Quite a few of you have asked me for my views on Singapore Airlines stock.

Since COVID lows, the stock is up almost 90%.

Even at current prices however – Singapore Airlines pays an astounding 7.1% dividend yield.

That’s a higher dividend yield than most bank stocks like DBS or OCBC bank (about 5 – 6% dividend yield).

And because of the strong demand for air-travel post COVID, Singapore Airlines continues to report record profits.

So… will I buy Singapore airline stock?

Let’s dive in.

Singapore Airlines pays a 7.1% dividend yield

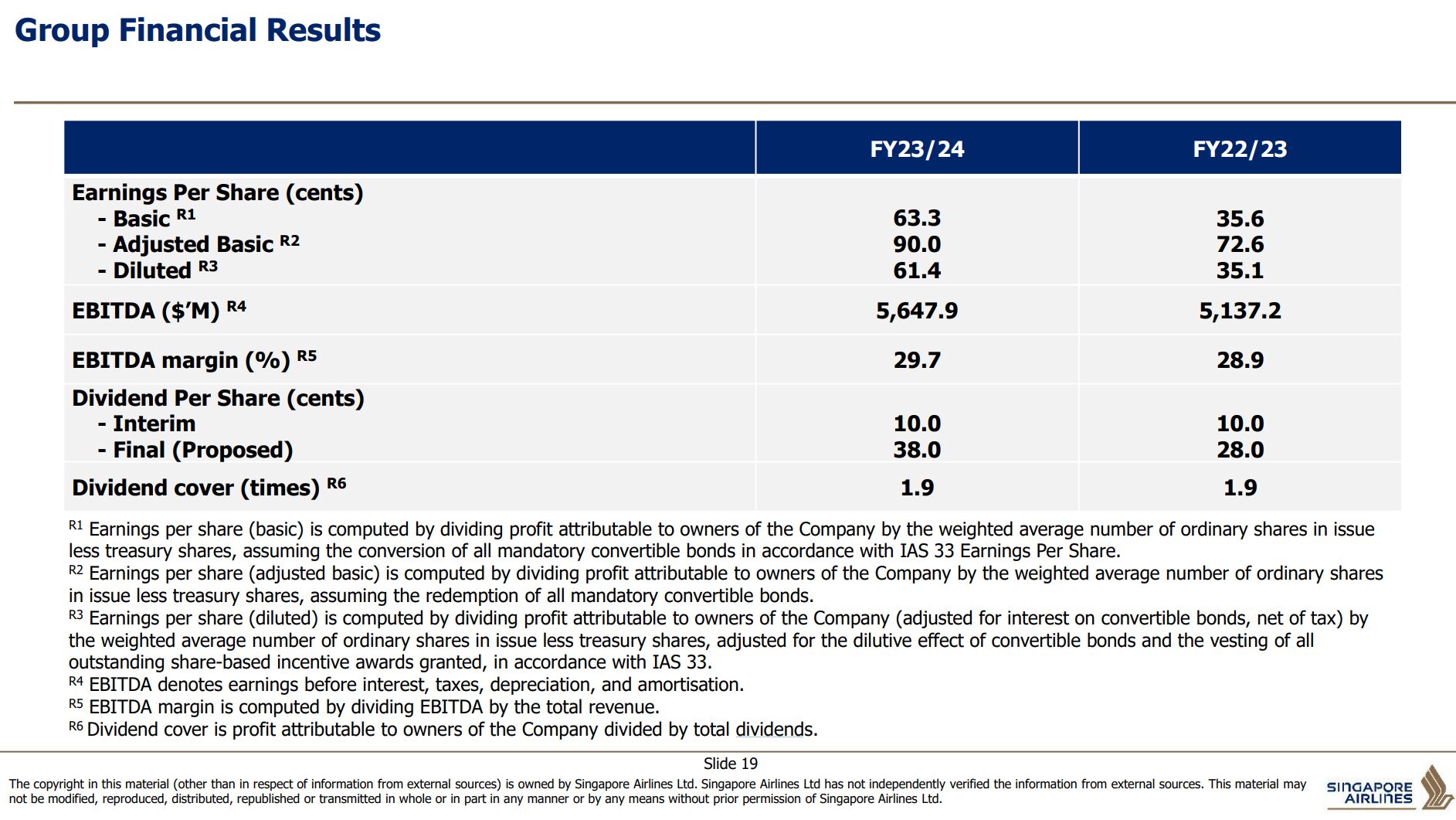

In FY24, Singapore airlines declared a total dividend of 48 cents.

