In case you missed it – Grab just announced that they will IPO later this year via a SPAC (Altimeter Growth Corp)

I’ve had a lot of requests to write a piece on Grab:

Hi FH,

Grab plans to list on NASDAQ via an SPAC altimeter.

How does this work? If I wanted to buy into the IPO, do I subscribe for the IPO? Or buy the listed SPAC? Do you think GRAB is a good investment?

Know there is a big SPAC craze now but have not read up on the specifics!

Perhaps you could address in one of your blog/patreon posts!

Thanks much in advance!

Lots to cover today, so let’s go!

I’ll split the article into two:

- How does Grab’s SPAC IPO work?

- Is Grab a good investment?

BTW – we share commentary on financial markets every week, so do sign up for our mailing list, its absolutely free (goes out every Sunday).

Don’t forget to join our Telegram Channel and Instagram or (YouTube)!

[mc4wp_form id=”173″]

Part I: How does Grab’s SPAC IPO work?

From Grab:

Grab Holdings Inc. (“Grab”), Southeast Asia’s leading superapp, today announced it intends to go public in the U.S. in partnership with Altimeter Growth Corp. (Nasdaq: “AGC”) in what is expected to be the largest-ever U.S. equity offering by a Southeast Asian company.

The combined company expects its securities will be traded on NASDAQ under the symbol “GRAB” in the coming months.

To sum it up:

- Grab is going to IPO via Altimeter Growth Corp (a SPAC)

- Valuation will be US$39.6 billion

- Plan to raise around US$4.5 billion, with $750 million already raised by the SPAC, and another $4.0 billion to be raised via a PIPE (private placement)

- Sponsor shares (held by Altimeter) will be locked up for 3 years

Why are SPACs good?

SPAC IPOs have been around for a while now, so they are not a new thing.

But they’ve been really hot ever since COVID, for 1 main reason – they drastically reduce the time to market.

With a traditional IPO you need to file a prospectus with the SEC (Securities Commission), answer a whole bunch of queries etc.

This takes around 6 to 9 months on average.

With a SPAC, you don’t have to prepare a full prospectus, and you don’t have to answer so many questions from the SEC.

This significantly cuts down the timeline by about 4 months. With a SPAC, you’re potentially looking at an IPO timeframe of about 4 or 5 months.

When the IPO market is red hot like it is right now, time is money.

You absolutely want to catch the IPO window when it’s open.

Wait another 4 months, and who knows the window may have closed entirely, or you’re looking at significantly reduced valuations.

And with a SPAC, there’s more control over the valuation because it’s agreed on upfront, rather than like a traditional IPO where it’s discussed with the underwriting banks literally right before the IPO.

So companies like SPACs because it’s quick and they lock in their desired valuation, banks like SPACs because they make ridiculous fees in the initial SPAC IPO and subsequent fundraising, and sponsors like SPACs because they make ridiculous fees raising the SPAC.

Big win for all the insiders right?

How do SPACs work?

Forbes has a fantastic article that covers the basics of SPAC, so do read it if you want more details.

I’ve extracted the key parts below:

SPACs are not new—they have been around for a long time and in the past were often referred to as “blank check companies.” A SPAC is a company that initially has no commercial operations and is formed solely to raise capital through an initial public offering (IPO). After the capital is raised and placed into an interest-bearing trust account, the SPAC seeks to acquire an existing privately held company, through what is commonly referred to as a “business combination.”

After a SPAC has raised its financing, it typically has two years to make an acquisition, subject to potential extension if sufficient SPAC stockholders vote to do so. If the SPAC is unable to make a deal within that time period, it has to return the money to its investors and the SPAC’s sponsor loses whatever initial investment it has made.

SPACs usually acquire privately held companies through a reverse merger, and the existing stockholders of the operating target company become the majority owners of the surviving entity. The end result is that the previously private company becomes a publicly traded company (sometimes referred to as a “De-SPAC transaction”).

SPACs offer private companies an alternative to the traditional IPO or direct listing route. SPACs can also allow for some shareholders of the target company to be bought out as part of the business combination.

