With all the talk about interest rate cuts going forward, this is probably as good a time to think about yield plays.

Take Netlink Trust for example.

At current price it pays about a 6.4% dividend yield.

If that dividend yield can be maintained, and interest rates go down, not only will you get the 6.4% dividend yield.

You may also see capital gains as prices go up to reflect a lower rate environment.

So… will I buy Netlink Trust at a 6.4% dividend yield?

I wrote this article a month or two back for FH Premium subscribers.

But I wanted to release for the benefit of all readers.

Do sign up for FH Premium for more articles like this.

I also share my full personal portfolio and stock / REIT watchlist on FH Premium.

Netlink Trust’s share price

This is the weekly chart for Netlink Trust.

Since the stock went ex-dividend on 29 May, share price has dropped quite a bit.

From $0.87 on 28 May, to $0.825 as at time of writing (10 June).

That’s a 5.2% drop, which is noticeable for a stable bond-like play like Netlink Trust.

Here’s the daily chart – note the gap down after Netlink Trust went ex-dividend.

In my experience this tends to be quite common for Singapore dividend stocks.

For some reason investors will wait until a stock goes ex-dividend before selling the position, which creates a larger than expected drop after ex-D.

So for long term buyers looking to add a position, it’s usually a good time to make use of the ex-D drop (assuming no change to the underlying fundamentals).

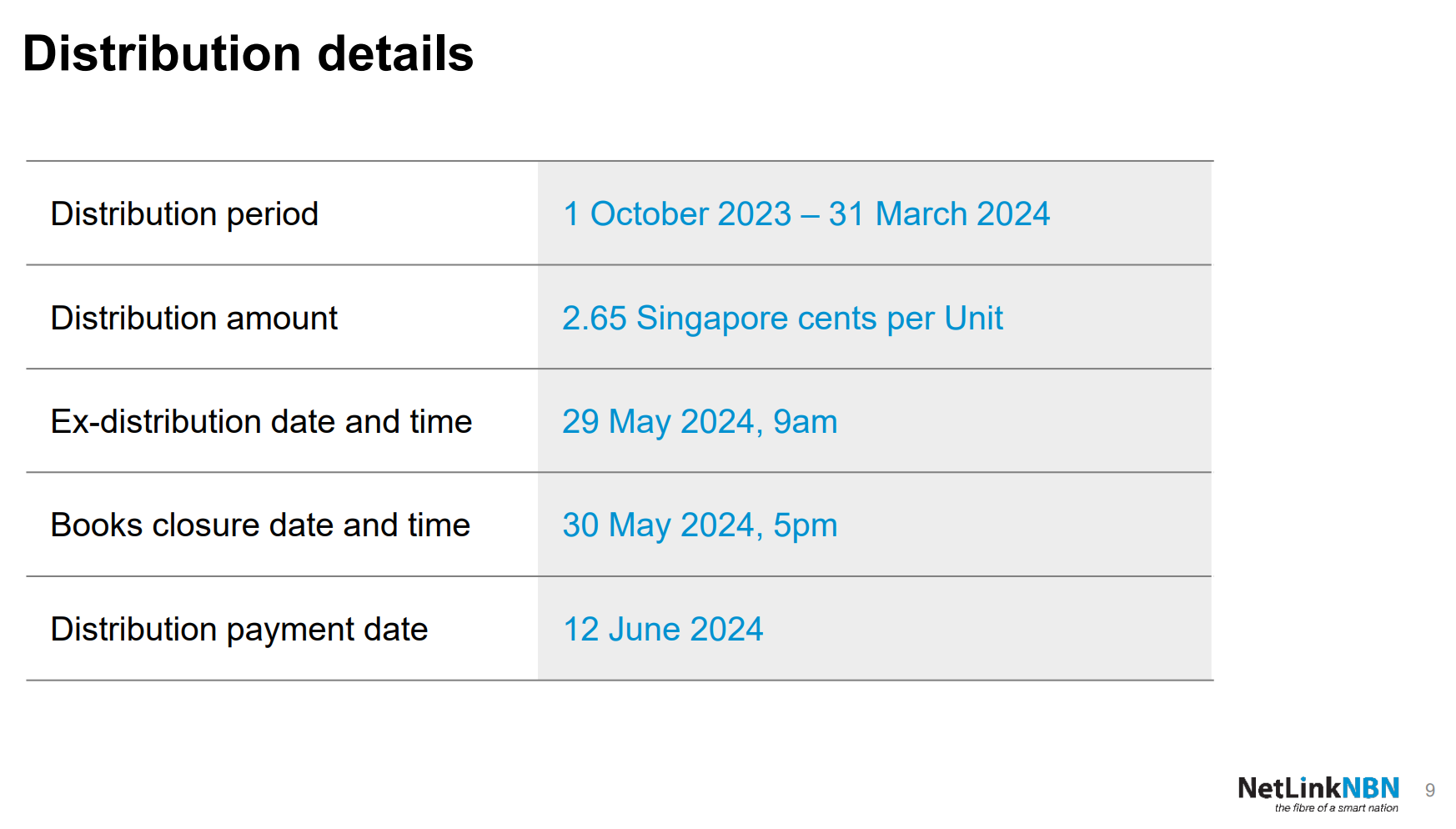

Netlink Trust pays a 6.4% dividend yield at this price

Latest DPU is 2.65 cents.

If we annualise that, we get a dividend yield of 6.4% at current price.

That’s not too shabby, and higher than certain blue chip REITs like CICT or Ascendas REIT.