Using the latest share price of $6.74 – that works out to a 7.1% dividend yield.

Given that DBS and OCBC bank pay about 6% dividend yield, Singapore airlines actually has a higher dividend yield than the Singapore banks.

And this 7.1% dividend yield is only at a conservative 52% payout ratio (similar payout ratio to the banks).

So as long as Singapore airlines can keep up the current level of profits, the dividend may be pretty sustainable.

Operational Performance of Singapore Airlines – almost at pre-COVID levels, but profits are way up

According to SIA – they expect to reach pre-pandemic passenger capacity levels within this FY.

It is interesting to note that even though capacity levels have not recovered to pre-pandemic levels.

Profits are way, way, way higher than pre-pandemic levels.

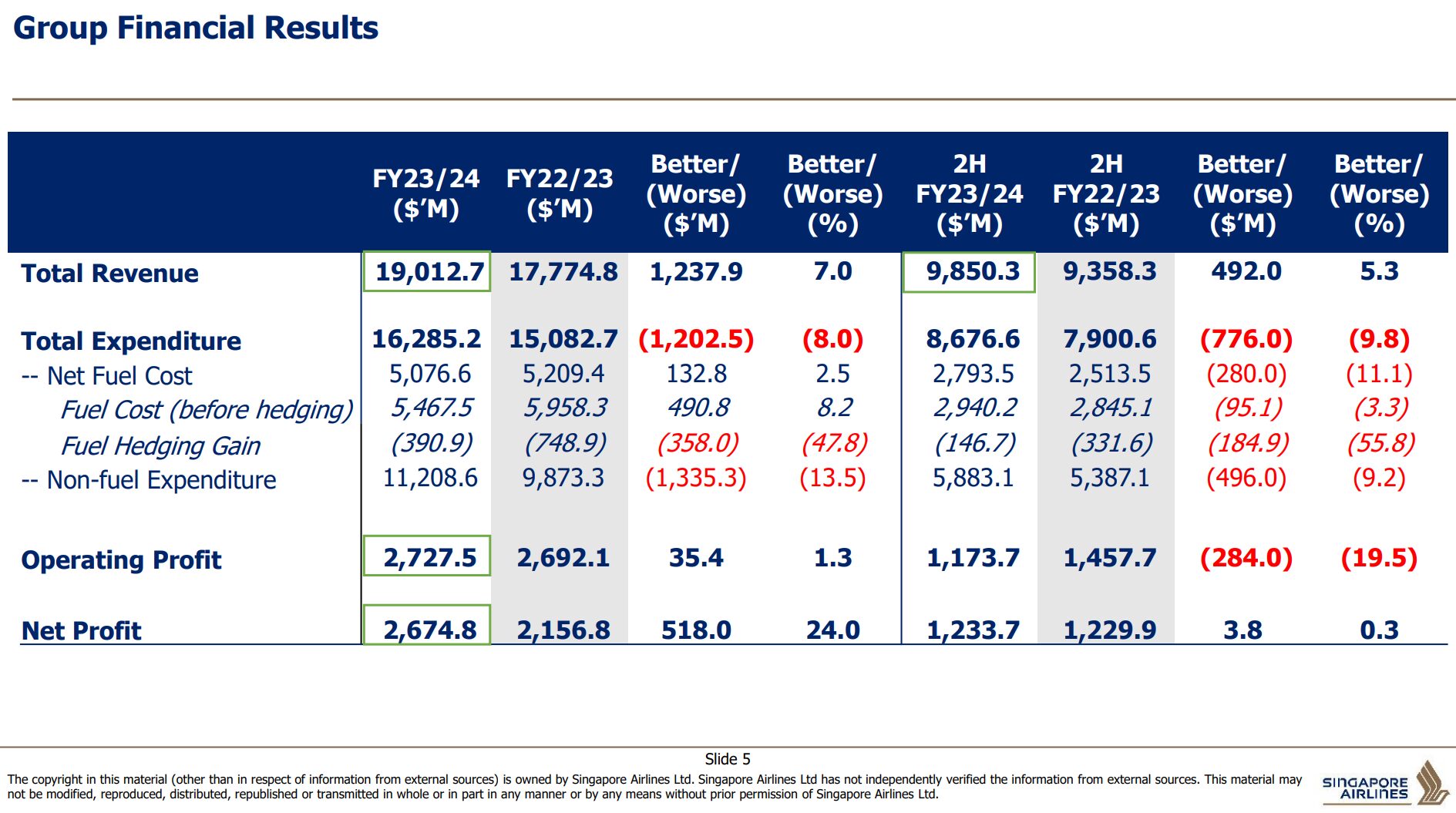

Some quick numbers:

- FY2023/24 net profit: S$2.675 billion

- FY2018/19 (pre-COVID) net profit: S$682.7 million

In plain English – Singapore Airlines FY24 profit is $2.0 billion higher (or 295% higher) than pre-COVID levels, despite the fact that their passenger capacity has not even recovered to pre-COVID levels.

That’s crazy stuff.

Why are Singapore Airlines’ profits so high, when capacity has not recovered fully?

So why are profits so high, even though capacity has not recovered fully?

Ticket prices for Singapore Airlines are significantly higher than they were pre-COVID

RASK is revenue per available seat kilometre.

It basically indicates how much SIA gets paid for each seat kilometre of capacity they have.

Pre-COVID, RASK stood at 7.5 cents.

In FY 24, RASK stood at 9.6 cents.

That’s a whopping 28% increase in prices.

If Singapore Airlines is charging more for each ticket, has demand been affected?

Normally what prevents a company like Singapore Airlines from increasing prices through the roof is that if prices go up too much, they become too expensive for customers who cut back.

However, air travel is pretty unique because after everyone was stuck at home for 2 years during COVID.

After the reopening in 2023, everyone was dying to travel again.

This sent demand for air travel through the roof – demand that was very much price inelastic.

Now PLF refers to passenger load factor – it basically indicate what percentage of SIA’s seat capacity is taken up.

PLF stood at 82.4% pre-COVID.

In FY 24, it was 88.0%.

A whopping 6.7% increase in capacity fill rate.

So… Higher ticket prices, and yet people are rushing to buy ticket?

In plain English.

The reason why Singapore Airlines is basically printing money at this point.

Is because they are charging more for each ticket.

And yet everyone is still dying to buy.

Ticket prices have gone up 28%, and yet their capacity fill rate has gone up 6.7%.

Singapore Airlines is basically printing money at this point.

I’ve extracted below Singapore Airlines’ profit margin for the past 8 years, you can see how the profit margins today are significantly higher than they were pre-COVID.

|

Fiscal Year |

Singapore Airlines Profit Margin |

|

2024 |

14.07% |

|

2023 |

14.42% |

|

2022 |

-4.13% |

|

2021 |

-99.58% |

|

2020 |

1.12% |

|

2019 |

2.76% |

|

2018 |

5.71% |

|

2017 |

2.55% |

Singapore Airlines is reporting record profits

It therefore should come as a surprise to no one that Singapore Airlines is reporting record profits.

Revenues are up 7%.

Expenses are up 8%.

And Net profits are up a whopping 24%.

But… have Singapore Airlines profits started to peak?

That being said, if you dive deeper into the numbers, it gets a bit more grey.

Yes net profit is up 24% year on year.

But why is operating profit only up by 1.3%?

It turns out that the big difference between operating profit and net profit is due to:

- Interest income (SIA is earning a higher interest income on their spare cash)

- Taxation

In plain English this means that the big jump in net profits is not actually due to the core business of air travel performing better – it’s due to one-off factors like lower tax and higher interest income.

Have Singapore Airlines Profit Margins already peaked?

If you look at the operating statistics.

You’ll find that:

- RASK peaked in early 2023

- PLF peaked in mid 2023

Cross check with the profit margins on a quarterly basis, and we see that profit margins does seem to have peaked some time in mid 2023, around the same time that RASK and PLF peaked.

|

Quarter |

Singapore Airlines’ Profit Margin |

|

Q4 FY2023/24 |

12.55% |

|

Q3 FY2023/24 |

15.59% |

|

Q2 FY2023/24 |

14.07% |

|

Q1 FY2023/24 |

16.39% |

|

Q4 FY2022/23 |

13.14% |

|

Q3 FY2022/23 |

12.96% |

|

Q2 FY2022/23 |

12.40% |

|

Q1 FY2022/23 |

9.42% |

Why has Singapore Airlines profit margins peaked?

