After last week’s article on the dividend investor looking to invest $500,000.

It got me thinking.

The investor had about $500,000 investible assets to deploy.

Let’s say the situation were different, and the goal is to:

- Achieve the highest total returns (whether its dividend yield or capital gains)

- For a reasonable amount of risk

- As an active investor

How would the portfolio look like instead?

In fact – if this were me, with $500,000 to invest in today’s 2024 market.

How would I go about investing that money?

How I may invest $500,000 as a Singapore Investor in 2024?

If you’re an active investor, you do need to have some kind of view on how you think the next 12 – 18 months will play out.

Sure, you may be wrong, and you won’t bet the whole house on the view.

But you do still need to have a view.

What are the possible macro futures that I see going forward (next 12 – 18 months)?

The way I see it, the 2 highest probability futures I see are:

- Economic slowdown due to higher interest rates, OR

- Resurging inflation due to interest rate cuts / higher fiscal spending

It all comes back down to how Yellen / Powell react in an election year.

If they keep monetary policy tight in an election year, I could well see (1) playing out, followed by panicked rate cuts when the economy does slow.

If they ease monetary policy too soon, I could well see (2).

This week saw the European Central Bank and Canadian Central Bank cut interest rates despite inflation staying sticky.

As we head into the second half of 2024, it’s not hard to see US policy makers making a similar mistake.

And based on latest poll it looks like Trump has a good chance of winning the Nov elections.

If so – he’s going to spend a lot of money, cut a lot of taxes, and that’s going to set inflation on fire during his next term.

