So MSCI announced the changes to its MSCI Singapore index this week.

Mapletree Pan Asia Commercial trust (MPACT) was removed from the MSCI Singapore Index (other stocks dropped are Mapletree Logistics Trust, CDL, Jardine C&C and Seatrium).

This led to MPACT’s share price dropping as low as $1.18 at one point.

But it closed the day flat at $1.22.

Now these kind of index removal news tends to be a contrarian bottom signal.

Once the initial index selling is out of the way, the stock usually bottoms out, and as long as fundamentals do not deteriorate they can rally after.

So I decided to take a closer look at Mapletree Asia Commercial Trust.

At a 7.5% annualised dividend yield, for a REIT that holds 2 crown jewels in Singapore (Vivocity and Mapletree Business City).

Is this REIT a good buy?

Mapletree Pan Asia Commercial Trust was removed from MSCI Index – Is this a short term bottom?

5 stocks / REITs were removed from the MSCI Singapore Index this week.

Beansprout has a nice chart showing their share price decline on that day:

Now these kind of index removal news tends to be a contrarian bottom signal.

Once the initial index selling is out of the way, the stock usually bottoms out, and as long as fundamentals do not deteriorate they can rally after.

How do other REIT prices react after a removal from the MSCI Singapore Index?

For example – this is Suntec REIT’s share price after it was removed on the MSCI Index on 12 May 2021.

The stock continued to sell-off for the next 1 – 2 weeks.

But after that it made a full recovery and recovered most of the decline.

Here’s Suntec REIT overlaid against the Lion-Philip S-REIT ETF.

You can see how after initial sell-off on the index news, the share price moved back to tracking the market generally.

Removal from MSCI Singapore can be a bottom – IF the fundamentals remain strong

But of course, all of the above is assuming the fundamentals of the REIT remain strong,

If the underlying real estate doesn’t perform well, none of this matters really.

So let’s take a closer look at the fundamentals of Mapletree Pan Asia Commercial Trust.

Mapletree Pan Asia Commercial Trust is at prices last hit in 2015 – Although back then it was a very different REIT (pure Singapore)

Just zooming out a little – the long term chart for this REIT is abysmal.

Since the top at 2.48 pre-COVID, the REIT price has collapsed 50%.

Mapletree Pan Asia Commercial Trust today is trading at prices last hit back in 2015, which is unbelievable stuff.

Yes – I get that it’s basically a different REIT today as it was still Mapletree Commercial Trust back in the day (without the Hong Kong and China assets that were injected via the acquisition of Mapletree Greater China Commercial Trust).

But still – that’s a huge drop.

Mapletree Pan Asia Commercial Trust pays a 7.5% Dividend Yield

Latest DPU is 2.29 cents, which is actually up 1.8% on a year on year basis.

If you annualise this DPU using latest share price of 1.22, you get a 7.5% dividend yield.

That’s frankly not too bad.

