As you likely would have heard by now.

DPM Lawrence Wong announced 2 big changes to CPF at last week’s budget.

After which many Singapore investors were up in arms.

Given how integral CPF is for Singapore investors (most of us would have a decent chunk of our net worth in CPF).

I wanted to take some time out to discuss:

- What exactly are the changes to CPF-SA?

- How does this affect Singapore Investors in retirement?

- Are we able to invest to replace the CPF-SA?

How does CPF-SA work today (before the changes)

Let’s take a step back and start right at the top.

How did CPF Special Account (CPF-SA) work before this round of changes?

The way it worked, is that at 55 years of age.

Everything in your CPF-SA would be transferred into a CPF Retirement Account (CPF-RA), up to the Full Retirement Sum (FRS).

If you didn’t have enough in your CPF-SA, the rest would come from CPF-OA.

And the CPF-RA would then be paid out as part of CPF Life, which is basically an annuity that pays you a certain amount each month from 65 until you die.

This led to a “loophole” known as CPF “Shielding”

This led to a “loophole”.

The way it worked, was that investors would invest their CPF-SA savings before turning 55.

On their 55th birthday, the CPF-SA funds that were invested were locked up, and cannot be used to fill up CPF-RA.

Instead the CPF-OA funds (yielding 2.5%) would be used to fill up CPF-RA.

Once this happened.

The investor would sell their CPF-SA investments.

All the money goes back into CPF-SA (yielding 4.08%).

And voila.

You now have a big chunk of cash in your CPF-SA earning 4.08% interest, instead of the 2.5% in CPF-OA.

And because you are above 55, you can withdraw the money from CPF-SA any time.

Basically – you have a savings account paying 4% with instant liquidity.

What are the changes to CPF announced by Lawrence Wong?

If you thought this doesn’t seem very fair.

Well, this “loophole” has now been plugged.

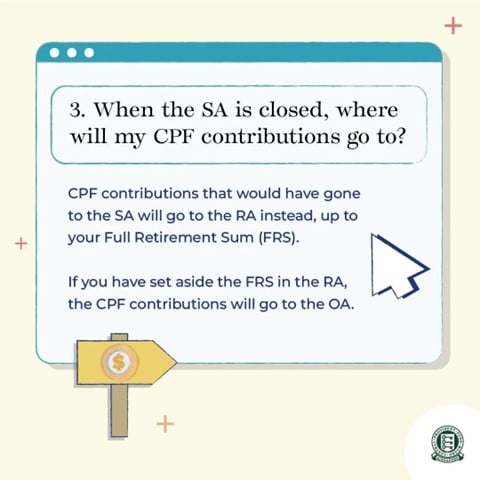

1) CPF Special Account now closed at age 55

At last week’s budget speech, DPM Lawrene Wong announced that the CPF-SA account will now be closed for CPF members aged 55.

This means after after 55, any CPF contributions that would have gone into the CPF-SA will now go into the CPF-RA instead (up to the FRS).

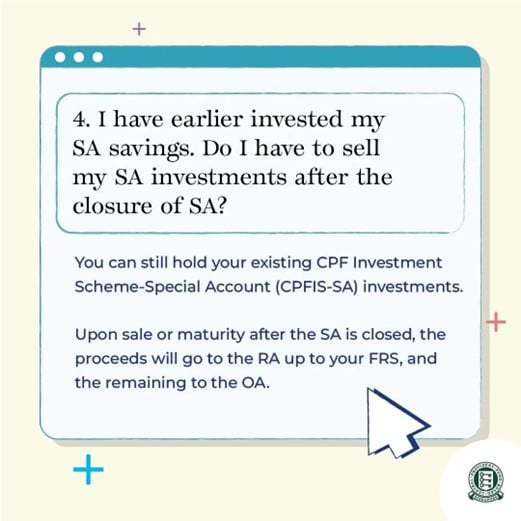

And if you have invested your CPF-SA money, once you sell those investments, the proceeds will go into the CPF-RA (up to the FRS).

