Let me just put it out there and say that this is one of the hardest markets to invest in for a while.

Even investing greats like Stanley Druckenmiller are coming out to say that they have no clue as to what happens next, because where we are today is without historical precedence.

In a climate like that – whatever your views on the macro, a healthy dose of humility is required.

It’s been quite a while since we’ve done a proper asset allocation piece on the public version of Financial Horse (much of the premium macro commentary is shared on Patreon).

So I wanted to remedy that today.

How I will invest $1 million in 2023’s “Recession” (as a Singapore Investor)

Ground Rules for Investing the $1 million

Let’s say you gave me $1 million tomorrow.

And told me to invest the money immediately, for myself, the only rules being:

- No Short-Term Trading (Buy and Hold favoured)

- My personal risk appetite (moderate risk)

How would I invest it tomorrow, without knowing exactly how the next 12 – 24 months will play out?

Million Dollar Question – Will there be a “Recession” in 2023 / 2024?

Before we can begin to answer this question, let’s deal with the elephant in the room.

Will there be a “Recession “in 2023 / 2024?

And I say “Recession” because everyone has been screaming recession since the Feds started their hiking cycle – and yet here we are with a roaring economy.

The thing about Recessions is that they’re kinda like a general election.

Yes, we all know it will come at some point.

But the timing is everything.

Economic Data / Earnings still very strong – no immediate recession

For the record, none of the hard economic data is showing any imminent recession.

Here’s US unemployment at 3.4% which is at multi decade lows.

Here’s the latest S&P500 earnings results:

Earnings Scorecard: For Q1 2023 (with 85% of S&P 500 companies reporting actual results), 79% of S&P 500 companies has reported a positive EPS surprise and 75% of S&P 500 companies have reported a positive revenue surprise.

79% with positive earnings surprise, 75% with positive revenue surprise.

That’s not the kind of data you would expect if a recession is imminent.

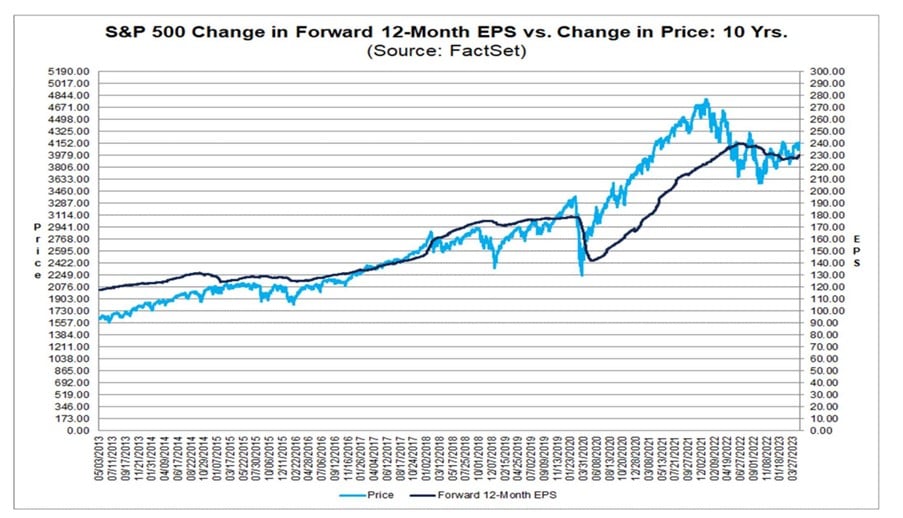

Here’s the change in forward earnings for reference.

Yes it’s come down, but only around 10%.

If this were a true recession, you’ll be looking at 20%+ drops in earnings.

Long story short – despite what the doomsayers are saying.

None of the hard economic data is showing an immediate recession.

But if interest rates stay at 5.25%… a recession will come

Let’s not miss the forest for the trees though.

If interest rates stay at 5.25% for long enough, I don’t doubt that a recession will come.

So the question then, is how long before Jerome Powell cuts interest rates?

