A couple of weeks back, I wrote an article titled “How to earn $30,000 a month passive dividend income from investments?” (from net worth of about $8 million).

The comments I got were along the lines of “Bro FH… can you also do an article targeted more for the common man?”

Fair enough.

Exactly what we’ll do today.

What is a more realistic monthly dividend income?

I received a lot of questions on this, and I extracted some of the more interesting ones below:

FH, can you consider writing an article for common folks like us in the group on ” Can you generate 1600 a month income by investing in Reits, Dividends shares and in perpetual annuity like Pruwealth for those in the mid 30s to 40s? (on a 400k portfolio as of now). Much appreciated by most of the common folks in the group

And:

You have written several articles of such nature which are beneficial.

However would you be able to write something on someone with $50-100k sum which I believe will benefit more audience many of us are just common folks. Thanks!

I asked a bit more about his current dividend portfolio

Curious, I asked the first reader a bit more about what his current portfolio looks like, and roughly what he’s looking for.

Can withstand volatility in shares and reits. 50% of the shares should be in the 2 banks. SIA, STE, and Vicom.

30% holdings in perpetual annuity, 30% in local shares and Reits. 10% in PRU Hk shares, The rest not sure where to invest.

Just needs to make decent money, just that I only have knowledge in these few stocks.. so stay in the tried and tested

Oof… that’s awfully specific

Immediate reaction was oof – that’s awfully specific about what he wants.

That 50% has to be in 2 banks, SIA, ST Engineering, and VICOM.

The way I see it, in investing you don’t need to be too dogmatic about what you buy.

You buy whatever will go up in price (and make you money), and you manage your risk well.

That’s all there is to it.

There’s no need to complicate things further by saying that hey I only want to make money buying x stock.

How to generate $1600 a month passive income by investing in Dividend Stocks, REITs and T-Bills etc

What is the dividend yield you need to achieve on a $400,000 portfolio?

Assuming $1600 a month in dividends.

That works out to a yearly dividend of $19,200.

On a $400,000 portfolio, that’s a 4.8% yield.

So in all honesty, it’s actually should be achievable without taking on too much risk.

Launch of Dividend Investing MasterClass – Massive Launch Discount!

Before I dive in, just a quick update that I’ve been working on this the past 3 years, and it’s finally done – the Dividend Investing MasterClass.

The Dividend Investing MasterClass is a complete all in one course.

That teaches you the fundamentals on constructing a dividend portfolio – to achieve the cash flow you need to achieve financial freedom, while managing risk.

Whatever your stage of life, if you’ve ever wanted to build a dividend portfolio, this is the course for you.

We’re launching with a special launch promo – a huge discount from the official course price, and complimentary access to FH Premium thrown in!

Check out more details here.