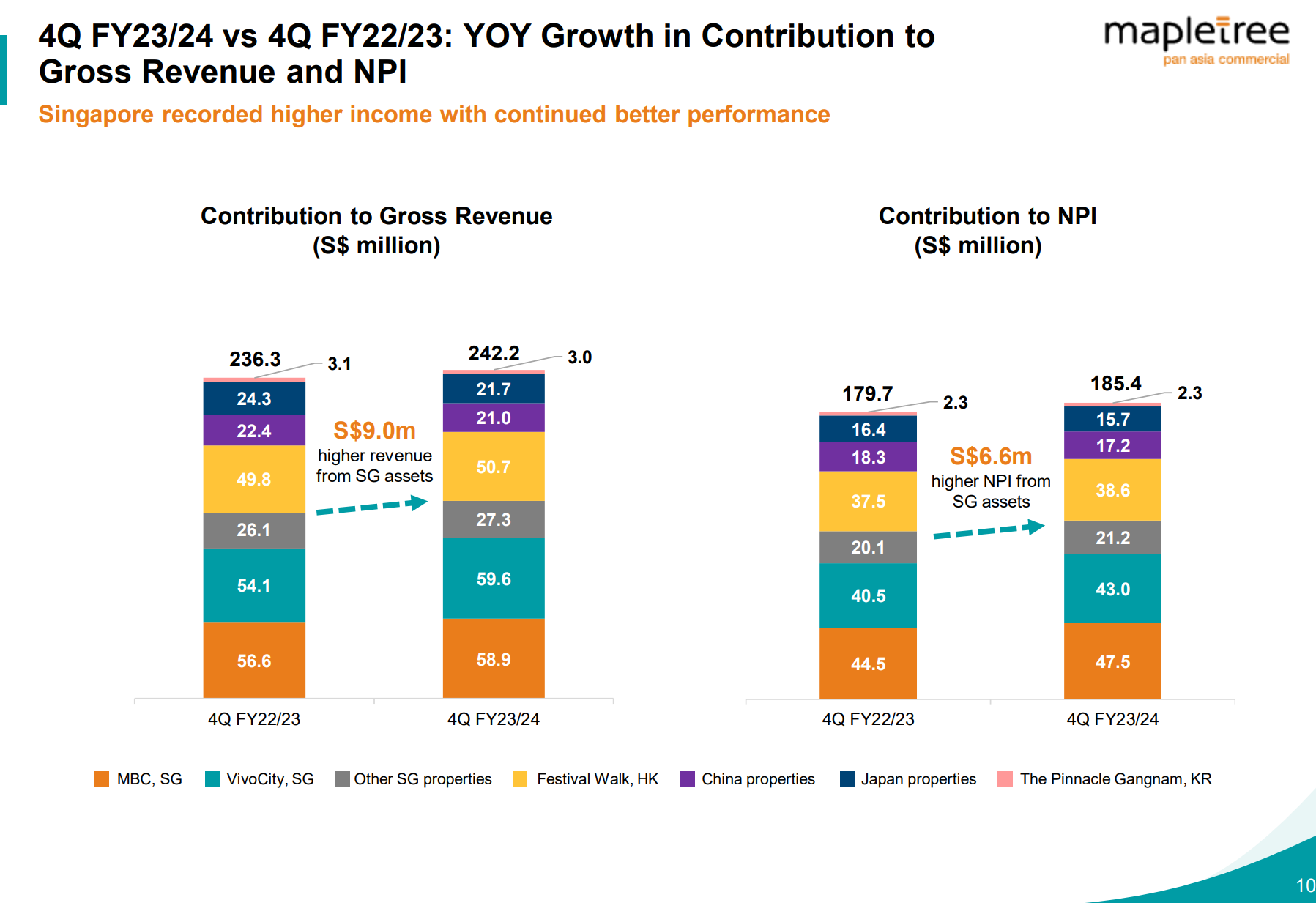

Performance of the real estate owned by Mapletree Pan Asia Commercial Trust

I’ve extracted the individual property performance below.

To sum up:

- The crown jewels (Mapletree Business City and Vivocity) are doing very well

- The rest of the Singapore portfolio is doing ok

- Hong Kong’s Festival Walk is improving vs last year (although to be fair it was from a very low base)

- The Japan property is not doing great (although some of this is due to weaker JPY)

- The China property is not doing great (again some of this is due to weaker RMB)

