So I received this really interesting question from a long time FH reader:

“Hi FH,

Hope you’ve been well!

We were hoping to pick your brains again. 😅 We recently sold our primary residence and freed up some funds which we would like to deploy into our stock and reit portfolio (up to $300,000) perhaps more geared towards creating passive dividend income. We were wondering if you could have a look at our current portfolio and provide some broad thoughts about how we should proceed?

A bit of background – we are a couple (ages 40+) without children and no plans for kids in the future.

We understand that a lot of our portfolio is currently capital gains geared but that is why we’re looking to focus more in the next few months/year on creating dividend income. But ultimately, a balanced portfolio is what we want to work towards that will eventually give us around $4-5000/month or more for retirement.

Our existing portfolio is about $200,000+.

P.S. Sorry, forgot to add that these are some stocks we’re currently considering purchasing/purchasing more of:

REITs

- MPACT

- Starhill global reit

- Ascendas REIT

Stocks

- AMD (US Semiconductor)

- Digital Ocean

- Cloudflare

ETFs

- Global X Copper Miners

- China Tech ETF (KWEB)

- MSCI Japan ETF (EWJ)

- INDA ETF”

What stocks / REITs are in the Singapore investor’s dividend portfolio today?

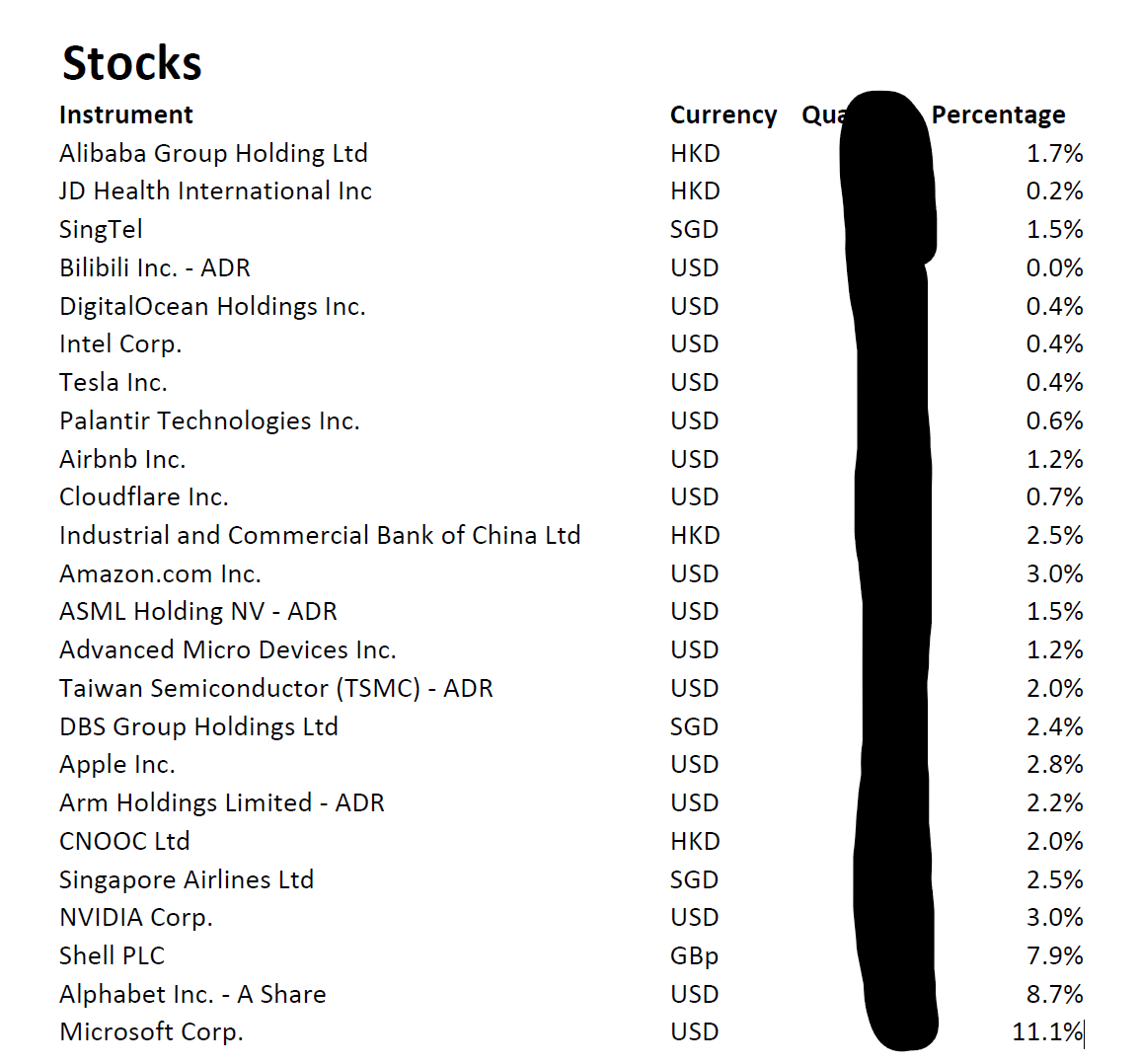

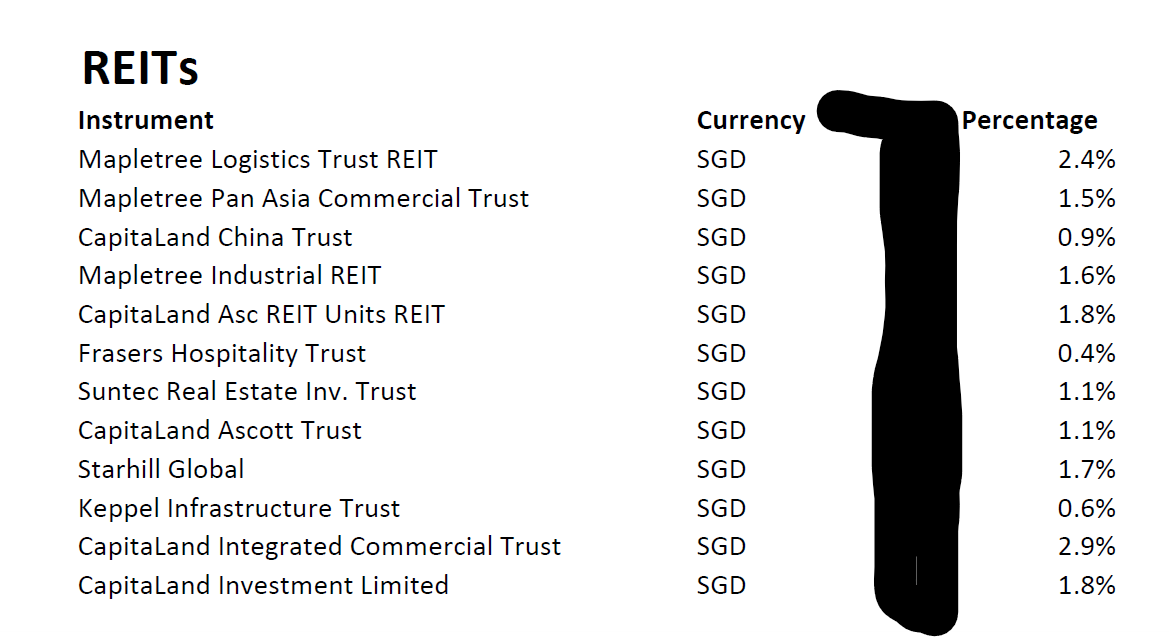

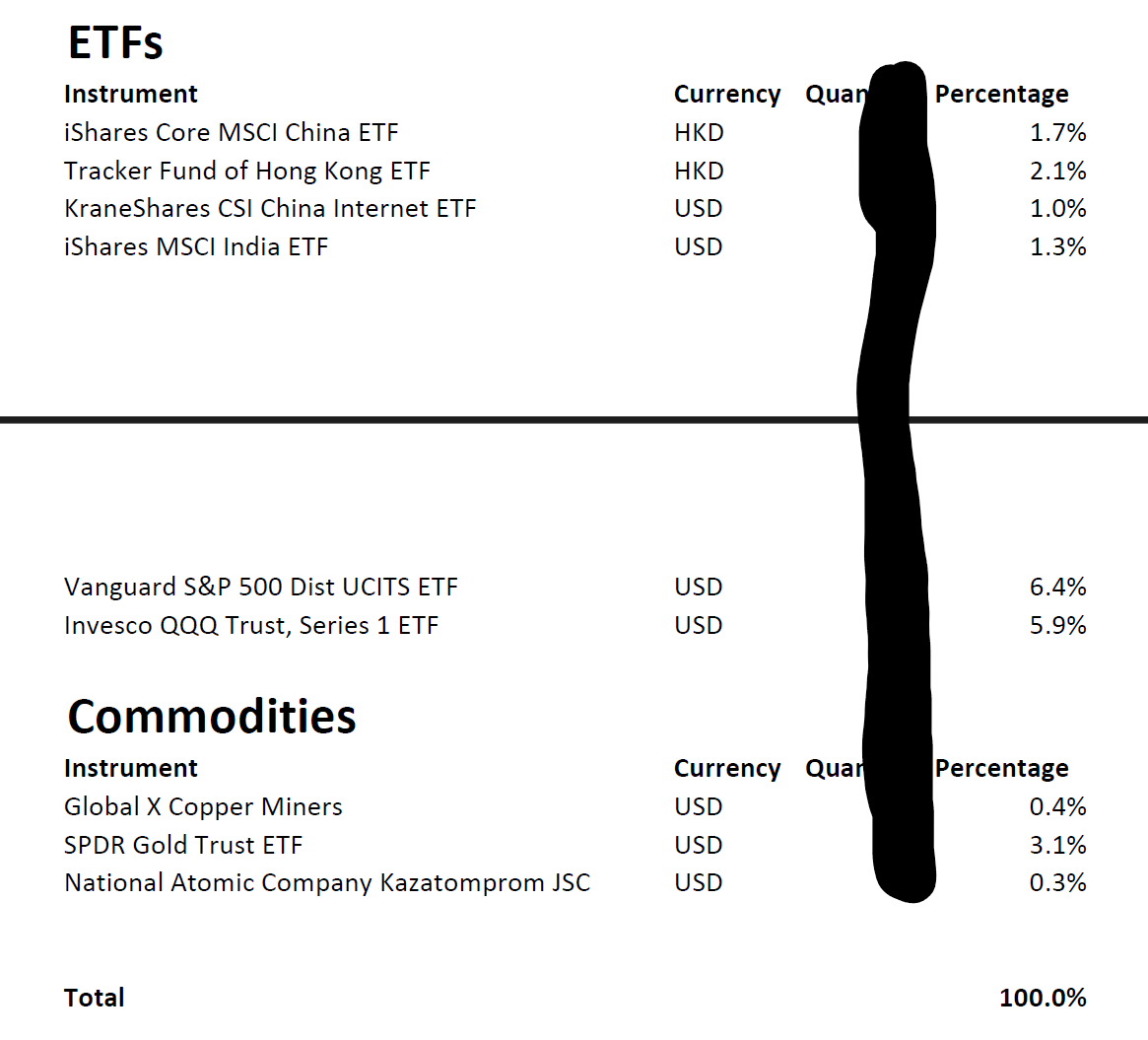

I’ve extracted the portfolio list below.

For privacy reasons, I have blocked out the quantity details.

60% of the dividend portfolio – US, China, and Singapore stocks

60% of the portfolio is invested in US, China and Singapore stocks.

The bulk of this (40% of total portfolio) is US tech stocks.

Followed by energy at 8% of the total portfolio (Shell).

China makes up 4.4% of the total portfolio.

Interestingly for a dividend portfolio, Singapore stocks are on the low side at 6.4% (Singtel, DBS, Singapore Airlines).

18% of the portfolio – Singapore REITs

As you would expect for a dividend heavy portfolio, there is a healthy allocation to Singapore REITs.

18% of the portfolio is allocated to REITs.

You can see the names below, they are fairly standard blue chips from Mapletree and CapitaLand.

18% of the portfolio is ETFs, 4% of the portfolio is Commodities

Another 18% of the portfolio is invested in ETFs.

The bulk of it is US ETFs (the usual S&P500 and NASDAQ – making up 12% of the portfolio).

The rest is China and India ETFs.

Finally, there is 4% allocation to commodities, the bulk of which is gold.

Sharing my high level views on this Singapore Investor’s dividend portfolio

I know there is a lot of detail above.

So I’ll try to keep my comments high level and simple.

3 big comments from me:

- Current Portfolio is heavily weighted towards capital gains plays (60%) – for a dividend portfolio

- Portfolio is too small to get $5000 a month dividend income (without taking excessive risk)

- For a dividend portfolio, this is underweight Singapore banks and overweight REITs

Current Portfolio is heavily weighted towards capital gains plays (60%) – for a dividend portfolio

The biggest comment that I had.

And one that the reader pointed out as well.

Is that this portfolio is heavily weighted towards capital gain stocks.

Looking at the portfolio, almost 70% of the portfolio is capital gains plays:

- US tech stocks

- US ETFs

- Commodities

Meanwhile, only 30% of the portfolio is invested in Singapore dividend stocks, being the:

- Singapore REITs

- Singapore stocks

- Oil stocks

So if the goal is dividends, I’m not sure if the current portfolio achieves that goal.