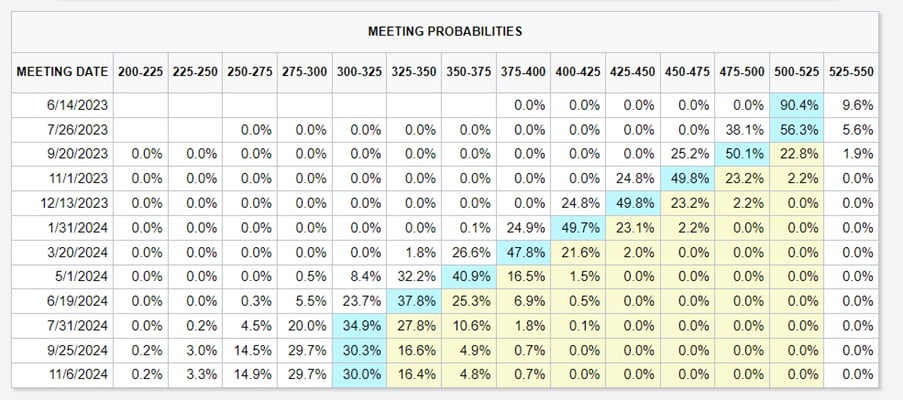

Market is saying we’re going to see 3 interest rate cuts by end 2023:

Jerome Powell says no interest rate cuts until inflation comes down.

Who’s going to be right here?

Inflation is coming down, but not as quickly as you would like

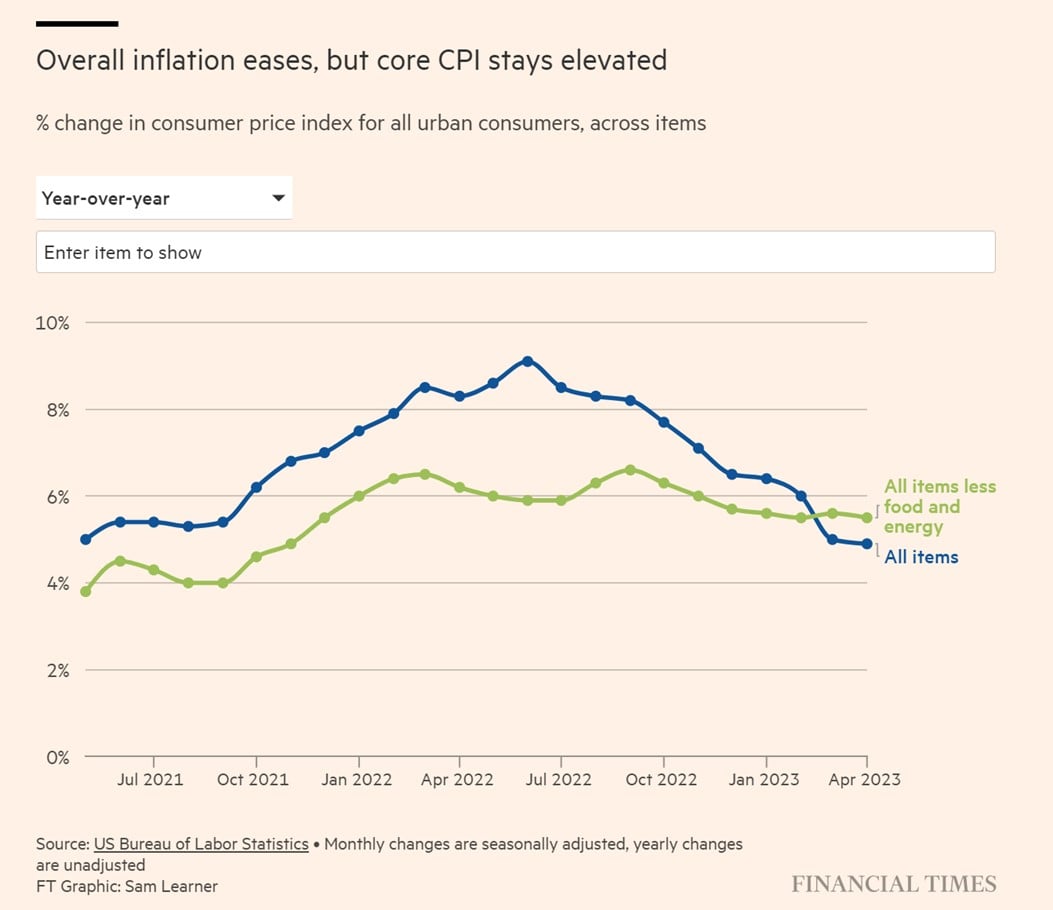

The CPI report that came out this week was notable because it does show inflation coming down:

The problem if you dig deeper into the data, is that inflation is unlikely to come down fast enough to justify rate cuts in 2023.

