I’ve been getting some pretty interesting questions on how to invest in today’s investment climate.

Here’s one of them:

Dear FH:

Been following you and read your articles with interest.

I am aged 50 plus and thinking about how to set up a portfolio to generate net cash of SGD30k.

My wife and I don’t live in SG at the moment.

We own properties in SG which are all not income generating at the moment.

Wanted to get your thoughts on the right way and fuss free to generate the desired return in a consistent way as we age.

1. Assume the free cash amount to be SGD8m (without paying down the mortgage under 2 below).

2. Landed FH houses and not rented out. Thinking of selling one of them and swap into an orchard road condo and then incur a mortgage of SGD4.5m. And so keep one fully paid landed house. Hoping to work for another 2-3 years and make use of “leverage”. Make sense to do this?

3. My wife mainly trades stocks in U.S. and HK. Overall position about HKD5.0m worth. So not much exposure.

The target of SGD30k is for both wife and husband so 15k each. It is really the hope to sleep better at night as you age and reduce financial monitoring or engineering. Not good at those things anyway. Was thinking of doing just all rental properties and living off rental income – but yield is so poor!

I guess the heart of the question is – for non financially savvy people – is it better to allocate more to properties even if the yield is lower?

And how much leverage is “good” leverage for someone at age 50 plus. 🙂

FH Response?

It’s a pretty interesting question, and I thought it may be useful for others out there.

So I figured I would share some views here, but of course this should not be taken as financial advice as I do not know the full picture of the investor’s financial situation.

There’s basically 4 key question:

- How to generate 30k income a month on 8m cash? Is this feasible?

- Sell landed freehold house and swap into an orchard road condo?

- For non financially savvy people – is it better to allocate more to properties even if the yield is lower

- How much leverage is “good” leverage for someone at age 50 plus.

How to generate $30,000 income a month on $8m cash? Is this feasible?

$30,000 income a month is $360,000 a year.

On $8 million free cash that’s 4.5% yield.

So the fundamental question here is whether you can reliably generate a smooth 4.5% yield (be it capital gains or dividend) on an $8 million portfolio.

In a simple, fuss free way, for someone who is not financially savvy.

I would say the answer really depends on the financial sophistication of the investor, and your ability to navigate financial markets.

Sophisticated Investor that is able to navigate the ups / downs of financial markets?

If you’re sophisticated, you can invest that full 8 million in a 100% equity portfolio.

You could see double digit returns in a good year, and in a bad year hopefully flattish (avoiding any big drawdowns).

But this approach does require careful risk management, because there are some years where the drawdown can get pretty horrendous (think 2008, 2020 or 2022).

If you don’t manage risk well, you could be sitting on pretty big paper losses on such years.

Not so sophisticated investor?

What if the investor is not so financially savvy?

Let’s say the approach is to reduce risk via passive asset allocation.

There are a couple of ways to do this, and let’s talk through them:

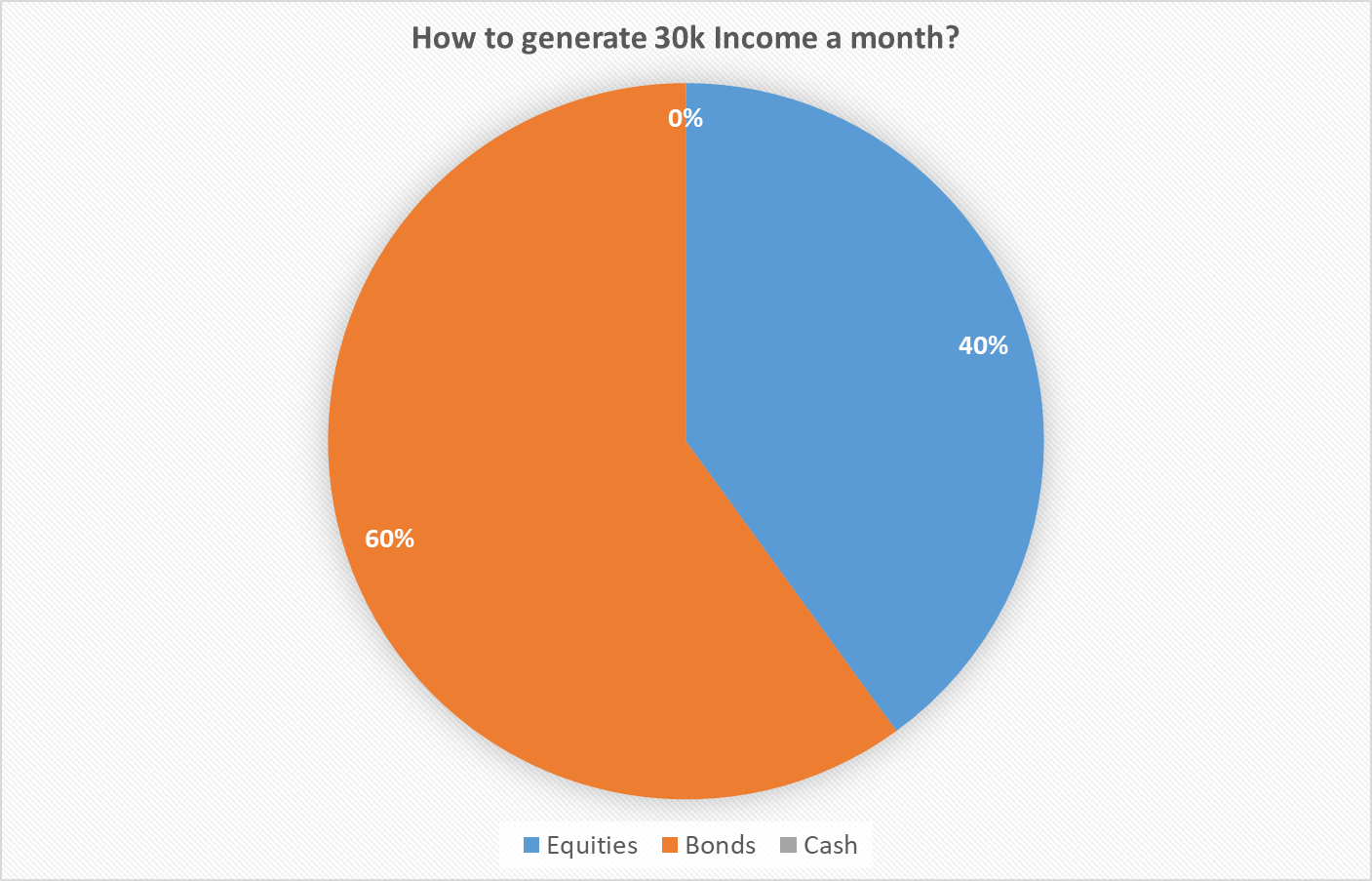

60/40 Bond-Equity split

Let’s start with the most basic – a 60/40 split.

Say you put 60% of the portfolio into a portfolio of low risk investment grade bonds hedged back to SGD.

And then you put the remaining 40% into a mix of equities – Singapore banks, REITs, US stocks.

Let’s say the bond component yields about 5.5% today (pretty achievable with about 3 – 5 year duration).

That’s $22,000 a month.

For the $8,000 a month shortfall – that means you need a 3% total return on the remaining 40% of the equities portfolio.

In a good year that should be no problem.

But in a bad year the equity portfolio may see losses (which I presume is the case since this would be a passive portfolio that tracks the market).

Maybe the bonds will appreciate in value to offset the equity losses, but given this new paradigm of structurally higher inflation / interest rates – you never really know.

So generally speaking, this approach is not so straightforward and may result in lumpy earnings.

There’s no easy way to generate “smooth” cash flow from the stock component, without getting active and really into the weeds.