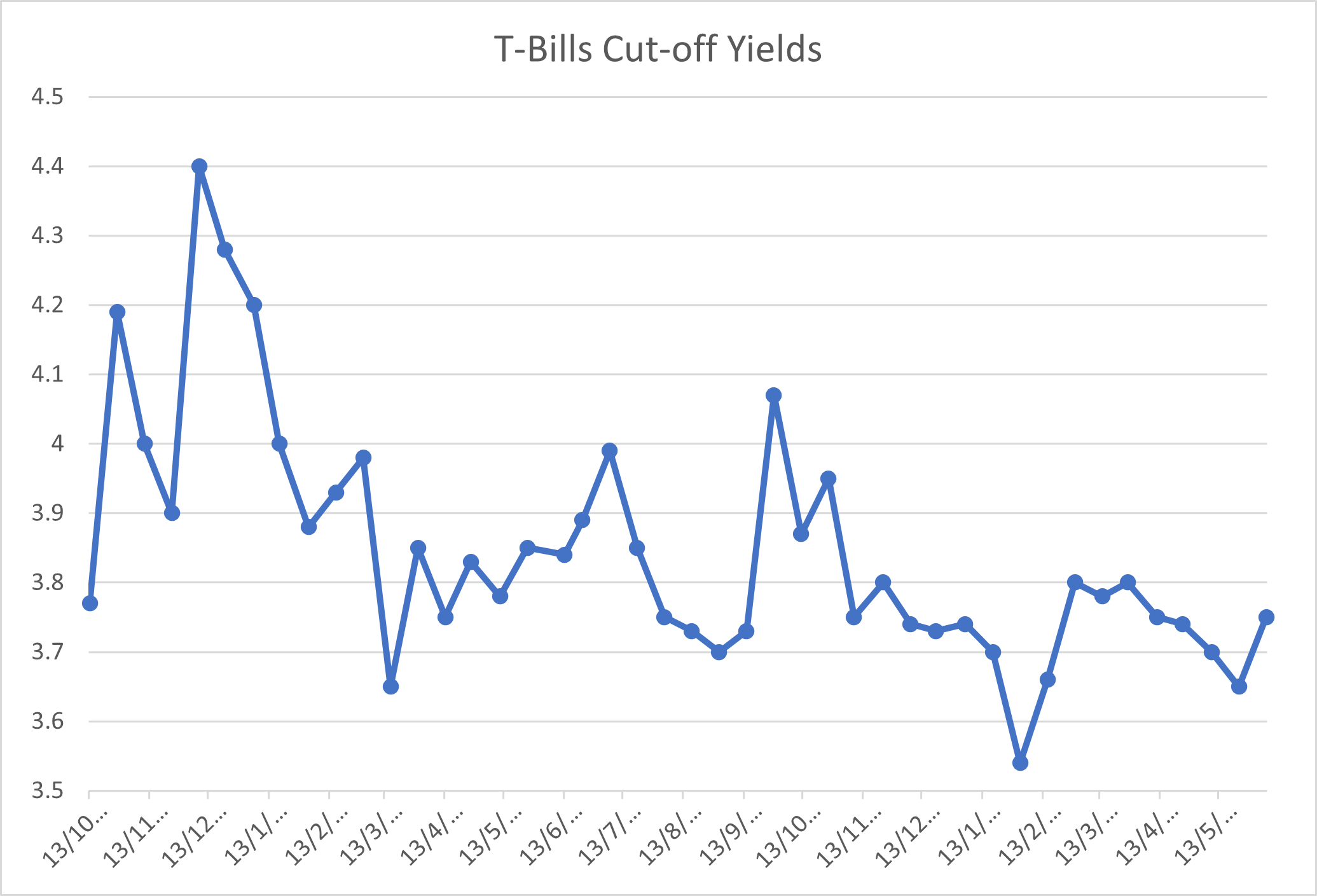

In a climate where cash yields are high and risk free – Ask yourself how much cash it makes sense to hold

As many of you have pointed out, in a climate where cash yields almost 4% risk free (3.76% on the latest T-Bills).

A big question every investor needs to ask is – how much cash to hold vs invest.

