Okay, so I wasn’t planning on doing this post.

But then I was reading the Link REIT acquisition of Jurong Point.

And posting quick thoughts on Twitter (do follow me on Twitter if you haven’t already).

And the more I looked at it, the more interesting this deal become.

So here goes… 3 key takeaways on Link REIT’s acquisition of Jurong Point.

3 Key Takeaways on Link REIT’s acquisition of Jurong Point

- Are Commercial Real Estate valuations going down?

- Financing is not cheap for Link REIT

- Are REITs in trouble?

Are Commercial Real Estate valuations going down?

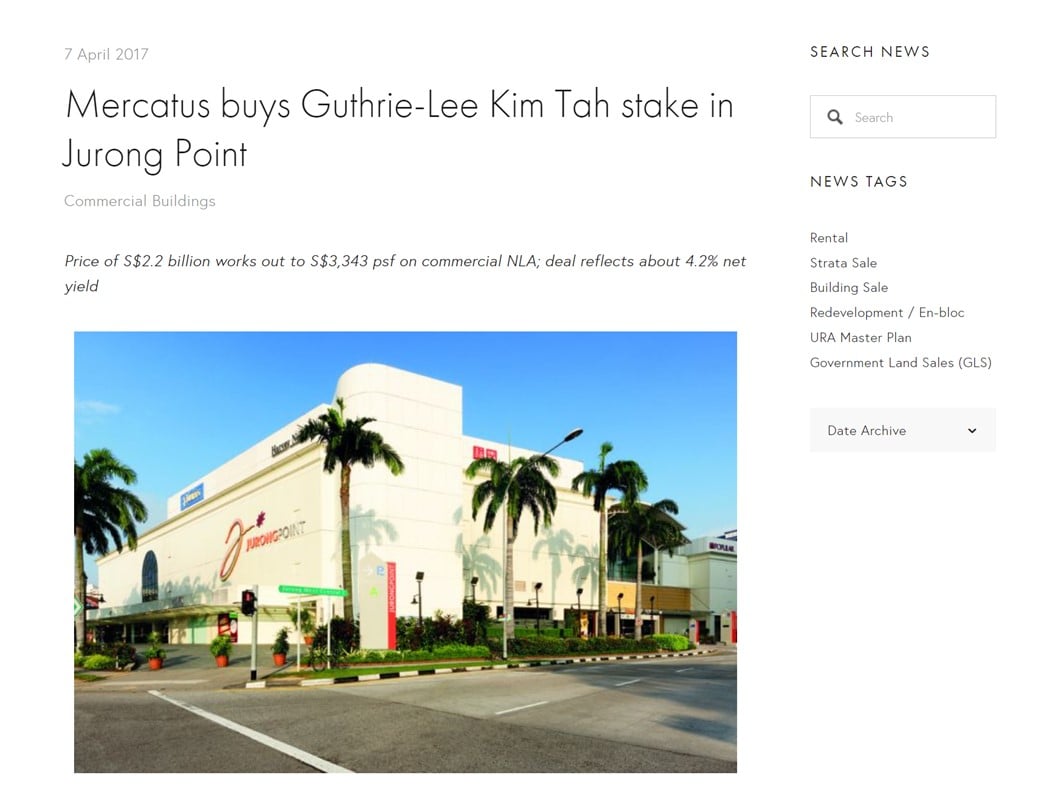

I must admit this horse doesn’t have the best memory.

But I do vaguely recall Mercatus buying Jurong Point for quite a large number a while back (Mercatus being the seller, owned by NTUC).

And sure enough, Mercatus bought Jurong Point for $2.2 billion back in 2017.

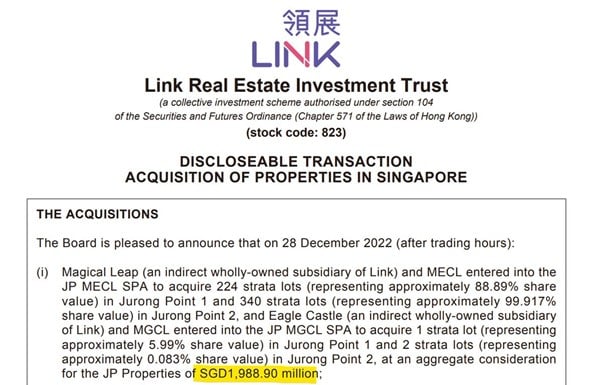

And 5 years later, in 2022.

