I’ve been getting a lot of questions about OCBC Bank recently.

After the big rally in DBS Bank shares of late (that makes OCBC comparatively “cheaper” by comparison).

And the news that OCBC Bank is buying a 100% stake in Great Eastern.

A lot of you have asked for my views on OCBC Bank, and whether it is a good buy.

So… that’s exactly what we’ll do today.

OCBC Bank trades at a 5.7% dividend yield, and 1.22x book value.

Is it a better buy than DBS or UOB Bank?

High level valuations of OCBC Bank vs DBS Bank and UOB Bank

I’ve summarised the key statistics of all 3 local banks below.

OCBC Bank is somewhere in the middle.

Better than UOB Bank in ROE and market cap.

But worse then DBS Bank both ROE and market cap.

That said at a price to book of 1.22x, it looks a lot more reasonably priced than DBS Bank (1.70x).

|

|

OCBC Bank |

DBS Bank |

UOB Bank |

|

Market Cap (billion) |

64.6 |

100.9 |

50.5 |

|

Dividend Yield |

5.70% |

6.05% |

5.62% |

|

Price to Book |

1.22 |

1.70 |

1.16 |

|

Return on Equity |

13.4% |

17.5% |

11.9% |

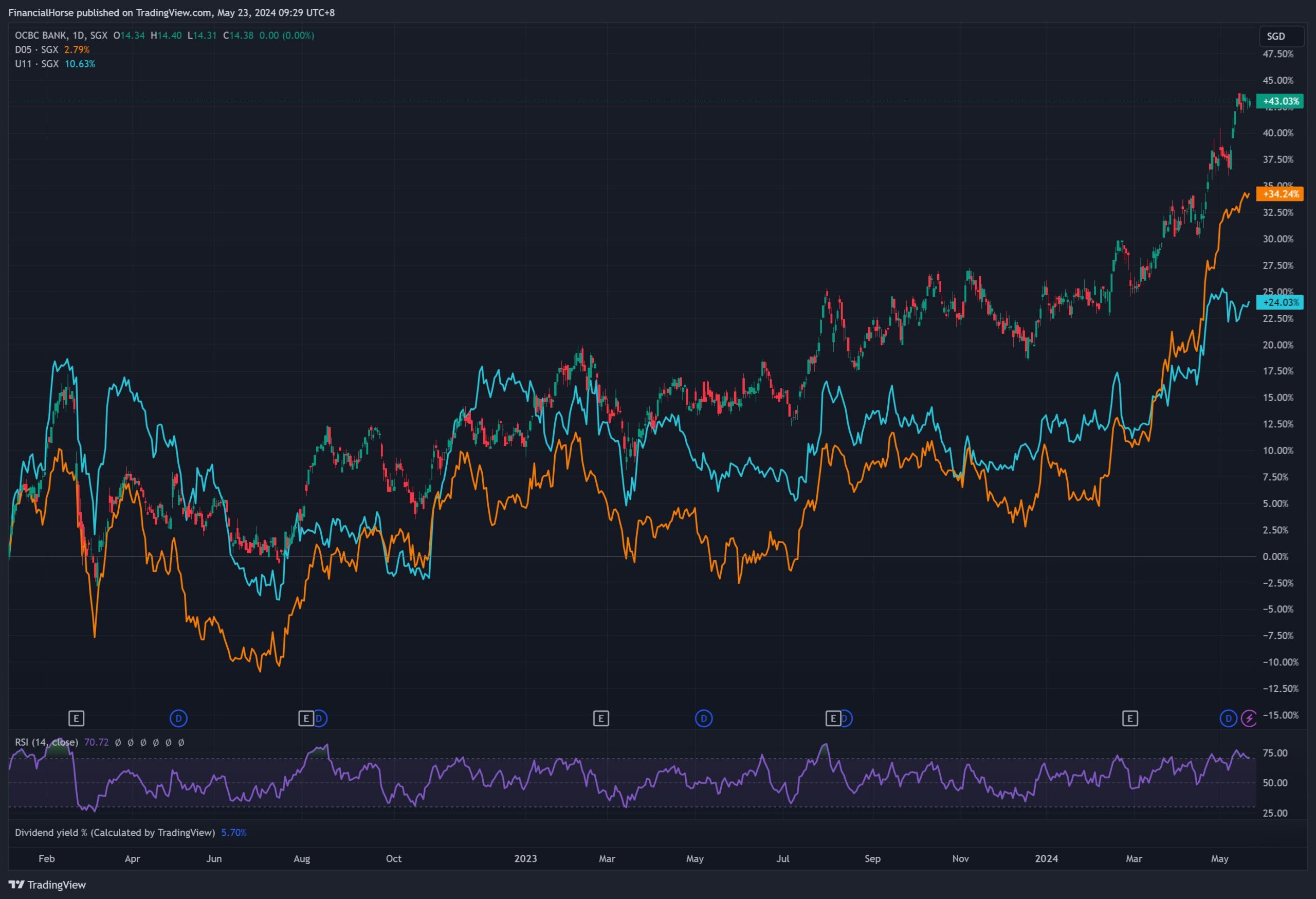

Price performance of OCBC Bank vs DBS Bank and UOB Bank

Here’s the price performance of OCBC Bank (candles) vs DBS Bank (orange) and UOB (blue).