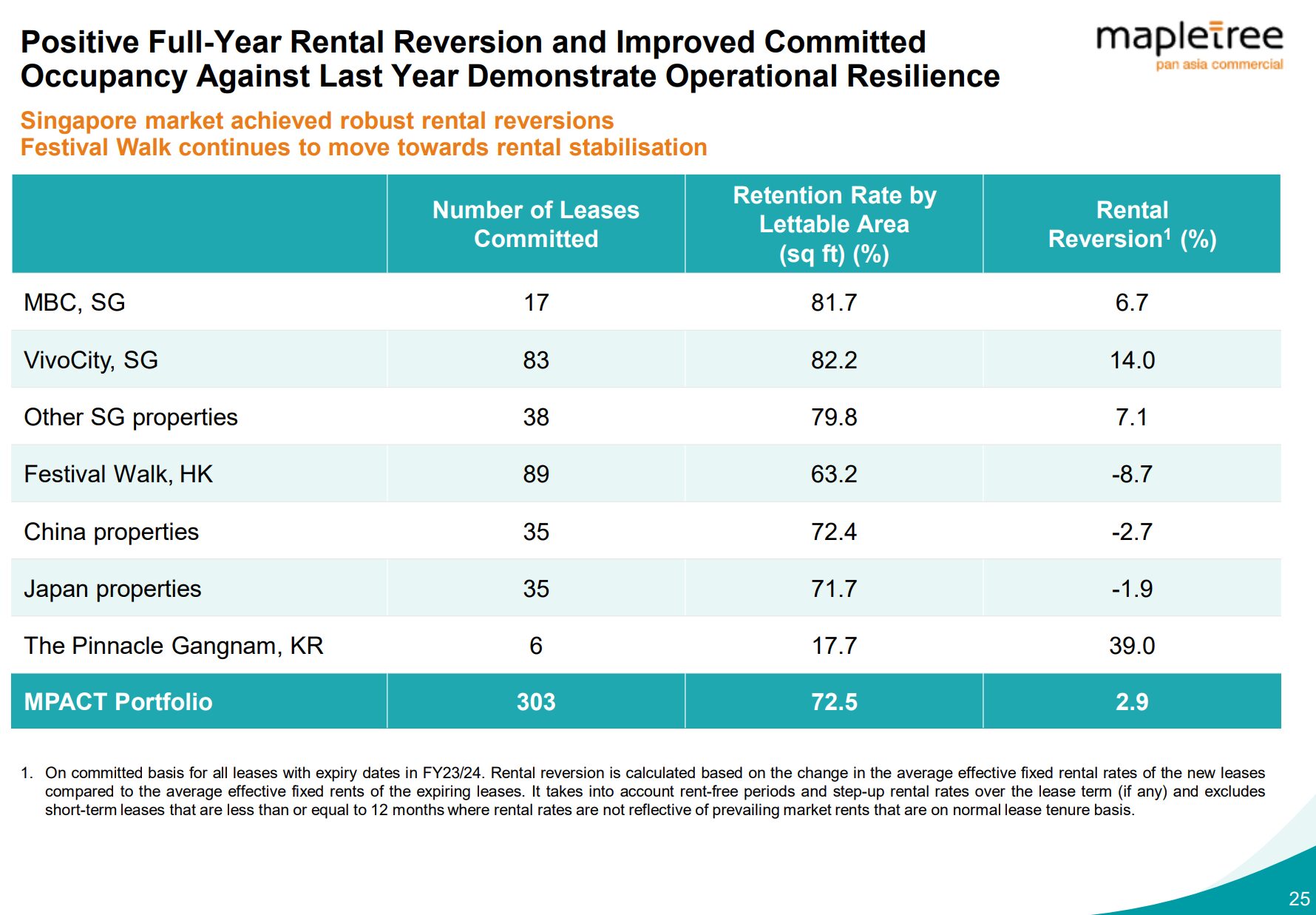

Rental reversions below paint a similar story.

All the original Mapletree Commercial Trust properties are performing well.

All the original Mapletree Greater China Commercial Trust properties are not doing so well.

