So I received the following question from a reader:

Hi FH,

Like to pick your brains on something.

I am in my 50s, and thinking about retirement due to job stresses.

I have a condo (main residence), and an investment property that is fully paid off (rental yield about $4,000 a month)

On top of that I have about $1.5 million in investible assets (after setting aside emergency funds).

Today they are invested in a mix of T-Bills, SSBs, FD, REITs etc.

I don’t want to buy another investment property because of ABSD.

And because interest rates are going down, I’m worried that the cash won’t generate a good yield going forward.

If you were me – what are the options you would consider for investing that $1.5 million?

Ideally I want to get about $6,000 a month in passive dividend income from there.

Together with the rental yield that gives me about $10,000 a month in passive income which should cover what I need.

With a $1.5 million investment portfolio – what dividend yield to generate $6,000 a month?

Let’s run some simple numbers.

With a $1.5 million investment portfolio.

$6,000 a month in dividend income works out to $72,000 a year, or a 4.8% dividend yield.

Is that hard?

Well – just a month or two ago you could park a big chunk of that money in a 6-month T-Bill and generating 3.8% risk free.

Throw in some REITs / Dividend stocks on top of that, the 4.8% dividend yield seems pretty feasible for not a lot of risk.

But – Interest rates going down… fast?

As the reader pointed out though – interest rates are going down very quickly.

Because of slowing US inflation and a weakening US labour market.

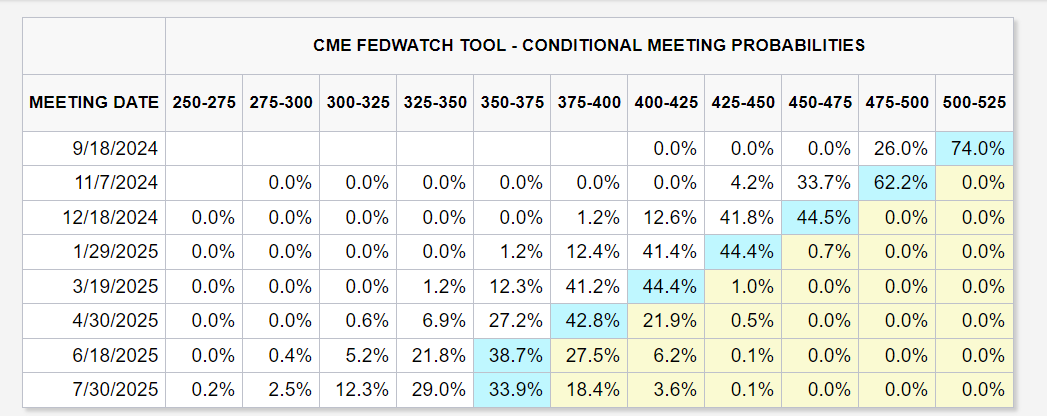

The market is expecting a lot of rate cuts from the Feds.

As of today, market is pricing in almost 8 interest rate cuts over the next 12 months.

That’s a whopping 2.0% drop in interest rates from now until mid 2025.