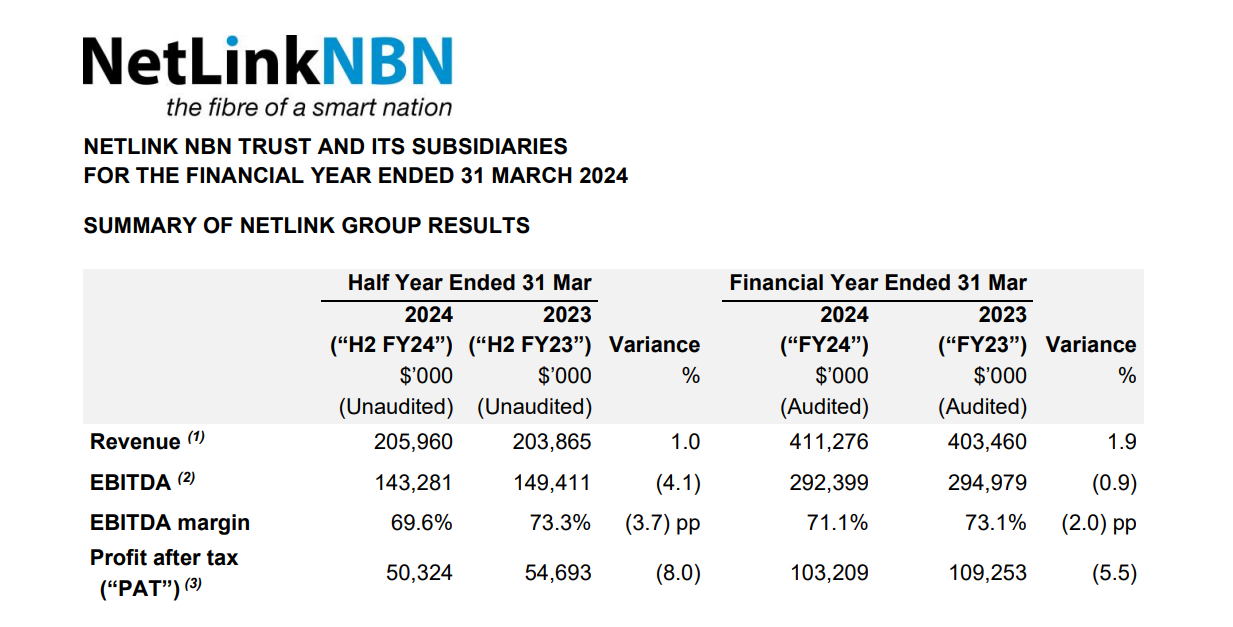

High level overview of the financials of Netlink Trust

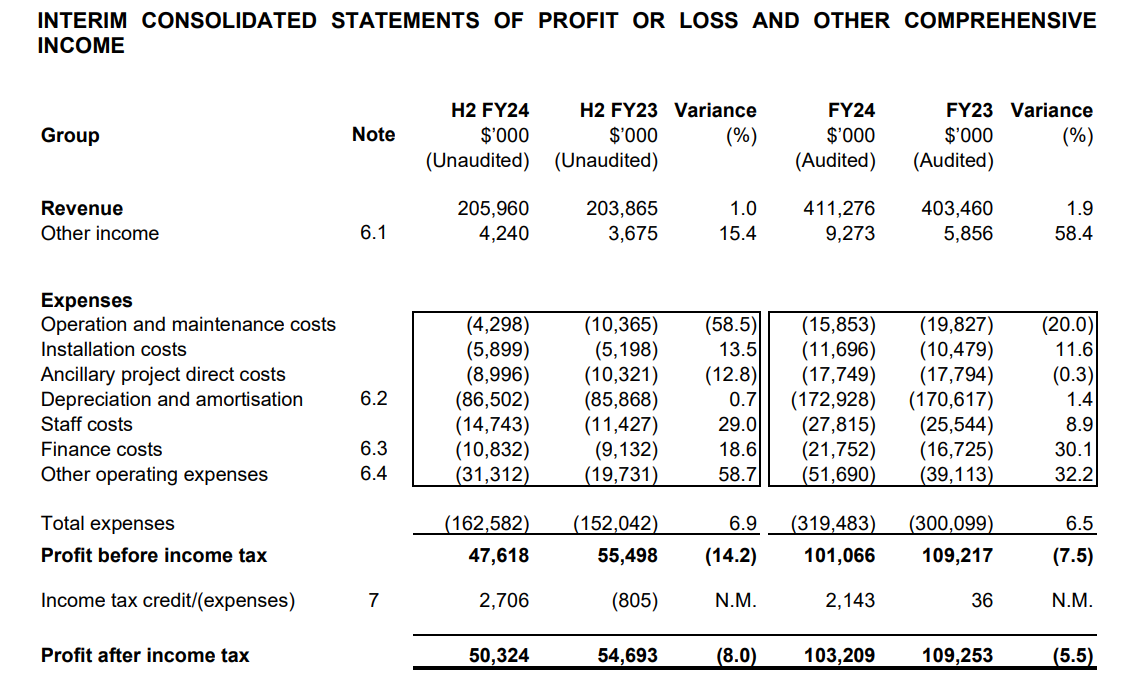

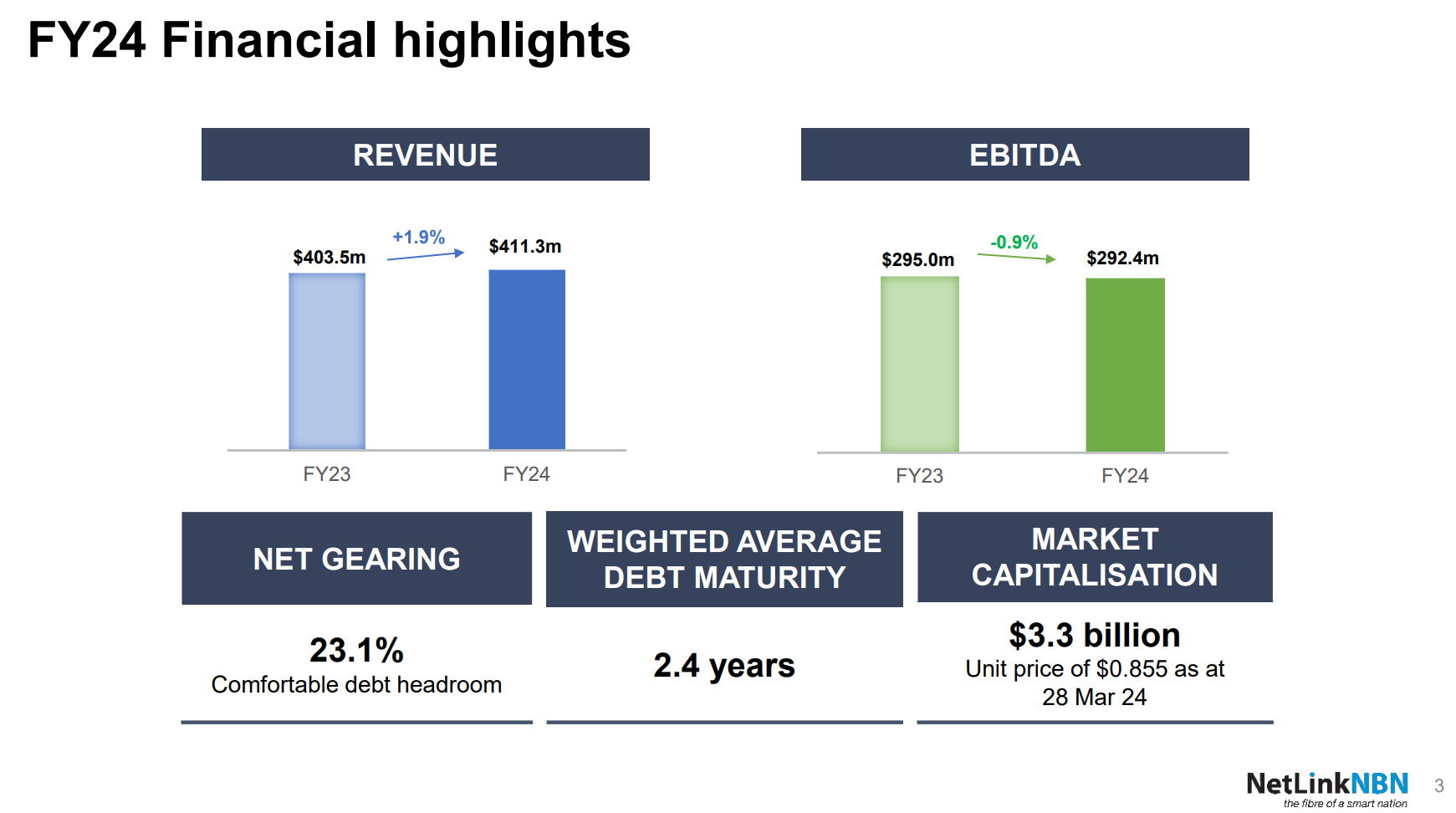

At a high level, this is the story from the P&L:

- Revenue is up 1.9% year on year

- EBITDA is down 0.9% year on year

- Profit after tax is down 5.5% year on year

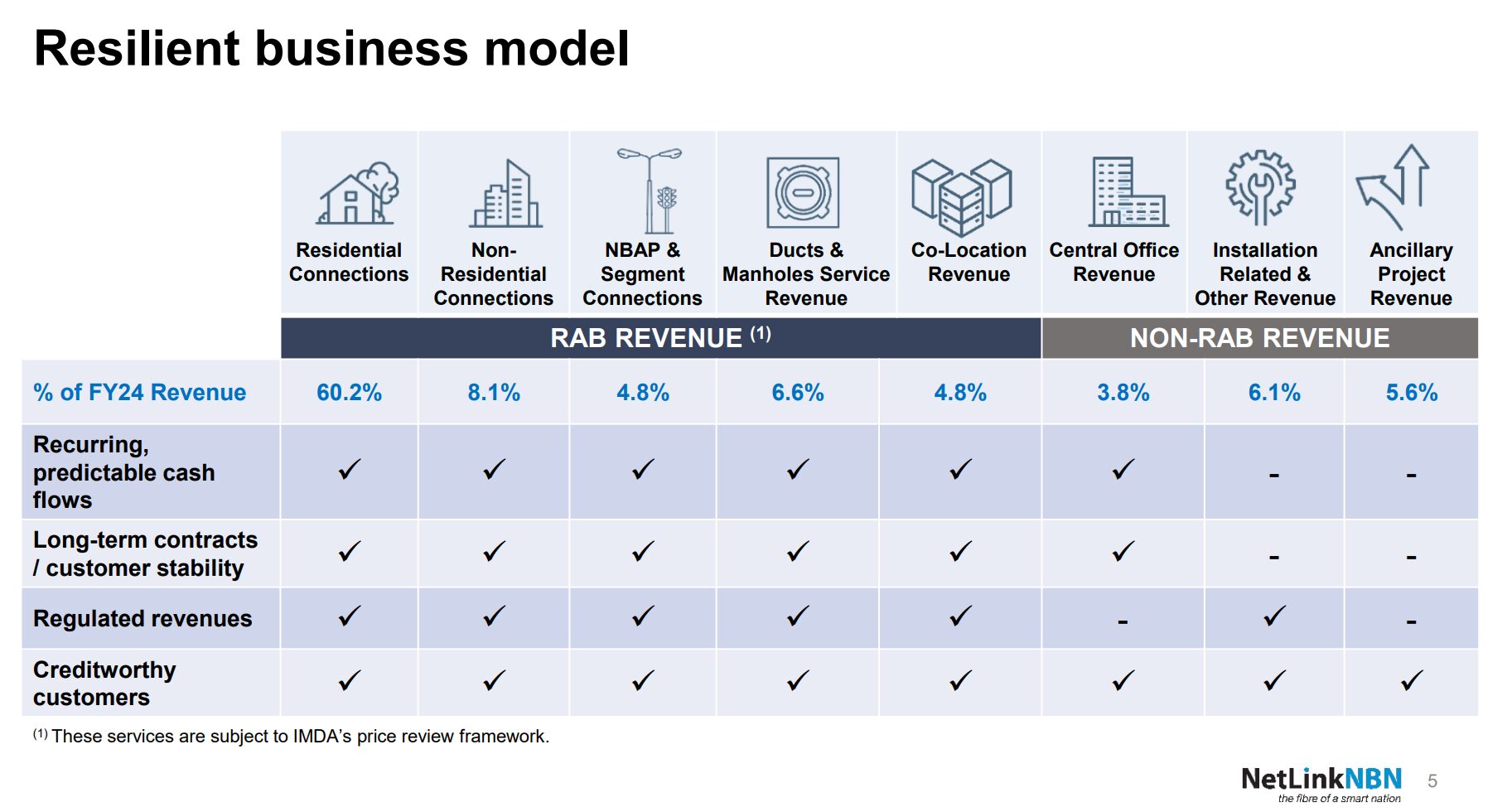

Revenue is growing nicely for Netlink Trust

You can see the breakdown of Netlink Trust’s revenue below, the bulk of which is residential and commercial fibre connections (making up almost 70% of revenue).

This is the context provided by Netlink Trust on revenue growth:

“(1) Revenue for H2 FY24 and FY24 were higher than H2 FY23 and FY23 by 1.0% and 1.9% respectively.

These increases were mainly contributed by higher connection revenue, installation related and other revenue, partially offset by lower ancillary work orders.”

