I came across this great comment from a FH Premium subscriber.

I’ve extracted the comment in full below (Credits: you know who you are)

From a top level perspective on global stock markets and investing as a whole:

- if value is not unlocked, shareholders will not benefit (think of assets heavy companies, think of Korean conglomerates etc.).

- if capital markets are not efficient, the stock market will not perform well. Think of sg mkt in the past, think of Chinese markets in the past.

- regardless of what opinions and preferences all of us have, undeniably, esp in the near and mid term, what drives the markets are capital flows and sentiments.

- every global market has its own merits. And some are more cyclical than others.

- With dollar weakening, EM markets will benefit generally.

- Commodities focussed countries tend to be more cyclical.

- Japan markets are waking up as the government is promulgating a more efficient capital markets. Encouraging its companies to do more shareholders’ friendly stuff such as shares buy backs.

- Korea market are dominated by legacies family-owned conglomerates we are hearing talks of making their capital markets more efficient.

- USA, whether we love them or not, has the most efficient capital market in the world. And USA has the world reserve currency. Plus a highly innovative technology industry and arguably one of the best tech incubators in the world.

- China is in the midst of opening its capital markets and getting more pro private sectors than before. That said, capital control still remains a drag on their markets. And yes, valuations are cheap but capital markets have to open up further for stock markets to fly.

Long story short, I think one doesn’t really have to make a binary investment decision (only China, not USA or anywhere else). There will always be ways to design one’s portfolio.

Although I agree that the recent USA fiasco had changed the world’s economic dynamics in some ways, it’s really hard to ignore us mkts altogether.

What is likely to happen moving forward is a more inflationary world (due to shifting of supply chains and a more nationalistic world), a long term upward bias towards median interest rates due to a more inflationary environment, greater geopolitical tensions and definitely a lot more printing of money.

With above framework, it will mean (when it comes to constructing my portfolio):

- no long term bonds for me (other than CPF), other than for short term speculative trading purposes.

- hard to ignore owning scarce assets due to massive printing of fiat (properties, precious metals, commodities etc.). And by extension, digital currencies like btc and ethereum

- a diversified global portfolio (geographically, across asset classes etc.)

- and be a lot more nimble rather than passive investing

- holding a decent amount of cash as war chest to deploy whenever opportunities arise as I will expect lots of volatility moving forward

- be sensitive to valuations when buying

- and keeping my eyes closely on tailwind industries and sectors

My key takeaways?

Like I said, good comment with a lot of nuance, and plenty to digest.

There are 3 key takeaways I want to touch on:

- Own scarce assets in an era of inflation / money printing

- Long term government bonds are a dangerous buy in this new paradigm

- Diversify geographically, but apply your mind to which countries and position sizing

- *Bonus* Decent war chest makes sense

This is an FH Premium post written 1-2 months back that I am making available to all readers.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

Own scarce assets in an era of inflation / money printing

I think whatever way you spin it, it’s fairly clear that the US government deficit is not going to get smaller.

After a brief attempt by Elon’s DOGE, efforts at government cost cutting have all been abandoned at this point.

And yes the Trump tariffs will generate revenue, but looking at the size of the tax cuts, and what is likely to be more government spending in the years ahead, and now with DOGE cost cutting out of the way, I don’t see it moving the needle meaningfully.

This is why there is so much upward pressure on US long term yields.

Once you accept that the US government budget deficit is not going away any time soon.

And you accept that because of reduced reliability of US as an ally (we discussed this in previous articles), the marginal inflow of capital into USD assets will decrease going forward (which you see manifested in a weaker USD).

This then begs the question of what asset classes will benefit.

I discussed this in detail in past week’s article, and the options I narrowed down to are:

- Bitcoin / Gold

- Stocks (the right stocks)

- Real estate (in the right places/countries)

Bitcoin / Gold is self explanatory so I won’t touch on it.

Stocks has some nuance, because we all know with the wrong stocks you’re better off just holding cash. But if you pick the right companies that has products the market needs and can grow earnings every year, that’s about as scarce as asset as it gets.

Real estate against has nuance, because real estate is a local business (you must understand supply demand dynamics in the local market), and real estate cannot be moved easily.

The last point is relevant to both stocks and real estate. The simplest example is to imagine you are a Chinese investor, and you buy US real estate (or stocks). Suddenly the US passes a law saying it is illegal for Chinese nationals to own US assets (and if you think this is impossible, just talk to the Russians after the Ukraine war).

As Singapore investors we don’t need to think so much about this because this is unlikely to happen to us, but you have to recognise that there are many other countries where this is not the case. Don’t underestimate this kind of impact in the years ahead.

Long term government bonds are a dangerous buy in this new paradigm

The corollary of a more inflationary world where the US runs a large budget deficit.

Is that it becomes a lot more dangerous to own long term government bonds.

Short term 6 – 12 month T-Bills are absolutely fine.

What I’m talking about here is a 10 or 20 year US government bond.