Grab’s SPAC IPO – Altimeter Growth Corp

Applied to Grab and Altimeter, the timeline goes like this:

- Altimeter Capital Management, the Sponsor, creates a SPAC (similar to how Mapletree will sponsor Mapletree Commercial Trust – the sponsor manages the whole thing and takes up a big initial stake)

- SPAC IPOs as Altimeter Growth Corp (Nasdaq: AGC), raising $750 million

- Identify a target (Grab)

- Get shareholder approval for the deal

- Raise additional $4 billion via Private Investment in Public Equity (PIPE – basically a placement)

- Get regulatory approval

- Complete the merger-IPO

So we are at Stage 3 now. The bolded stuff is what comes next.

Based on usual timelines, it should take about 4 to 5 months to complete the IPO. Which means we’re looking at August – September 2021 IPO if things go smoothly, give or take.

How to invest in Grab’s SPAC IPO?

The rules for a SPAC IPO are slightly different from a traditional IPO.

But if you boil it down to its core, the fundamental concept is the same.

If you’re an insider or institutional investor, you get preferential treatment. If you don’t (ie. Retail investor), you have to buy it on the open market and accept whatever price you get there.

Insiders / Institutional Investors

For insiders / institutional investors, there are 2 options to invest:

Option 1. Exercise a Warrant

If you subscribed to Altimeter Growth Corp at IPO, you are given a warrant.

This warrant gives you the right to buy more Altimeter SPAC shares at $10.

So if you see the Grab deal and you like it, just exercise and buy the shares at $10.

The shares are trading at $12.5 on the open market, so it’s a good deal.

Option 2. Subscribe for the PIPE

Alternatively, you can subscribe for the PIPE – basically a private placement. The price is almost always fixed at $10.

Think of this like the final pre-IPO round, where insiders get to buy into the IPO at a discounted price before it trades on the open market.

The list of committed PIPE are some really big names:

- BlackRock

- Counterpoint Global (Morgan Stanley Investment Management)

- T.Rowe Price Associates, Inc.

- Fidelity International

- Fidelity Management and Research LLC

- Janus Henderson Investors,

- Mubadala, Nuveen

- Permodalan Nasional Berhad

- Temasek.

Insiders buy at a discount

Of course, by now it will be obvious that the insiders are getting a good deal, because they can buy into Altimeter at $10, when then market price is at 12.52 today.

But hey – I’m not the one who makes the rules.

That’s just how the system is set up today. Perhaps in time crypto and DeFi can change all that.

Retail Investor

As a retail investor, there really only 1 option – buy Altimeter Growth Corp on the open market.

So the only thing you can control is the timing of the purchase.

Do you buy it now, and let the insiders exercise at $10 to dilute you?

Or do you wait a while and hope for a better entry price.

That’s broadly the options on the table here.

So to answer the question, I dug around some other big name SPAC IPOs.

Virgin Galactic was a big name SPAC done by Chamath in 2019. Red arrow below marks the listing date