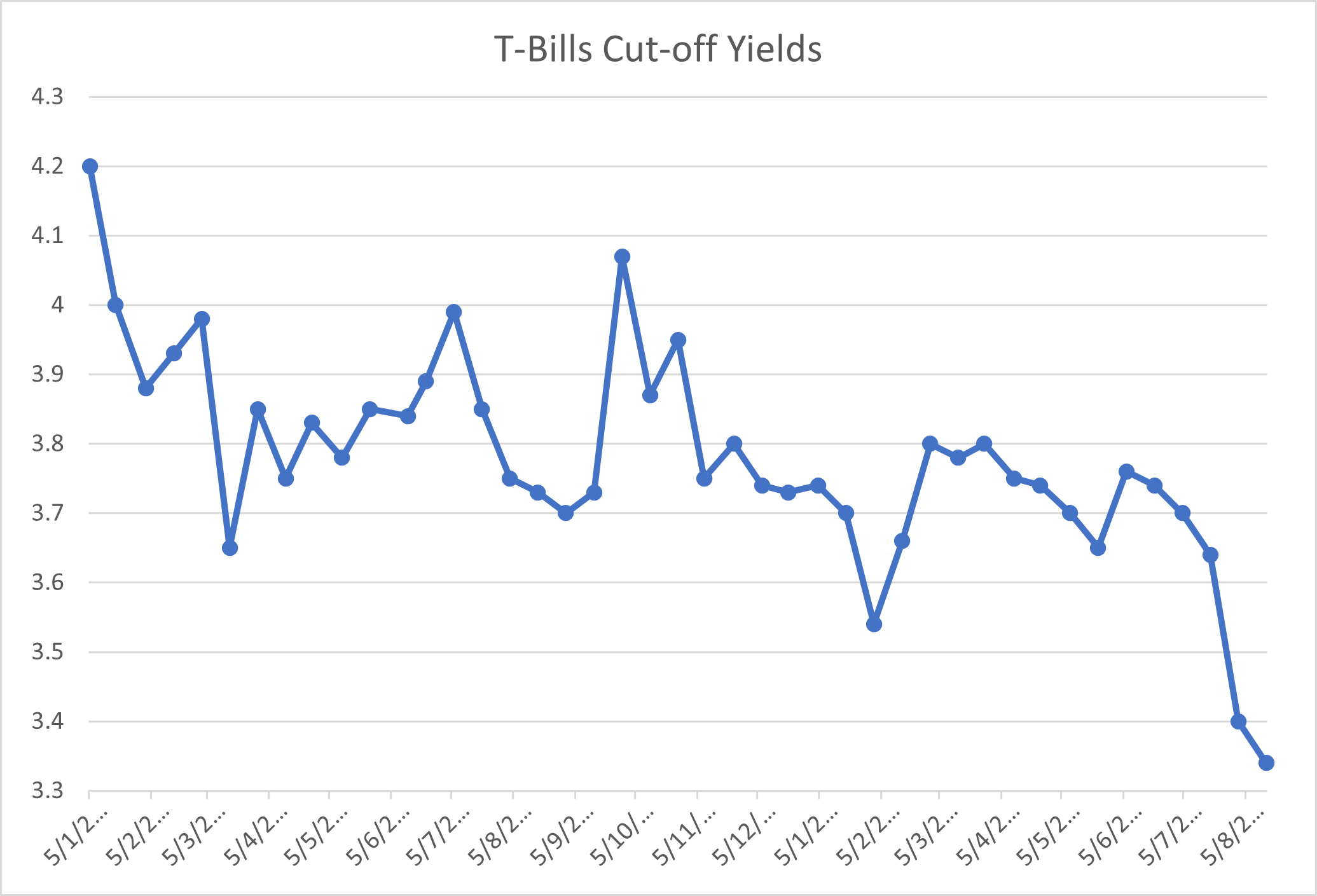

Because of that, interest rate have fallen sharply across the board.

The latest 6-month T-Bills yield only 3.34%:

While the Singapore 10 year yield has fallen from 3.5% in late April to 2.7% today:

What are the options for a Singapore dividend investor in 2024? To lock in yields?

I’ve summarised the various options for a Singapore dividend investor below, if you’re looking to “lock in” yields.

|

Asset Class |

Risk level |

Estimated yield |

Can you “lock in” yields |

|

Cash (eg. T-Bills, Singapore Savings Bonds, Fixed Deposits) |

Risk Free |

3.3 – 3.5% |

No (except for SSBs) |

|

Bonds |

Low – Medium risk |

4-6% depending on level of risk |

Yes |

|

Dividend Stocks |

Medium – High risk |

4-6% |

Yes |

|

REITs |

Medium – High risk |

5-8% |

Yes |

How to earn $6000+ a month in passive dividend income – with falling interest rates? Buy Dividend Stocks, REITs and Bonds?

For obvious reasons I do not know the reader’s exact risk profile, so I cannot comment on that.

But if I were in a situation like that?

I might go with a split like the below:

|

Amount |

Average Dividend Yield (%) |

Dividend |

|

|

Dividend Stocks |

500,000.00 |

6.13 |

30,666.67 |

|

REIT (“Blue Chips”) |

300,000.00 |

5.4 |

16,200.00 |

|

REIT (“higher risk”) |

200,000.00 |

7.0 |

13,920.00 |

|

Bonds |

300,000.00 |

4.0 |

12,000.00 |

|

Cash |

200,000.00 |

3.4 |

6,800.00 |

|

1,500,000.00 |

5.31% |

79,586.67 |

|

|

Dividend per month |

6,632.22 |

Let’s talk through each asset class, and what I might consider buying.