Prices are dividend adjusted, and start from Jan 2022.

You can see how OCBC’s 43% total return has outperformed both DBS Bank and UOB Bank.

To be absolutely fair – this was because OCBC’s starting valuation in Jan 2022 was significantly lower than DBS Bank and UOB Bank (it was “cheaper” in Jan 2022).

This meant there was more room for OCBC Bank to “catch up” with DBS and UOB.

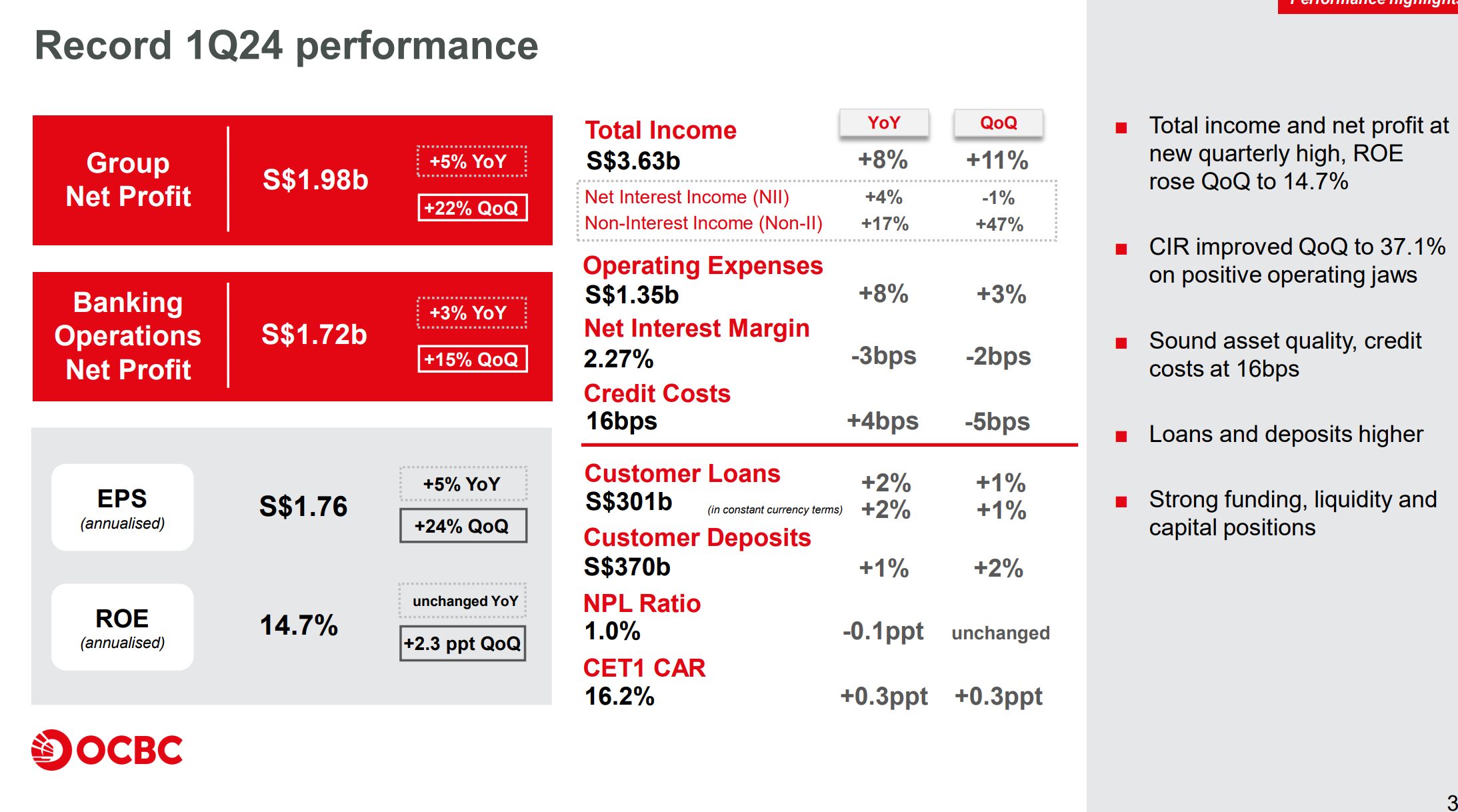