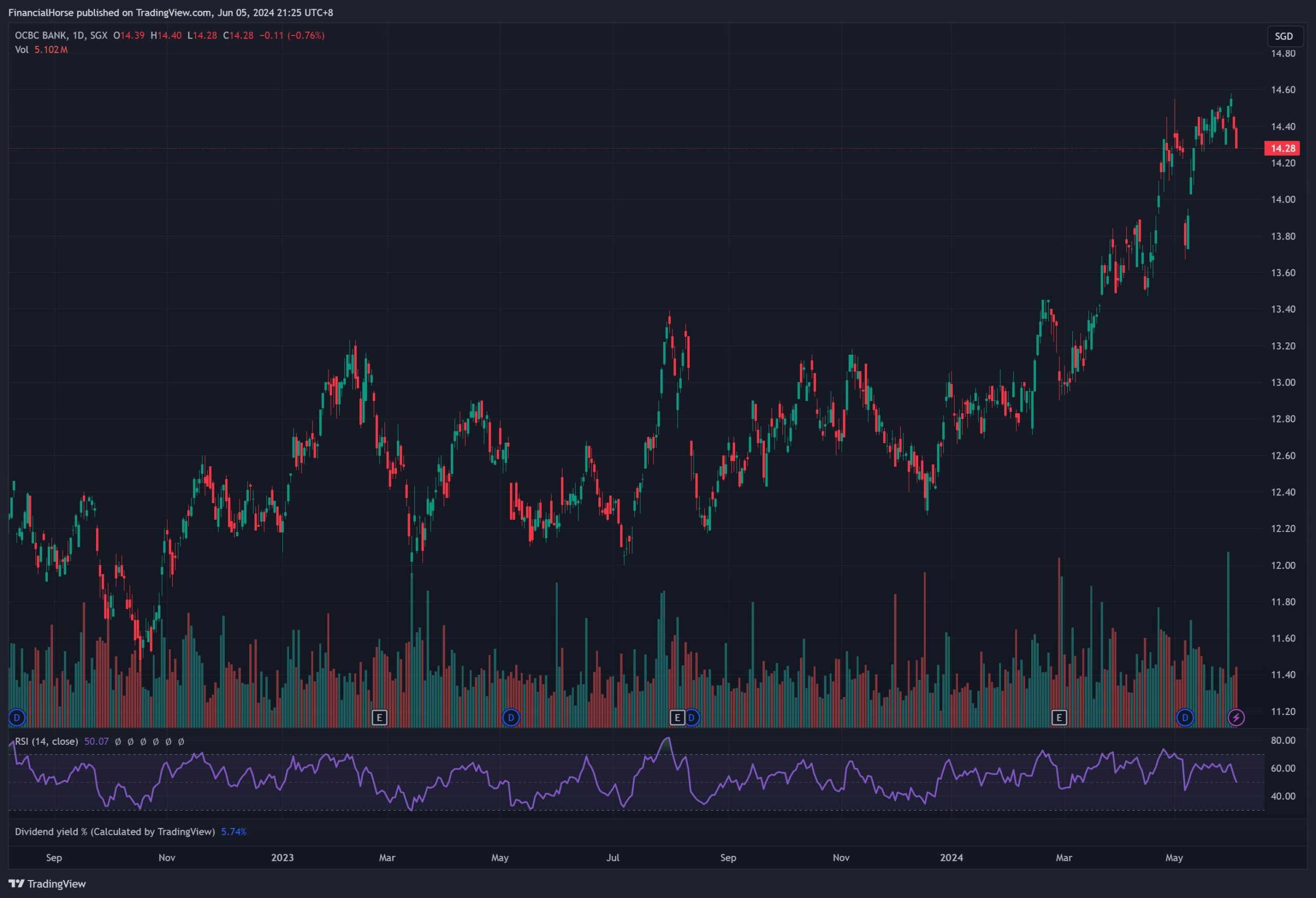

Sure, a 5.7% dividend yield on OCBC Bank looks nice and all, but don’t forget that’s only about a 2% yield premium vs a risk free 6-month T-Bill.

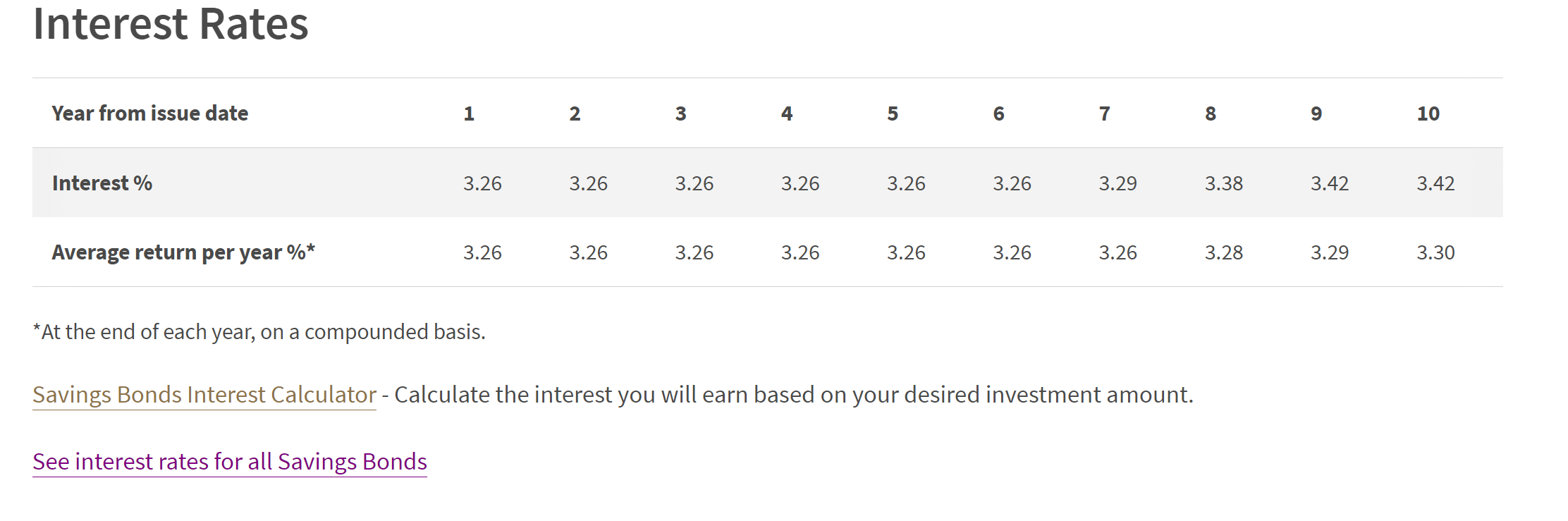

And if you think 6-month T-Bills are too short a duration.

This month’s Singapore Savings Bonds let you lock in a yield of 3.30% for up to 10 years.

Completely risk free, that can be redeemed any time.

How much cash would I hold today for my investment portfolio?

Ultimately – there is no right or wrong here.

Each investor needs to answer this for themselves.

So for purposes of this article, I’m going to keep it simple.

I’m assuming the cash has already been set aside.

And after leaving aside the necessary amount of cash, we have $500,000 left to invest.

How much REITs to buy?

Let’s start at the top with every Singapore Investor’s favourite asset class (or should I say ex-favourite).

REITs.

I know that REITs have fallen out of favour of late, to be replaced by banks.