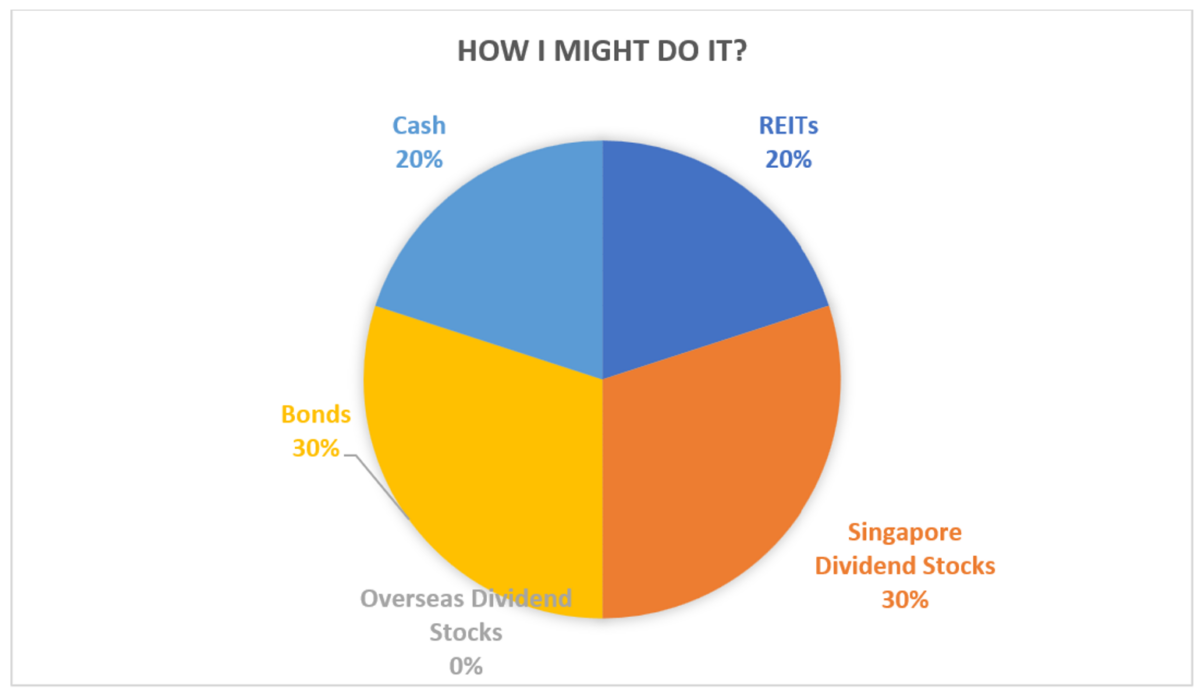

How I might do it?

I thought about it, and this is the rough asset allocation I might use:

| Asset Class | Percentage | Amount | Dividend Yield | Monthly Dividend |

| REITs | 20% | 80,000.00 | 6.0% | 400.00 |

| Singapore Dividend Stocks | 30% | 120,000.00 | 5.5% | 550.00 |

| Overseas Dividend Stocks | 0% | – | 7.0% | – |

| Bonds | 30% | 120,000.00 | 5.5% | 550.00 |

| Cash | 20% | 80,000.00 | 3.0% | 200.00 |

| 100% | 400,000.00 | 1,700.00 |

Sharing my thought process on the asset allocation?

Let me address the big questions that would crop up.

Why only 50% in REITs and Dividend Stocks? Rest in cash and bonds?

The way I see it.

If I merely need to achieve a 4.8% blended dividend yield today.

Because this is a climate of higher interest rates (unlike the past decade).

I can actually achieve a good chunk of that returns just by sitting in bonds / cash instrument.

And there is no need to take on additional risk by being in equities.

The US 2 year government bond yield today sits at about 4.2%.

Assuming a 1.5 – 2% yield spread for Investment Grade Bonds.

This means that you can realistically achieve about a 5.5% yield simply buying short duration Investment Grade USD Bonds, even after hedging back to SGD to account for FX risk.

That’s just a complete sea change from the past decade where you had to sit in dividend stocks / REITs just to be able to achieve a 5%+ yield.

Stick to short duration bonds only

Of course with bonds, you want to stick to the short duration stuff only.

The US 10 year sits at 4.2%, virtually identical to the 2 year.

In my view it makes zero sense to buy the 10 year and get locked in for 10 years – and take on the risk of capital losses if interest rates go up.

Especially with Trump in office, and who knows what policies he’s going to run the next 4 years.

Better to just sit in the short duration space today, given that the yield curve is so flat.

The only risk with buying short duration is if interest rates drop a lot in the next 1 – 2 years.

But given Trump is in office, I think we look to be in a decade of structurally higher inflation / interest rates, and hence I am less worried about this risk.

Why 20% REITs, 30% Dividend Stocks?

For the 50% of the portfolio invested in equities.

Why did I split it 60-40 between dividend stocks and REITs?

Are REITs still attractive today? For a Singapore dividend portfolio?

A lot of you have been asking for my views on REITs today.

The short answer is that after the sell-off, I sure like REITs a lot more today than I did just 2 months back when REITs were trading at close to 2 year highs.

But remember what I said above about this perhaps being a decade of structurally higher inflation and interest rates?