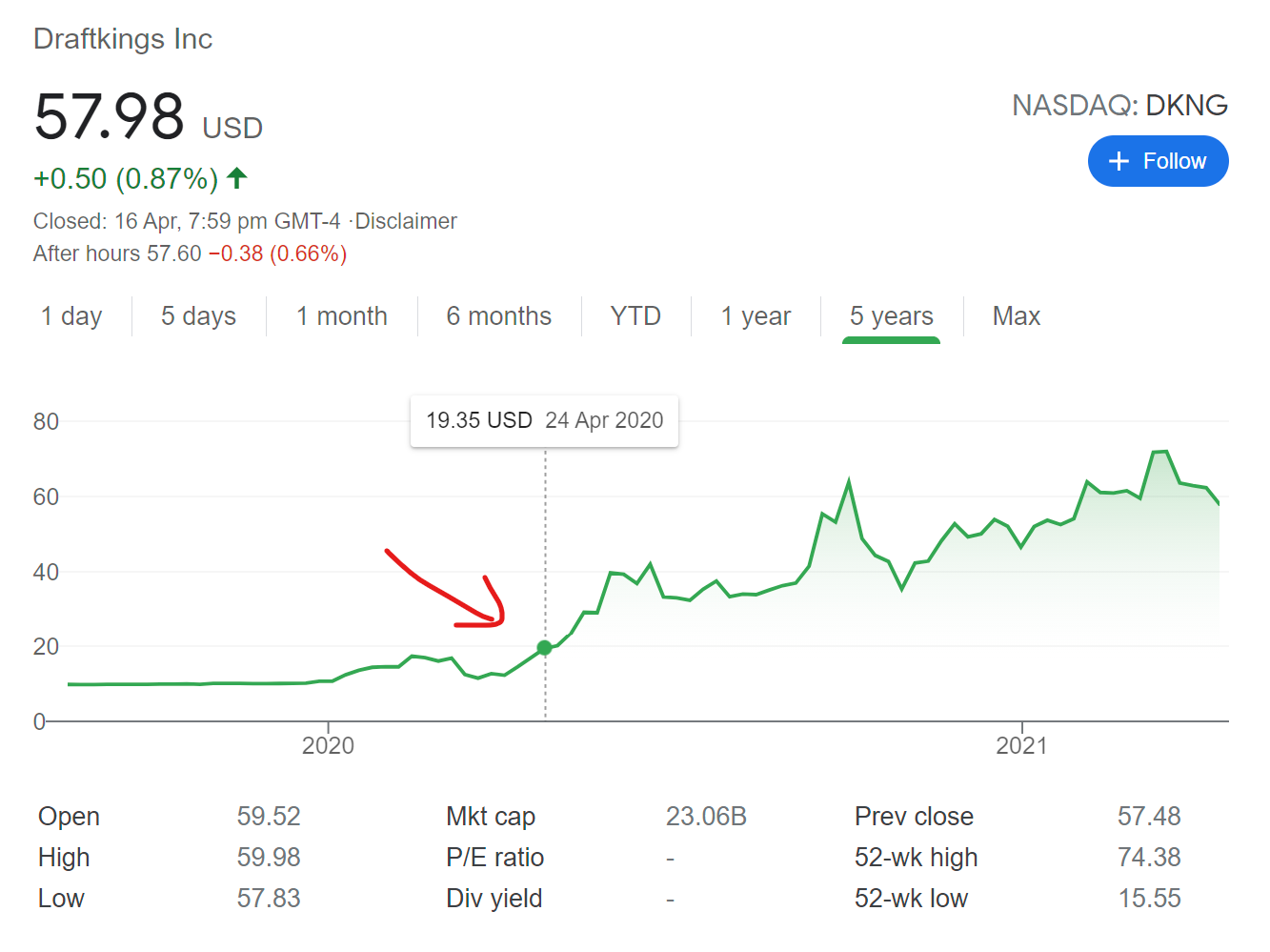

Same for Draft Kings SPAC IPO below:

I also dug around a couple of other big name SPAC IPOs and there’s no clear trend in place.

Basically, my takeaway is that:

- The initial valuation + stock in question + how bubbly the market sentiment is matter A LOT

- Some SPAC IPOs will just tank following the IPO

- But some take off and just keep going up if sentiment around the stock and macro sentiment is very bubbly

So no clear conclusion here.

We need to take a closer look at Grab, the valuations, and the macro context to answer this question.

Part II: Is Grab a good investment?

The official filings for Grab’s SPAC IPO have not been made yet, so we only have access to the investor presentation.

So while I cobbled together a rough analysis based on public info, do understand that this is not complete.

I will be updating this closer to Grab’s official IPO, when more information comes to light.

Grab’s IPO Narrative

I took this from Grab’s Press Release, which says a lot about how they plan to position this IPO (emphasis mine):

Southeast Asia is one of the fastest growing digital economies in the world, with a population approximately twice the size of the United States. Yet online penetration for food delivery, on-demand mobility and electronic transactions are a fraction of the U.S. and China. Across online food delivery, ride-hailing and digital wallet payments, Grab expects its total addressable market to grow from approximately US$52 billion in 2020 to more than US$180 billion by 2025

Grab’s decision to become a public company was driven by strong financial performance in 2020, despite COVID-19. Grab posted GMV of approximately US$12.5 billion in 2020, surpassing pre-pandemic levels and more than doubling from 2018. The company is also currently the category leader in Southeast Asia for its core verticals [5], accounting for approximately 72% of total regional GMV for ride-hailing, 50% of total regional GMV for online food delivery and 23% of regional TPV for digital wallet payments in 2020.