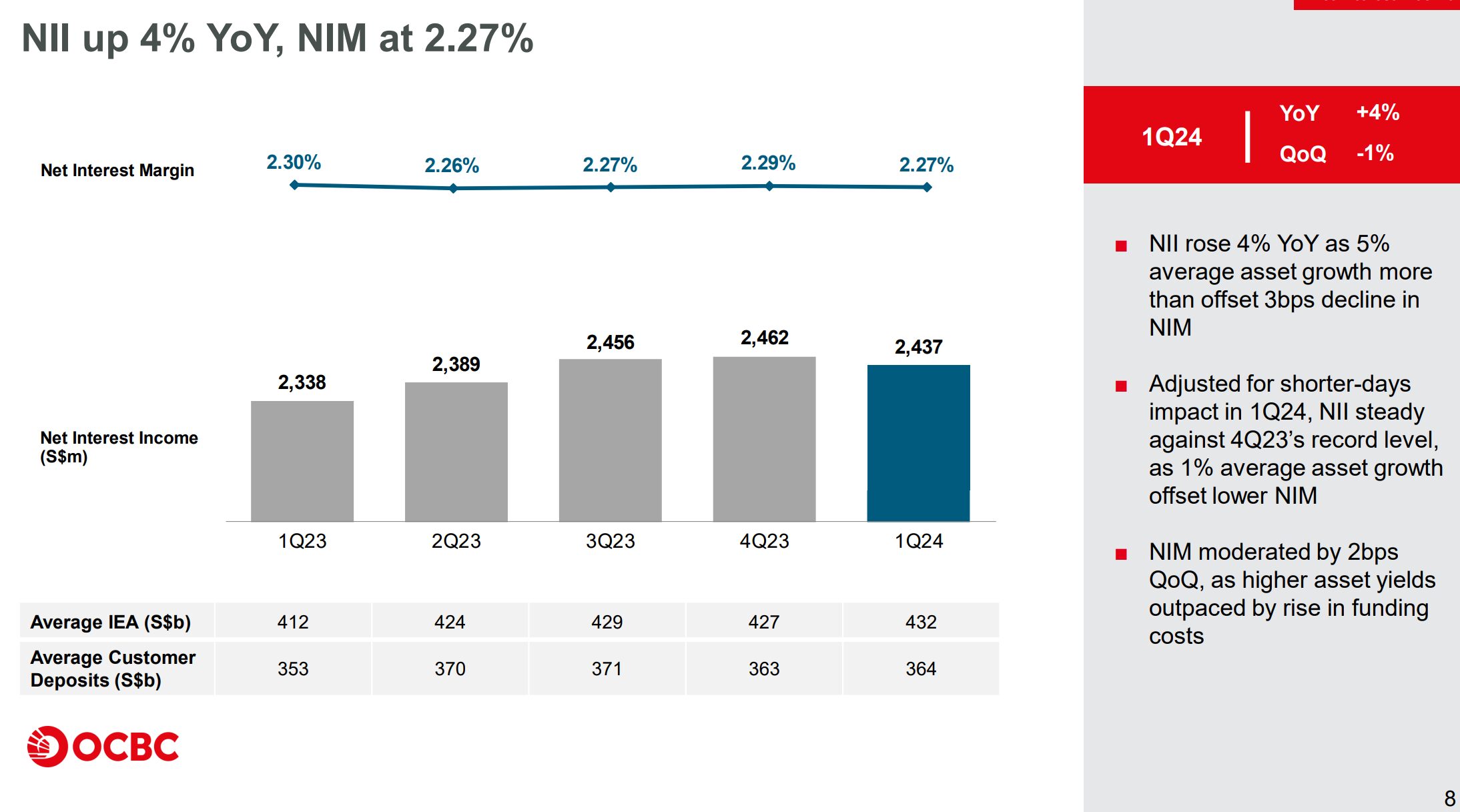

OCBC’s 1Q 2024 Financial Results are stellar

UOB Bank reported a drop in net profits in their latest financial results, which led to some worry that this would mark the top in earnings for Singapore bank stocks.

Well, OCBC’s latest results put that worry to rest.

Financial results are stellar across the board.

Net profit is up 5% year on year, and up 22% quarter on quarter.