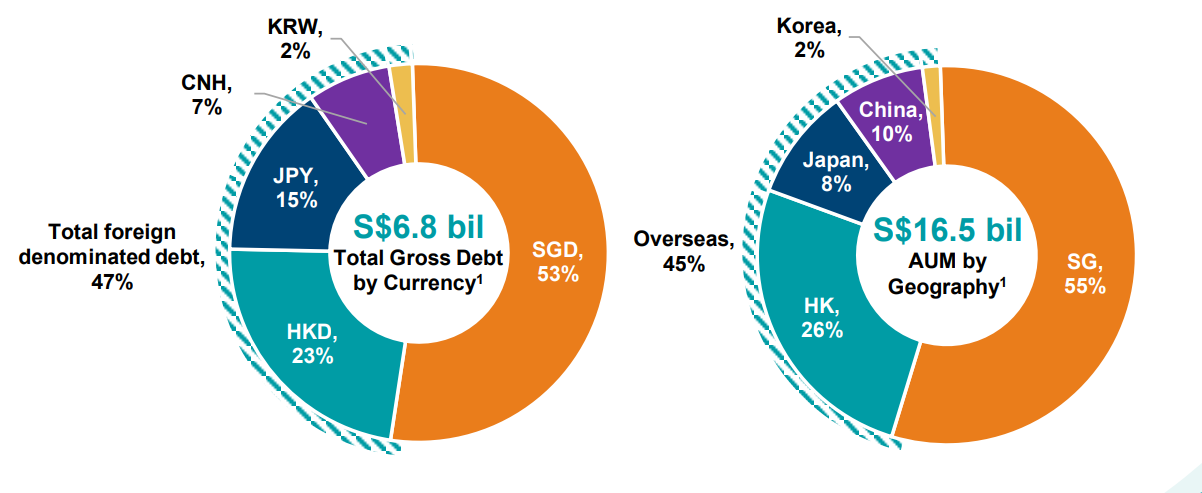

The Hong Kong allocation is punishing this REIT

Let’s deal with the elephant in the room.

There is no doubt that MPACT’s Singapore portfolio of Mapletree Business City and Vivocity are performing well.

The real problem with MPACT is the Hong Kong Festival walk.

This makes up 26% of the REIT’s AUM and is not small.

Is Hong Kong real estate in structural decline?

The main question here I suppose.

Is Hong Kong retail real estate in structural decline?

Here’s the share price of Link REIT, Hong Kong’s largest retail REIT.

It makes MPACT’s chart look pretty by comparison.

Since the top, Link REIT is down almost 64%.

Most Singaporeans love to visit Hong Kong, so I am sure many of you are well aware of the structural problems faced by Hong Kong real estate.

It is that after the clampdown by Beijing.

Neighbouring Shenzhen is just much cheaper, much newer, and much more attractive for almost everything.

If you’re a Hong Konger – why go to a Hong Kong mall and suffer high prices, when you can just pop down to neighbouring Shenzhen and shop in a newer mall at lower prices?

So that’s the structural problem here for Hong Kong retail real estate, that I am not sure will be resolved in the years ahead.

So you can kind of understand why Link REIT’s share price looks like that, and why MPACT’s Festival walk is reporting -8.7% rental reversions:

My Personal View on Hong Kong Real Estate?

I don’t have easy answers for this one.

I do think Hong Kong commercial real estate has big structural problems in the years ahead, and I am not sure if they can be easily resolved.

This is a big problem for the REIT.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

Mapletree Pan Asia Commercial Trust has a lot of debt

The second problem is that this REIT took up a lot of debt to finance their buyout of Mapletree Greater China Commercial Trust.