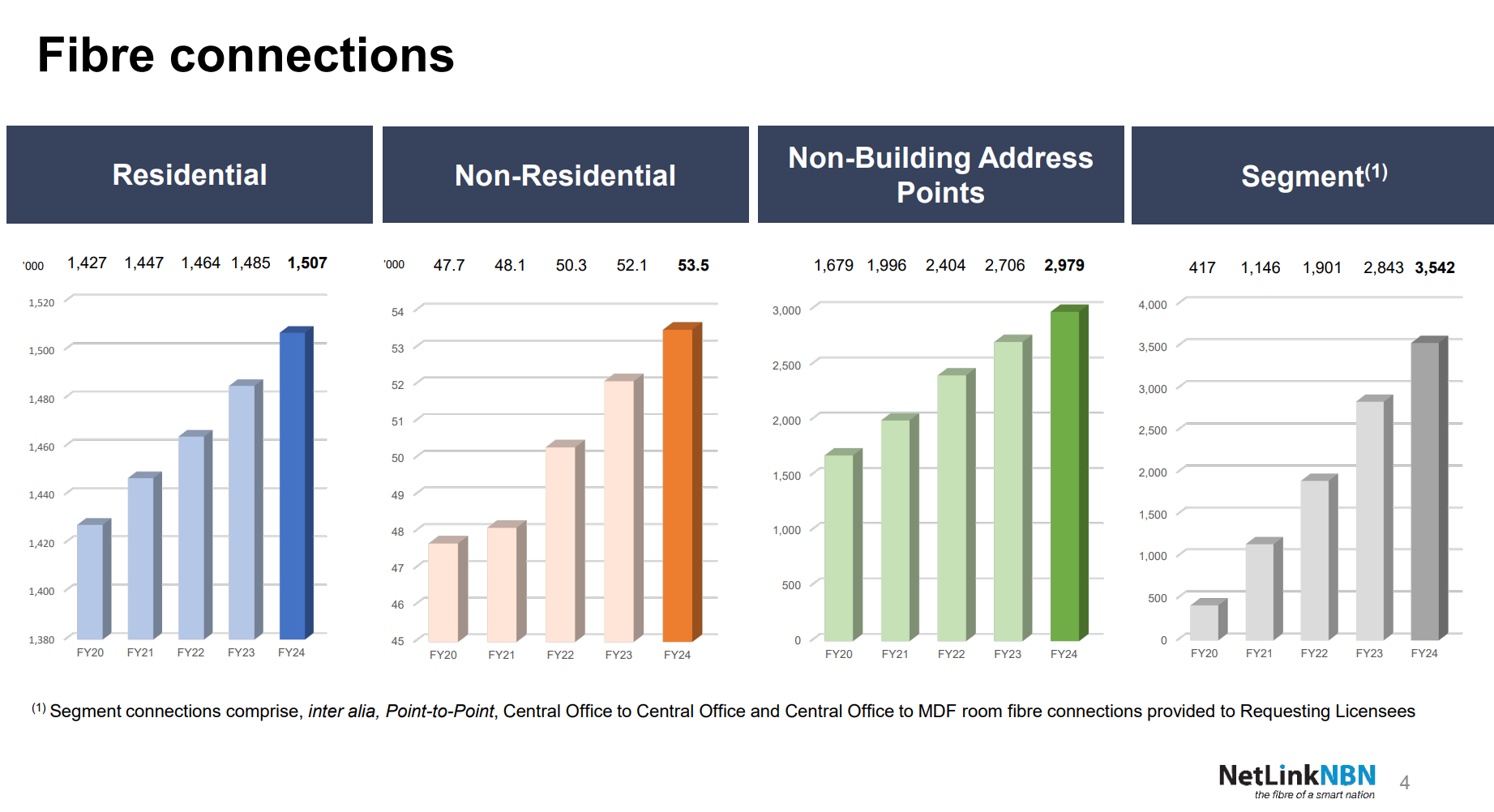

So generally speaking, looks like revenue growth is driven by higher fibre connections – on which you can see the breakdown in growth below:

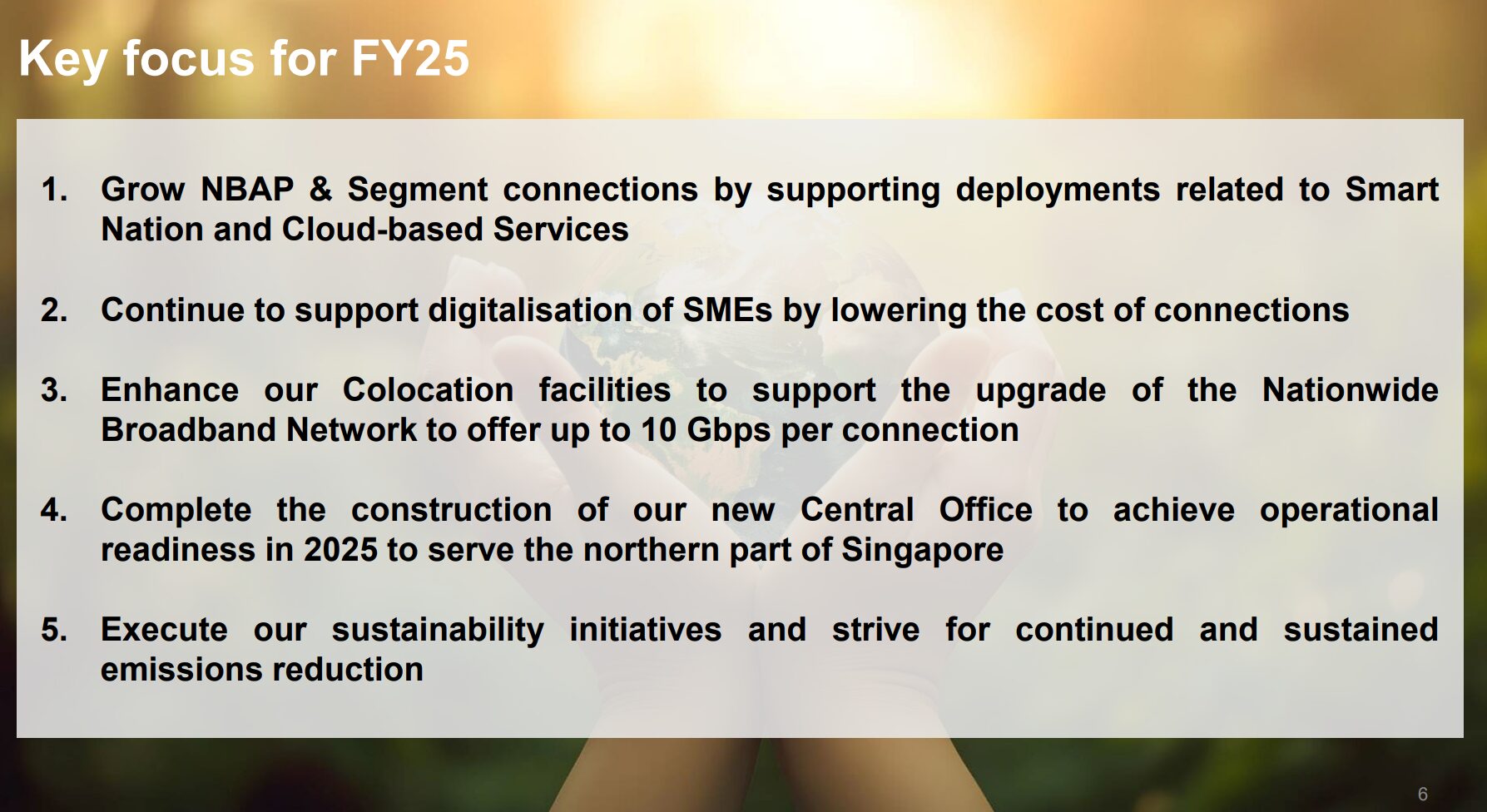

Key focus going forward is NBAP & Segment?

However, residential / non-residential connections are near saturation as close to 100% of households are already on fibre connections, so any increase going forward will only track population growth.

This begs the question of where will future growth come from for Netlink Trust?

The answer according to Netlink, is “NBAP & Segment”:

What exactly does this mean?

To break down the technical jargon:

- NBAP Connection refers to a connection provided by NetLink Trust (Singapore’s designated nationwide broadband network operator) for accessing locations classified as NBAP instead of residential or non-residential premises. An NBAP location generally refers to outdoor locations or locations without a physical address in mainland Singapore or its connected islands.

- Segment refers to dedicated fibre links between network nodes and equipment locations – that allow telecom operators and enterprises to build out their connectivity infrastructure leveraging NetLink’s nationwide fibre network

In simple words, the growth is going to come from (a) Internet of Things stuff like traffic lights or street lamps, and (b) allowing telcos / enterprises to connect their equipment using fibre.

You can see this below.

Residential / Commercial connections cannot maintain the same rate of growth we saw the past few years as almost everyone is on a fibre network already, but these NBAP / Segment stuff still has growth ahead of it.

Does Netlink Trust deserve to trade at a higher yield because it holds depreciating assets?

For the record, yes I get that Netlink Trust is a business trust and holds depreciating assets like fibre networks (instead of REITs that hold freehold real estate that can appreciate over time).

And that because of that some yield premium is required relative to REITs.

Let’s examine this argument further.

Netlink Trust’s fibre assets were first deployed in 2009.