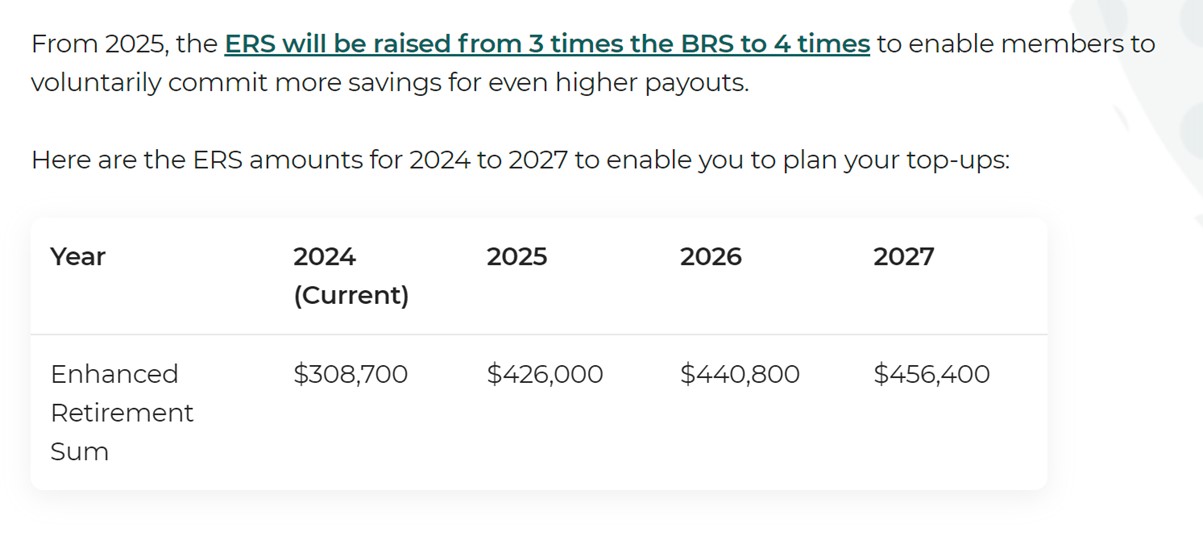

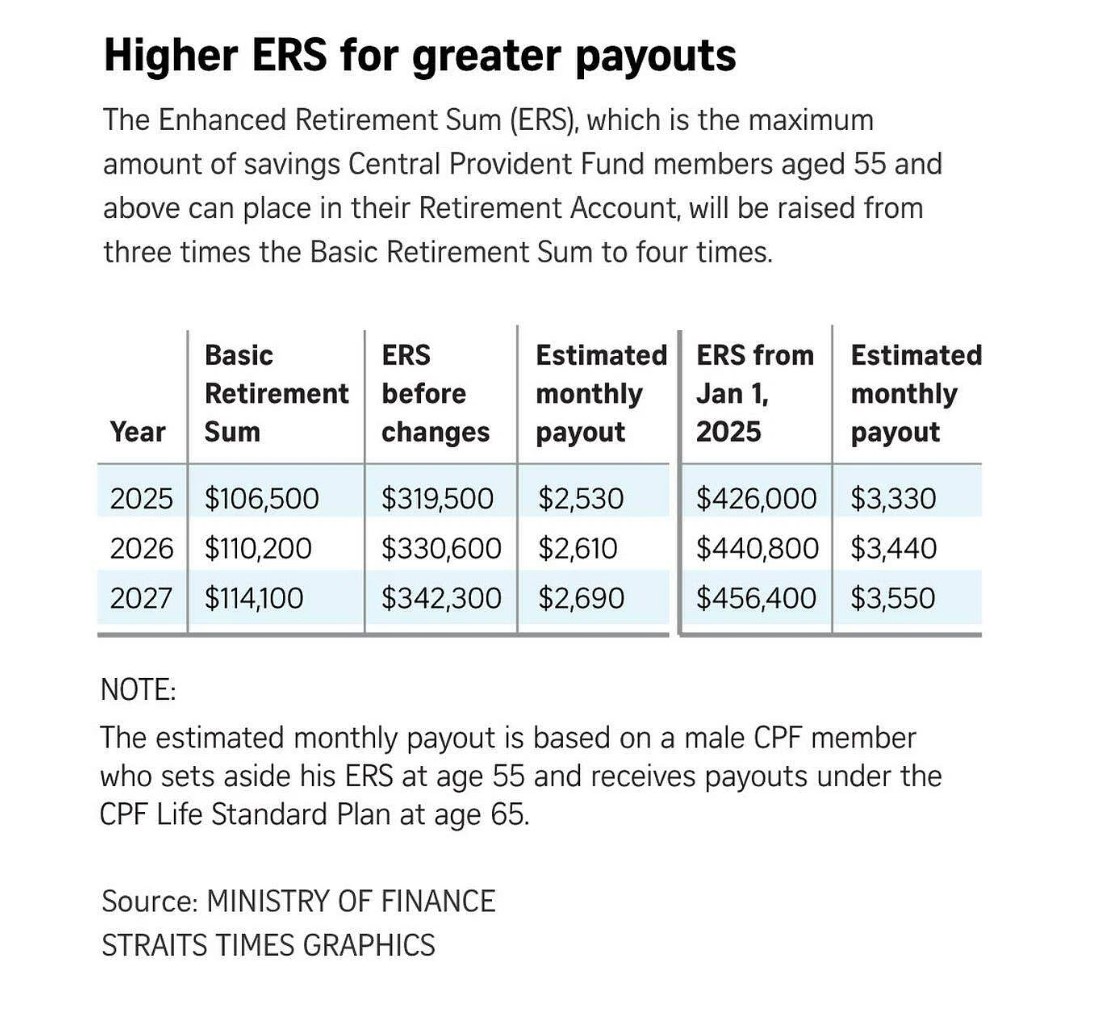

2) Enhanced Retirement Sum (ERS) raised to 4 times the Basic Retirement Sum (BRS)

Which brings us to the next big change

The maximum amount that you can top up into the CPF-RA.

Is now increased to four times the Basic Retirement Sum (BRS), from three times currently. That means the ERS will be $426,000 in 2025.

Choices at age 55 for CPF members after the change?

After this change, there are basically 2 choices at age 55.

You can top up CPF-RA to the Enhanced Retirement Sum (ERS). The money in CPF-RA will earn 4.08%, but cannot be withdrawn, and can only be paid out via CPF LIFE.

Or you can top up CPF-RA to the Full Retirement Sum (FRS) only, and let the rest go into CPF-OA earning 2.5% (which can be withdrawn any time).