I suppose it comes down to 2 big factors:

- Every other airline is growing capacity (more supply)

- Higher costs due to inflation

Every other airline is growing capacity (more supply)

This one isn’t rocket science.

If Singapore airlines is increasing capacity rapidly – so is every other airline out there.

Supply for air travel is growing rapidly to meet the demand.

So unlike in 2023 right after the reopen when demand-supply was hugely imbalanced.

Today the demand-supply situation is more balanced, which means lower margins for Singapore Airlines.

Higher costs due to inflation

As with any company operating in the real world these days.

Higher operating costs due to inflation have become a very real concern.

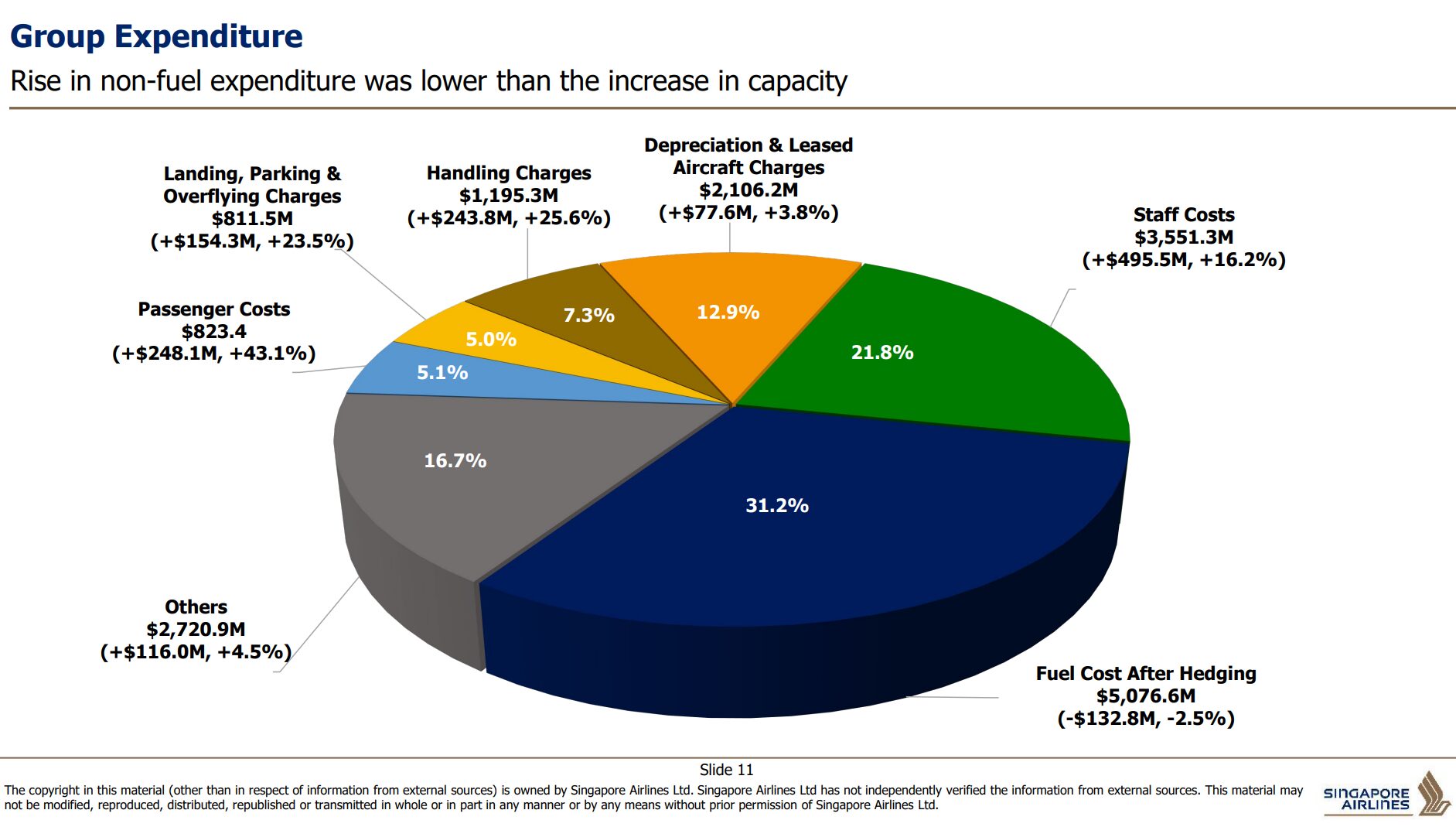

The 2 biggest costs for Singapore Airlines are:

- Fuel cost (31%)

- Staff costs (22%)

Oil Price has been muted of late

The good news is that oil price has been rangebound of late.