Yes I know there are options such as buying downside protected S&P500 ETFs to cut out downside risk, but I do think that requires some sophistication and understanding of what you are buying.

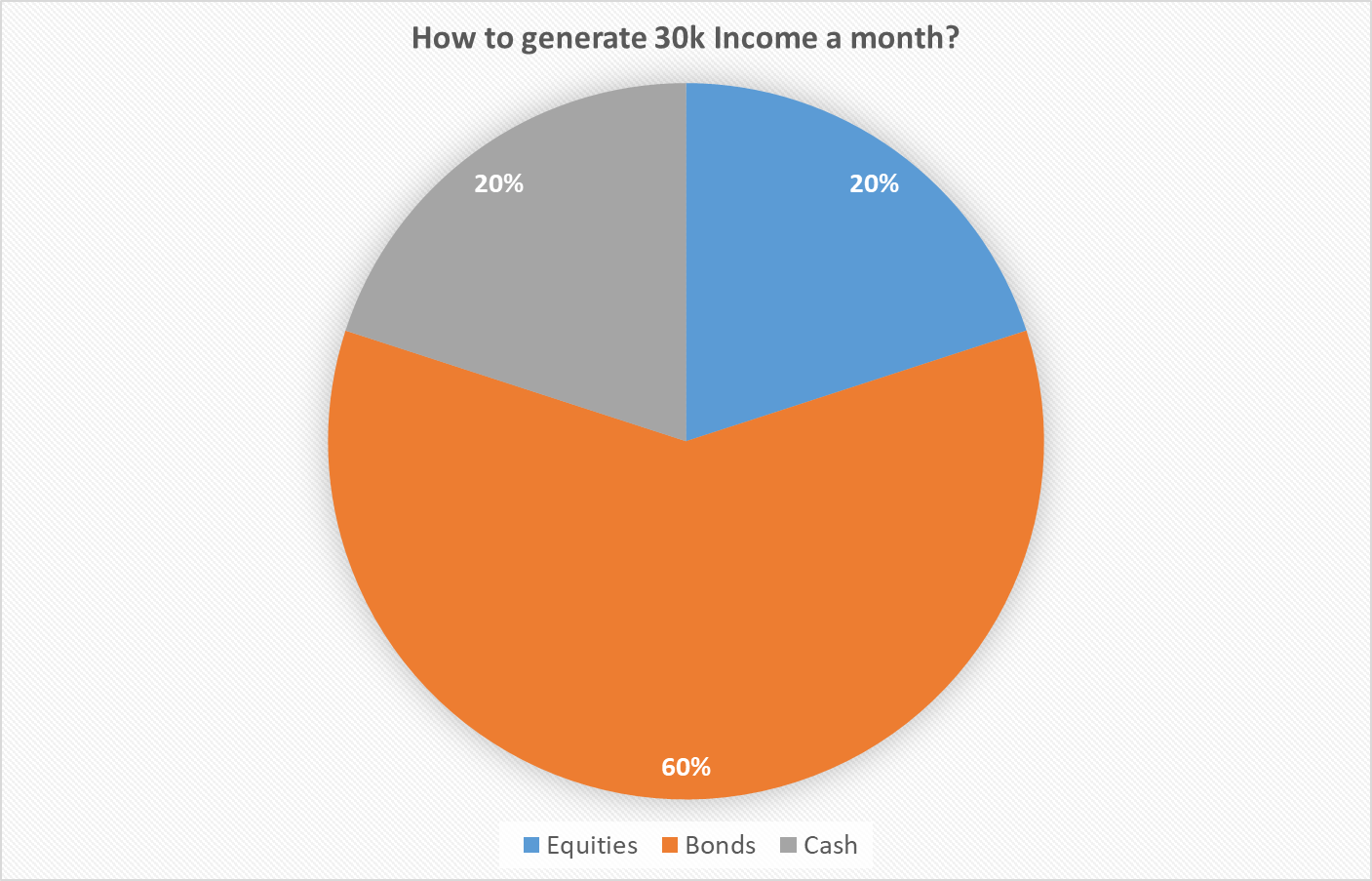

What if you reduce the Equities component? 60/20/20?