Which is the “better” choice?

Is topping up CPF-RA to the ERS a good choice? Note this is a one-way transfer

To answer this question, we need to understand how CPF-RA works.

The way it works, is that any amount transferred into the CPF-RA cannot be transferred out.

This is a one-way transfer.

All the amount in CPF-RA will earn 4.08% interest up to age 65.

At 65, the CPF-RA amount will go into CPF-LIFE.

And CPF LIFE will pay you x amount monthly, from 65 until the day you die.

So for example if you top up your CPF-RA to the maximum of $426,000 in 2025.

You will get an estimated monthly payout of $3,330 from 65 until your death.

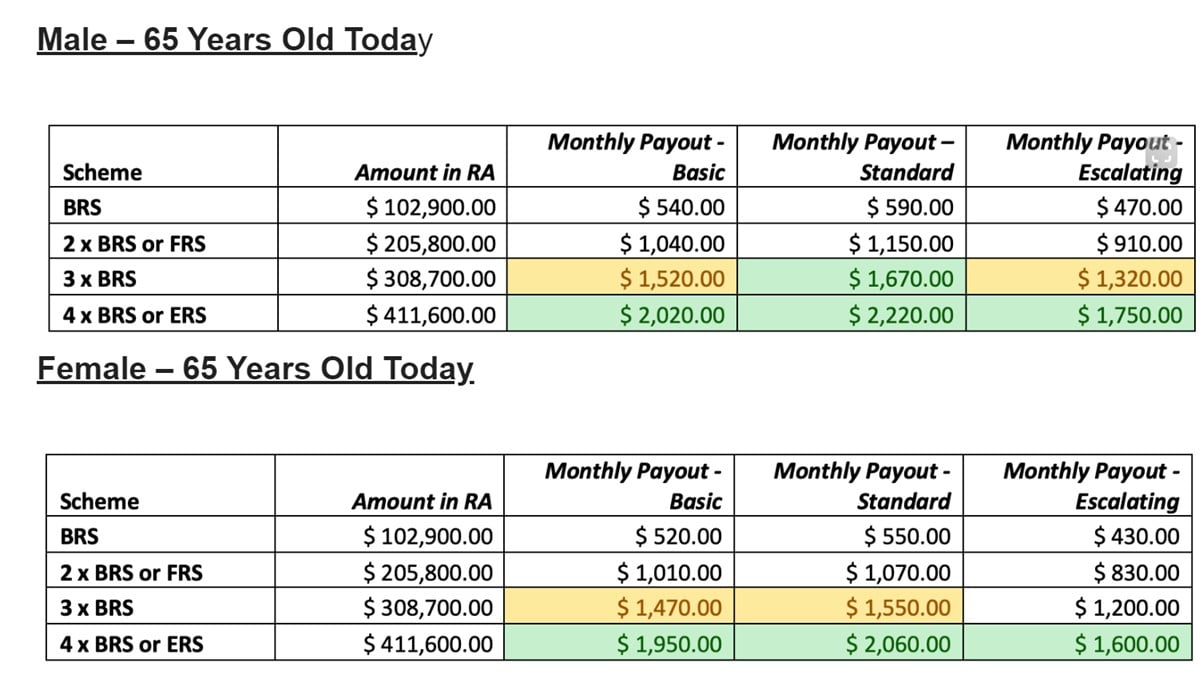

I came across this great table below (from Dr Wealth) that shows the monthly payout amounts based on how much you have in your CPF-RA.