Capital Gains Portfolio vs Dividend stock portfolio – which is better for a Singapore Investor?

But let’s take a step back.

Why are Singapore investors so in love with dividends?

Conceptually it shouldn’t matter to you as an investor whether you make money from capital gains or dividends right?

If you make 10% on Amazon, you can just sell 8% of that to get an 8% “Dividend Yield”.

Money is money, it doesn’t matter if it comes from capital gains or dividend yield.

But… that leaves out the emotional side of dividend investing

That said, the above is from a theoretical perspective.

It doesn’t take into account the emotional side of dividend investing.

Dividends are sexy because you don’t need to lift a finger (to sell the stock).

You just buy and hold, and every quarter you get a nice chunk of money in your bank account, without having to monitor the price or sell any stock.

It kinda feels like “free money” – I get it.

With capital gains stocks, you need to sell stocks to realise the “dividend”

Let’s just give a simple example.

If you have $100 in Amazon, and you’re looking for $8 “dividend yield” a year.

If the price doubles to $200 – you’re in luck, now you only need to sell 4% of the portfolio each year.

But what if the price halves to $50?

Now you need to sell 16% of the portfolio just to achieve the $8 dividend.

That’s not sustainable, and it won’t be long before you’ve sold all your stock.

So capital gains you need to actively monitor share price, and make those buy/sell decisions to realise the dividend.

How do you know which stock to sell and when?

It’s messy, and I get the appeal of dividend stocks.

The problem with dividend stocks – by its nature they are mature, slow growth companies

The problem with dividend stocks though.

Is that a company only pays a dividend when they cannot find a better use for the cash.

If a company is growing revenue 30% year on year, you bet they would be using that spare cash to reinvest in the core business.

So if you build a dividend portfolio, by its very nature you are self-selecting for a list of mautre, slow growth companies.

And in many cases, it’s not like dividend stocks are “safer” than capital gains stocks.

Remember names like Singpost?

Once a favoured dividend stock, share price has collapsed 75% from its peak:

Or Singtel – down 45% from its highs:

Don’t forget the risk of a dividend cut?

And don’t kid yourself that the dividend is sacrosanct.

Back to the example above.

If Amazon share price halves – chances are good we are already in some kind of global recession.

In that scenario, are Singapore dividend stocks like DBS or CapitaLand Ascendas REIT going to maintain their dividend?

If COVID was any example, we saw quite noticeable dividend cuts in 2020.

So… run a balanced portfolio – own both dividend stocks and capital gains stocks?

I guess what I am trying to say here.

Is that you need to understand what is it about dividend stocks that you like?

And is it worth the tradeoff.

In many cases, the more appropriate solution is to run a hybrid portfolio, similar to what this investor did (although this portfolio is heavily tilted towards capital gains).

For example, a more balanced approach may be something like 50% dividend stocks, and 50% capital gains stocks, to have a good blend of exposure to mature dividend paying stocks, and also high growth stocks.

How to get $5000 a month dividend income in retirement?

Now this dividend investor has a $200,000 portfolio today.

With $300,000 cash to invest further.

This gives a total portfolio size of $500,000.

Assuming that $500,000 is invested at a 6.5% dividend yield (which I think is achievable without taking on excessive risk).

That works out to $32,500 a year in dividends, or $2708 a month.

Given that the investor is looking for $4000 – $5000 dividends a month.

This falls well short of the target, even if you assume 100% investment in dividend stocks.

Portfolio is too small to get $5000 a month dividend income (without taking excessive risk)

Which brings me to the next point.

With a $500,000 portfolio.

To achieve the minimum of $4000 dividends a month the investor wants.

Requires a 9.6% dividend yield.

I don’t want to mince words, but I don’t think that is realistic in this market unless you take on quite a bit of risk.

There are no easy solutions to this one.

Ultimately, there are only 2 options:

- Accept a lower monthly dividend

- Get more money (start with a bigger portfolio)

What would I do with this portfolio – capital gains or dividend?

For what it’s worth.

The reader shared that they are in their 40s, with no children and no plan for kids.

If they plan to continue working

If they plan to continue working until their 50s, that’s a good 10 – 15 years more to work and build the portfolio size.

If so, I would say there’s no need to make drastic changes to the portfolio, and they can keep the capital gains focus.

Keep growing the pot, until they are closer to retirement, then change to a dividend portfolio then.

By then, the portfolio size would be much larger, and possibly able to hit the $5000 a month dividend income target.