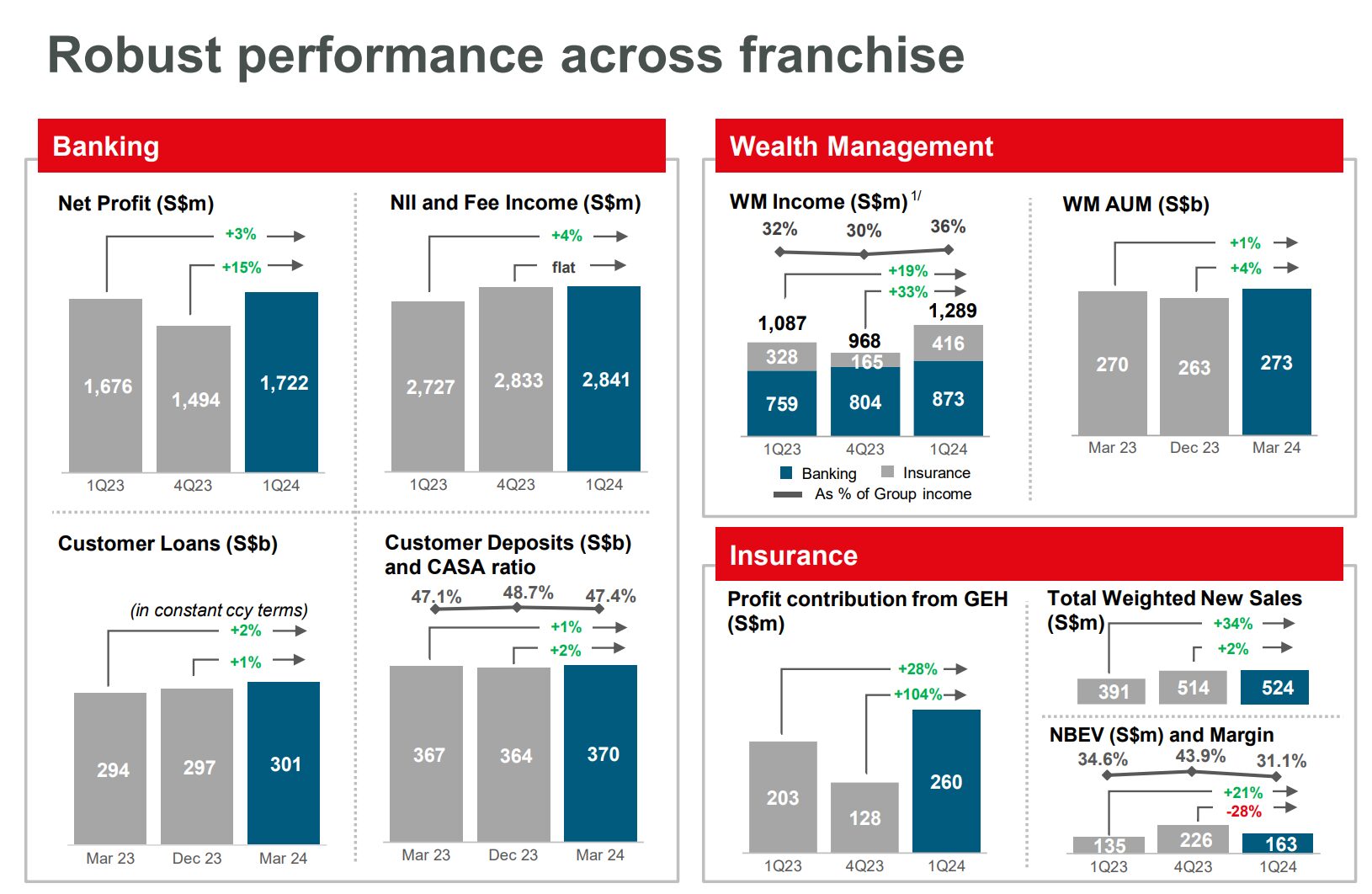

OCBC is firing on all cylinders – with every business unit from banking to wealth management to insurance reporting stronger performance.