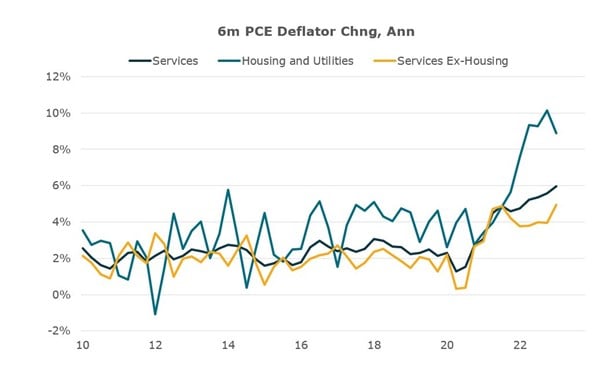

You can see that the stickiest parts of inflation (housing and services) remains very high:

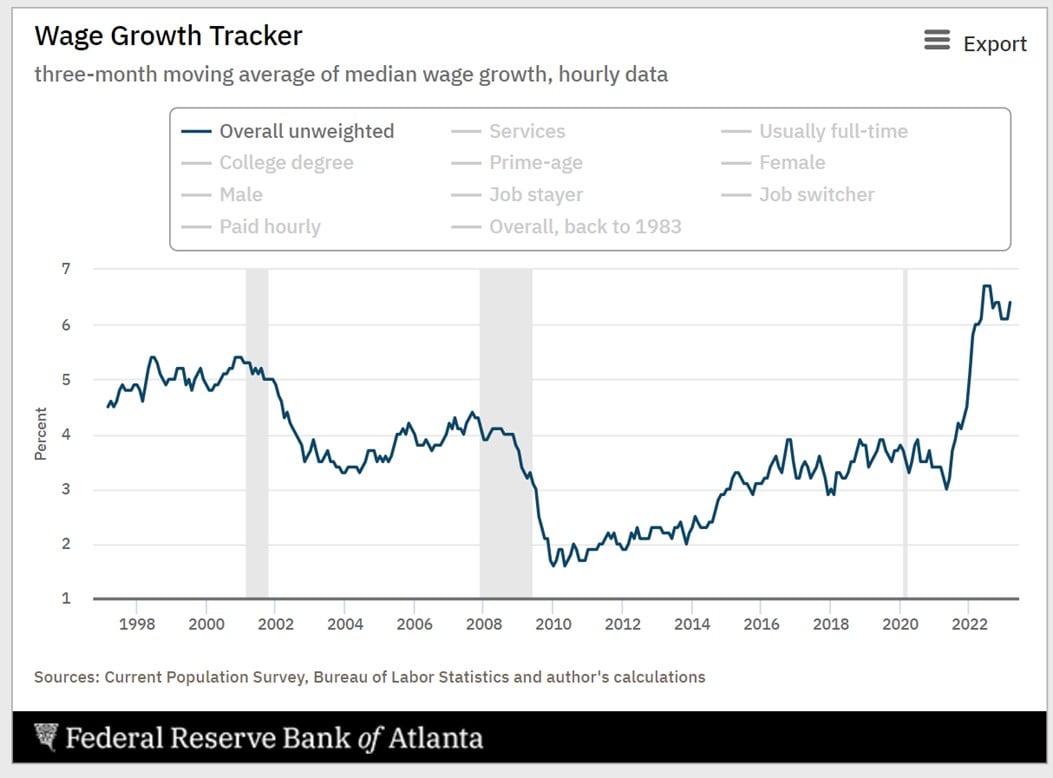

For services inflation to come down, you need to see inflation go up by at least 1 percentage point.

And for wage growth to come down to a more acceptable level.