If they plan to retire soon

But of course, if the plan is to retire in the next few years.

Hence the urgent need to transition to a dividend portfolio.

Then frankly the numbers don’t really work out, unless they can accept a lower dividend yield (or have a larger portfolio).

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

For a dividend portfolio, this is underweight Singapore banks and overweight REITs

The final point I had.

Is that for a dividend portfolio.

The portfolio is very underweight Singapore banks, and comparatively very overweight REITs.

There’s only a 2.4% allocation to DBS bank, while there is a 18% allocation to REITs.

Are banks a risky play today for a dividend investor?

I get the conundrum.

DBS Bank sits at all time highs today.

Chances are the next move from Jerome Powell is going to be an interest rate cut.

There is significant uncertainty over whether the economy will slow or pick up in the months ahead.

Long story short – we are very late in the business cycle.

At this time, do you really want to run a big allocation to Singapore banks?

For what it’s worth, I get all that.

But I think this consideration is more relevant if you’re running an active portfolio, where you’re actively trying to time and outperform the market (which for the record is the kind of portfolio I myself run – see my full portfolio on FH Premium).

But by its very nature dividend portfolios are not about that.

They are meant to be more passive buy and hold style plays, where you just sit back and get the dividend in your bank account each quarter.

So yes, for an active portfolio a lower allocation to banks may make sense.

But for a passive dividend portfolio, the allocation to banks is definitely on the low side.

Banks provide a pseudo hedge for the rest of the REITs in the portfolio.

If interest rates stay high, the REITs will suffer, but the banks may do well.

DBS Bank pays a 6% dividend yield today, and if you’re building a dividend portfolio today you do need some allocation to banks, the only question is how much.

You can argue that this portfolio doesn’t need much banks because the commodities / oil would hedge a higher interest rate scenario. But then those names pay a much lower dividend yield, so it goes back again to whether you want to invest for capital gains or dividend yield.

What about the Capital Gains stocks part of the portfolio?

Just to share some quick views on the rest of the portfolio.

The stocks component is mostly US Tech and semiconductors, which would have done very well the past year or so.

Frankly I don’t have very much comments on this part of the portfolio – assuming the goal is capital gains.

I might take profit in some of the big caps after their big runup and buy smaller caps (which comparatively have more room to run – see the names I am keen on on the FH Stock / REIT Watchlist).

But we’re probably nit picking at this point.

Owning FAANG + Semiconductors has worked pretty well the past year or so.

Should you run a concentrated or diversified dividend portfolio – as a Singapore Investor?

One final point on portfolio concentration.

A simple trick is to look at your Top 10 stocks / REITs in the portfolio.

Add them all up as a percentage of your portfolio.

This number usually ranges from 50% – 70%.

If you’re on the lower end, your portfolio is generally more diversified.

If you’re on the higher end, your portfolio is more concentrated.

This investor’s portfolio has a Top 10 allocation that’s around 54% of the portfolio.

Concentrate to get rich. Diversify to stay rich.

And again on this – there’s no right or wrong.

It just goes back to what you’re trying to achieve.

As I like to say.

Concentrate to get rich.

Diversify to stay rich.

You need to decide which phase of life are you in.

If you’re in the stage of aggressive wealth building – concentrate your assets.

If you think you have enough and you’re more concerned with protecting what you have – diversify your assets.

You need to know if you’re playing attack or defence, and then allocate accordingly.

This article was written on 31 May 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

– Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Well they are not there yet, but getting there is probably the fun part and what the questioner is seeking advice on.

Assuming they choose to continue working, one approach they could take is to add any incremental savings to the dividend part of the portfolio. Do the same for the dividends received over time. Over time, the portfolio should become more balanced towards dividends. This way they avoid the psychological aspect of having to sell down some of their growth stocks.

They could also opt to sell a small percentage of their growth stocks each year to help in this rebalancing aspect over time.

If we have information on their income, and estimated savings rate, it would be possible to run some simulations based on certain assumptions on when they would hit their goal of 5k per month dividend income. Variables that would shorten the time taken are 1) amount saved, 2) dividend yield, 3) capital gains/losses on the overall stock portfolio (both growth & dividend).

Finally, notice they have no cash holdings, which I assume is parked somewhere else and not part of the “investment” portfolio. Cash yields something today, so I guess that counts towards the income and compounding aspect as well!

That’s a good point. Instead of cutting over abruptly, do it on a slow / incremental basis.

This gives them time to adjust to a dividend portfolio, and figure out whether it works for them or not.

Really like this suggestion, thanks for raising.