The assets are amortised using the straight-line method, over the estimated useful life of 25 years (for fibre) and 35 years (for ducts & manholes).

I did a general search online, and the results are that:

- The usual (conservative) depreciation period for fibre assets is about 20 – 25 years

- However, practically speaking, the effective life can be 40+ years (up to 50 – 75 years based on some reports), depending very much on installation method, operating conditions, manufacturing process etc

Assuming the conservative 25 years, this would mean Netlink Trust’s assets would near end of life around 2034 (10 years away).

Assuming an optimistic 40 years, this would mean 2049 (25 years away).

So the answer to this has pretty big implications on the investment.

If the fibre networks are going to require wholesale replacement in 10 years time, you wouldn’t want to hold Netlink Trust when this becomes apparent.

Let’s dive deeper into the financials to see if there are any clues to this.

Operating expenses actually went down for Netlink Trust?

Diving deeper into the P&L tells an interesting story.

Operating and maintenance costs actually fell 20% in FY24 – from $19.8m to $15.9m.

I suppose this is good, because if the network is in trouble you would expect maintenance costs to go up.

However, total expenses rose 6.5%, largely driven by 2 line items:

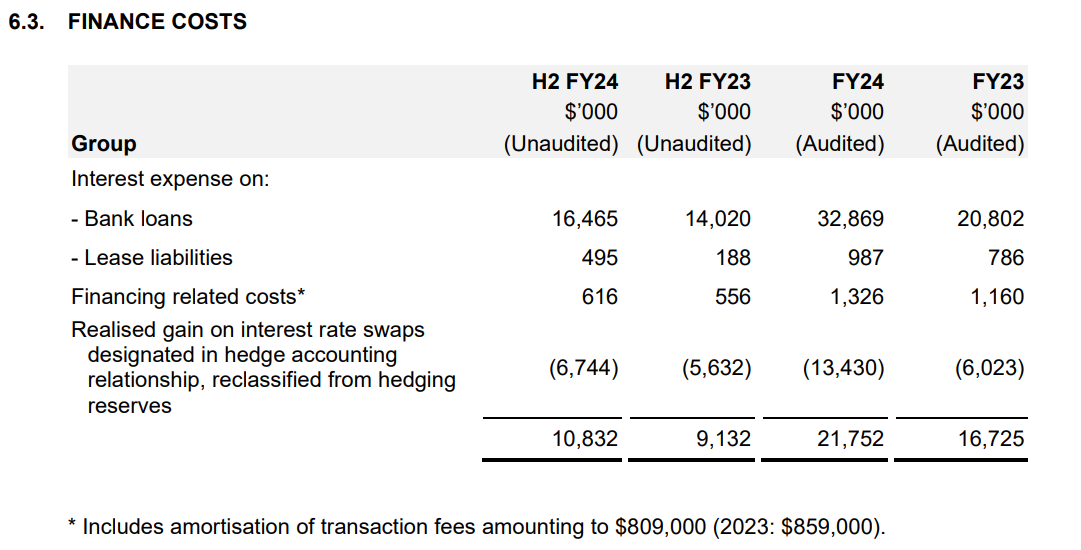

- Finance Costs

- Other Operating Expenses

Finance costs is straightforward – the bulk of it is due to higher interest rates.

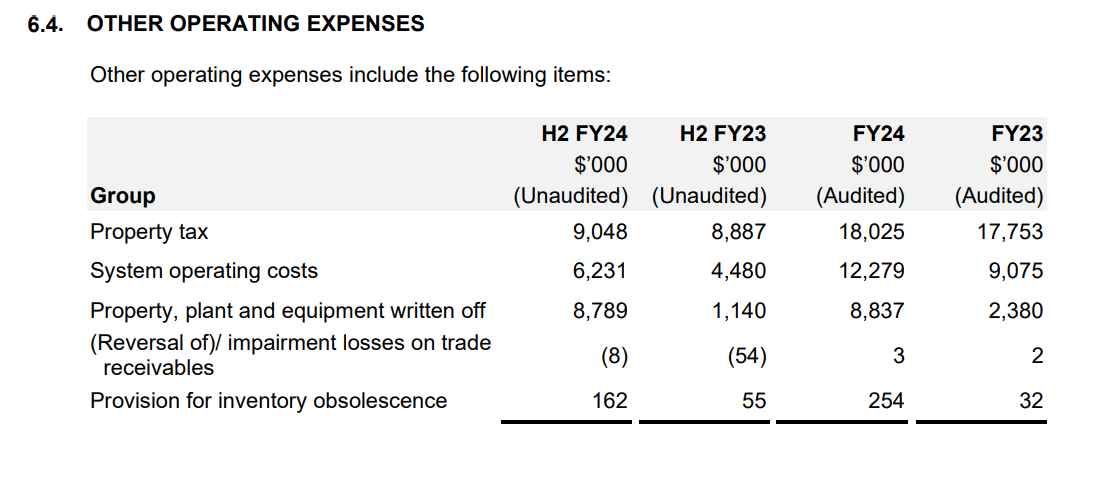

Other operating expenses is more nuanced – coming mainly from a rise in system operating costs and PPE written off.

The financial statements breaks this down further:

- In H2 FY24, a one-off non-cash write-off of decommissioned network assets amounting to $8.8 million was recorded,

- offset by a one-off refund of $5.2 million following the resolution of disputed power charges.

Excluding the one-off items, the decrease in EBITDA was attributable to higher operating expenses despite higher revenue. EBITDA for FY24 was lower than FY23 by 0.9%.

Other than the one-off items, the FY24 EBITDA declined slightly as a result of higher operating expenses.

So it looks like the write-off is due to decommissioned network assets, but unfortunately no further detail was provided as to why it was decommissioned.