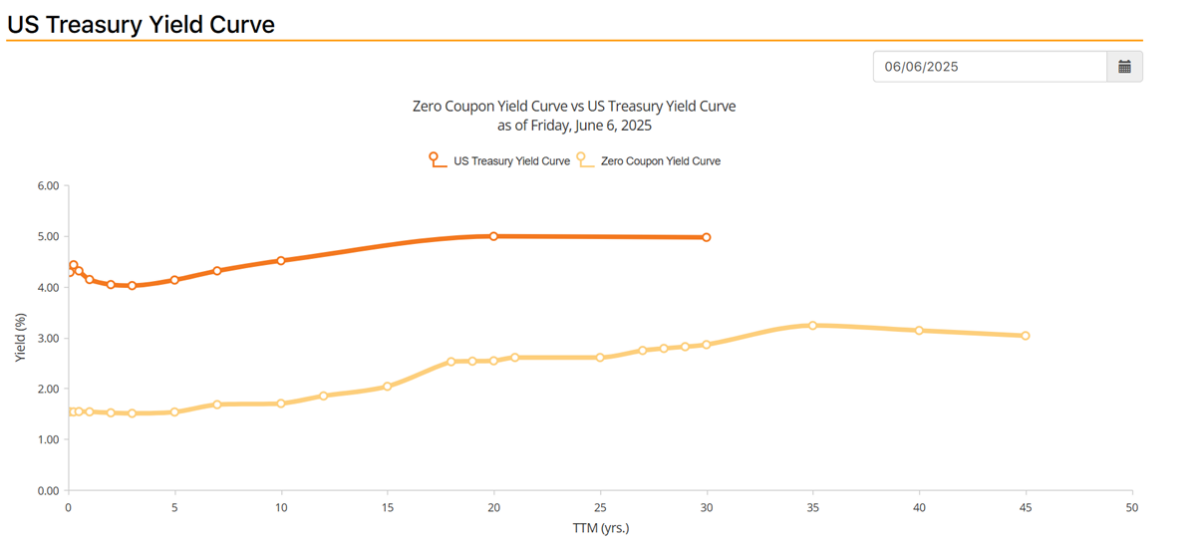

Yes the 4%+ yield is juicy and all, but over a 10 – 20 year horizon, are you really certain what the US government is going to do over that kind of timeframe?

If long term yields go to 5% and beyond, as a holder of long term US debt you will be sitting on huge losses.

And look at the yield curve below, you don’t even get much of a higher yield by going to longer durations.

The only benefit of a longer duration is the ability to “lock in” yields.

But if you accept that we are in a paradigm of structurally higher government deficits, inflation, and interest rates, then this benefit is no longer as important.

Long story short – if you want to own bonds (and I think bonds are actually pretty attractive), own the short duration bonds.

Anything from 6 months to 3 – 4 years I think is fine, depending on the kind of lock up you can accept.

But really I wouldn’t touch anything with a 5 year duration or more.

Diversify geographically, but apply your mind to which countries and position sizing

The 3 key markets I would focus on as a Singapore investor are:

- US

- Singapore

- China

Some of you asked me why not Europe, and my reason is that Europe has structural challenges that make it uncompetitive as a market (regulatory climate, political systems, work culture etc). You can stock pick for Europe (eg. LVMH, SAP etc), but if you buy a broad European stock index these are the challenges.

Within US, Singapore, China, how do you allocate?

Really that’s the million dollar question for each investor to decide, but here are some guiding principles in my view:

- Yes there is talk about end of US exceptionalism, but at the end of the day you still need a healthy allocation to US assets given the strong potential performance

- As a Singapore investor, you cannot not be allocated to Singapore (you need assets for SGD hedge and inflation hedge if Singapore economy does well)

- China is a wildcard – to me you want some allocation, but you also don’t want to overdo it until there are meaningful signs of stimulus

You can see my full personal portfolio, and how I am allocated, on FH Premium.

*Bonus* Decent war chest makes sense

And the final point.

You can see how the stock market the past 5 years since COVID, has become much more volatile than the 10 years before that when the Feds kept rates at zero, and inflation was not a problem.

In my view – I don’t see that changing going forward.

Expect a volatile and bumpy ride for capital markets.

And in a climate like that, a decent war chest makes a lot of sense as:

- It helps you sleep at night when markets are volatile

- It earns a decent yield today (yes T-Bills rates are down, but you can still scrape together decent yield compared to pre-COVID)

- It enables you to take advantage of market sell-offs

The drawback with cash of course, in that in an era of large government deficits and structurally higher inflation, cash won’t keep pace with inflation.

So that’s where the allocation to risk assets comes in, and the need to find what is the right balance between a war chest and risk assets.

With my own war chest though, not all of it is in cash, and some of it is in longer duration bonds like PIMCO GIS Income Fund, or even bond proxies like Netlink Trust, REITs etc to earn a higher yield.

And you can see my full personal portfolio, and my full stock / REIT watchlist, on FH Premium.

This is an FH Premium post written 1-2 months back that I am making available to all readers.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

Here’s an (old) idea. Build a bond ladder (T-bills) with one-third of your safety fund, and put the other two-thirds into Singapore Savings Bonds (SSBs). At the moment SSBs (incredibly) pay more interest than T-bills, so you could (quite sensibly) make it 100% of any “new” money up to the S$200K limit. The major benefit of SSBs is you can get all your money back with interest until withdrawal date without penalty. If you lose your job, or need money, you can just use your maturing T-bills, and if you have a bond ladder they mature every 2-weeks.

With that kind of safety-net you should have no trouble sleeping at night. Once your 12-month safety funds are in place, then start looking for actual investments.

If you’re lucky enough to have S$1million to invest, then allocate the other S$800,000 to low-cost index funds, topping up your CPF, and maybe paying down your mortgage (if you have one).

Great comment!