Basically, Southeast Asia is one of the fastest growing digital economies in the world, and Grab is the #1 Superapp in Southeast Asia.

Invest in Southeast Asia, invest in Grab.

Simple stuff.

Grab’s SPAC IPO Valuations

Then we get to valuations, which is a mind blowing US$39.6 billion (SGD$52.8 billion).

For the record, UOB’s market cap is $43 billion, so this would value Grab at bigger than UOB.

This S$52 billion valuation works out to a price to sales ratio of 24.75.

Some comparative valuations below:

|

Company |

Price / Sales Ratio |

Market Cap (USD) |

|

Grab |

24.75 |

39.6 b |

|

Uber |

9.32 |

110 b |

|

Doordash |

15.85 |

45 b |

|

Deliveroo |

5.9 |

6.2 b |

Pretty steep when you look at it as a Ride Hailing / Food Delivery company.

When you look at it as a super app + Fintech play, then maybe the valuation makes sense. So I can kind of get why they would want to play up the Superapp / Fintech angle.

Grab’s Financials

Grab’s financials are really interesting.

2 big takeaways:

- Delivery is bigger than rides

- Projected to turn a profit by 2023

Delivery is bigger than rides

This was interesting for me.

I always thought of Grab as a ride hailing company.

Turns out after COVID, they are now a food delivery company.

2020 food delivery revenue came in at 5.5 billion, versus 3.2 billion for ride hailing.

That’s 49% of total revenue in 2020.

According to Grab’s projections, the delivery business will be the biggest revenue generator until 2023, and they expect it to turn a profit this year.

Projected to turn a profit by 2023

From TechinAsia:

Grab’s EBITDA (earnings before interest, taxes, depreciation, and amortization) loss margin for 2020 was -47%.

For comparison, Uber’s EBITDA margin in 2018 – the last full year prior to its US listing in 2019 – was around -18%.

To reach profitability by 2023, Grab needs to scale its financial services to achieve positive unit economics, while at the same time improve margins on its mobility and delivery units.

Negative 47% margin is crazy talk. You have burning cash and you have burning cash.

Even Uber was burning less cash right before the IPO.

But okay, I get that 2020 was COVID year, and Grab is trying very aggressively to expand into Fintech.

Whatever the case, Grab projects to turn a profit by 2023.

So they have a lot to do from now until 2021 to 2023. Chop Chop.

Strong Founder Control

As with tech IPOs, founder control will be really strong.

Anthony Tan will control about 60.4% of the voting rights despite only holding 2.2% of the company.

Remaining shareholders are:

- SoftBank Vision Fund, which will hold 18.6% of all shares;

- Uber Technologies, 14.3%;

- Chinese ride-hailing company Didi Chuxing, 7.5%; and

- Toyota Motor, 5.9%.

Very strong names.

Will I invest in Grab’s SPAC IPO – Altimeter Growth Corp?

There’s basically 2 decisions to be made:

- Do I want to invest in Grab long term?

- Do I want to buy Grab’s SPAC now?

Do I want to invest in Grab long term?

I think the valuation is very steep.

But hey, Coinbase briefly touched $100 billion this week, so what do I know about valuations in this market.

Grab is going up against 2 fierce competitors: SEA, and Gojek-Tokopedia.

Both are very strong executors.

To justify Grab’s valuation, they really need to show some headway into Fintech.

Personally I’m undecided on this right now, I would want to take a closer look at the further disclosures in the coming months leading up to IPO.

Do I want to buy Grab’s SPAC now?

Personal view – I don’t think there’s much incentive in buying Grab’s Altimeter SPAC right now, unless I think it’s going to fly in the coming months.

But with a $39 billion valuation, and insiders coming in at $10 to dilute the stake, I don’t really see it going that high in the short term unless the tech bubble gets really crazy.

I also don’t think macro will be supportive going forward.