What Dividend Stocks (excluding REITs) would I consider buying for the dividend portfolio?

I thought very long and hard about this one.

If say you gave me $500,000 today.

Forced me to go out tomorrow and buy dividend stocks (excluding REITs / real estate).

Which dividend stocks would I be comfortable with?

And really, apart from the 3 local banks of DBS, UOB and OCBC, I couldn’t really come up with many good options.

I mean sure, gun to my head there are names I can think of like ST Engineering, Singtel, Keppel, Sembcorp etc that I don’t mind owning.

But do I think any of those offer great value at today’s price?

Not really to be honest.

So ultimately I decided to keep it simple and stick to the 3 local banks for the dividend stocks.

If you buy all 3 local banks in equal weight, you would get a blended dividend yield of 6.1%.

And that’s frankly not too bad.

|

Dividend Stock |

Dividend Yield (%) |

|

DBS Bank |

6.3 |

|

UOB Bank |

5.9 |

|

OCBC Bank |

6.2 |

|

Average: |

6.13 |

What is the risk with buying bank stocks today? How to hedge that risk?

The biggest risk with buying bank stocks today though.

Is that the Feds have literally told you that they are going to cut interest rates going forward.

So you would be buying into a declining interest rate climate (with a lot of cuts priced in), all while US data is pointed towards elevated risk of a recession (I say elevated because its not a sure thing, but the data is suggesting risk of a recession if policy makers do not react properly).

My personal view – I think that even if interest rates drop, the Singapore banks may be able to maintain their dividend yields as current the current 50% payout ratios are not demanding.

The key assumption being that we avoid a recession.

If we get a recession, and the Feds cut interest rates aggressively, then of course all bets are off.

Because of that you don’t want to all-in Singapore banks as well, and you want something to hedge that recessionary scenario.

That’s where the next portion of the portfolio comes in – REITs / real estate exposure.

Can REITs truly hedge against a recession / downside interest rate risk?

The logic behind REITs, is that if we get a recession, and interest rates are cut aggressively.

Then REITs should benefit as interest expense goes down, while REITs become more attractive to investors since bonds/cash now pay a lower yield.

Of course, that is just theory.

In reality if we actually get a recession, I don’t expect REITs to be immune as rentals would come down.

Because of that I would want to have cash/bonds in the portfolio as well (which should perform better in a recession).

But sometimes in investing you want to stay big picture and not overthink things.

If interest rates are coming down – REITs may stand to benefit, therefore some exposure makes sense.

What REITs would I consider buying for the dividend portfolio?

With REITs today, they can broadly be split up into 2 segments.

On one hand you have the safe, “Blue Chip” REITs from strong sponsors that hold primarily Singapore real estate.

Couple of indicative REITs below, blended dividend yield is about 5.4% for this basket.

|

REIT (“Blue Chips”) |

Dividend Yield (%) |

|

CapitaLand Integrated Commercial Trust |

5.2 |

|

Ascendas REIT |

5.7 |

|

Frasers Centrepoint |

5.3 |

|

Average |

5.4 |

And then on the other hand you have the more risky REITs that either (a) are smaller in size, or (b) carry overseas real estate exposure (and therefore more risk).

Again a couple of indicative REITs below, blended dividend yield for this basket is 7.0%.

|

REIT (“higher risk”) |

Dividend Yield (%) |

|

MPACT |

7.0 |

|

Keppel REIT |

6.8 |

|

Starhill Global REIT |

7.5 |

|

Ascott REIT / FEHT / CDL HT |

6.5 |

|

Mapletree Logistics Trust |

7.0 |

|

Average |

7.0 |

How to allocate the REITs in the portfolio?

I can then mix the blue chip REITs and the higher risk REITs depending on risk appetite.

The more risk adverse can stick to the former, those with higher risk appetite can overweight the latter.

Note the REITs above are just indicative only, I am not saying to go out and buy them as price still matters.

My full REIT (and stock) watchlist is shared on FH Premium, with my price targets.

Cash – holds value well in a recession, but interest rates are dropping quickly

That said, dividend stocks / REITs would not be immune in a recession, so we still need some cash.

The biggest problem with cash in a declining interest rate environment – you cannot “lock-in” yields.