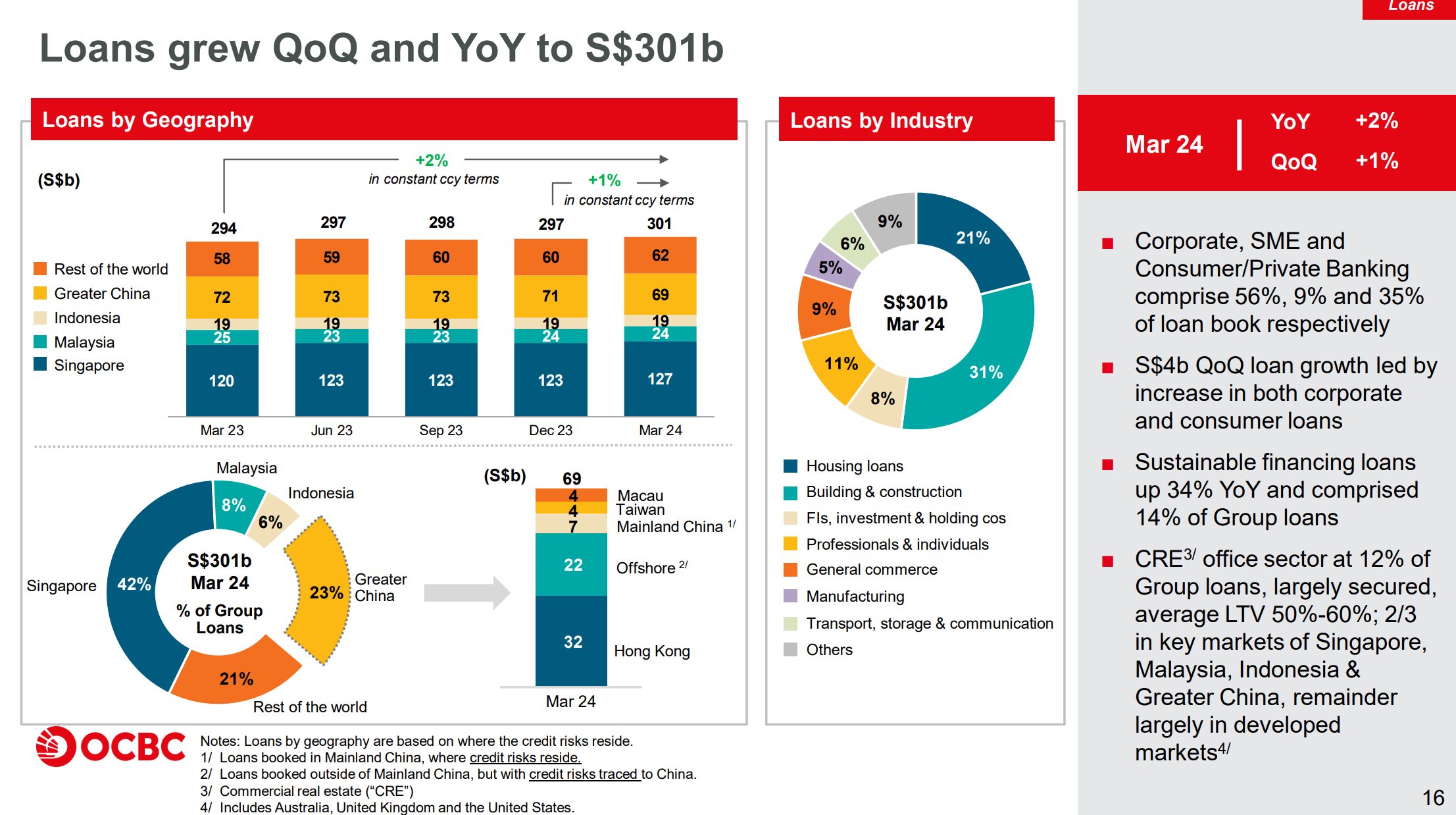

OCBC is reporting only 1% loan growth

Interestingly – the record profits come despite the fact that OCBC’s loan book grew only 1% on a QOQ basis (2% on a YOY basis).

Whether this is because of a lack of demand, or the banks themselves being conservative and not wanting to lend is not so clear.

I suppose this is not a bad thing.

Given all the uncertainty over the economy going forward, there’s no real need to go out there and make risky loans to make even more profits, only to have it come back and haunt you if there is an economic slowdown.

Especially when OCBC is already making record profits today despite the 1% loan growth.

OCBC’s Net Interest Margin down slightly – due to rise in funding cost

Net interest margins dipped slightly from 2.29% to 2.27%.

OCBC Bank’s explanation is that this is because of a rise in funding costs.

You can see below how 79% of OCBC’s funding base is customer deposits – basically the money you and I deposit with OCBC bank.

So they’re basically saying their interest margins are coming down because they have to pay us more on our deposits.

Have Net Interest Margins peaked for OCBC Bank?

At this point there’s no doubt the Feds are going to cut interest rates going forward.

The only question is how soon, and how many.

Whatever the case, the headline lending rate that OCBC lends at is likely to drop going forward.

This means that whether OCBC can preserve their Net Interest Margins going forward will depend very much on whether they can pay customers a lower interest on their deposit.

I suppose the answer here is likely yes, given the kind of market power OCBC bank has in Singapore.

UOB themselves just cut the interest rates on their flagship UOB One Account, and I would expect this to spread to the rest of the Singapore banks over time.

So who knows, maybe net interest margins can stay at current levels – as long as they cut the rates they pay on customer deposits.

