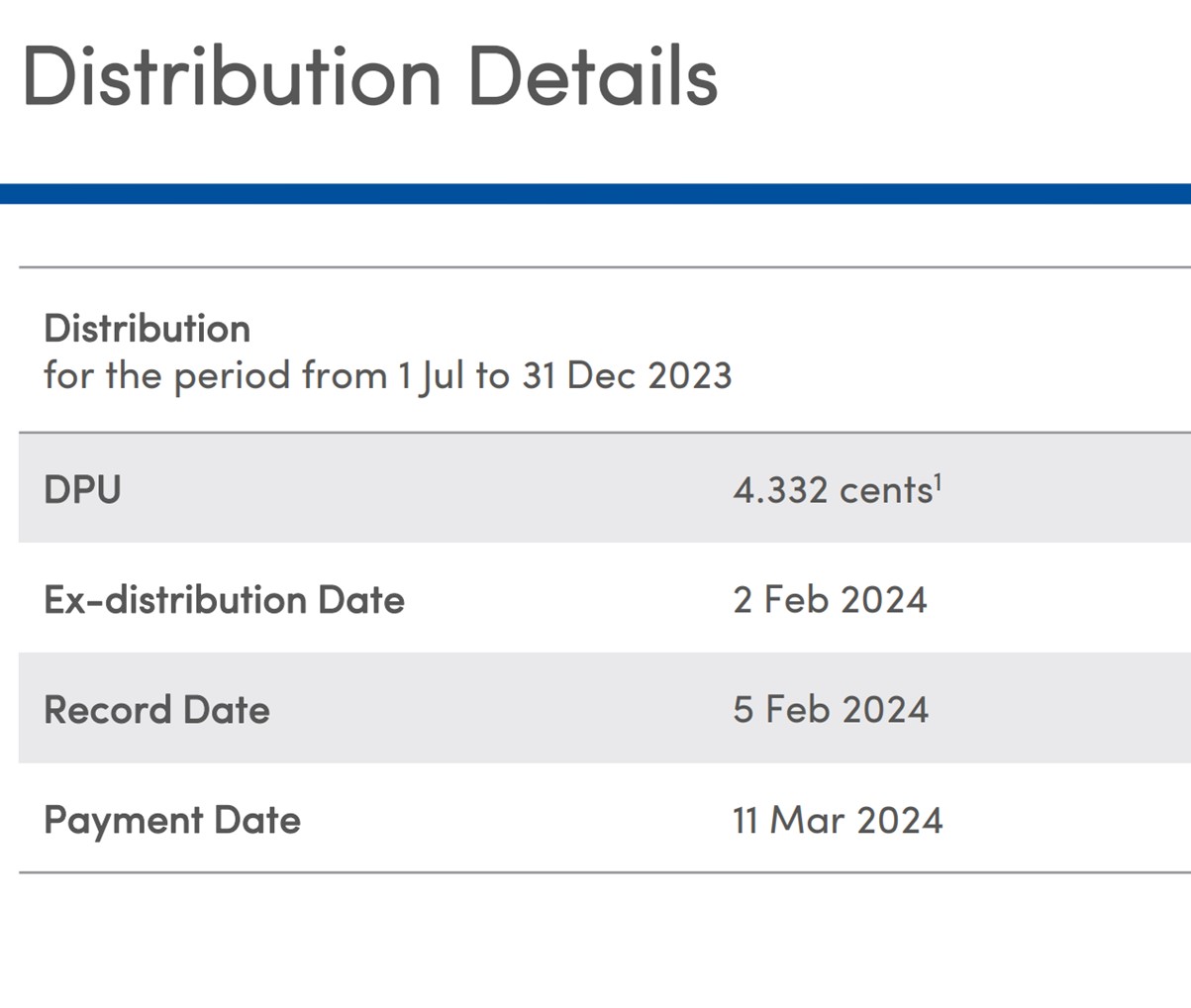

With a 4.332 cents DPU, that implies you may see a drop of 3 – 5 cents on 2 Feb alone.

Of course, this is not set in stone, but something that I’ve noticed in past experience.

Because of that, I would at least want to wait for 2 Feb to see how price trades ex-D.

List of shareholders for Keppel DC REIT?

Temasek is the biggest holder of Keppel DC REIT at 21%.

The rest are mainly retail / individual investors, with no big institutional names.

This is a double edged sword – as retail can be prone to panic selling on the downside.

So you may need to watch for downside risk if the key technical supports break.

Will I buy Keppel DC REIT?

As shared with those on the Financial Horse Tier, I recently picked up a small position in Keppel DC REIT.

I think I shared previously that when adding a new position I like to pick up a small position first to have some skin in the game, and have a reference point price-wise, while I continue up the analysis.

This was the same – so I added a small position in Keppel DC REIT, and the decision now is whether to average into the position, and when to do so.

Looking at all of the above, the fact that management is not giving a lot of guidance on the tenant situation is worrying.

The market hates uncertainty, and until this matter is cleared up, I would expect the REIT’s share price to stay weak.

That said, if you take a longer term view, I do think this is similar to COVID in the sense that the difficulties are temporary.

I do not expect it to last forever – eventually the tenant situation is likely to be solved, or a new tenant found, and some level of rental restored.

So I would be keen to average into the position on any further declines, given this is a data centre REIT with 55% exposure to Singapore data centres (quite a scarce asset class).

The 2 Feb ex-D date is probably the first big milestone to watch.

Usually the REIT will sell-off by the DPU amount on ex-D, which implies a 3-5 cents sell-off on 2 Feb alone (of course, this is not set in stone, actual amount may be smaller/bigger).

And technical wise, key level to watch if 1.7 breaks would be $1.6.

While fundamental wise, 1.55 is attractive to watch.

So those are the key levels I would be watching for in the weeks ahead when adding.

But of course, if there is a true sell-off the market can blow past these levels, so do be cautious as always.

Note that this FH Premium article was written in early Feb and has not been updated since.

For my latest views on Keppel DC REIT, do sign up for FH Premium.

Given the number of great investment opportunities out there today, I can afford to be picky, and only buy stocks / REITs where both the fundamental and technical analysis lines up (see my full watchlist on FH Premium).

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

– Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.