The yields on 6-month T-Bills (or fixed deposit) are only guaranteed for the tenure.

So if it’s a 6-month T-Bill or fixed deposit, you only lock-in the yields for 6 months.

If interest rates are much lower in 6 months, that could be a problem.

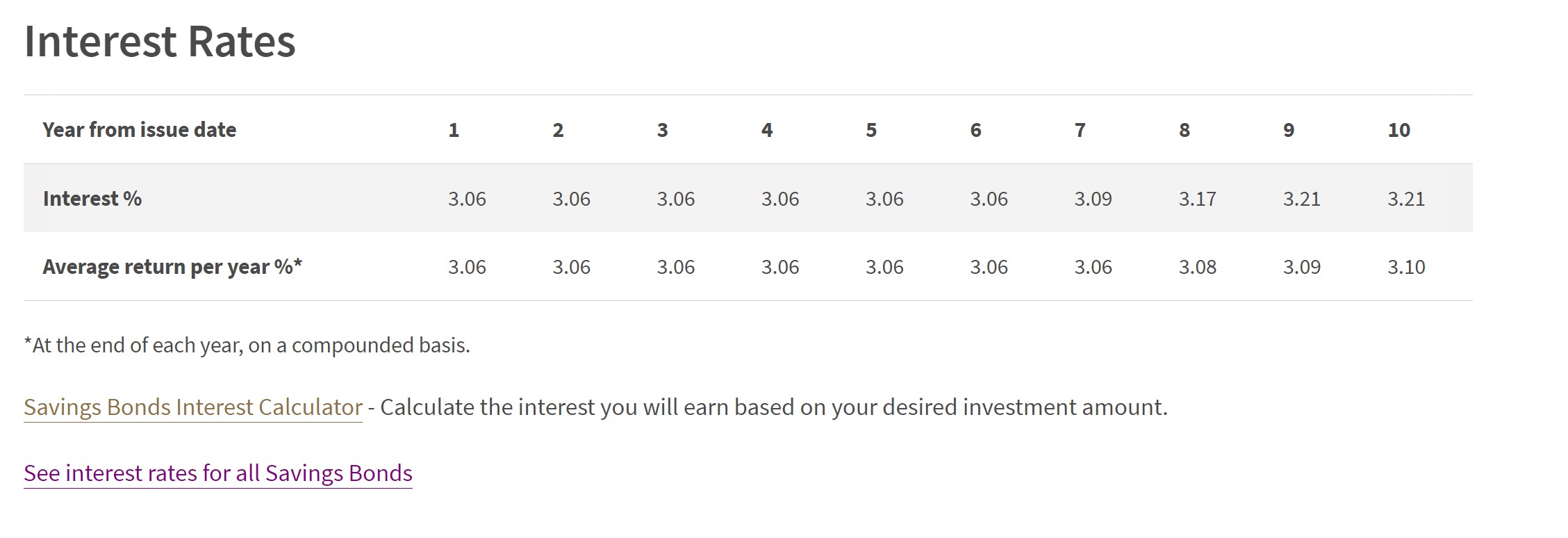

The exception is Singapore Savings Bonds – and actually with the sharp drop in interest rates this month’s SSBs at 3.06% first year yield are worth a look if you don’t have any (will write more on this tomorrow).

Do bonds make sense for a dividend portfolio? To lock in yields.

Because of that, at this point in the cycle it may make sense to increase duration.

Instead of buying 6 month T-Bills, you may instead buy a 4 year bond.

4 years is long enough to “lock-in” yields for a longer period, and yet not long enough that you will suffer big capital losses if interest rates go up.

For most retail investors the best way to achieve diversified exposure to bonds is to use a bond fund.

There are many options these days from the various Robo Investors.

