I’ve noticed quite active discussion about CapitaLand Invesment among readers.

So I wanted to release this FH Premium article written last month, to give an insight into my thinking.

Note that this was written in early April, so some of the charts are slightly outdated – but the thought process remains relevant.

If you find this useful – do sign up for FH Premium for more premium articles like this.

So the list of stocks that you guys (FH Premium readers) have asked for a deeper dive on are:

- CapitaLand Investment

- CDL

- Parkway Life REIT

- Ping An

- Link REIT

(If there are any others that you want a deep dive into, please feel free to leave a comment below.)

In today’s article I decided to take a deeper look at CapitaLand Investment.

CapitaLand has big exposure to China real estate, so it’s a good opportunity to discuss some of the recent developments in China.

As always, I spend some time discussing the broader geopolitical climate and thought process, but if you want the summary just skip to the conclusion at the end.

CapitaLand Investment’s share price is at cycle lows (since IPO)

Here’s the latest share price for CapitaLand Investment.

At 2.70, this is close to the all time lows since “IPO” in 2021 (technically not IPO but a spin off).

Dividend yield is 4.44% at this price (12 cents per share).

If you include the special dividend of 6.1 cents in FY 2022 (distribution of 0.057013 CapitaLand Ascott Trust (CLAS) unit per ordinary share and the closing market price of S$1.07 per CLAS unit on 11 May 2023).

Then it is a dividend yield of 6.7% (including special dividend).

However do note that there was no special dividend for FY 2023 (there was 0.03 special dividend in FY 2021 however), so I think the 4.44% dividend yield is the more “accurate” number.

Meanwhile CapitaLand Investment trades at 0.99x book value.

For a Temasek backed real estate developer that holds quite a sound property portfolio, and is trying to position itself as a real estate investment manager (asset light model like Blackrock / Blackstone).

Is there value at this price?

Is CapitaLand Investment a good buy at this price?

CapitaLand issued a profit warning for FY2023, and for good reason because profit dropped over 70% on a year on year basis.

The big reason for that loss – is due to revaluation loss arising from lower property prices.

The 2 big losers?

China, and US.

The Singapore portfolio did well (which is why I keep saying to focus on Singapore real estate this cycle).

India portfolio did decent too, and Europe was average.

But the 2 big markets of China and US performed terribly.

Note how China makes up 34% of the AUM and suffered a $511 million loss.

While USA + UK + Europe makes up 9% of the AUM, and USA alone suffered a $213 million loss.

Just goes to show how huge the decline in US real estate prices has been.

Note also that 34% of CapitaLand Investment’s AUM is in China, which means their China AUM is larger than their Singapore AUM:

Because of this, there are 3 points to discuss when analysing CapitaLand Investment:

- Macro – Has China bottomed?

- Macro – Interest rate outlook for real estate?

- Micro – Is CapitaLand Investment executing well?

Macro – Has China bottomed? (affects CapitaLand Investment’s China portfolio)

Ray Dalio had a great piece on China over the weekend.

It is not easy to summarise because there is a lot of nuance to the views (so I highly recommend reading if you are serious about investing in China).

But economically, the key takeaways are:

- China is going through a period where they need to transition their economy away from real estate / infrastructure growth, into new areas of growth like advanced manufacturing and domestic consumption

- This creates a lot of domestic discontent, as certain parts of the economy like real estate perform very poorly during this period. So ordinary folks will feel poorer because of lower income and lower house values, while the elites are in danger of losing their business empire and they consider political challenge against Xi

- At the same time, this coincides with a period of greater “conflict” with the west. Both in technology (bans on advanced technology sharing with China) and trade (tariffs or trade barriers against China)

What should China do?

Dalio’s conclusion is that (emphasis mine):

…the leadership needs to have a debt restructuring, which it should do via engineering a beautiful deleveraging or it will have a “lost decade” like Japan’s.

While many people think policy makers should ease monetary policy to create more credit, I think they correctly view creating more credit and debt like giving an alcoholic a drink to help ease withdrawal problems.

I believe that they should engineer both 1) a deleveraging (which is deflationary, depressing, and will reduce the debt burden) and 2) an easing of monetary policy (which is inflationary, stimulative, and will ease the debt burden) so that the deflationary ways of reducing debt and the inflationary ways of doing it balance. This is what I mean by a “beautiful deleveraging.”

What happens if this is not done?

In my opinion, this should have been done two years ago and if not done will probably lead to a lost decade.

I think some of the economic leaders, especially those who did this under Zhu Rongji, understand how to do this, but it is very difficult and politically dangerous to do because it engineers big changes in wealth, which is politically challenging, especially during a difficult time because people squawk. In my opinion, if the leadership doesn’t execute a beautiful deleveraging, China will have a Japanese-style lost decade with Marxist characteristics.