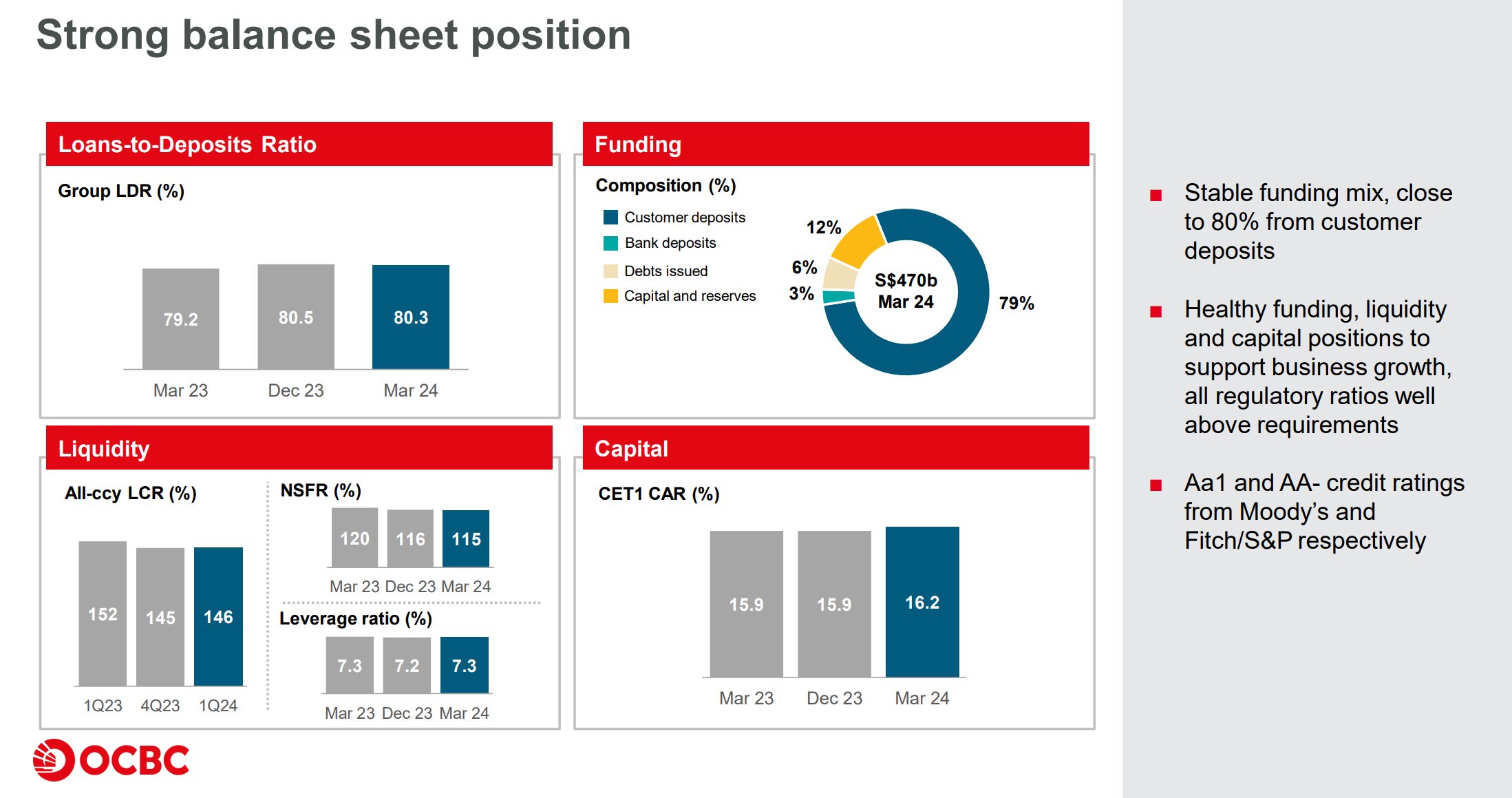

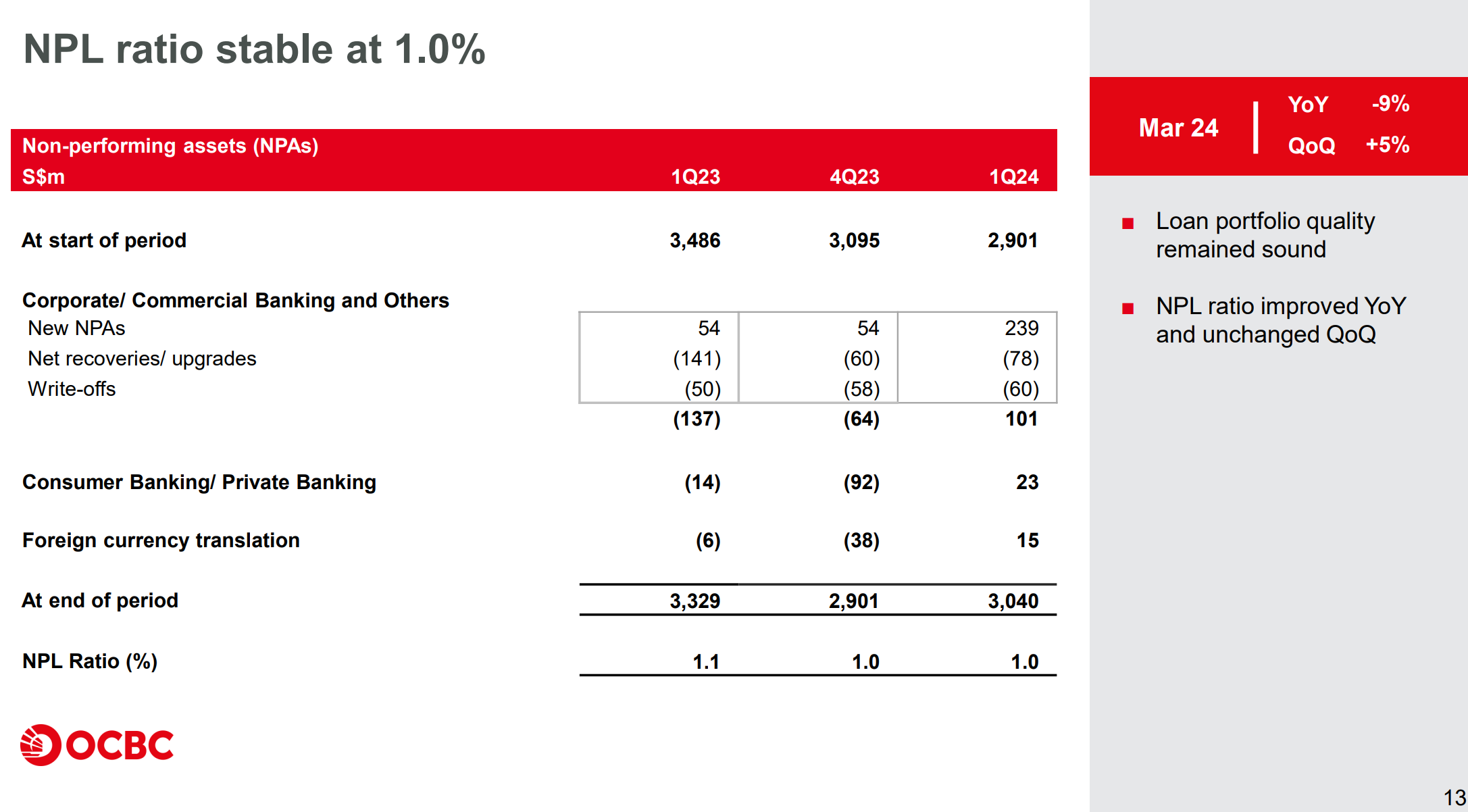

OCBC’s Balance Sheet is rock solid, Non-performing loans at 1.0%

Just for the record, OCBC’s balance sheet remains rock solid with a 16.2% CET 1 Ratio.

In simple English this means that for every $100 in deposits they have (okay to be very technical it is risk-weighted assets), they hold $16.2 in high quality assets (such as government bonds).

By banking standards, this is considered rock solid (JP Morgan by contrast runs about 15% CET 1 Ratio).

While Non-Performing Loans remains ridiculously low at 1.0% of the loan book.

OCBC Bank buys Great Eastern for $1.4 billion

Now the big news that a lot of you have asked me about.

OCBC Bank announced that they are making a $1.4 billion offer to buy the remaining 11.56% stake in Great Eastern that they do not already own.

Once completed, Great Eastern will be delisted and 100% owned by OCBC.

Why is OCBC buying Great Eastern for $1.4 billion?

Why is OCBC doing this?

Here’s what OCBC had to say (emphasis mine – my TLDR summary is below):

Oversea-Chinese Banking Corporation Limited (“OCBC”) today announced a S$1.4 billion voluntary unconditional general offer (“Offer”) for the 11.56% stake in Great Eastern Holdings Limited (“Great Eastern”) that it does not currently own, a move aimed at strengthening OCBC’s business pillars of banking, wealth management and insurance, and optimising its capital to enhance shareholder returns. OCBC’s corporate strategy gained strong momentum in 2023, leveraging OCBC’s strengths to capitalise on the vast opportunities in one of the world’s fastest-growing regions. The Offer is therefore in line with OCBC’s strategy to solidify its wealth management leadership position to drive growth by capturing rising Asian wealth.

…

OCBC Group Chief Executive Officer Ms Helen Wong said: “The Offer is a natural progression of OCBC’s strategy. We have moved intentionally to build up a strong wealth management franchise by hiring the best people and instituting best practices and processes, and raising our investment in Great Eastern. We have been looking at opportunities to best use our capital and believe the Offer allows us to deploy our resources into a key business that is expected to be earnings accretive to OCBC.”