If this continues, or if we see a drop in oil price, that could be pretty good news for Singapore Airlines.

Staff costs – we know this is going up

Where it gets more tricky is staff costs.

All that news about SIA staff getting a 7.94 months bonus.

That is going to hit the bottom line.

You can see how staff costs increased by $500 million, or 16% year on year.

There’s no way around this one – that’s just the reality of the world we are living in today.

Economic uncertainty – if inflation comes down, will economic growth slow with it?

You’re caught between a rock and a hard place on this one.

Let’s say inflation comes down, and things like staff costs and oil prices stop going up so much.

Sure that will be fantastic for Singapore Airlines on the costs side.

But if you really think about it – what is going to cause staff costs and oil prices to go down?

The most likely scenario is some kind of broad global economic slowdown.

In which case – what is the impact on demand for global air tralve?

In 2008 for example, demand for air travel completely fell off a cliff, with devastating consequences for airlines.

Now I’m not saying that 2008 is going to repeat.

I’m just saying that airlines are economically sensitive stocks.

Investors hoping for staff costs / oil prices to stop going up so much, should be aware of what that implies for the broader economy.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

FY Results are not amazing – Singapore Airlines share price has been flat the past 2 quarters

The market seems to have sniffed this out too.

Singapore Airlines share price has been flat for the past 2 quarters.

In fact if you zoom out and look at the longer term price chart.

You’ll find that Singapore airlines share price actually peaked in mid 2023, around the same time that RASK and PLF (and profit margins) peaked.

This makes sense, as the peak in RASK and PLF means the “easy money” has already been made riding the post-pandemic travel boom.

And that going forward, SIA would have to work much harder for the growth through improving the core product offering (as opposed to simply riding the post-pandemic travel boom).

Valuations of Singapore Airlines

Let me touch on valuations, and that I will try and round up and share my views on Singapore airlines.

Singapore Airlines trades at a 1.23x book value today.

ROE is 14.8%, which is actually quite impressive for an airline.

The long term ROE is about 12-13% for airlines, so 14.8% is definitely on the higher end of that range.

PE ratio looks dirt cheap at 7.5x, but a lot of this is due to record profit margins from the post pandemic travel boom, and it’s not so clear if this can be maintained going forward.