None of this has happened yet.

Long story short – barring a complete collapse in the economy, inflation is unlikely to come down to the Fed’s target of 2% so soon.

Which means it’s hard to see interest rate cuts just yet.

So… is a recession / hard landing incoming? My personal view?

Personal views here.

Whether we see a recession, and how deep a recession if we get one.

Will depend on how quick Jerome Powell cuts interest rates when growth starts to slow.

The path we are on – growth will start to slow in the second half of 2023.

Jerome Powell so far is talking tough on not cutting interest rates even when growth slows, to bring inflation down.

He is prioritising fighting inflation, over preventing a recession.

The market is calling his bluff and saying that in the second half of 2023 he is going to cut interest rates 3 times.

Who’s going to be right here?

Well, we can venture a guess, but ultimately only Jerome Powell himself knows the answer.

Gun to my head?

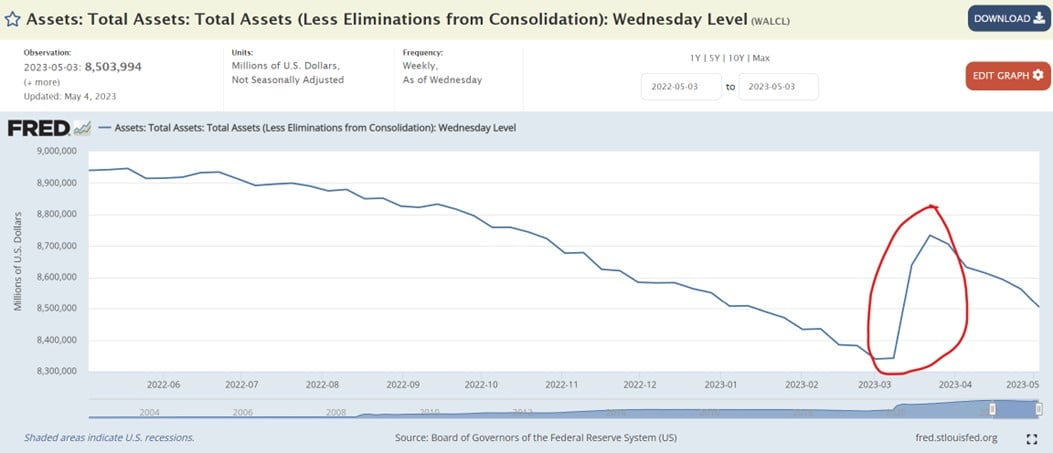

I used to think Powell was serious about inflation, but then in March when the regional banks failed he folded like a pack of cards and undid 6 months of Quantitative Tightening just like that.

And don’t forget 2024 is a US elections year.

Will Powell still be so tough on inflation if unemployment is up and Biden is in danger of losing?

So… I don’t know really.