My views on China?

As you can see, Dalio’s views are very much in line with what I’ve been saying.

China is at risk of a Japan style lost decade here, if they do not handle the real estate crisis properly.

Given the size of the real estate industry (almost 30% of China’s GDP), you cannot replace it with domestic consumption or manufacturing overnight, short of a massive stimulus injection.

At the same time, actually handling the real estate crisis properly is not easy because it will be deeply unpopular and will lead to political challenge, which is why you see Xi taking steps to consolidate his power.

All while the western nations are actively trying to derail China’s development.

To date – we have seen very little signs of the massive stimulus injection required to spark a turnaround in China, the kind of “beautiful deleveraging” Dalio speaks of.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

Has that changed of late? Is China starting to inject the necessary stimulus?

That said – there are tentative signs that Beijing may be starting to change their views on this.

SCMP ran an interesting article last week that suggested China may start their own version of QE – buying China government bonds to inject money into the economy.

If this happens, this could be a meaningful policy signal, although the amount of QE needs to be large enough to move the needle (given the size of China’s real estate problem).

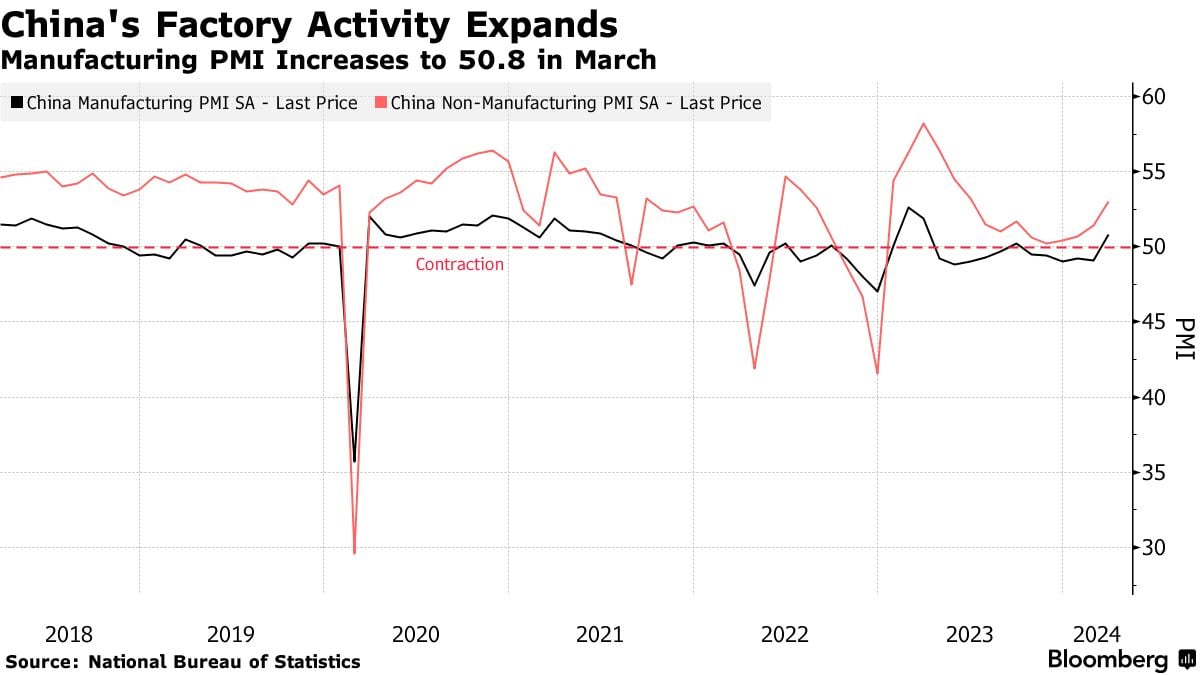

At the same time, economic data is picking up, and China’s PMI shows signs of a rebound:

So… Has China bottomed? Is it time to buy China stocks / real estate dividend plays?

Short answer is that I don’t know. Nobody knows.

The longer answer, is that China won’t bottom until we see what Ray Dalio coins the “beautiful deleveraging”.

Or more simply – enough money printing to offset the deflationary impact of the real estate bust.

So far, we haven’t seen that.

But if the PBOC does indeed start QE and money printing, that could very well change.

I’ve also noticed that 15,000 on the Hang Seng Index seems to be the line in the sand that policy makers will defend at all costs, marking when they intervened in both Nov 2022 and Jan 2024.