The assumption made is that:

“Based on research from the Lee Kuan Yew School of Public Policy, this number [required to survive in retirement] is $1,421. If we adjust this by 3% inflation every year, the expenses will be about $1,552 every month in 2024.

The minimum amount you’ll need per month should vary from 80% to 100% of this $1,552, so amounts should range from $1,242 to $1,553 in today’s dollars.”

To hit that minimum amount, just the FRS is not enough, and you need to top up to ERS:

How does CPF Life really work? Is it “worth it” to top up?

I came across a really good article published on Dr Wealth that crunches the numbers on how CPF LIFE works, in further detail.

I’ve extracted the key highlights below (views in italics are from the author, and not mine):

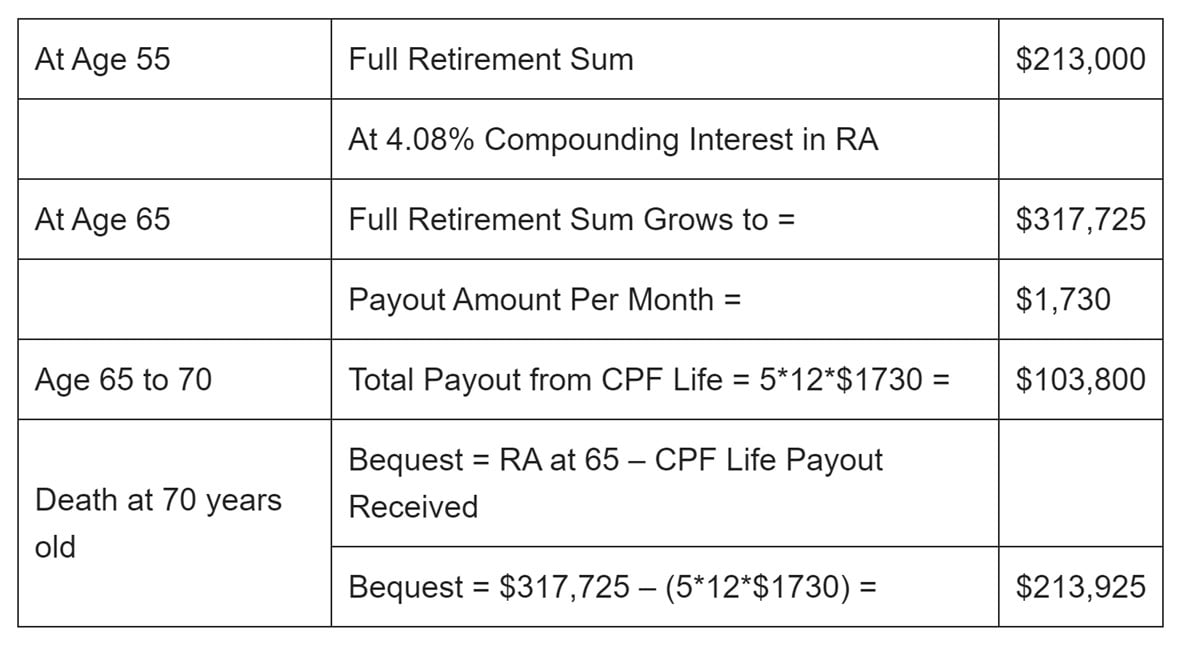

““After you pass away, your beneficiaries will receive your CPF LIFE premium balance, which is the total CPF LIFE premium that you have paid minus the total payouts you have received, together with any remaining CPF savings.

For example, if you paid a CPF LIFE premium of $200,000 and pass away after receiving a monthly payout of $1,000 for 10 months, we will pay your CPF LIFE premium balance of $190,000 (i.e. $200,000 – [$1,000 x 10 months]), together with any CPF savings to your beneficiaries.”