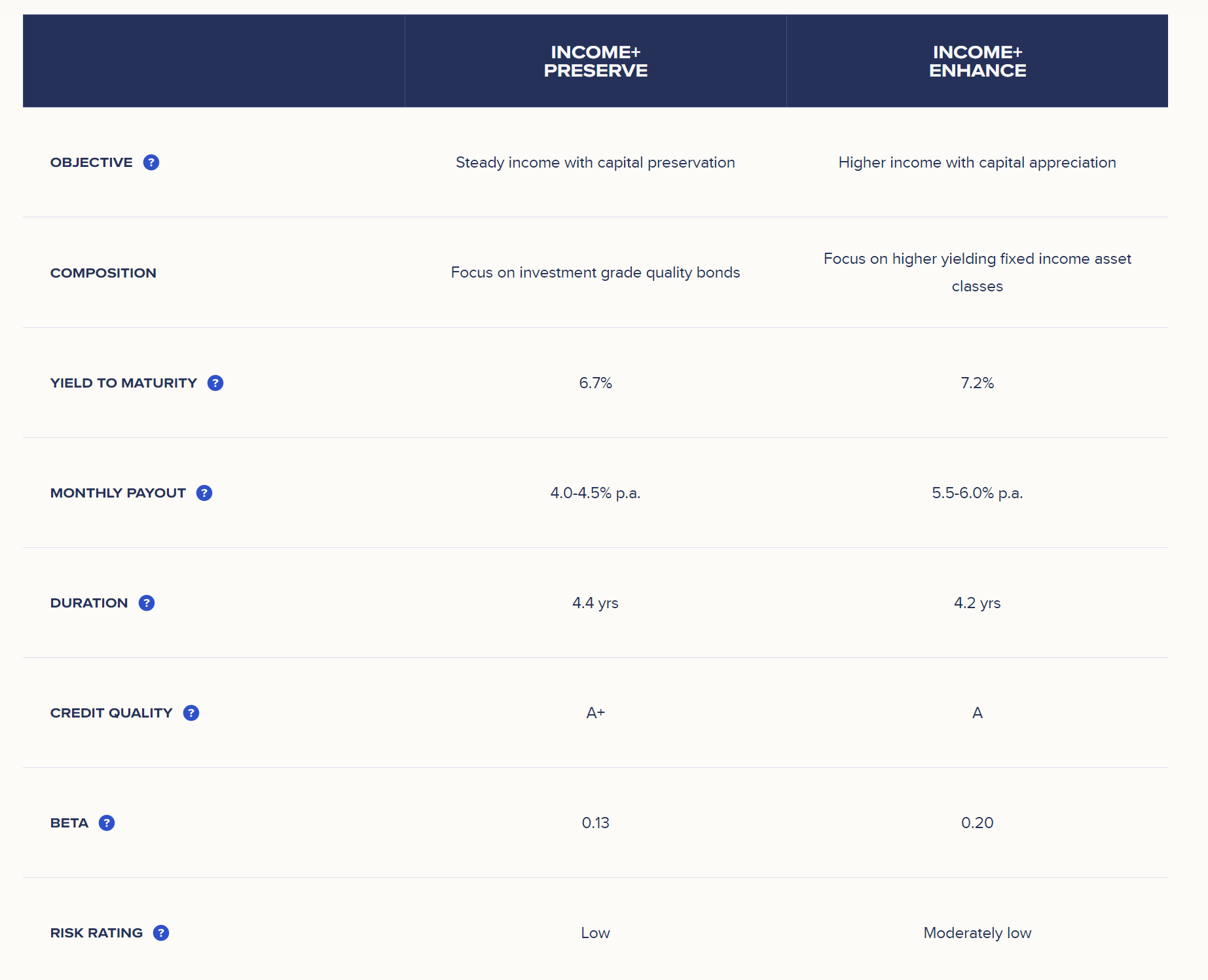

Here’s Syfe Income portfolios for example, with a target yield for 4-4.5% or 5.5-6% (depending on risk level), with a duration of about 4 years:

Endowus has something similar with their Income portfolios.

What are the risks of investing in a bond fund?

A lot of you have asked what are the risks of investing in a bond fund.

If you pick an SGD hedged bond fund (and you should), then the FX risk is hedged away.

And because the bond funds are broadly diversified, this means the single issuer risk is also diversified away.

The key risks you take on (that cannot be easily diversified/hedged) are:

- Macro risk – bond defaults due to recession

- Interest rate risk – capital losses from rising interest rates

That’s just a risk you have to be comfortable with for these bond funds.

As of today, I would say for a low-risk bond portfolio you’re probably looking at about 4%+ yield.

This would have been higher just a month or two back (perhaps as high as 5%) – but you can see how interest rates have plunged sharply since late July:

You can now follow Financial Horse on Google Chrome to avoid missing any posts!