We’ve had a brief respite short term with yields going back down, but I think the broader trend for yields in 2021 is up. And that’s bad news for very richly valued tech companies, with most of their earnings far out in the future.

So my preference would be to let the macro rising yields play out, and let more information come to light as we approach the IPO date.

And then make my decision then.

Closing Thoughts: Is Grab too big NOT to invest in?

There’s another train of thought that goes like this:

Because of how big Grab is, it would be foolish to not invest in it, because everyone else is investing in it.

So if Grab becomes the next Tencent, everyone else gets rich, but if you don’t, so you lose.

If Grab fails, then because everyone is invested in it, everyone else loses money, so you don’t lose more than everyone else.

It may seem stupid, but many fund managers operate on this analysis.

It’s like the Alibaba IPO back in 2014. If you are a fund manager & you don’t buy it and it moons, you get fired because how could you miss out on Alibaba. If you buy it and it tanks, you don’t get fired because the whole industry invested in Alibaba, and nobody saw it coming.

Same for Bitcoin today.

So that’s one way to look at it too. Especially for us living in South East Asia.

But either way, I think there’s no need for me to decide on it now.

Definitely could be wrong, but I personally don’t see the SPAC price running away short term given the macro climate + valuations.

So that gives me some time to let the information from the IPO come to light, and make a decision with more information.

That said retail sentiment is super hot right now, so the price may be very volatile going forward.

But that’s just me though, would love to hear what you think. Are you investing in Grab’s SPAC IPO?

As always, this article is written on 17 April 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Nope, horrible company with atrocious customer service. It’s just a pure money play for the founders to get rich.

Haha, thanks for sharing your views. 🙂

Well…lets just wait for the balance sheet 😛

Curious – why is balance sheet important? From what we know they have about 3b cash on hand, and after the IPO they will have another 4b.

That should be enough for working capital. The execution is what I would be more concerned about.

Can try small

Yeah that’s a fair point.

For me, it’s a wait-and-see attitude. I would like to have a closer look at the company’s financials. Besides the SPAC, it’s said that Grab is considering a dual listing on SGX. What are you thoughts on this potential dual listing (That’s a lot of cash they are raising)?

Sg is such a small market with such low liquidity, and the compliance requirements are not straightforward. If they wanted to dual list Asia then HK would be the natural choice. So it doesn’t seem like a pure business / fundraise decision here.

So there seems to be other reasons in play here, perhaps to play to the Sg Govt or SGX. Maybe some broader strategy to boost SGX’s tech presence going forward.

On the cash part – the more cash they raise the better. IPO window is red hot now, and nobody knows how long that lasts. The more money they can raise to take on SEA + Gojek/Toko, the better for them.

Yes totally agree, execution is key, lowering customer acquisition costs etc. will be important as well. I’m just really interested in the finance side, how many loans are they giving, how much investments they hold etc. Its like a bank without banking regulations, profit margins will be very high, but risks can be high as well

I’m hearing that a bulk of the profits from Fintech comes from the Sg business (because Sg audience is more affluent compared to the region), but still hearsay for now. Let’s wait for more disclosures on this. 🙂

2021 numbers gonna disappoint and the shares will barely go up to less than 30 just basically buy on rumours sell on the news after 1st day another coin base flop

Is no one else concerned that the CEO has only 3% stake with 60% voting power?

Yes, concerns me. Sadly many of the tech deals are structured this way these days.

That’s the truth. Unfortunately that kinda firms get rich. Me – Not going to invest.

Could you Plesse explain to me how the p/s came out to 24.75?

The revenue is 12.5b and market cap 40b.

Yes I was thinking about this too.

The short answer is that the 12.5b is Gross Merchandise Value (GMV), whereas I used the revenue as disclosed by Grab.

It’s debatable whether the correct number is GMV or Revenue, especially for a player like Grab where for food deliveries / drives, much of the GMV will be passed on to the driver / restaurant / delivery person.

I decided to use revenue in the end, but as long as you understand the assumptions in play, I think GMV is perfectly fine too.

Grab , is a company that leveraging on other assets and scale fast.

Not much assets the own.