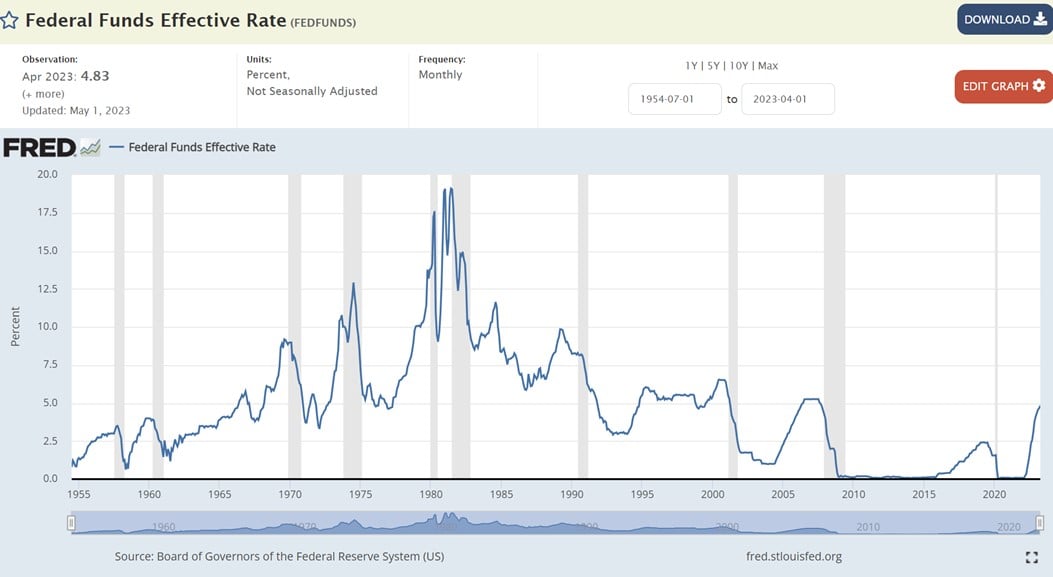

But don’t forget that the Feds have never achieved a soft landing when they were this much behind the curve on inflation.

They were pumping $120 billion a month in 2021 when Dogecoin was mooning, and then in 2022 they panicked and raised 500 bps in 12 months.

History is not really on the side of the Feds here.

How much risk exposure to run in a time like that?

So if you think that Jerome Powell is indeed going to slash interest rates in the second half of 2023.

And you want to run a 100% long equities portfolio.

You’re certainly more than welcome to do so (hey it’s your money), and who knows you might look like a genius in 24 months’ time.

Personally, I would not be max risk exposure here

Whatever the case though, you do need to accept that the uncertainty over what happens next is very high – and depends very much on how Powell reacts to slowing growth in the next 12 months.

If you tell me that inflation will be at 8% and the S&P500 is up 30% in 18 months – yeah I can absolutely see a path for that if Powell cuts early.

If you tell me that inflation will be at 2% and the S&P500 is down 30% in 18 months – yeah I can absolutely see a path for that if Powell keeps rates high for longer.

Which is more likely right now?

I don’t have a strong view.

And frankly, I don’t see a reason to take a punt on this one.

Not when I’m getting paid close to 4% risk free on cash, just to sit on the sidelines and watch this play out.

If I were investing $1 million of my own money, I don’t see a big need to be a cowboy here.

Stanley Druckenmiller gave an interview recently where he said that he doesn’t see any “fat pitches” in the current market. And that the uncertainty over what happens next is very high.

I mean, I just absolutely agree with him here.

How I will invest $1 million in 2023’s “Recession” (as a Singapore Investor)

With that in mind, here’s how I would invest my hypothetical $1 million, if you asked me to deploy it all tomorrow.

For the record, please do not take this as financial advice.

- $550,000 (55%) Cash or Bonds

- Fixed Deposit – $200,000

- T-Bills – $200,000

- Fixed Income (Bonds) – $150,000

- $150,000 (15%) REITs

- Mapletree Industrial Trust

- Mapletree Pan Asia Commercial Trust

- Ascendas REIT

- Lendlease REIT

- Keppel REIT

- $100,000 (10%) Commodities / Precious Metals

- Energy (Oil)

- Copper

- Precious Metals

- $200,000 (20%) Equities

- S&P500 / NASDAQ

- Hang Seng Index

- DBS/UOB/OCBC

Let me share my high-level thought process.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Why so much cash?

I discussed the key points above.

The level of uncertainty over what happens next is very high.

When you’re getting paid close to 4% on cash, and close to 5-6% on high quality fixed income.

I don’t see a big need to take on equity risk premium.

I wait to see what happens next, and then I invest my cash accordingly.

The worst thing that can happen is to be 100% invested today, and for the stock market to drop 30% in a recession – and I have no cash to buy in.

When would I start deploying the cash in size?

The key point I would be watching out for is the central banks’ reaction function to the coming recession / slowdown.

Or in plain English – how Jerome Powell reacts to slowing growth.

If I see Jerome Powell panicking and slashing rates to prevent a recession, you bet that I’m going all-in.

But if Jerome Powell sticks to his guns and keeps interest rates at 5.25%, I’m happy to continue sitting in cash and enjoying the high yields.

How to allocate between Fixed Income (Bonds) / Cash?

The main difference with fixed income (Bonds) vs cash is that the former has a longer duration.

So instead of buying a 6 months T-Bills (cash), you might buy a 20 year Treasury Bond.

The thinking is that as growth slows, interest rates go down, and bond prices go up.