Just:

- Click the 3 dots on the top right of Google Chrome

- Click Follow!

- And Financial Horse posts will now appear on your home page, under Following:

You can also follow Financial Horse on:

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

Estimated passive dividend income this portfolio will generate?

Assuming a 1/3 split between Dividend Stocks, REITs and Bonds/cash.

We’re looking at about a 5.3% blended yield across the portfolio.

At $1.5 million in assets, this works out to $6,600 a month in passive income, above the target the reader was looking for.

|

Amount |

Average Dividend Yield (%) |

Dividend |

|

|

Dividend Stock |

500,000.00 |

6.13 |

30,666.67 |

|

REIT (“Blue Chips”) |

300,000.00 |

5.4 |

16,200.00 |

|

REIT (“higher risk”) |

200,000.00 |

7.0 |

13,920.00 |

|

Bonds |

300,000.00 |

4.0 |

12,000.00 |

|

Cash |

200,000.00 |

3.4 |

6,800.00 |

|

1,500,000.00 |

5.31% |

79,586.67 |

|

|

Dividend per month |

6,632.22 |

What is the key risk with this dividend portfolio?

For obvious reasons, this portfolio is not without risk.

Risk free is the Singapore Saving Bond at 3.1% yield – anything higher implies that you are taking on some form of risk.

Let’s game out the various macro scenarios.

If you ask me, the possible scenarios over the next 12 months are:

- Recession – Fed rate cuts are insufficient and US economy tips over into recession

- Inflation – A Trump victory leads to trade barriers / huge fiscal spending, reigniting inflation

- Stagflation – A Harris victory leads to more of the same – a weakening US economy with sticky inflation

- Goldilocks soft landing – the holy grail for investing – the US economy stays strong, inflation comes down, Feds slash interest rates 2.0% in the next 12 months

The performance of the asset classes in the different scenarios:

|

|

Dividend Stocks (Banks) |

REITs |

Bonds/cash |

|

Recession |

Bad |

Average |

Good |

|

Inflation |

Average |

Bad |

Good |

|

Stagflation |

Average |

Average |

Average |

|

Goldilocks soft landing |

Good |

Average |

Average |

So generally speaking the portfolio as a whole should be able to hold its own in the 4 scenarios above.

Yes of course there will be losses, but the goal is always to keep the losses to a level that is manageable.

And in each of the 4 scenarios, some part of the portfolio should perform well enough to cushion the downside risk.

Closing Thoughts: But… the dividend portfolio lacks oomph? No big upside potential?

The biggest risk though, seems to be that there is no real oomph to the portfolio.

You know, in the inflation / soft landing scenario – you may see US tech stocks / crypto going up 50%.

And yet this portfolio probably only returns 5-10% in that scenario.

So it goes back to the kind of investor you are.

Some investors are completely fine watching the market going up 25%, as long as their portfolio delivers the 6% targeted return they are happy.

Some investors will watch the market go up 25% and all their investing discipline goes out the window, and they sell their existing positions to chase the hottest new thing.

You need to know the kind of investor you are.

For me personally, I feel that a portfolio like that above lacks the upside potential if we get a global liquidity boom.

To add on that kick into the portfolio, I suppose you could throw in US AI stocks or crypto for the more adventurous, or something like the S&P500 or NASDAQ 100 for the less adventurous.

Personally for me I would probably go with a selection of US tech stocks, and with some AI exposure, and you can see the names I am buying (or selling) on FH Premium.

There have been huge moves in stock prices the past few weeks, with lots of opportunity in markets.

I will be updating my stock and REIT watchlist this weekend on the names that I am keen to buy, do sign up for FH Premium if you are keen.

Never miss another post from Financial Horse!

Follow Financial Horse on:

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

Hi FH, thanks for the insights. Been a reader for sometime, I noted you have always focused on SG equities.

Would like to know your views passive investing in the US S&P as a core strategy? Thanks in advance!

It’s perfectly fine.

An FH Premium subscriber actually asked this as well, and this was my answer:

“I think the biggest missing component is allocation to growth. I would just do something simple like the S&P500. But note that US stocks are very cyclical and volatile, so doing so will significantly increase portfolio volatility. But it brings the upside potential.”

US stocks are a great investment – if you know what you are doing and can stomach the downside risk. Volatility is much higher though, which brings its own challenges + opportunities.