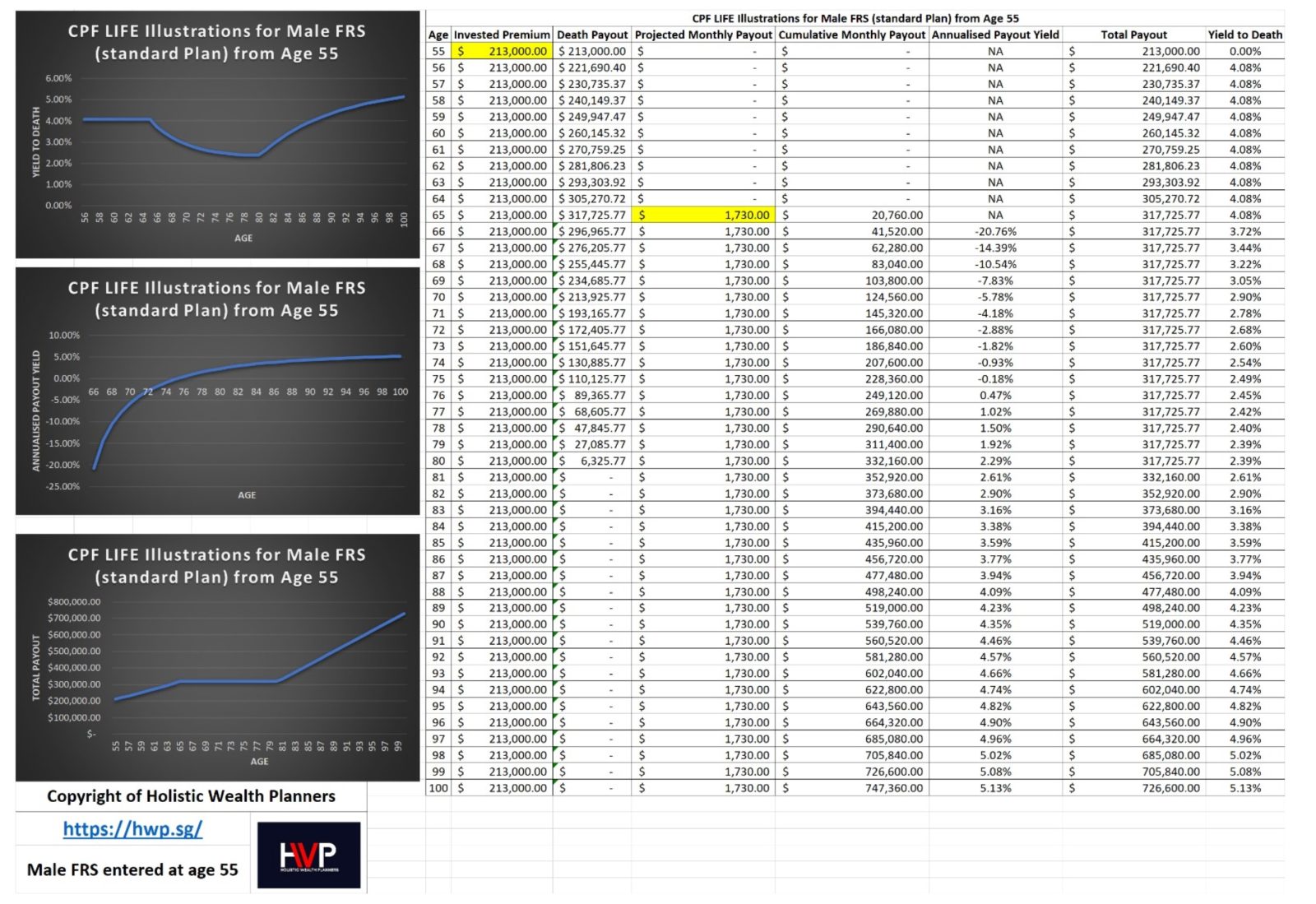

Based on the formula provided, we can calculate the bequest amount for death at 70 years old for a male enrolled in the CPF Life Standard Plan.

You will notice that the total CPF LIFE payout ($103,800) + bequest ($213,925) is still the same as the RA amount at age 65 ($317,725)….

You may ask, does this mean that the $317,725 never grows from age 65? Where does the interest go? The interest earned goes to the CPF LIFE pool, the pooling interest is the concept of annuity, those people who have a shorter lifespan, unfortunately, the interest earned will be used to support a lifetime payout for those people who live longer…

…

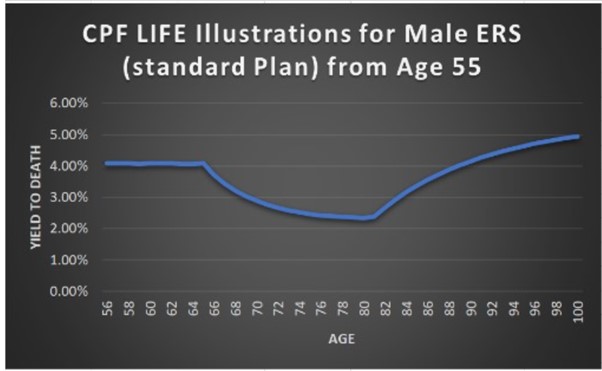

- There are two yields in the image. The annualized payout yield calculates the return based solely on the CPF LIFE payout, excluding the bequest. This is useful for people who are just looking at how much they will receive from the RA savings as bequest payout is not for them. Yield to death is the total return including CPF LIFE payout and bequest.