So the fundamental problem above is that equities volatility is high.

What if you reduce the equities component?

Say you dropped equities to 20% of the portfolio, and replaced that with cash.

Realistically the cash yields about 3.0% today, which means that you can hit a $26,000 a month income even before you count the equities component.

So in a good year the stocks do well and all is great.

In a bad year the equities go down, but since it’s only 20% it’s not the end of the world.

This could be a better approach than the pure 60/40, although it does sacrifice returns.

Follow Financial Horse to avoid missing any post!

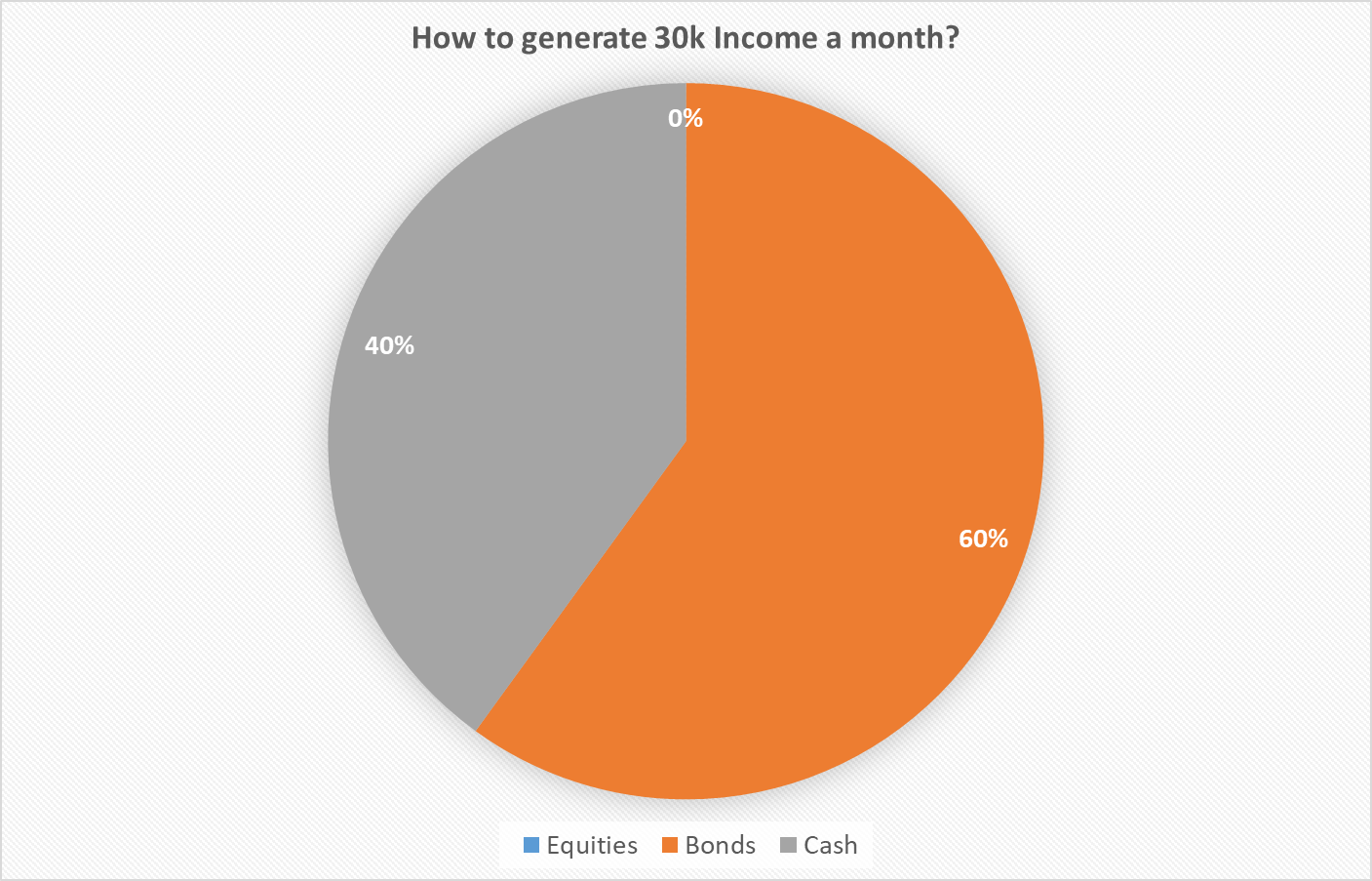

What if you switch to no equities?

What if you want something even safer?

Say you drop the equities component entirely.

Put 60% into bonds, and 40% into cash.

Funnily enough – that still gets you to $30,000 a month.

What is the risk of no equities? No inflation hedge?

The biggest risk of running zero equity exposure is of course – inflation.

When you hold bonds/cash, the maximum upside is capped at the yield.

Whereas if you buy stocks, then theoretically there is no cap on the upside.

And I have my fears that with Trump back in office, and the Feds on a rate cut path, and financial markets powering to all time highs, we could see the return of inflation in 2025.

If you don’t hold any stocks, my main gripe is that you do need something that can hold its own against inflation (especially since the investor is only in his 50s).

Which is probably a good time to discuss the next option.

Sell landed freehold house and swap into an orchard road condo?

The real estate option:

Landed FH houses and not rented out.

Thinking of selling one of them and swap into an orchard road condo and then incur a mortgage of SGD4.5m.

And so keep one fully paid landed house.

Hoping to work for another 2-3 years and make use of “leverage”.

Make sense to do this?

Was thinking of doing just all rental properties and living off rental income – but yield is so poor!

I’m going to go out on a limb and say that if you buy Singapore properties today (with a mortgage of 75% LTV).

Generally speaking the investment will not be cash flow positive – as almost all the rental income generated will have to go back into property expenses (mortgage repayment, maintenance, agent fees etc).