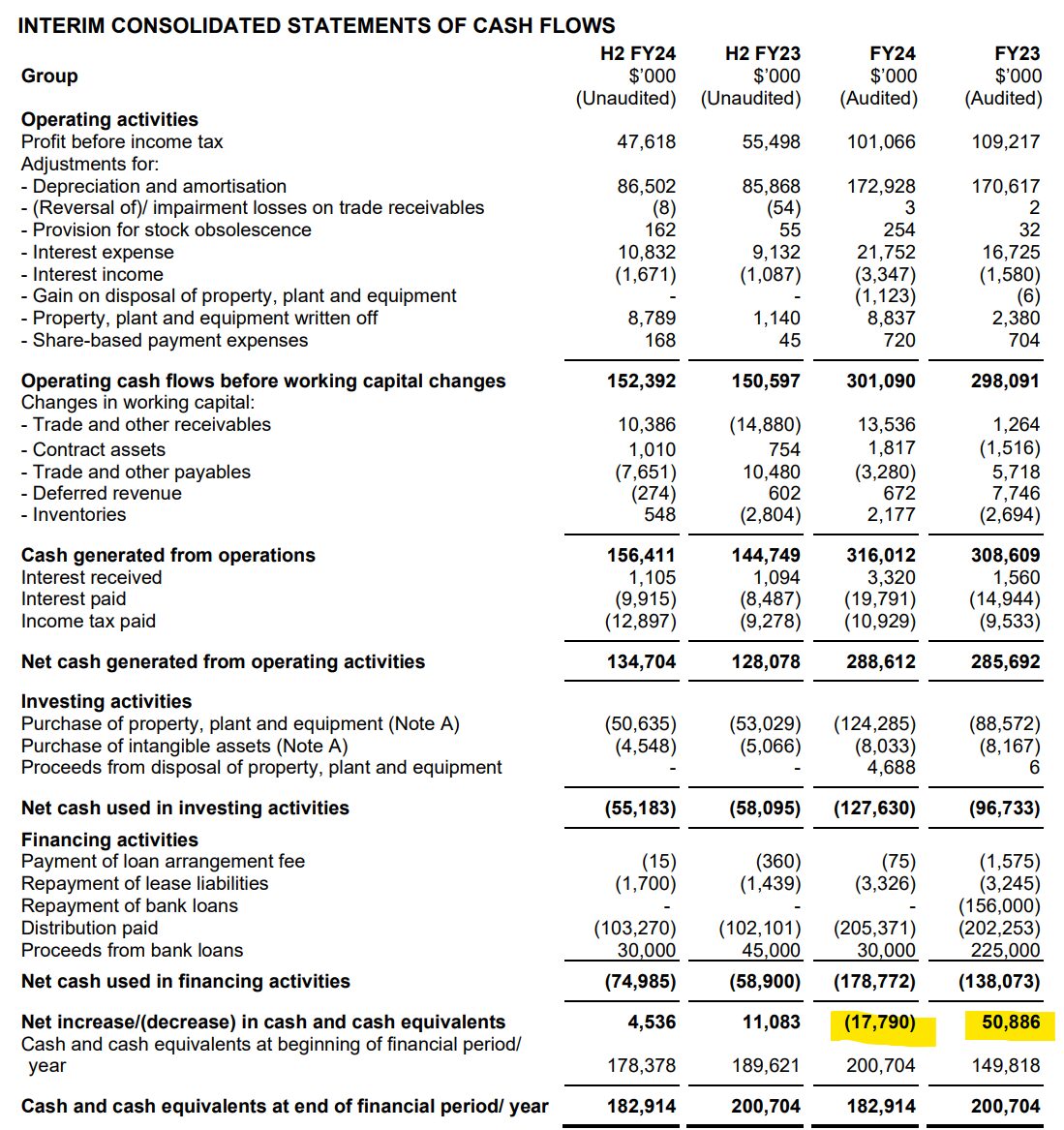

Negative Cash Flow – How is Netlink Trust financing the higher dividend if profits are down?

The other red flag that many of you noticed is that Netlink Trust reported negative cash flow in the most recent FY.

This led to concerns that the higher DPU is being funded via borrowings, rather than organic cash flow.

Looking at the cash flows, the troubling one is the increase in purchase of PPE (property, plant and equipment) from $88 million to $124 million.

This is broken down further below, but again no information is provided on what these PPE are.

We don’t really know if Netlink is buying these for new connections (in which case it is fine), or to replace old assets that are degrading (which would be worrying).

What does this all mean for Netlink Trust?

It goes back to the analysis above.

If Netlink trust is spending all these money on new fibre connections, and if its writing off assets that are just not relevant anymore (wrong location), that’s probably fine.

If so the analogy would be equivalent to a REIT buying new properties or doing AEI – you’re investing to get higher revenue down the road.

But if Netlink trust is spending all these money to replace existing fibre connection which has degraded, writing off assets that has degraded earlier than expected, that’s going to be a problem.

The analogy for a REIT would be as if the building has a big hole in the roof, and the REIT has to spend a lot of money just to repair the roof and maintain the same level of revenue.

Unfortunately we don’t know the answer to this one – as it’s not very clear what the spending is directed to.

Update – Responses from Netlink Trust

As it turns out, a similar question was posed to management by shareholders.

I extract the question, and Netlink Trust’s reply below (emphasis mine).

NetLink’s NAV decreases yearly. NetLink pays more DPU than it’s EPS. Is this a concern?

NetLink’s response

NetLink’s net profits are lower than operating cash flows primarily due to significant noncash depreciation and amortisation expense. This is a common characteristic in capital intensive infrastructure business.

NetLink is a business trust. One of the key advantages of the business trust structure is that it allows NetLink to pay distributions from its cash flow and is not limited by profit or retained earnings. Hence, EPS is not an indication of the DPU that can be declared to unitholders.

Investors should focus on NetLink’s ability to generate cash flow to make distribution payments. A declining NAV is a concern only if this affects the ability of the entity to continue to generate a healthy level of cash flow going forward. This is not the case for NetLink as: (1) our business is expected to continue to generate a healthy level of cash flow to support distribution; (2) we continue to invest in our network and this investment will translate to higher revenue in accordance with the Regulated Asset Base framework; and (3) we prudently fund our growth through a combination of internally generated cash flow as well as our balance sheet strength to borrow.

You can now follow Financial Horse on Google Chrome to avoid missing any posts!

Just:

- Click the 3 dots on the top right of Google Chrome

- Click Follow!

- And Financial Horse posts will now appear on your home page, under Following:

You can also follow Financial Horse on:

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

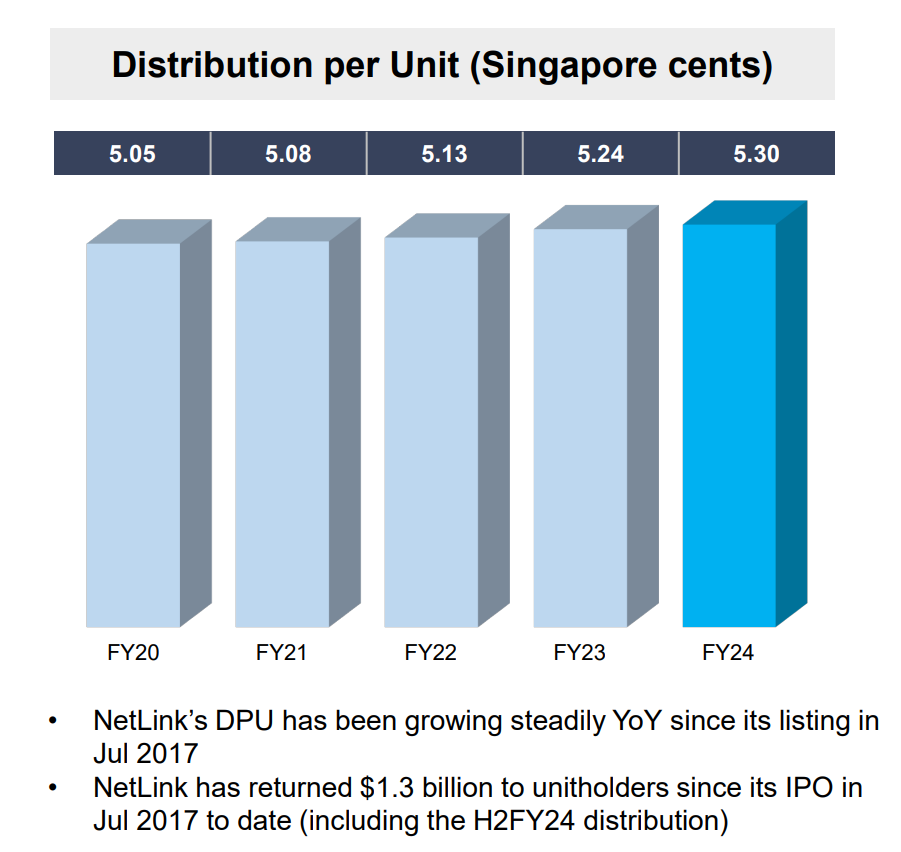

Netlink’s DPU has been growing consistently for the past 5 years

On the bright side though.