So Fixed Income lets you lock in higher yields for longer, and allows you to enjoy capital gains if interest rates do go down.

I shared with Patreons how call options on long duration Treasury ETFs can be a way to bet on a coming recession / growth slowdown.

But it’s quite a sophisticated play with a lot of nuances that cannot be easily summarised here.

So do join as a Patreon if you’re keen to explore more.

Long story short – if you think that growth is slowing down, fixed income (bonds) can do well going forward.

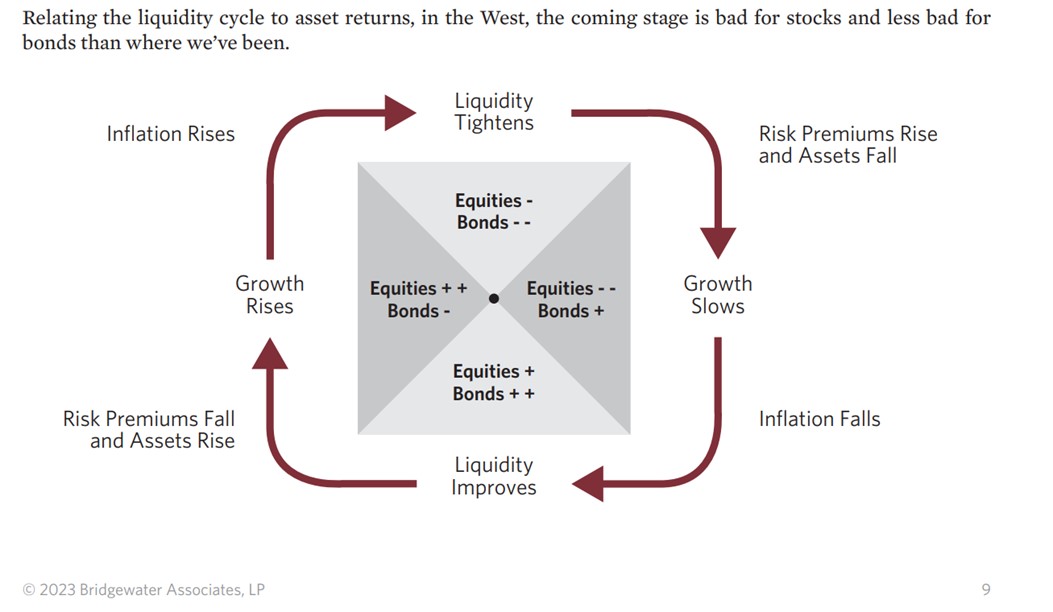

Here’s Bridgewater illustrating this dynamic:

REITs a good investment in 2023?

Given that we are likely close to peak interest rates here.

I suppose it wouldn’t hurt to allocate some money to REITs, to hedge against what is to happen next.

Who knows, maybe interest rates do get slashed to 0%, and REITs rally 50% from here?

There are certain REITs out there like Lendlease REIT or Keppel REIT that trade at close to 7% yields, and with Singapore focussed property portfolios that I like.

With $1 million, I would probably allocate some money there today.

I would probably focus more on REITs with Singapore heavy portfolios, as they are likely to weather the coming Commercial Real Estate storm better.

Full list of REIT names I like are shared on Patreon.

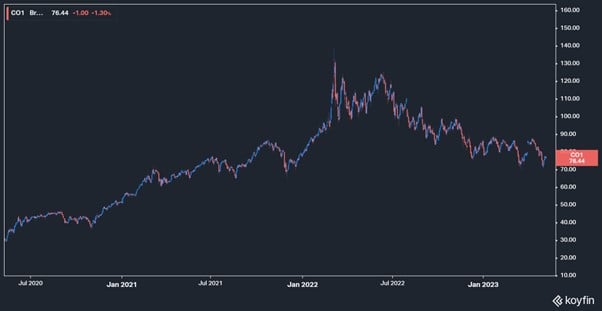

Commodities a good investment in 2023?

Frankly – commodities are a bit tricky here.

If we are indeed going into a period of economic slowdown, that’s going to hit demand for commodities in the near term.

Don’t get me wrong, I still believe strongly in commodities in the mid term.