Mercatus is selling it for $1.988 billion to Link REIT.

Approximately a 10% drop in valuation.

In real estate speak – that works out to about a 4.8% cap rate (versus the 4.2% cap rate that Mercatus paid in 2017).

For those who are newer to real estate, cap rates tell you how expensive a property is, and the higher it is, the “cheaper” it is.

So simplistically – Jurong Point is cheaper today than it was in 2017.

I suppose there are only 2 ways to interpret this.

Either (1) Mercatus overpaid in 2017, or (2) commercial real estate prices are going down.

Is there a third option?

I suppose there is a third option that Link REIT got a good deal.

Because you know… they are savvy negotiators?

But considering that both CapitaLand (via CICT) and Frasers (via FCT) were both rumoured to be looking at the deal as well, it doesn’t seem like the case.

It seems like Mercatus did do proper price discovery with a few potential buyers, and this is close to the “best” price they could have gotten given current market conditions.

So… overpaid or are real estate prices going down?

As to whether it’s (1) or (2), I leave it to you to decide.

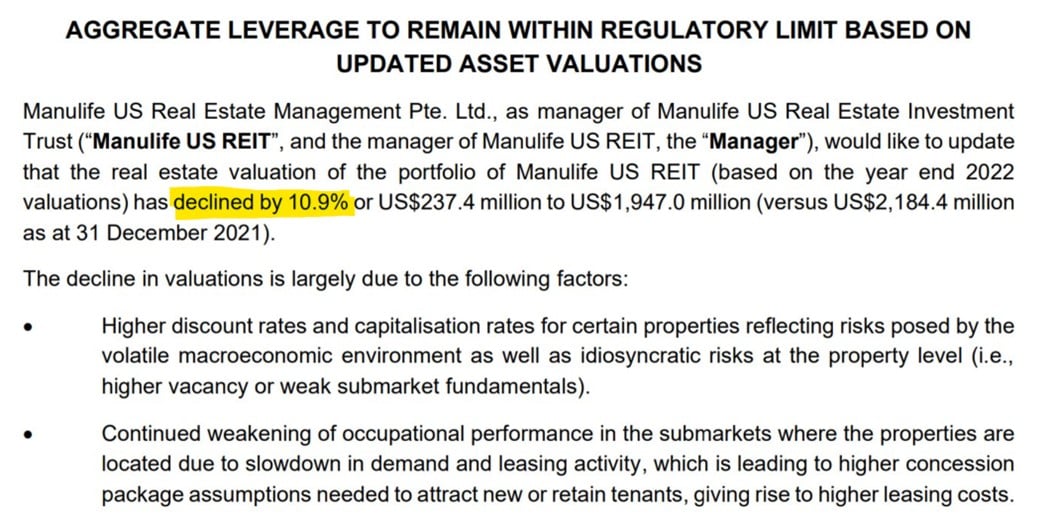

Although interestingly, just this week, Manulife also announced that they are revaluing their property portfolio downwards by 10.9% due to (1) higher interest rates (resulting in higher cap rates) and (2) weakening US submarket performance.

So… it does lend some support to the view that commercial real estate prices are weakening.

I’ve been talking for a while about how real estate prices valued in an era of 0% interest rates, no longer make sense when interest rates are going to 5%.

Is this a sign of things to come?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Financing is not cheap for Link REIT