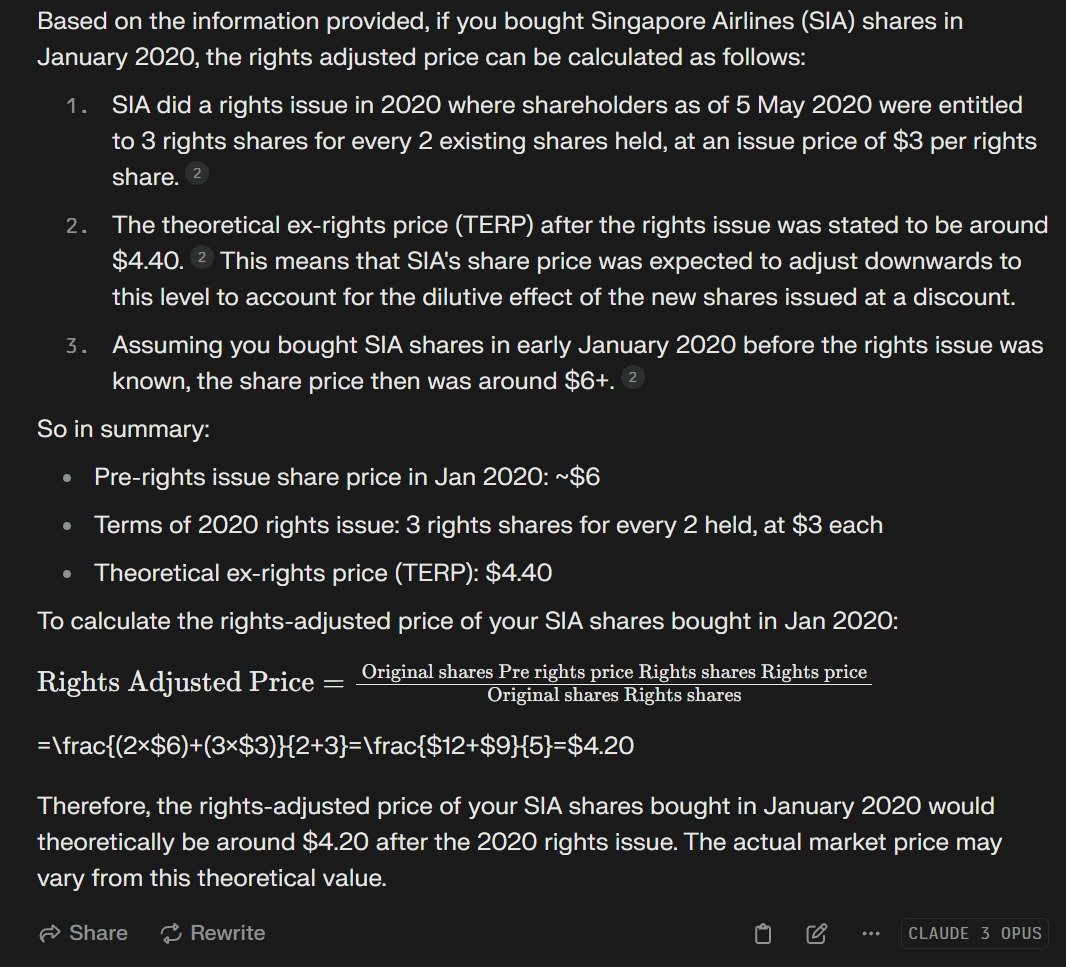

Singapore Airlines share price is up 113% since rights issue?

Singapore Airlines included the chart below showing how share price is up 113% since the rights issue price of $3.

I mean I get what they are trying to say, and factually it’s not wrong.

But just to put things in context.

Singapore Airlines did a 3 for 2 rights issue on 5 May 2020 (I covered this way back in 2020).

To buy Singapore Airlines stock at the $3 rights issue price, you would have had to own Singapore Airline shares even before that.

Realistically, had you bought Singapore Airlines shares in January 2020 (and subscribed for your rights in full), your rights adjusted price would be about $4.20.

So versus the rights adjusted price, shareholders would be up about 50% – which is probably a more realistic number than comparing is versus the rights price.

But frankly – that’s actually not that bad an outcome, being up 50% even if you had bought SIA shared pre-COVID.

Note: This screenshot above is the answer I got from Perplexity AI which is absolutely amazing to speed up stocks research.

I’m using a pro subscription – use my referral code for a 50% discount if you’re keen.