The cash generated will only be the excess cash between what was gained from the sale, and what was invested into the new home.

The situation is different had you bought the property pre-2022, but based on today’s prices that’s how I see it.

The benefit of course is that the freehold houses are not rented out today (not generating income).

By switching into a condo they will be able to generate rental income – but do note there are pretty hefty transaction costs in terms of agent fees and stamp duty.

Query also whether there is another option for the landed free houses to be leased out to generate some rental income, but I suppose there is a good reason why that has not already happened today.

Ultimately though, I don’t really see how the real estate solution solves the cash flow issue, this is more of a capital gains / total return kind of play.

It’s okay if the goal is to generate total returns, but if the goal is to generate monthly cash flow I’m not sure this will work unless you buy the property without a mortgage (or a small mortgage).

For non-financially savvy people – is it better to allocate more to properties even if the yield is lower

Coming back to this question.

I think investing this decade is much more dynamic (or volatile) than last decade.

And it requires a more active approach, unless you are fine to be pure passive and just eat any big drawdown in markets.

The past decade was one where central banks pumped in liquidity constantly, suppressing volatility.

Whereas this decade the return of structural inflation means a much more bumpy ride for equities.

So if your goal is to generate a smooth 4.5% yield on a 8m portfolio, without any big drawdowns, and you want to do it in a passive approach.

Well I just don’t think it will be that smooth.

You will have years where you generate double digit returns, you will have years where you may undershoot the 4.5% yield.

So the question is whether that is something you can live with.

Property investment is “smoother”?

The benefit with properties – is that the earnings is much “smoother”.

Part of this is artificial, because unlike stocks, properties are not marked to market on a daily basis.

So you just collect your monthly rental, and you “ignore” the market price of the properties.