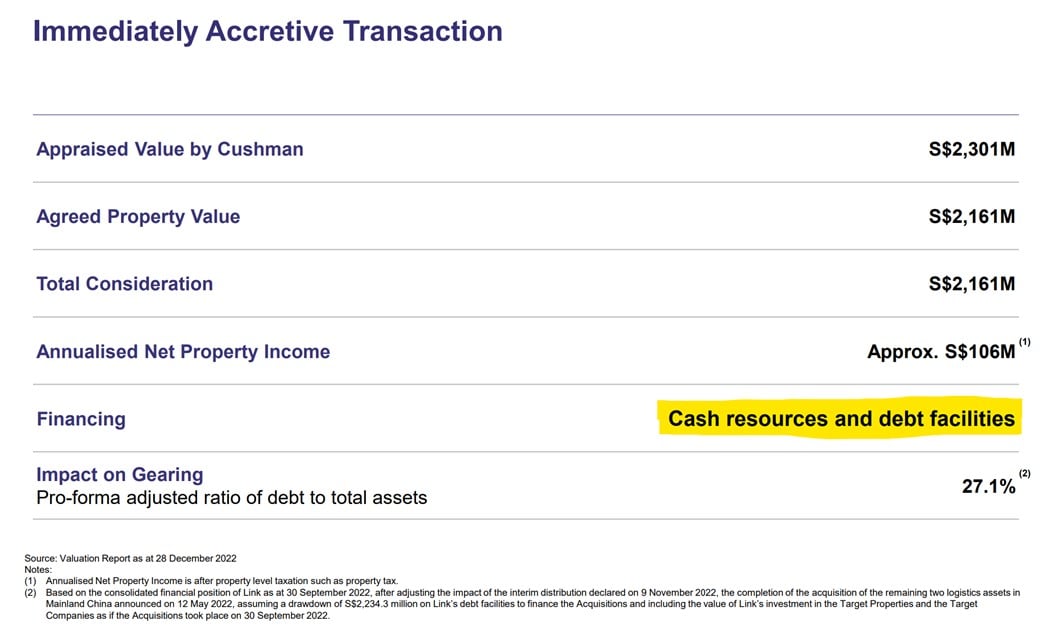

So… who in their right mind would buy $2.16 billion worth of real estate in this market you ask.

And how would they fund it?

Yeah… exact same questions I had.

Turns out Link REIT is funding it via cash and debt.

Their gearing is only 27.1%, so I suppose they do have a lot of debt headroom.

That said, debt still has a cost.

Link REIT raised S$568 million recently via convertible bonds.

At 4.5%.

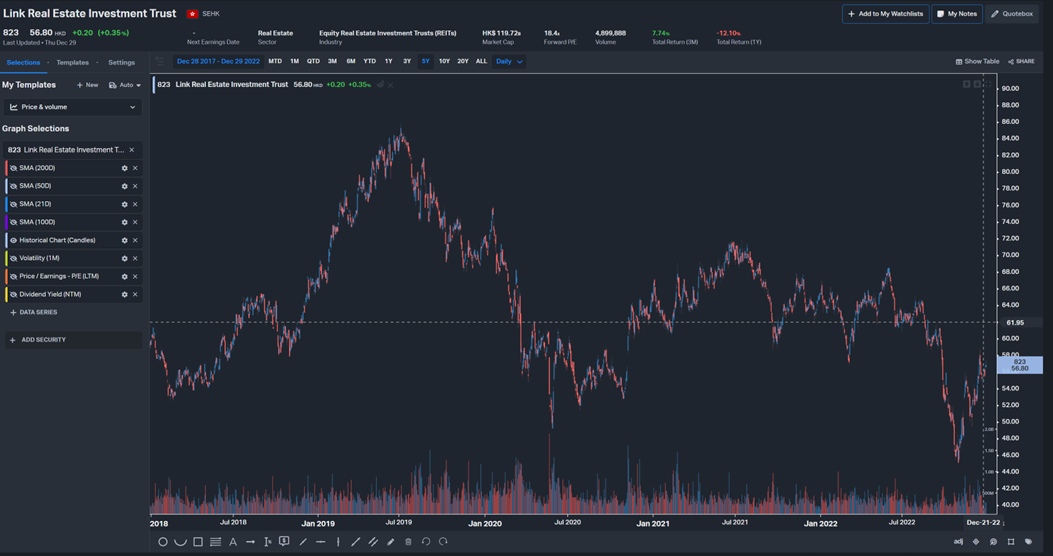

But here’s the kicker – the conversion price (where the bonds can be converted into Link REIT Units) is $61.92.

For a REIT where the NAV is $80.86.

You can see the conversion price marked below, where Link REIT spent a good part of the past 5 years trading above.

I suppose what I’m trying to say, is that debt does not come cheap in this market.

4.5% convertible debt, with a conversion price that is (1) only 10% above current price, and (2) below NAV.

To buy real estate at a 4.8% cap rate.

Man… I can see why nobody is doing deals in this market.

The financing just doesn’t make sense.