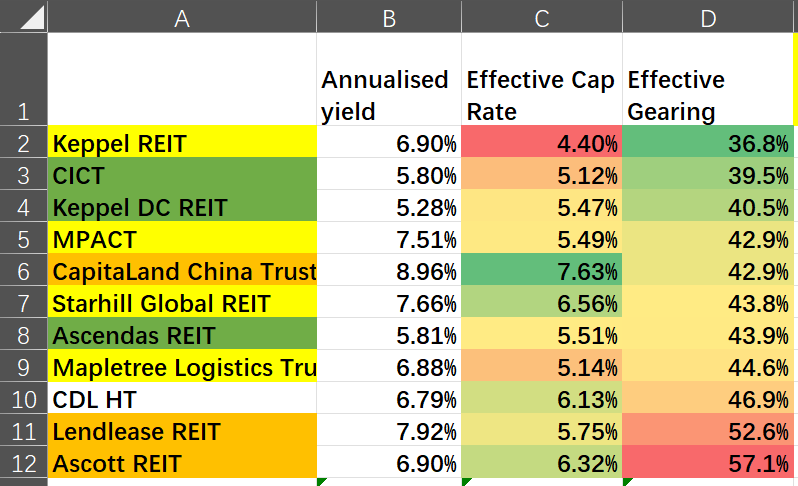

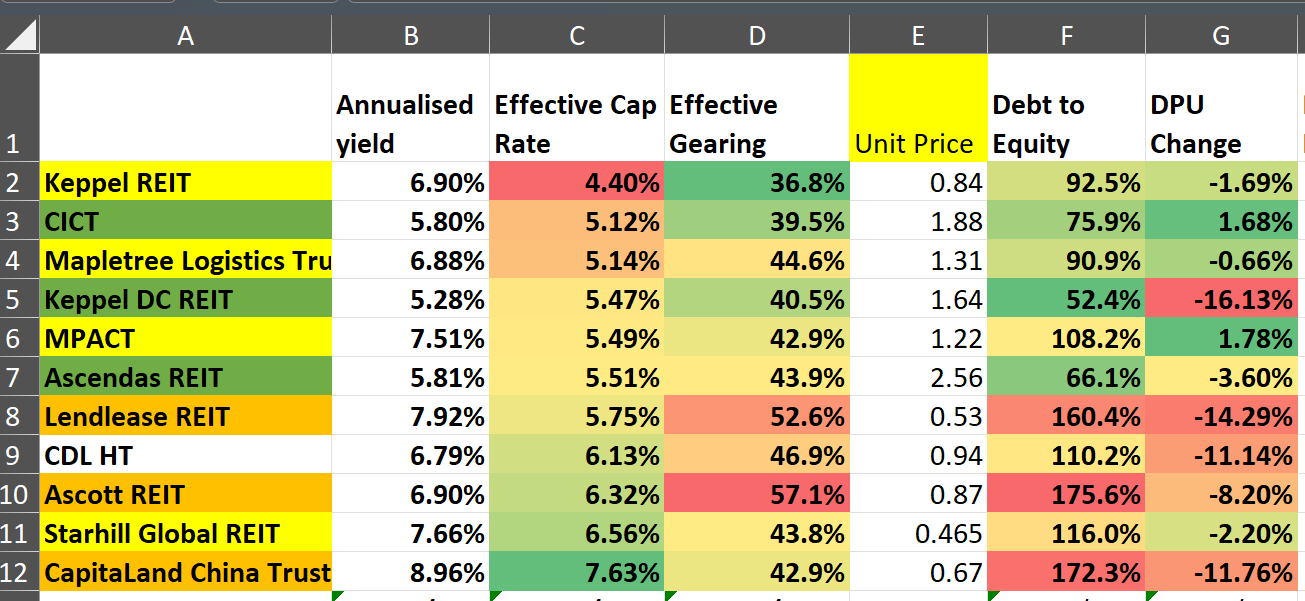

Total effective gearing if you include the perpetuals is 42.9%.

Objectively speaking that’s not high when you compare with the other Singapore REITs (see list below).

But the REIT would be in a much better place had they not loaded up on all this debt and kept gearing in the mid 30s range.

Do REITs offer asymmetric risk-reward if interest rates go down?

Average cost of debt is 3.35%.

That has increased massively vs 2.68% a year ago.

But against Dec 2023, it is only up slightly vs 3.33%.

I see this as a positive for REITs generally.

Because interest rates have stabilised around current levels, going forward we will not see interest expenses increase as drastically as we saw the past 12 months.

In fact there could even be a positive surprise on this front if interest rates are cut.

That’s the asymmetric risk-reward with REITs today.

If interest rates stay high, much of that is already priced in after the price declines.

Yes prices may trade sideways or grind lower, but you’re getting paid a healthy dividend yield while you wait.

Whereas if interest rates do get cut, boy you could see pretty nice upside – depending on how much and how quickly interest rates are cut.

Have long term interest rates peaked?

After the policy statements by Yellen and Powell in early May (being no further increase to Treasury issuance, and no rate cuts + QT to drop to $25 billion a month).

Long term interest rates seem to have peaked.

The US 10 year went from 4.7% before the announcements, to 4.3% today.

Likewise the Singapore 10 year has gone from 3.5%, to 3.18%.

Some of this was due to the latest US CPI print coming in below expectations.

But whatever the case, long term interest rates have come down quite a bit since early May.

And if this holds up, this will be good for REITs.

Valuation of Mapletree Pan Asia Commercial Trust

As shared previously, with higher interest rates I don’t like to use book value for the REITs anymore.

A lot of these book valuations were done in an era when interest rates were stuck at 0%, and make no sense today.

So I prefer to use the effective cap rate concept.

This is basically net property income / (Market Cap of the REIT + Outstanding Debt).

This gives you an idea of how much you are paying for each dollar of net rental income.

Some REITs achieve a high dividend yield by loading up a lot of debt, and effective cap rate helps to filter that out and provide an apples to apples comparison across REITs.