I think the underinvestment in supply is going to come back to haunt us, while demand is not going anywhere so soon (as the green revolution is unlikely to be straightforward).

So I like commodities and I think some exposure is warranted for long term investors, but the short term is tricky.

Position size accordingly.

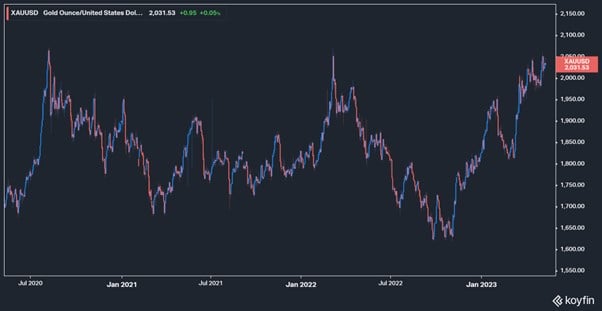

Precious Metals (Gold) a good investment in 2023?

Gold is another interesting one.

Since bottoming at $1600 in Oct 2022 at the height of the Fed hiking cycle.

Gold has roared back to an all time high of $2000 today.

Nothing like a couple of failing banks in the US to work wonders for gold’s price.

I myself hold significant gold positions as a long term asset allocation.

But at these levels, I do worry about gold in the short term.

If Powell holds interest rates high to bring inflation down, that might not be pleasant for gold.

Equities (stocks) a good investment in 2023?

And finally, equities.

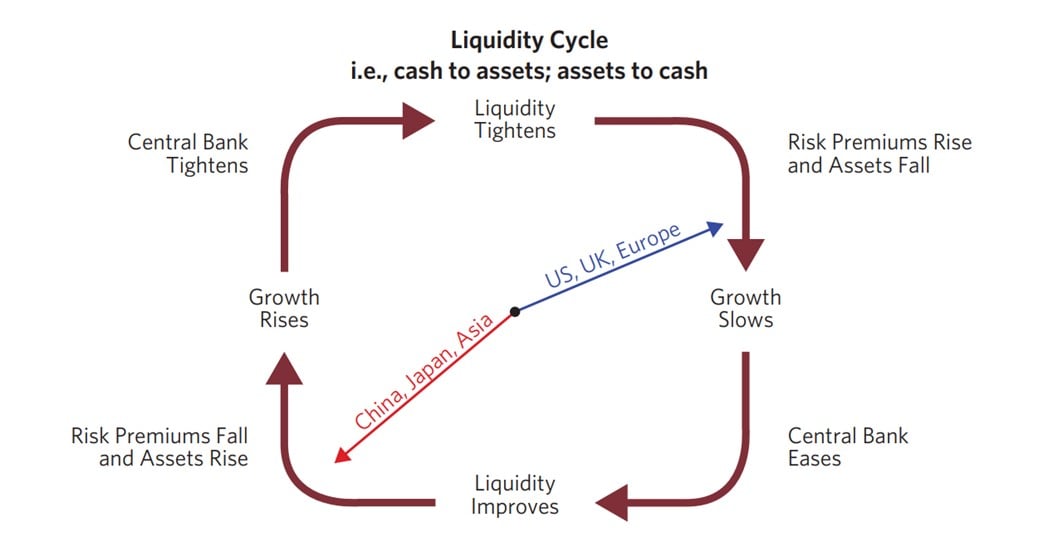

Bridgewater has an interesting investment clock where they show where they see each country in the liquidity cycle (and the implications for stock prices).

If I were allocating to equities today, as a Singapore investor?

I would probably overweight China and Singapore, and underweight the US / Europe.

Similar views to Bridgewater, I think Asia is just more advanced in the cycle as compared to the West.

The West has some tough choices ahead of it – on how to balance fighting inflation with preventing a recession.

Less so for the East, partly because we didn’t go so crazy with stimulus in the post-COVID period.

Sectors wise I don’t doubt that AI can be as transformative for the world as the internet itself, so in the years ahead there will be a lot of opportunities (both real and hype) in this space.

Lots of opportunity if you look at the right spots.