While most REITs are reporting declining earnings.

Netlink Trust’s DPU has been remarkably stable.

The 5 year track record below – Netlink Trust has been raising its dividend every single year for the past 5 years (ever since IPO in fact).

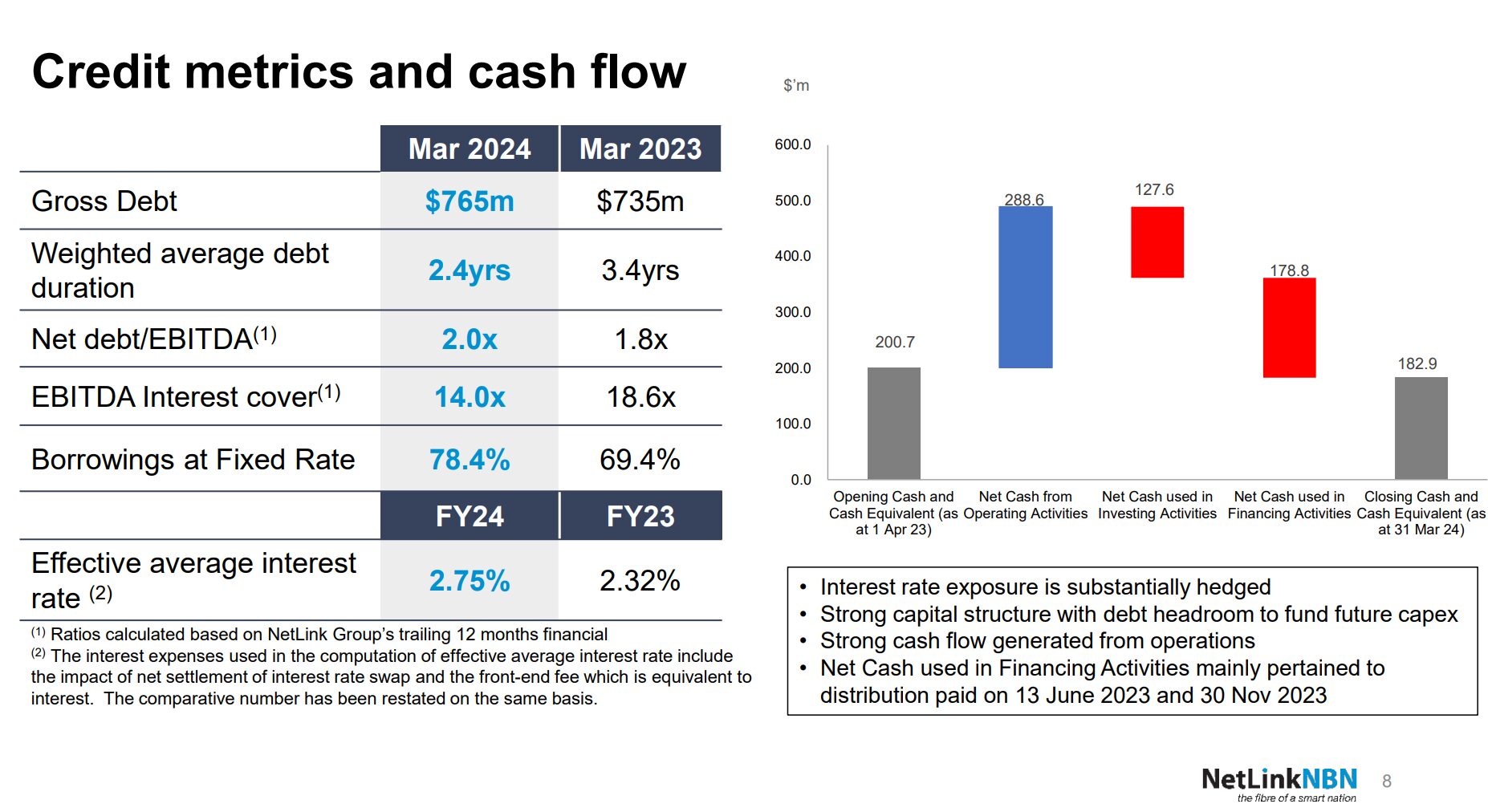

Balance Sheet of Netlink Trust – very low 23% gearing

For what it’s worth, gearing is a ridiculously low at 23.1%.

Many REITs today are running high 30% gearing, so this is much, much lower than most REITs.

Effective interest rate is 2.75% though, which indicates there is room for this to increase somewhere to the mid 3% range.

But because gearing is low at 23%, the interest expense increase will not be as devastating for Netlink as it was for most REITs.