Mapletree Pan Asia Commercial Trust has an effective cap rate of 5.49%.

You can see below how it stacks up against other big REITs.

By contrast:

- CICT trades at 5.12% cap rate

- Ascendas REIT trades at 5.51% cap rate

- CapitaLand China trades at 7.6% cap rate

Is Mapletree Pan Asia Commercial Trust fairly valued?

Is 5.49% cap rate fair for this REIT?

Let’s run some back of the napkin numbers.

No doubt the Singapore property portfolio is best in class – so let’s assume a 4.5% cap rate for that.

Hong Kong real estate is poor, so let’s give it a 7% cap rate.

For Japan/China, let’s use a blended 6.25% cap rate (5% for Japan, 7.5% for China).

Putting all the numbers together gives us a 5.5% blended cap rate.

Interestingly – that’s very close to where MPACT is trading today.

By that metric, it’s hard to say MPACT is an absolute steal at today’s price, nor is it overvalued.

It just looks fairly valued – and you can see the assumptions I used above.

Will I buy Mapletree Pan Asia Commercial Trust at a 7.5% dividend yield?

There is no doubt in my mind that without the Hong Kong property, Mapletree Pan Asia Commercial Trust would be a fantastic buy.

But you could also argue that without the Hong Kong property, Mapletree Pan Asia Commercial Trust would not be trading at this price.

Fair enough.

The fact of the matter is that this is an all or nothing deal.

You can either buy MPACT with its full property portfolio today, or you choose to not buy MPACT.

Hong Kong Real Estate is in structural decline – this will be a problem for the REIT

Personally, I do think Hong Kong real estate is in structural decline.

And I don’t see that changing, unless:

- Something changes on the political front in how Beijing views Hong Kong

- Prices are extremely cheap

None of which is the case today.

So this problem will hang over the REIT for years to come.

The problem, is that I really like the Singapore assets of Vivocity and Mapletree Business City.

I see them as best in class assets, that will continue to perform well for years to come.

And any upside from the Greater Southern Waterfront rejuvenation masterplan is just icing on the cake.

Technical Analysis of Mapletree Pan Asia Commercial Trust

I actually wanted to buy MPACT when it dipped below 1.22 this week.

However, the share price rebounded quickly and I never got a chance to fill the order.

If you look at the charts, 1.22 looks to be a key support level that has generally held for now.

So if it goes back to 1.22, I could see myself adding to my position.

Will I buy Mapletree Pan Asia Commercial Trust at a 7.5% dividend yield?

Full disclosure that I hold a position in this REIT today.

My average cost for the REIT is 1.4.

I think if it goes to back to 1.22 and the support holds, I might add to the position.

But if prices goes up, I don’t really see a need to chase the price up when I already have a position.

The way I see it, in this new regime of higher interest rates, price is crucial.

A good REIT at a bad price can still be a bad investment.

And given what I expect to be significant interest rate volatility in the years ahead, even if I miss the boat now, I may get an opportunity again down the road.

So that’s how I’m seeing Mapletree Pan Asia Commercial Trust today.

Some of you have been asking me based on the cap rate table above, which REITs I find attractive. I will write on this in the next FH Premium article.

I’ll also be updating my REIT & Stock Watchlist this weekend to share updated views on the REITs / Stocks on my watchlist, especially given the changes to pricing and macro conditions the past few weeks.

Do sign up on FH Premium if you’re keen.

This article was written on 17 May 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

– Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Hi can I check how did you calculate effective gearing using Ascott REIT as an example? Your calculation of 57.1% appears significantly higher than Ascott’s reported gearing of 37.7% in their 1Q24 Business Update (the footnotes mentioned that net debt/net assets = 58.1%). Just wanted to understand the nuances between the different calculations, thank you!

I took the debt + perpetuals / net assets.

It should be similar to how Ascott calculates their net debt/net assets.

The complexity is that the leverage number excludes perpetuals, which are treated as equity on the balance sheet. While this makes sense in a pre-COVID world where interest rates were zero, this doesn’t make sense in today’s world where perps have a very real financing cost associated with it. So you need to add the perps back in, to get a more accurate picture of the underlying leverage.

A REIT can achieve a higher DPU via higher gearing, but in today’s world that higher gearing comes at a cost.