Closing Thoughts: This is asset allocation heading into the “recession”

Now this was meant as a broad overview piece on how I would allocate $1 million today, heading into the uncertainty of how the next 12 – 24 months will play out.

I’ll probably take the chance to expand on this further for Patreons, to go into how I would allocate within asset classes, and what specific names I would look at.

So do sign up if you’re keen.

PS. I received a question on this, and just to clarify, this asset allocation is meant to be how I would invest today (ie. before the recession hits).

As to how I would invest if / when the recession comes – The problem is that as of today, we dont know what the recession will look like (if at all), as much will depend on the Fed reaction function over the next 6 – 9 months.

We also don’t know if Powell will hold rates high enough to break inflation for good, or if inflation is going to come back a second time.

So what I will invest when the time comes will depend on the answers to these questions. I need to know what is cheap (valuations wise), and also what the recovery is going to look like (is inflation contained for good, or will a second round of tightening be required like 1970s).

A bit too premature to answer that question today.

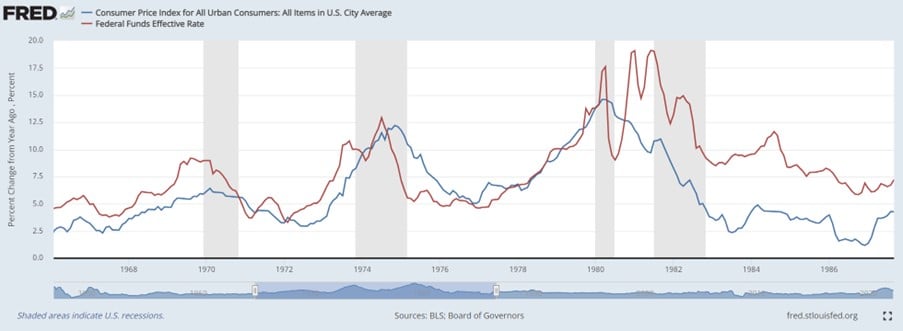

Has the Stock Market bottomed?

I wanted to leave you with a final thought.

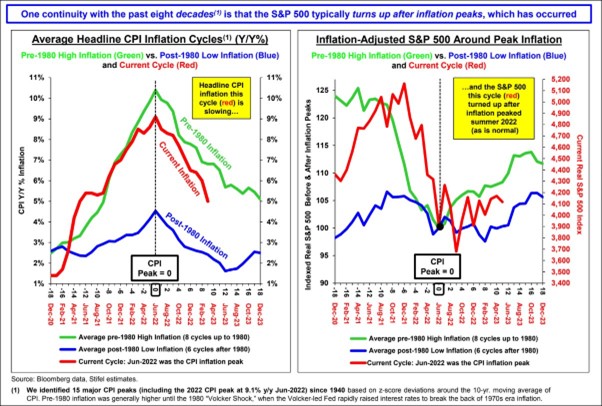

Quite a few of you have commented on the possibility that the stock market bottomed this cycle in Oct / Nov 2022.

There are charts like the below, that show that the stock market usually bottoms when inflation peaks:

My main problem with this thinking is that it makes a lot of assumptions as to what how Jerome Powell will react in the months ahead.

And also how the pre-1980 inflation data conveniently includes all the post-WWII cycles.

If you only include the data from the 1970s, you’ll find it tells a very different story.

You’ll find that in the 1970s Arthur Burns (then Fed Chair) was too quick to cut interest rates when the recession came.

Allowing inflation to roar back once he cut rates.

And requiring a second tightening cycle, and a second recession.

Which eventually required a third tightening cycle, and a third recession:

Where we are today, I think there is a good chance of something similar playing out if Jerome Powell is too quick to cut interest rates.

And that’s a massive risk that long term investors need to bear in mind.

Because how you allocate capital in a world where inflation is contained, and how you allocate capital in a world where inflation is not contained, could not be more different.

This article is written on 11 May 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates like this one. You can access my full personal portfolio to check out how I am positioned as well.

WeBull Account – Get up to USD 500 worth of fractional shares + chance to win USD888 / Tesla Model 3 (expires 30 May)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares, and a chance to win USD 888 or a Tesla 3.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking for the best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!