But call me old fashioned – I think there is decent risk-reward if you’re selective about which REITs you buy.

Do REITs offer attractive risk-reward today?

If we go back to the 2 macro futures above.

I think the economic slowdown scenario could be pretty good for REITs – as it will result in lower interest rates.

Yes rental and occupancy rates probably suffer.

But the reprieve from the lower interest rates probably offsets the lower rentals – it’s basically the past 18 months in reverse.

What about the inflationary scenario?

That said, in the inflationary scenario REIT probably aren’t going to do well, as interest rates would stay high in this scenario.

But after the sell-off in REITs, many of them are at a price where even if interest rates stay at current levels you probably won’t see a lot of downside (after factoring in dividends).

How much of the investment portfolio would I allocate to REITs?

I would probably allocate about $100,000 to $150,000 to REITs in this portfolio.

I would focus on REITs that:

- Hold primarily Singapore properties

- With a strong balance sheet

- Decent sponsor

I want to keep this article high level and not talk about individual REITs – so for those who are keen you can see the REITs I am keen on in the FH REIT / Stock watchlist on FH Premium.

Note that US 10 year interest rates seem to have topped since the Treasury and Fed announcements in early May.

If so, this could be good news for REITs.

Would I buy banks as a dividend stock for this investment portfolio?

Now on banks – I completely get it.

It seems like investors can’t get enough of banks today.

The dividend keeps going up, and share price keeps going up.

It’s the exact opposite of REITs.

But if you go back to the 2 macro futures I set out above.

In the economic slowdown scenario – I don’t think the banks will do particularly well as it means lower interest rates (and possibly higher defaults).

In the inflation scenario – banks will definitely do okay-ish.

But if the price of everything is going up due to global liquidity – you’re going to see much higher upside on stuff like US Tech, Crypto or commodities / gold.

I’m not saying banks are a bad investment, I’m just saying there are other investments out there with more attractive risk-reward profile.

That being said, this probably wouldn’t be a “proper” Singapore portfolio without some allocation to the banks.

I could see myself putting $25,000 to $50,000 in the Singapore banks.

I mean that’s how investing works right.

You could have a very strong view on something. And yet position your portfolio for the exact opposite, just in case you’re wrong.

What is a better way to hedge the “inflationary” macro outcome? Other than buying banks?

Assuming we get the inflationary scenario.

Where the Feds cut interest rates, and Trump wins the elections (and proceeds to spend big).

You may see asset prices jump across the board, driven largely by a depreciation in the value of money itself.

The best hedges in such a scenario are a mix of:

- US Tech / Bitcoin

- Gold

- Commodities

Buy US Tech / Bitcoin as a play on liquidity?

If you want an asset class to bet on global liquidity conditions.

There’s probably nothing better than US Tech / Bitcoin.

Arguably Bitcoin is the purer play because you don’t even know to worry about things like earnings.

Bitcoin is just a pure speculative asset class, and responds almost exclusively to global liquidity conditions.

But I do get that not everyone is comfortable with Bitcoin, from a portfolio perspective you don’t want to be overexposed to Bitcoin (which is a highly volatile asset class).

US tech plays a similar role as well.

The problem with US Tech though is that it’s come down to 7 names at the moment.

All of which have run up significantly, and are quite richly valued.

Yes, I get that we are in an AI Supercycle, and these 7 names are printing profits.

But it makes me very nervous when valuations are this high, and when everyone in the market is piling into the same 7 names.

How much of the investment portfolio would I allocate to US Tech / Bitcoin?

I would probably allocate about $150,000 – $200,000 of the portfolio to a mix of US Tech / Bitcoin.

Personally I do think some allocation to the 7 stock above (and Bitcoin / Crypto) is required, but just how much will depend on risk appetite.

I see better value in the mid cap names at the moment, for example the picks and shovels plays that would benefit if this monster AI capex spending continues to play out (for eg. the memory, connectivity, electricity players etc – see full list on the FH Stock Watch).

Gold as an alternative portfolio hedge?

Gold is similar to Bitcoin in that as an investor – you either love it or hate it.

Some investors think of gold as the only true form of money.

While some other investors think of gold as a barbarous relic.

Me – I’m more practical.

If the price goes up, and I can make money from it, I like it.

The charts for gold’s price are very bullish.

In Feb 2024, Gold price broke above the 2050 support line that goes back to 2020.