This coincidentally is the level that goes back to 1997, so there may be a “face” element to it in not letting the Hang Seng fall below the level when Hong Kong was reunited with China in 1997.

This could be a key trading signal in the sense that policy makers may not tolerate a big drop from here.

So no doubt China assets are cheap.

But as of today, we still don’t know if they will go through a “beautiful deleveraging” (in which case it would be a buy), or if they will go through a Japan style lost decade (in which case there is no hurry to buy).

Macro – Interest rate outlook for real estate? (affects CapitaLand’s global portfolio ex China)

We’ve discussed interest rates to death elsewhere, so I won’t belabour the point.

Do refer to the other articles on FH Premium that discuss interest rates.

Micro – Is CapitaLand Investment executing well as a company?

To give credit where credit is due.

I actually think CapitaLand Investment is executing well.

Management has been actively trying to transform into an asset light, real estate fund manager model like Blackrock / Blackstone.

And you can see from the charts below that this is paying dividends, as an increasingly large portion of their profits comes from fee based income (from managing real estate).

This is good, as it provides a stable fee based income to smooth out the volatility from shifts in real estate prices (while also providing upside potential if real estate prices recover).

CapitaLand Investment doesn’t have any liquidity issues – problem is one of profitability

Balance sheet is decent enough (for this climate).

Debt to equity is 0.56x.

Net debt to assets is 32%, which is lower leverage than many REITs.

I’ve been saying that the problem with real estate this cycle is not the liquidity risk (like in 2008).

None of the real estate players have problems borrowing, the problem is more of higher interest rates grinding down on profitability and real estate prices.

Summing up my views on CapitaLand Investment?

Will I buy CapitaLand Investment stock?

Full disclosure that I used to have a position in CapitaLand.

After the “IPO” and share price rose to the high 3s, I sold my entire position.

And I’ve not bought it back since.

The problem with CapitaLand as I see it – is the 34% AUM in China.

And for that 34% China AUM, you’re only getting a 4.44% dividend yield (without one-off dividends, there was none in 2023).

Let’s put it this way:

If I were bullish on China, I would just buy a pure China play like CapitaLand China Trust or Hang Lung. They pay 8-9% dividend yields at current prices, and offer 20-30% upside (or more) if China recovers.

If I were bullish on Singapore real estate, I would buy REITs like Ascendas REIT or CICT which pay 5.5% dividend yields, 1% higher than CapitaLand. Smaller caps like Starhill Global REIT can go as high as 7-8% dividend yields.

If I were bullish on US / European real estate (and I’m not), I would buy specific US or European focussed REITs, many of which offer double digit dividend yields (assuming things play out well).

In almost every scenario, there is a better play than CapitaLand Investment.

The only scenario where CapitaLand truly shines, is if:

- China does well, and

- Global interest rates drop.

This happened in early 2023, which is why the share price soared into the high 3s then.

The question I suppose, is whether this is likely to happen again.

I don’t know the answer to this, and if it does no doubt I would change my mind on this stock.

But even if it does, I wonder if the better play is to buy a basket of S-REITS and China focussed real estate plays instead.

You get a higher dividend yield while you wait, and probably higher capital gains if things go well.

Closing Thoughts: That said… CapitaLand management does seem to be executing well

For what it’s worth, I think CapitaLand management is executing well in transitioning into a fee based real estate manager.

The problems are not due to their fault – a weak China real estate market, and high global interest rates.

But as an investor, I can’t separate the management team and the macro climate.

As the Warren Buffet quote goes: “When a manager with a reputation for brilliance tackles a business with a reputation for bad economics, the reputation of the business remains intact.”

There are structural challenges for both global real estate (higher interest rates) and China (deleveraging).

The kind of AUM CapitaLand has exposes them to both.

No matter how good management is, there’s only so much you can do when there are structural headwinds against you.

Frankly I don’t see myself buying back into CapitaLand Investment.

I would rather just buy a basket of REITs (if I were betting on lower interest rates) and specific China focussed real estate plays instead (if I were bullish on China).

This would allow me to cut loss / take profit on either thesis, instead of needing to have both thesis work in my favour to make money.

In any case, I think the current sell-off is a good opportunity to add to stock / REIT positions.

I’ve shared on FH Premium the individual stocks / REITs I am keen to add (with rough target pricing), and I also share my latest personal portfolio.

Note that this FH Premium article was written in early April, so some of the charts are slightly outdated – but the thought process remains relevant.

If you find this useful – do sign up for FH Premium for more premium articles like this.

I share my latest macro thinking, as well as my Stock / REIT watchlist and personal portfolio, on FH Premium.

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

WeBull Account – Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund USD 500

- Execute 5 trades

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.