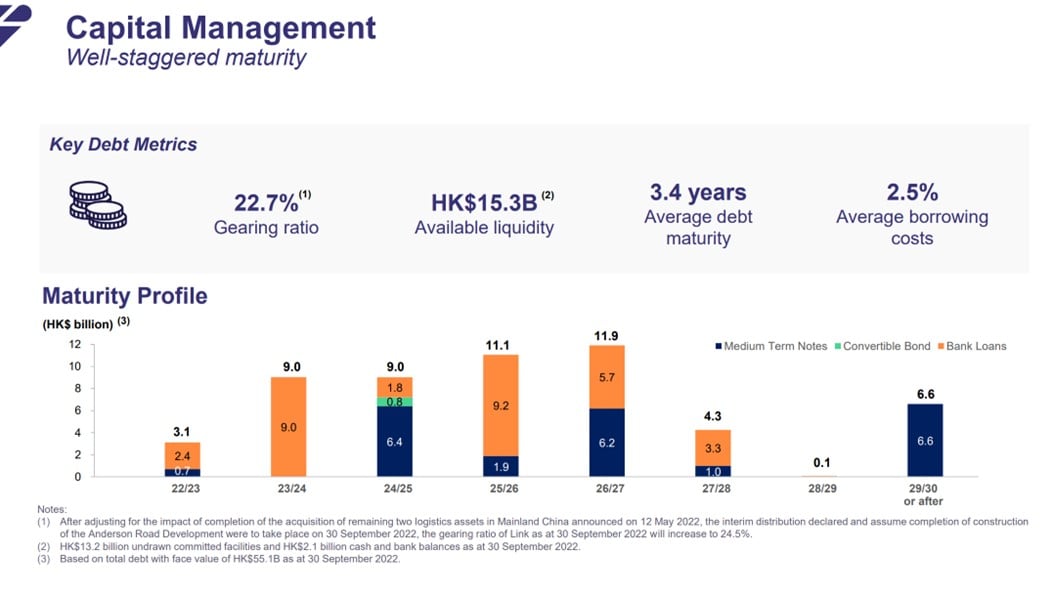

For what it’s worth, Link REIT’s average cost of debt is 2.5% for now, but one expects that will surely increase going forward

So… why did Link REIT buy Jurong Point? And why did Mercatus sell?

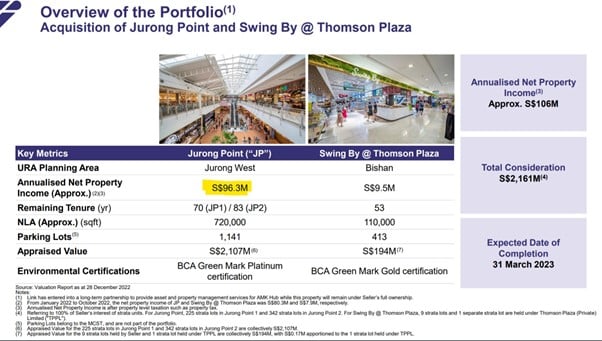

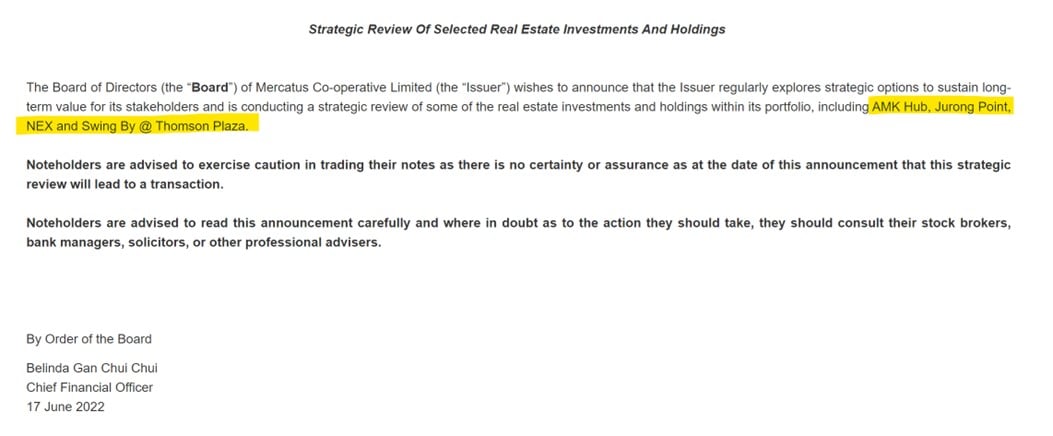

If you recall, the original property portfolio was for (1) AMK Hub, (2) Jurong Point, (3) NEX and (4) Swing By @ Thomson Plaza.