Yup don’t disagree. Seems to be the new model though – Airbnb doesn’t own any real estate and they’re bigger than most hospitality players. 😉

Thank you

Thank you. May I ask where you got the Information from that the CEO has 3% stake / 60% voting power?

It’s from the Nikkei: https://asia.nikkei.com/Business/Startups/Grab-CEO-takes-60-of-voting-rights-5-take-aways-from-IPO-plan

I think Bloomberg did a story on this recently too.

I think what you said here is critical in regards to short term price action immediately following IPO:

“If you are a fund manager & you don’t buy it and it moons, you get fired because how could you miss out on Alibaba.”

We all know how well SEA did last year. (I 6x my investment in it.) Quit frankly, I think you are naive if you don’t think fund managers are going to push the price upwards in the first 6-8 weeks of the IPO. This is another trend in De-SPAC if you look at their charts. Imo, long term play with shares is great, because everyone seems to be underestimating the Fintech and “Super App” element. The customer acquisition costs and retention are phenomenal plus Grab already insures over 100 million drivers through its Financial services arm and strategic partnership with Chubb, the largest publicly traded insurer in the world. Short term, I think calls expiring Oct 15 are a great play to take advantage of the price discovery phase and the aforementioned fund manager investments, many of which take days or weeks to build up their positions.

I think what you said here is critical in regards to short term price action immediately following IPO:

“If you are a fund manager & you don’t buy it and it moons, you get fired because how could you miss out on Alibaba.”

We all know how well SEA did last year. (I 6x my investment in it.) Quit frankly, I think you are naive if you don’t think fund managers are going to push the price upwards in the first 6-8 weeks of the IPO. This is another trend in De-SPAC if you look at their charts. Imo, long term play with shares is great, because everyone seems to be underestimating the Fintech and “Super App” element. The customer acquisition costs and retention (over 70% with customers who use 3 or more services) are phenomenal plus Grab already insures over 100 million drivers through its Financial services arm and strategic partnership with Chubb, the largest publicly traded insurer in the world. Short term, I think calls expiring Oct 15 are a great play to take advantage of the price discovery phase and the aforementioned fund manager investments, many of which take days or weeks to build up their positions. Call options are a great way to take advantage of this volatility and price discovery knowing full well that the price will drop once the market runs out of buyers. People often say that warrants are like calls but they lack IV and theta, something we can take advantage of as retail investors.

That’s a really good comment, thank you for raising this.

I don’t disagree with you, call option buying could be a great way to play it. Doesn’t even need to be the Oct 15 call only – space it out and buy a bunch of them at different strike prices to maximise the gain.

Lots of upside if things go well, minimal downside if things go south.

Hi there, thanks for the article. I just wanted to ask whether the USD750mn investment from Altimeter is a fixed amount – or would they change accordingly to the AGC market cap? would there be another private placement from AGC to complete the 750mn?

Yes the 750m has already been raised – it was raised when the SPAC IPO-ed. The next round will come when they’re raising the 4b to purchase Grab.

The next 4b comes via PIPE – so a big chunk will be from early insiders who subscribe to the shares at $10 a pop.

Thanks for the reply! I have a follow up question if you don’t mind – so what would happen to the current AGC spac shareholders? Seeing the current trading price is at $11.32 and they only issued 50,000,000 shares priced at $10 initially, where does the rest of the money comes from?

Mostly raised via the Private Placement. So the people who bought the initial 50m shares each get a number of warrants. This allows them to exercise the warrant to subcribe for additional shares at $10.

So to raise the additional financing, the SPAC shareholders will exercise the warrants to subscribe for additional shares. If not enough shareholders subscribe, then it will be raised via a private placement to new investors.

Hi Fh,

With Altimeter trading at $10, would you think it’s a better time to get in on the Grab bandwagon as opposed to 2 months back when it was trading at $12.50?

Thanks!

Hi FH, just wondering, let’s say I buy 100 shares of Altimeter, does that mean I only get 100 shares of Grab once the deal goes through? Or I only buy 1 share of Altimeter and get the option to buy as many shares of Grab once IPO? Thanks!

No it should be the former – 1 share of Altimeter into 1 share of Grab.

You only get the second approach if you participated in the SPAC IPO – which is really only open to institutionals and insiders.