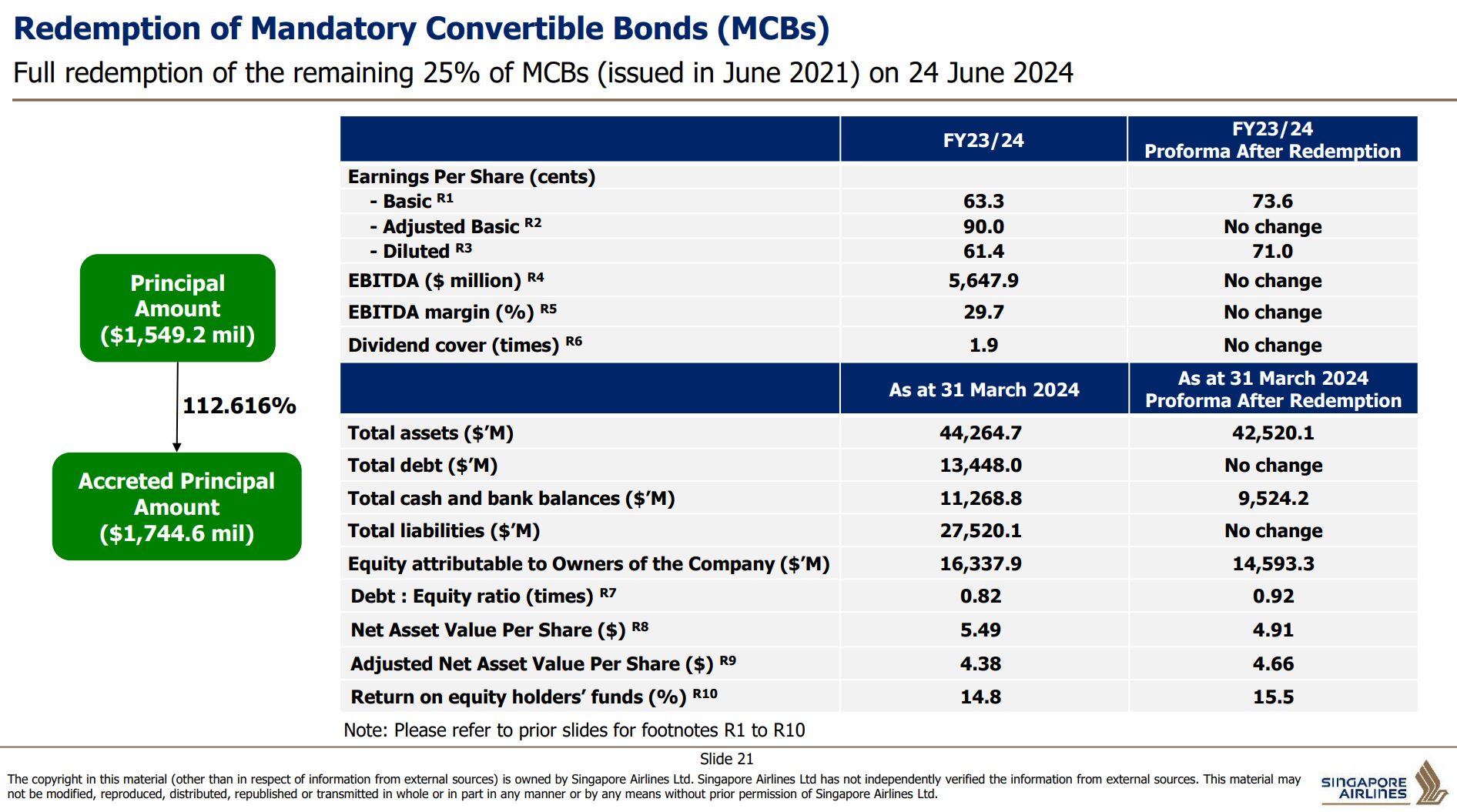

Full redemption of MCBs – COVID era measures are unwound

On that note, Singapore Airlines will also be redeeming the final 25% of MCBs that were issued in June 2021 to tide the company through COVID.

This closes the final chapter on the pandemic era measures.

Singapore Airlines (SIA) pays a 7.1% dividend yield – Will I buy this airline stock? (as a Singapore Investor)

Let’s try to sum up everything we’ve discussed above.

Singapore Airline’s best year was 2023 – right after Singapore reopened from COVID.

That was the year when demand for air travel exploded.

And yet supply for air travel capacity had not recovered fully.

This allowed Singapore Airlines to charge record high prices, and yet have record high capacity fill rates.

Profit margins exploded as a result, and share price did very well.

Since then however, supply from competitors has started to catch up.

Higher costs have started to impact bottom lines.

And so the share price has started to come back down to earth since mid 2023.

Will I buy Singapore Airlines stock? (as a Singapore Investor)

Fundamentally my biggest concern with Singapore Airlines stock today is where is the upside going to come from?

If you’re buying for the 7.1% dividend yield, then ok it could be sustainable as long as there isn’t an economic slowdown.

But capital gains wise – realistically, it’s hard to see Singapore Airline stock moving another 50% from here.

Whereas if there is an economic slowdown, or oil price jumps, or staff costs continue to go up, I could see profits come under pressure and downside risk for the stock.

Even if there are no big downside risks, the higher operating costs and higher supply from the market will grind on the stock and bring margins down.

I mean Singapore Airlines is probably an okay buy for the dividend yield and to get exposure to air travel.

But if it were me and I had bought during COVID I would look to lock in profits around here and rotate into other stocks with more upside potential (see full list of stocks on the FH Stock Watchlist).

Is SATS a better investment than Singapore Airlines?

On that note – another stock I have been getting a lot of questions about is SATS (the airport ground handler and food provider).

You can see that while Singapore Airlines stock is close to all time highs.

SATS stock is still range bound and close to pandemic lows.

Which raises the question that if you are bullish on air travel going forward.

Is SATS a better play than Singapore Airlines?

I wrote a deep dive on SATS for FH Premium subscribers last week – so do sign up if you are keen to check out my views.

This article was written on 14 June 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

– Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.