That’s a lot harder to do with stocks.

So short answer – if indeed you’re not financially savvy and want a “smooth” approach, it is possible that buying properties may be the better play.

Note that when I say properties I’m only referring to Singapore residential property, and I’m assuming you can buy without incurring ABSD.

The analysis for other real estate, or with ABSD, if quite different.

Which option generates a higher total return? Stocks or Real Estate?

Let’s say you’re comfortable sitting through the stock market volatility.

Buying a basket of stocks today and holding for 10 years, vs buying Singapore residential property and holding for 10 years.

Which will generate the higher total return?

Boy… that is a really tough question.

Because don’t forget with real estate the 75% leverage can really juice your return on equity, if indeed property prices outpace inflation.

And don’t forget this question is for the next 10 years, not the past 10 years.

To be absolutely honest – this is not a question I have a high conviction answer on.

What would I do?

I would say if you can afford it – just buy both.

Buy stocks, and buy real estate.

And make sure you have enough cash to survive regardless of how bad things get (which means don’t overleverage).

The list of stocks / REITs I am invested in (and keen to buy more of) are shared on FH Premium.

How much leverage is “good” leverage for someone at age 50 plus?

This final question goes back to risk appetite.

If you’re risk adverse, you definitely don’t want to run such a high leverage ratio.

My personal view?

If I were in a similar situation, I think I’ll probably just go ahead and max out the 75% LTV on the property purchase.

With Feds on a rate cut path, and Trump in office.

I think maxxing out a mortgage at 2.45% today to buy hard assets is something I would do (as long as you have enough cash to cover the mortgage if things head south).

Especially so for an investor with $8m free cash to cover the mortgage if things get hairy.

And worst case if short term interest rates are much higher on refinancing, the mortgage can always be paid off at that time.

The difference is that Singapore residential real estate is much less volatile than stocks, so I would be more comfortable running higher leverage on Singapore residential real estate than other asset classes.

But that’s just how I see it, and there is no right or wrong here.

For those who are risk averse, no doubt the better choice may be to not take on so much leverage.

Closing Thoughts: Do you want to get rich(er), or do you want to not be poor?

Ultimately though – it comes back to the question of do you want to get rich(er), or do you want to not be poor.

That’s the fundamental question, and all the investment decisions flow from there.

The options for growing wealth by its very nature entail some risk, so the question is whether you are comfortable with that risk.

Whereas if you are already comfortable with your current financial situation – then there is absolutely no need to risk things getting worse, and you can run a less risky approach.

This is a question only each investor can answer for themselves.

This post is written on 15 Nov 2024 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Hi, agree with your advice to max out 75% LTV on the property. Likewise, wondering why the owner can’t take out a Cash-out loan on the existing landed property. That’s what I have been doing as my landed appreciates through the years.

That’s a good point – there does look to be some room to optimise the capital structure. Currently there looks to be some wasted opportunity here.

Dear FH: After reading your article, I have 3 comments to make:

1) If someone with $8M investible assets plus a few FH landed houses in Singapore is grappling with how to generate sufficient passive income to fund his golden years, it makes me wonder if the common folks like us can ever contemplate retirement?

2) Having said that, the crux of the issue here is “how much is enough?” for one to retire happily? Do you really need $30,000 a month to retire in Singapore comfortably?

3) If I have his/her net worth, I will engage a professional to plan my retirement. Why sweat when you don’t need to?

Haha for what it’s worth, my thoughts below:

1) I think you hit the nail on the head with point (2). It is about how much is enough. Some of us may be able to get by on 2k a month, some of us would be unhappy on 30k a month. There’s no right or wrong here – it’s all about what you expect.

3) I dont think this is so straightforward. At 8m net worth, it is still worth nothing to the private banks. And you never really know if the professional has your true interests at heart, or is just out to milk you for fees. Best to apply a critical lens to it, and decide what is best for yourself.