- Based on the annualized payout yield, the breakeven point where you get back the same or more from CPF LIFE than your RA savings invested at age 55 is around age 75 or 76. If your lifespan is shorter than this age, you will be losing money if you do not take the bequest into consideration.

- The worst age to die is age 80… Yes, you heard that right. The reason is that from age 65 to age 80, the bequest payout decreases by the amount that you received from CPF LIFE. The total payout for CPF LIFE + bequest remains constant until around age 80. Your yield to death at worst could be just 2.27%, this is worse than the OA account!

- Before age 65, if you pass on, you don’t get any single cent for yourself. This is obvious as you cannot touch RA before age 65. So, it’s critical to ensure that you have sufficient savings for yourself before age 65.

- You need to live until age 88/90 to see the 4+% yield. This is critical. Don’t just decide to go all in to RA to the ERS just because RA is giving 4.08% – you may end up only seeing a 4+% return after age 88/90!

- If you live long enough, you can get 5+% from CPF LIFE. This is because you will receive CPF LIFE for a longer period. So make sure you manage your health and live long enough to outperform 4.08%.”

Which is better – CPF-SA or CPF LIFE?

Very interesting stuff.

I’ve zoomed in on the yield to death chart run by the author above.

CPF LIFE is basically an annuity.

The way annuities work, is that they pool the funds together, and everybody gets a payout from the common pot until they die.

Logically, this means that the longer you live, the more you “make” from CPF LIFE (higher effective yield).

Whereas if you die before a certain age, then technically you “make” less from CPF LIFE (lower effective yield).

You can see the effective yield charted above.

To be absolutely fair though, this is how annuities are supposed to work.

They are meant as an “insurance” for the scenario where you live longer than you expected and are running out of retirement funds.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

My view – CPF SA vs CPF LIFE… are just different?

The author’s conclusion after the analysis above, is that:

“In summary, having a CPF SA is definitely better than RA as SA 4.08% is real and you can use it anytime. RA 4.08% is on paper only; you should look at CPF LIFE return to decide if you want to leave your excess SA to OA or top up to RA to the ERS.

So, will you do FRS or ERS after reading this article? For me, I will go for FRS, but I still have about 20 more years to hit age 55; by then, CPF rules may change again, and this is the biggest risk for CPF.”

Frankly I’m not sure if I agree with this.

The way I see it, they are different instruments, with different objectives.

CPF SA is good in that you know any money you put in will pay 4.0% risk free, and can be withdrawn any time.

CPF LIFE is good in that it is an annuity.

If you for some reason luckily (or unluckily) live to 120 years old.

You will continue to receive the monthly payout all the way to 120, which makes CPF LIFE and amazing return on investment.

Whether CPF SA or CPF LIFE is better, depends on what you want in an investment.

That said, I can see why some investors are up in arms

That said, I can definitely understand why some investors are up in arms.

If you had been planning your investment strategy around the fact that you would have a 4.0% yielding risk free instrument with instant liquidity after 55.

Well, that plan has gone out the window now.

BT ran an article on it this week.

The example given, was that if you are 55 with $200,000 in your CPF-SA (after FRS) – before this you could have withdrawn $3,000 a month at 3% inflation for 5.7 years.

Now that CPF-SA is closed and the money goes into CPF-OA?

This will only last 5.5 years.

And of course, the longer the period you stretch, the bigger the impact.

What are the implications for investing? For Singapore Investors?

As I thought about it, it came down to 2 key implications:

- Policy risk with retirement plans – expect the unexpected

- Learning to invest?

Policy Risk with retirement plans – expect the unexpected?

When you are investing for the long term, say a 20 – 30 year period.

You have to recognise that the world will change over a long period like that.

Things that make sense today, may not make sense in 20 years time.

So when you’re investing for retirement over such long periods.

It’s prudent to at least bear in mind the possibility that what seems certain today, may change over a long time period like that.

It’s something we are familiar with as investors, and a similar mindset should be applied to all investments.

Learning to invest may be inevitable

As much as I hate to say this.

I don’t think CPF should be viewed as the ONLY option for retirement.