Especially now with Trump in office for the next 4 years?

Well if I am right on that, that’s just a very different paradigm for REITs.

Yes you will still be able to enjoy a decent 5 – 6% dividend yield.

And yes rentals are going up, and with falling interest expenses you may see DPU growth going forward.

But structurally, this paradigm may not offer the same tailwinds for REITs as it did the past decade when interest rates were stuck at zero.

Hence this goes back to position sizing, in that you want to manage your overall exposure to the REITs asset class.

Why even buy REITs in that case?

I suppose the question would be – why even buy REITs in that case.

Why not just invest it all in bank stocks and enjoy the 6% yield, with earnings growth and capital growth potential?

And I suppose the answer there is diversification.

You simply don’t want to put all your eggs in one basket.

There are some scenarios such as a recession where interest rates get cut drastically, that would be terrible for banks, yet not so bad for REITs.

And at this price after the sell-off, I think REITs are starting to look attractive as a dividend play again.

It’s one of those where as a Singapore dividend investor – I don’t think you can afford to run zero exposure given that the market is only this big.

But the better question is how much exposure.

I settled on a 60-40 split, but of course feel free to disagree with me.

Why no Overseas Dividend Stocks?

What about overseas dividend stocks?

China banks like ICBC pay a 7%+ dividend yield today, are they a good buy?

Despite all the negativity over China, you can see how ICBC actually is up 40% from 2023 lows, and has been trending up since early 2024.

You could literally have bought China banks last year on all the negativity, and be up 50% total returns wise (including dividends) through all the doom and gloom.

Even if you don’t like China banks, other dividend plays like China Mobile (Telco) or CNOOC (China Oil) pay 7%ish dividend yields.

Are China dividend stocks a good buy?

This is a tricky one – and goes back to risk appetite.

If you know what you’re doing, and you understand the risks of investing in China, I think valuations here are very cheap for patient, long term investors.

But even so – you want to position size well.

If you’re not familiar with China, and you are the kind prone to panic selling if price drops, then better to just stay away.

Personally I run China exposure, but currently it’s sized at around 10% of my portfolio, and I would only increase further in size once I have confirmation signs of meaningful consumer stimulus from Beijing (and the charts confirm this).

No right or wrong here – I leave each investor to figure out the answer for themselves.