And since then it’s blasted as high as $2400 at one point.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

Why is gold price performing so well? Is gold a good investment?

I wrote an article for FH Premium subscribers on gold.

The long and short is that gold (like Bitcoin) is an asset class made for our times.

In an era of unlimited money printing by central banks, unconstrained spending by governments, and a new cold war developing between US and China.

Gold is arguably one of the purest forms of money.

In that unlike USD, nobody can confiscate your gold, or prevent you from transacting in gold.

And nobody can print more gold (unlike USD).

Central banks all around the world have been adding to their gold reserves since the Ukraine war, and this doesn’t look likely to stop any time soon.

The chart for gold is very bullish, and structurally there are a lot of reasons to like gold in the mid term.

I might put $25,000 to $50,000 in gold for this portfolio.

Are China / Japan / India a good hedge for a Singapore investor?

A lot of you have also reached out with questions on China, Japan and India stocks.

I may look to do deeper articles on each of them.

But the long and short is that I think each of them offers interesting diversification from the usual US / Singapore stocks.

China because of the decoupling is on a completely different business cycle from the West, which means there are powerful diversification benefits.

That said China does have a whole host of issues from the real estate situation to US sanctions to political issues.

And the charts show that China stocks remains in a long term downtrend since 2018 when the US-China trade war first started under Trump.

So careful position sizing is required.

Japan is at a point where their interest rates are still stuck at zero when the US is at 5.5%, and they are benefitting from the friendshoring as a US ally.

Valuations wise – Japan is also much, much cheaper than US stocks.

India has powerful demographics going for it, and they also benefit from the friendshoring out of China.

That said the recent “defeat” for Modi was a big blow for his political agenda.

Allocation wise, I might allocate $25,000 to $50,000 to China / Japan / India, mainly as a diversifier to the US / Singapore stocks, while each benefitting from their own structural tailwinds.

Will I buy commodities for my portfolio?

Oil is the alpha commodity, so let’s start with oil.

The problem with oil is that if we have an economic slowdown, you may see demand drop.

And yet on the supply side – oil’s price has been largely kept in the $80 range because of OPEC+ supply cuts.

Which leads to a scenario where there isn’t a lot of upside if supply cuts continue and demand stays at these levels, but a fair bit of downside risk if things go wrong.

Because of that I took profits in my oil positions recently in my personal portfolio (weekly updates shared on FH Premium), and redeployed them elsewhere.

Ultimately for commodities – I do want some exposure, but I won’t overdo it.

Probably about $25,000 to $50,000 exposure to commodities.

And it won’t all be oil stocks, I would throw in some uranium or copper stocks in there as well, being commodities that I am bullish on in the mid term (exact names on FH Premium).

It’s a good diversifier, with lots of mid term structural tailwinds, and could do pretty well in an inflationary scenario.

How I may invest $500,000 as a Singapore Investor in 2024?

To sum up, this is what the overall asset allocation looks like.

The numbers are in ranges to give flexibility to play around in practice:

- REITs – $100,000 – $150,000

- Singapore Banks – $25,000 – $50,000

- US Tech / Bitcoin (or crypto) – $150,000 – $200,000

- Gold – $25,000 – $50,000

- China / Japan / India – $25,000 – $50,000

- Commodities – $25,000 – $50,000

And again, this article is meant to be high level so I have not gone into individual names.

You can see the full list of names on the FH Stock / REIT Watchlist.

Do also note that the above may not be indicative of how my personal portfolio is positioned. You can see my full personal portfolio shared on FH Premium.

This article was written on 7 June 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

WeBull Account – Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

think you are too conservative. I am going to DCA semi as long as they continue to post good earnings.

Why commodities? Over long-term tech always outperforms all other sectors. Have you seen commodity 10x, 100x? Only US tech can be multibagger. Commodities, country ETFs , REITs nah…

Sg stock: the only investible right now is DBS. I think we are in sticky inflation. REITs 6% dividend is not even worth it.

Over long-term the only market that can truly make you rich is US stocks.

Other markets are quite dead.

By semis you mean NVDA or the whole basket of semi stocks?

I completely get where you’re coming from for the record. These days, investors have been conditioned to think that US stocks are the only game in town, and the results back that up!

My only concern is that what happens when one day this no longer works. Would investors be able to exit quickly enough? But I don’t deny that for as long as the music is playing, US tech / semis is the place to be.