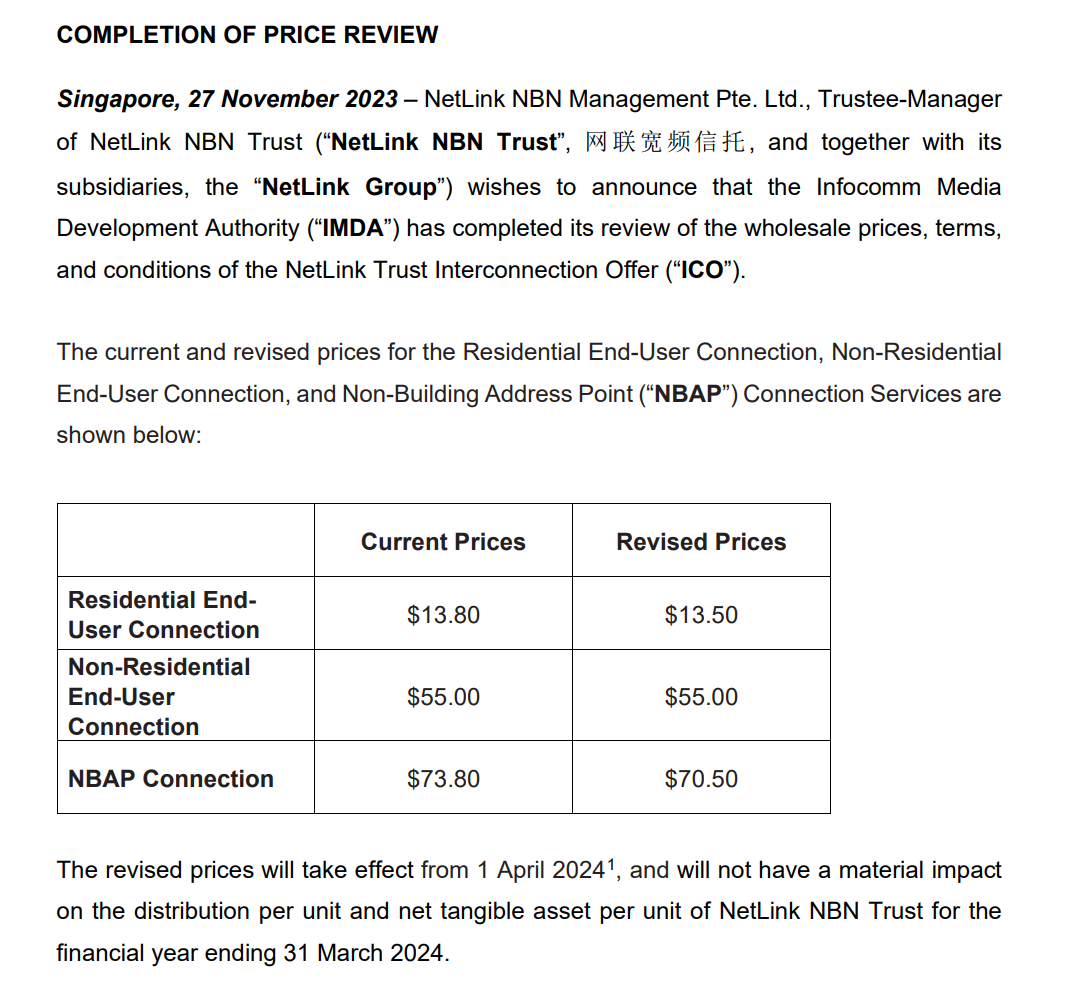

IMDA Price Review – Price increases for Netlink Trust are heavily regulated

One final point to note is that as Netlink Trust provides internet connections for Singapore homes, this makes price increases a very sensitive (and political) topic.

Long story short is that Netlink Trust cannot raise prices without IMDA approval.

In fact all prices are regulated by IMDA – and you can see how in the most recent review, Netlink Trust was forced to reduce prices for residential connections and NBAP connections.

This works out to a 2.2% decrease in pricing, and given residential makes up 60% of Netlink’s Revenue, this is bound to have some impact on the FY25 numbers.

So… Will I buy Netlink Trust at 6.4% dividend yield?

Okay so this article may come across a bit doom and gloom.

But I suppose that is the nature of fixed income style investments.

When you buy a bond (or Netlink style investment), the upside you can earn is pretty much limited to the dividend yield (6.4%) and some limited capital gains if market interest rates drop.

It’s not like stock where if you’re right, you can 2x your money or more.

So when you’re buying bonds and your upside is capped, that makes it vitally important to guard your downside risk.

Hence why fixed income investors tend to be much more pessimistic and numbers focussed than equity investors (who are more story driven).

What are the key risks with Netlink Trust?

To sum up the key concerns:

- The effective life of the Fibre assets is unknown. Worst case there may be another 10 years, best case there may be another 25 years or more.

- Spending has indeed been going up at Netlink Trust, resulting in negative cash flows. It is not clear if this spending is to replace existing assets or finance new investments. However gearing is very low at 23%, which provides a lot of debt headroom to kick the can down the road.

- IMDA regulates pricing – you cannot rule out the fact that IMDA may require further price decreases (or cap increases) to combat inflation

I suppose the point is that there is no free lunch in this world.

Risk free yield is the SSB at 3.2%.

A low risk bond like Astrea 8 pays a 4.35% yield at market prices.

So if you want risk free or low risk, those are the kind of yields you are looking at for SGD.

With Netlink Trust at 6.4% dividend yield, the question is whether that 3.0% yield spread is sufficient enough to compensate you for the risk.

Technical Analysis of Netlink Trust

Here’s the monthly chart for Netlink.

The lowest that price went in 2020 and 2022 was 0.79.

While the next lowest in 2023-2024 was 0.81.

So from a TA point of view, these would be the key levels I would be watching for.

So… Will I buy Netlink Trust at 6.4% dividend yield?

Personal view – I think the risk-reward is acceptable for me.

Of course it is not risk free, so you want to position size and not put your life savings into one counter.

But as a diversifier for yield plays.

Personally I like it.

The underlying assets are as stable / recession proof as it gets – nobody is cancelling their fibre connection even in a recession.

And at 23% gearing there is a lot of debt headroom before things start getting hairy.

And 23% gearing is low enough that Netlink Trust should not be as exposed to rising interest rates as other REITs.

Yes, there are definitely risks such as negative cash flow, the effective life of the fibre assets, whether IMDA will require further price changes and so on.

So don’t be blind to the risks, and size it well.

I may actually look to add to my position with the current sell-off, against using SRS funds.

0.81 would be a key support to watch if it gets there, although frankly I am open to adding at current prices as well.

Will monitor closely to see how price plays out the next few days / weeks.

I wrote this article a month or two back for FH Premium subscribers.

Do sign up for FH Premium for more articles like this.

I also share my full personal portfolio and stock / REIT watchlist on FH Premium.

This article was written on 19 July 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

4.20% yield on first $20,000 at Chocolate Finance

I wrote a detailed review on Chocolate Finance, so do check if out if you are keen.

Long story short is that Chocolate finance pays 4.2% on the first $20,000, withdrawable instantly.

The funds are invested in a selection of bond and money market funds, and Chocolate Finance will top up any returns if they are lower than 4.2%.

To be clear this is not SDIC insured and not risk free.

So I leave it for investors to decide if you are comfortable with the risks (see my full review here).

Chocolate Finance currently is invite only, but you can use the FH invite link below if you are keen to try it out:

https://share.chocolate.app/nxW9/ep4q7wxp

– Get USD 400 cash voucher

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 400 cash voucher.

You just need to:

- Deposit USD 2000 (or 10,000 for higher rewards)

- Execute 5 trades (for higher rewards)

Note that Webull is also offering zero commission for US options trading right now.

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Another key question to ask Netlink Trust is with the nation’s move towards next generation 10Gbps, is a refresh of fibre installations required? If so, then the close to saturation installations will require another visit by Netlink Trust all over again to activate 10GBps fibre connectivity

That’s a good question. Netlink actually answered this in the FAQs to the AGM. I extract the reply below:

With the current network capable of supporting transmission speeds of

10Gbps, what is the risk of obsolescence now that the Singapore

government is shifting to a 10Gbps nationwide broadband network as the

standard? Will significant capital investments be required/expected for the

development of a “next-next-generation” network with speeds of 100Gbps

or better?

NetLink’s Response

The existing fibre network could support newer passive optical network

technologies with a transmission speed of 10Gbps and beyond. The risk of the

existing fibre network becoming obsolete is therefore very low.

IMDA had on 21 February 2024 announced that it will invest up to $100 million to

upgrade the Nationwide Broadband Network (NBN) from 1Gbps to 10Gbps. This

initiative, which is in line with the Digital Connectivity Blueprint, entails NetLink

working closely with the ISPs to upgrade the NBN from now to 2028, which will

form the backbone of future applications and innovation, at speeds up to 10 times

faster than today. The level of capex that NetLink has to incur in support of this

initiative is manageable and has been taken into account in our budget plan.

At this stage, it will be far too early to assess the level of investments required for

further upgrades beyond 10Gbps.