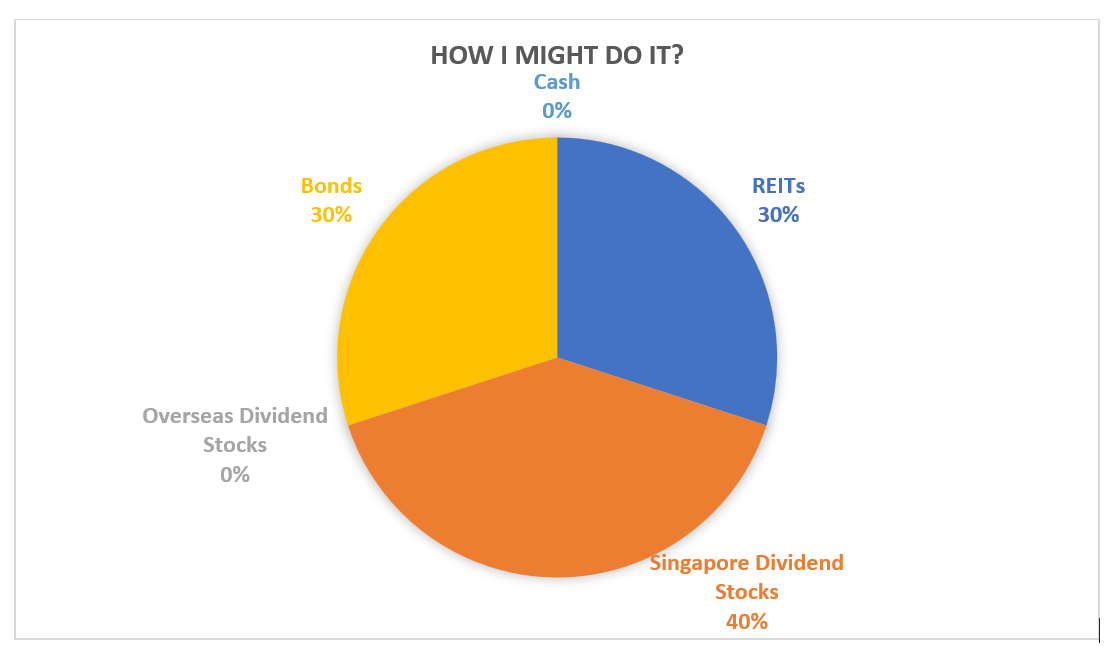

Is 20% cash too low or too high?

Note that this portfolio includes 20% cash, for the simple reason that I wasn’t sure whether the $400,000 number was meant to be fully invested, or whether it included the reader’s entire “investible” sum.

Assuming you already have emergency funds stashed away, and the portfolio is meant to be fully invested at all times.

I suppose it could be adjusted to something like this instead:

| Asset Class | Percentage | Amount | Dividend Yield | Monthly Dividend |

| REITs | 30% | 120,000.00 | 6.0% | 600.00 |

| Singapore Dividend Stocks | 40% | 160,000.00 | 5.5% | 733.33 |

| Overseas Dividend Stocks | 0% | – | 7.0% | – |

| Bonds | 30% | 120,000.00 | 5.5% | 550.00 |

| Cash | 0% | – | 3.0% | – |

| 100% | 400,000.00 | 1,883.33 |

But as you can see, it’s quite a substantial increase in risk, for just an extra $183 a month in dividends.

In my view, that’s just not worth the risk.

Keeping 20% of the portfolio in cash provides a lot of flexibility if (and when) a market sell-off comes around.

And given that cash is yielding 3% today, the opportunity cost of being in cash is not that significant.

What single stocks would I buy for the dividend portfolio?

I didn’t want to go too much into single names as that’s what the rest of Financial Horse is for.

But I figured I would share some high level thoughts on stock picking here.

For the REITs, I would stick primarily with Singapore properties.

And make sure its from a solid blue chip Sponsor, with a sound balance sheet.

I just think that in this climate, overseas real estate is too risky unless you know exactly what you’re getting yourself into, and the interest rate volatility means that you want as strong a balance sheet as you can to tide through whatever is to come.

For dividend stocks – this is probably going to be primarily the bank stocks.

I might throw in a smattering of the GLCs too, as some of them are looking quite attractive to me today, and offer attractive dividend yields.

The Dividend Investing MasterClass goes into much greater detail on this – what to analyse when picking dividend stocks / REITs, what red flags to watch, how to manage risk, position size single stocks and so on.

Do check it out if you are keen.