The general recommendation is to not have more than 20 – 40% of your net worth in annuities.

CPF LIFE should be viewed as an annuity, to hedge the scenario where you live longer than expected.

The rest of your net worth can then go into a mix of income generating assets such as:

- Dividend stocks

- REITs

- Government Bonds (Singapore Savings Bonds, T-Bills etc)

- Stocks for capital gains

- Property

Are we able to invest to replace the CPF-SA? To achieve 4% yield risk free from 55 to 65?

Just for discussion’s sake.

Let’s say we wanted to “replace” CPF-SA.

Is that possible with investments available to us today?

T-Bills to replace CPF-SA?

The most obvious option is T-Bills.

6-month T-Bills pay 3.66% risk free, which is close enough to CPF-SA’s 4.08%.

The main risk though is refinancing risk.

The 3.66% yield is only locked in for the next 6 months.

If you are 55 today, do you know where interest rates will go in the next 10 years?

What if interest rates go down to 2.5% in 2025?

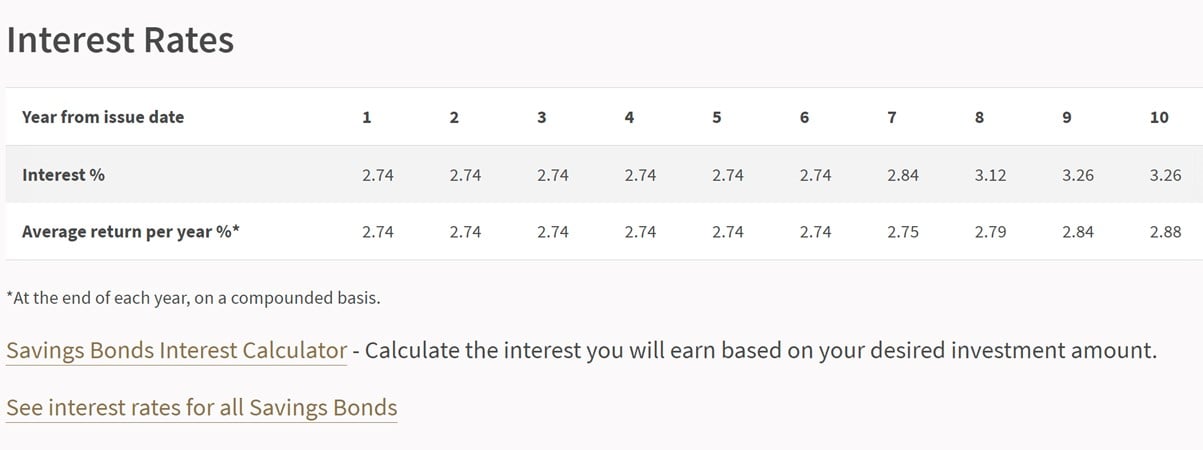

10-year Singapore Government Bond to replace CPF-SA?

You can try to buy a 10-year Singapore Government Bond instead.

This yields 3.11% today risk free, but still falls well short of CPF-SA at 4.08%.

Liquidity is a problem too.

If you want your money back before the 10-year maturity period.

You need to sell the bond on the market.

If interest rates go up, you may be forced to take a capital loss.

That’s quite a lot of risk and complexity as compared to a fire and forget CPF-SA account.

What about Singapore Savings Bonds?

You could try for Singapore Savings Bonds instead.

These can be redeemed any time without risk of capital loss, and are risk free as well.

Problem is that the interest rates for the first few years are not that attractive at <3%.

Dividend Stocks or REITs to replace CPF-SA?

Then we have dividend stocks or REITs.

Let’s say you split the money 50-50 into the 3 local banks, and a bunch of blue chip REITs from CapitaLand/Mapletree/Frasers.

You’re probably looking at a pretty decent 6%-ish dividend yield.

But what happens in the next recession?

What happens when the dividend gets cut?

What happens if there is a risk off and the market value of the shares fall 30%?

No doubt equities deliver higher returns, but that returns come at a cost – being volatility.

Rental property to replace CPF-SA?

What about every Singaporean’s favourite – real estate?

Assuming you have a fully paid off property, you could be looking at anywhere from 3-4% yield depending on the property you have.

That’s actually not too bad.

But rental rates fluctuate over time, and may go lower on renewal.

Maintenance costs are also very real.

And don’t underestimate the amount of work required for an investment property – not everyone may be keen to handle this in retirement.

Closing Thoughts: No real alternative to CPF-SA?

For retirees looking for a replacement for a risk free investment paying 4.0% and has instant liquidity.