Nex was taken out of the deal entirely.

While AMK Hub was taken out of the deal, but the sweetener is that Link REIT gets to manage AMK Hub “long-term”.

One assumes that this is a precursor to Link REIT eventually buying AMK Hub…

The fact that this had to happen, with both CICT and FCT pulling out of the deal (reportedly), is interesting.

I do have my own theories on why it played out this way, but that’s ultimately going to be speculation.

In any case, I suppose from Link REIT’s perspective, this acquisition can be seen as a longer term strategic move, to expand into Singapore.

And to diversify away from Hong Kong and Mainland China.

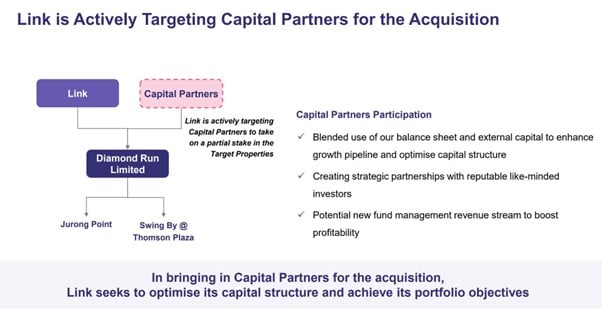

Interestingly, Link REIT is looking for partners for the acquisition.

So perhaps indeed, this acquisition is too big for them (or any one REIT) to swallow in this market conditions.

Are REITs in trouble?

Looking at the numbers, I can see why FCT and CICT backed out.

The financing does not make sense.

You can’t tap equity at these prices, not when your share price is so low (especially if its below NAV).

The equity fund raise would be too dilutive, and the market would murder you if you tried (look at SATS for reference).

And debt… well Link REIT tried doing debt.

And it’s quite clear the debt doesn’t come cheap these days.

4.5% convertible bond with a strike price that could very easily be exercised.

That’s not a good deal, and shows how tight the debt markets are right now.

So I really struggle to see how REITs will make any acquisitions moving forward.

Everyone is expecting interest rates to come down in 2023/2024.

If they don’t, and they stay up, I think commercial real estate might be in for a world of pain.

But let’s see…

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Everything being equal, is it not a fair valuation for the price of a leasehold property to be lower now than it was 5 years ago?

Good point, I get where you’re coming from.

nice post :). still working hard over the holiday weeks I see!

What theories do you have behind why FCT and CICT pulled out of the race? Valuations of Jurong Point not low enough for them? Financing costs too high? Or is there something else?

Also, in terms of revaluation timing for underlying properties, do you have any insight into when these will be done across the industry? So for example, we saw what happened with Manulife REIT. Should we be expecting the same for others sometime in 2023?

Thanks – wasn’t planning on writing this post but I was looking at Link’s numbers and I really couldn’t help myself after that…

Yeah I didn’t want to dive into this question in the article because it would be just speculation, and I could be wrong.

Since you asked though, my suspicion is due to (1) valuation not cheap, and (2) cant work out an appropriate financing package in this market.

At 4.8% cap rate, it’s definitely cheaper than it was in 2021 (prob 4 – 4.5% cap rate last year), but not at the point where it is cheap enough that it’s a must buy (considering the risk free is going to 5%).

And at 2b, that’s a big amount to swallow, which at the very minimum would require the sponsor to hold 50% of the purchase, and the rest would need to be funded via debt/equity, both of which is not going to come cheap in this market.

So I can see why both stepped away, and I think it was the right thing to do. Market would have hammered their share price otherwise, and you can see how share price recovered once the market realised the acquisition was off the table for those 2 REITs.

The revaluation is a good question. It feels like everyone knows that a storm is coming, but nobody wants to be the first to do it. They’re going to wait until they’re forced to do so, or until someone else does it. Or hope that Powell cuts rates before they are forced to make any hard decisions.

I think the answer will go back to individual property portfolio and sponsor quality. No easy answers here.