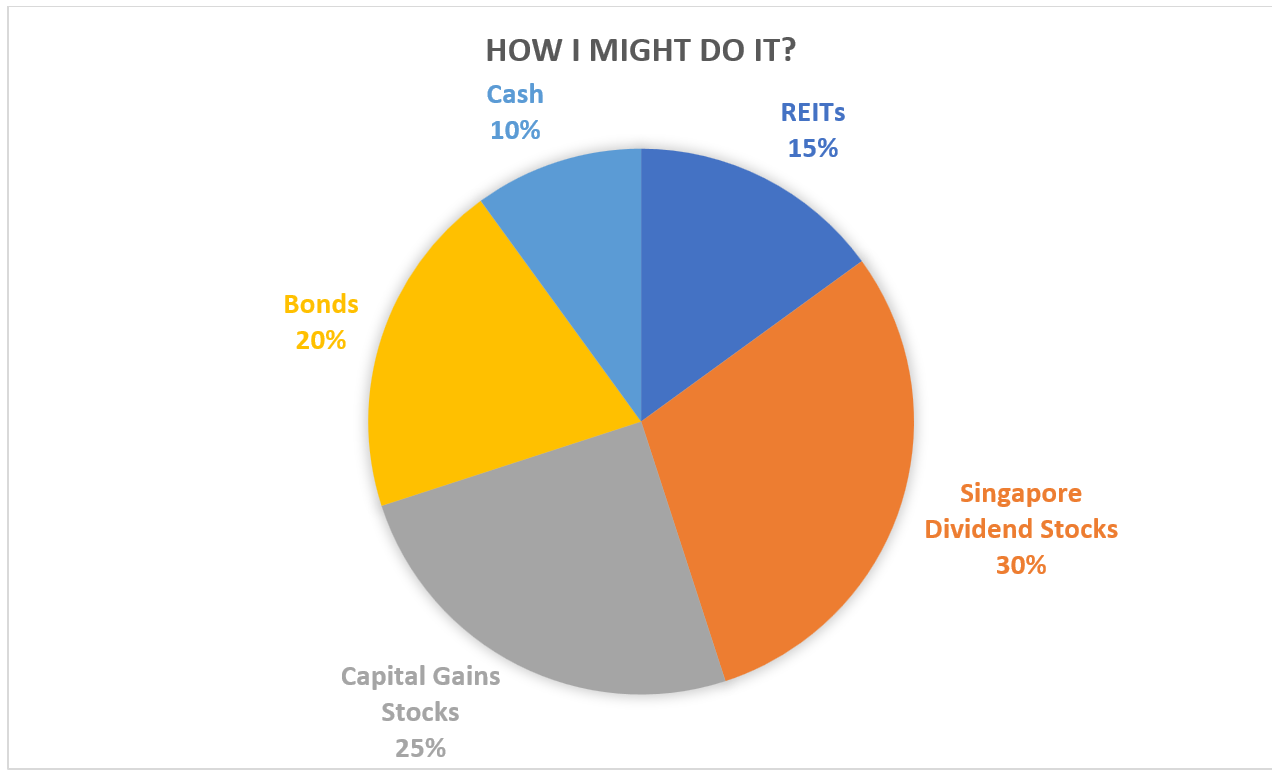

What if you want more capital gains potential?

Final point.

The portfolio is mainly concentrated in dividend / yield style plays.

This was by design because the question was on creating a portfolio to generate monthly dividend income.

But what if the goal was for more of a balance between capital gains and dividends?

I suppose the answer is straightforward – mix in some capital gains stocks, whether it’s US Tech or Crypto (or whatever your favourite capital gains play is):

| Asset Class | Percentage | Amount | Dividend Yield | Monthly Dividend |

| REITs | 15% | 60,000.00 | 6.0% | 300.00 |

| Singapore Dividend Stocks | 30% | 120,000.00 | 5.5% | 550.00 |

| Capital Gains Stocks | 25% | 100,000.00 | 0.0% | – |

| Bonds | 20% | 80,000.00 | 5.5% | 366.67 |

| Cash | 10% | 40,000.00 | 3.0% | 100.00 |

| 100% | 400,000.00 | 1,316.67 |

The implications of course, is that this drastically changes the risk profile of the portfolio.

And you can also see how the monthly dividend income falls quite drastically.

Capital gains are not as consistent as dividends, and by its very nature carries with it a lot more volatility (both on the upside and downside).

So it really goes back to what you’re looking for.

I would say for younger investors, you probably want to run a bigger exposure to capital gains plays to build wealth aggressively.

If you’re more advanced in your investment journey, and your investment portfolio is already very large, tilting more heavily towards dividend plays may make sense.

Launch of Dividend Investing MasterClass – Massive Launch Discount!

If you found the discussion above useful, and want to go into further details on how to build a dividend portfolio while managing risk.

You’ll want to check out the Dividend Investing MasterClass.

The Dividend Investing MasterClass is a complete all in one course.

That teaches you the fundamentals on constructing a dividend portfolio – to achieve the cash flow you need to achieve financial freedom, while managing risk.

Whatever your stage of life, if you’ve ever wanted to build a dividend portfolio, this is the course for you.

We’re launching with a special launch promo – a huge discount from the official course price, and complimentary access to FH Premium thrown in!

Check out more details here.