There really just isn’t an equivalent out there.

So I can kinda see why investors are up in arms about this.

Although if you think about it, this is probably why this change had to be made as well, as there is no equivalent investment out there that has similar characteristics.

Love to hear what you think though!

Are you impacted by the CPF-SA changes?

Do you like this change to CPF, or hate it?

This article was written on 23 Feb 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

– Get up to USD 3000 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 3000 free shares.

You just need to:

- Fund SGD2000

- Maintain until 31 March

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

So nothing has changed except the high yield savings account interest pays 2.5% instead of 4%,

Any change to the mechanism?

No, pretty much as you said. CPFSA is closed, the money goes to CPFOA which pays 2.5% instead of 4%.

And you can now top up more money into CPF-RA/CPF LIFE if you choose to.

I think the best thing is for everyone to write a goodbye letter on their thoughts and broken dreams so that we can move on and move past the grieving stage

It ain’t coming back guys

Fair enough haha.

Dear FH,

Thanks for another easy to read article. I appreciate it.

Questions:

1) A 50 year old SG citzen

2) Does not intend to use his OA for investment or housing repayment etc.

3) Have already accumlated sufficient funds in the SA account to meet the FRS and do not intend to use SA fund to make any investment etc.

With the change in the policy, does it means that he can transfer his OA to SA to earn the higher interest and treat it like some kind of 5 year SG T-bill (Just that interest are not paid upfront & no possibility to bring the fund back to OA account before he turn 55?

Thanks

Yes – that pretty much sums it up.

Actually even before the change this person could have done the same, and withdrawn from the CPF-SA after 55 (the excess beyond FRS).

I understand that over-55s cannot withdraw top-ups at age 65, so if we top-up our RA from SA, say an amount from FRS to ERS, can that “extra” 2xBRS be withdrawn at 65 ?

No, anything that is topped up into CPF-RA will become part of CPF LIFE at 65, and cannot be withdrawn. Top up into CPF-RA is a one way top up and cannot be reversed.

Thanks for the reply.

Thus, assuming one puts the default FRS at 55, is it right to say that the only thing we can extract from RA at 65, if we pledge our property, is an amount equal to the BRS at age 55? cos everything else beyong 55 in the RA is considered a top-up ?

You can’t withdraw anything from CPFRA – it only withdraws via CPF Life which is the annuity with monthly payouts.

Thus, assuming one puts the default FRS at 55, is it right to say that the only thing we can extract from CPF Life before 65, if we pledge our property, is an amount equal to the BRS at age 55? cos everything else beyond 55 in the RA is considered a top-up ?

Yes, that’s right.

Thanks. Not many people might be aware of this because i have never seen this mentioned anywhere else. Everyone is just talking about topping up to 4xBRS in 2025.

Hi FH,

If our parents have options to choose between CPF Life & Retirement Sum Scheme “RSS”, is the latter better in terms of the Rate?

Trying to think more after your analysis above on how low the yield can be at 2.27 % !

//

The total payout for CPF LIFE + bequest remains constant until around age 80. Your yield to death at worst could be just 2.27%, this is worse than the OA account!

//

They are the same thing actually. Anything you put into CPF-RA will become part of CPF Life. The only way to “opt-out” is to only top up CPF RA to the minimum.

FH, for those born after 1958, we can withdraw an additional amount of 20% of RA at 65, excluding any cash top-ups etc, so does that include the property-pledged BRS drawdown ?

Basically, my question is if we can then draw down an amount equal to one BRS or 1.2x BRS ?

Thanks.

I believe this is included, so the max is only 1 BRS. But suggest just to confirm with CPF on this, they can advise specifically for your scenario.

You can have a look at this link – it explains how much you can withdraw in each scenario: https://www.cpf.gov.sg/member/faq/retirement-income/retirement-withdrawals/how-is-the-withdrawable-amount-computed

Thanks, I believe you are correct. I did read thru the FAQ but it is ambiguous. If we are correct, they should just say so ie the lower of either 1BRS or 20%RA just to be clear

For those reaching 55 this year, no need to consider CPF-SA shielding as SA will be closed in 2025 anyway. But I assume it still make sense to transfer CPF-OA to CPF-SA before Jan 2025 or invest CPF-OA in for higher interest gain.

i suppose it’s better than to T-Bills, short term, to get the additional 1.5% interest.

It depends on your age. If you’re close to 55 it’s probably fine, because the money will unlock soon anyway. If you’re very young you may want to ask if the tradeoff in liquidity is worth it, as you cannot access the money until 55.

If you are very young there is also policy risk in the sense that policy may change again before 55.