Rationale

- A) Offer is in line with OCBC’s corporate strategy and strengthens its business pillars of banking, wealth management and insurance

First announced in 2022, OCBC’s corporate strategy is focused on four growth drivers to capture regional trade, investment and wealth flows. One of the growth drivers is to capture rising Asian wealth with its Singapore-Hong Kong-Dubai hubs and digital propositions.

In a fast-growing region that has seen rising demand for products and solutions to enhance and preserve wealth, bringing Great Eastern even closer to OCBC reinforces its long-term vision of becoming the leading wealth management player.

As Great Eastern has been part of OCBC’s stable of companies for decades, OCBC and Great Eastern share a strong synergistic relationship. OCBC is able to customise a full suite of investment, insurance and estate planning solutions for its customers, while Great Eastern has benefited from its access to OCBC’s extensive retail and commercial customer base.

- B) Offer enhances returns and optimises capital

The Offer is expected to be earnings accretive to OCBC.1 Great Eastern provides diversification to OCBC’s earnings base to deliver balanced earnings growth through economic cycles. Great Eastern has contributed an average of about S$700 million annually in net profit to OCBC over the past 10 years, which translates to an average of about 15% of OCBC’s annual net profit over this period.

The Offer presents an opportunity for OCBC to deploy its capital to generate greater returns for its shareholders. By increasing its investment in Great Eastern, OCBC can further capture the benefits from ongoing synergies and have a greater share of Great Eastern’s value.

1 Based on the financial statements of OCBC and Great Eastern for the financial year ended 31 December 2023.

Ms Wong added: “This is not the first time that we are making an offer to increase our investment in Great Eastern – first in 2004, followed by 2006. As OCBC has been the majority shareholder of Great Eastern for the past 20 years, the Group has entrenched institutional knowledge and expertise to manage the insurance business. We are confident this exercise complements our One Group, One Brand strategy. This will further accelerate our ambitious wealth management plans and build even tighter bonds and synergies across all our business pillars and key markets”.

What does that mean… in Plain English?

Okay that’s a whole lot of corporate speak, so let me break that down into plain English.

OCBC Bank is saying that wealth management is a key business for them, and over the years they have been putting a lot of effort into making Great Eastern great (no pun intended).

And eventually it got to a point where they said hey why not let’s just own 100% of Great Eastern ourselves.

We know the business, we like it, and it fits with our core strategy of wealth management.

AND – this is where I think is the crucial part.

Because of record earnings, OCBC is flush with cash.

Because of that they’ve been looking to deploy the cash somewhere.

They could have gone out and bought a whole new business like what UOB did with the Citibank credit card business.

Or they could have taken the safe route and bought an asset they already knew well – Great Eastern.

And they decided to go with the latter.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

For what it’s worth – I think this is a good acquisition by OCBC

I’m usually not a big fan of M&A.

I find that in M&A the buyer always overpays.

And all that corporate speak about reaping “synergies”?

Very little of it is actually realized in practice.

But for what it’s worth I thought this acquisition of Great Eastern by OCBC was a no brainer.

OCBC has a lot of cash to deploy because of record earnings.

Plus they already owned 88.44% of Great Eastern before this, and they are familiar with the business – so it’s not like they’re buying an unknown.

Did OCBC Overpay for Great Eastern?

Per OCBC:

“The Offer price of S$25.60 represents a 36.9% premium over Great Eastern’s last traded price of S$18.70 and premiums of 38.6%, 40.0% and 42.4% over the one-month, three-month and 12-month periods up to and including the last trading date of 9 May 2024.”

But here’s the long term chart of Great Eastern.

It’s a typical SGX stock, having gone nowhere for years.

So yes the 36.9% premium sounds big.

But in the bigger scheme of things it’s just 2019 prices.

And it works out to a reasonable 15.8x P/E ratio.

As M&A pricings go, I think this is a fairly attractive deal for OCBC Bank.

My views on OCBC Bank’s acquisition of Great Eastern

So for those of you asking me for my views on OCBC Bank buying Great Eastern – I think it’s a good deal for OCBC Bank.

It allows them to deploy some of their excess capital.

They are buying a known asset, so there’s not going to be any nasty surprises here.

And the valuation is attractive.

This makes it better than 90% of the M&A deals that I see listed companies try to do.

Judging by the market reaction – market seems to share similar views:

OCBC is buying back its shares at all time highs

What leaves me scratching my head though.

Is the decision by OCBC to repurchase their own shares at all time highs:

Yes they’ve only bought 1.9 million shares out of the 225 million shares they are authorised for.

That’s not even 1% of their buyback mandate.

But I mean look at the price of OCBC below.

I know they are flush with cash, but do you really have to throw it away buying back shares at all time highs?

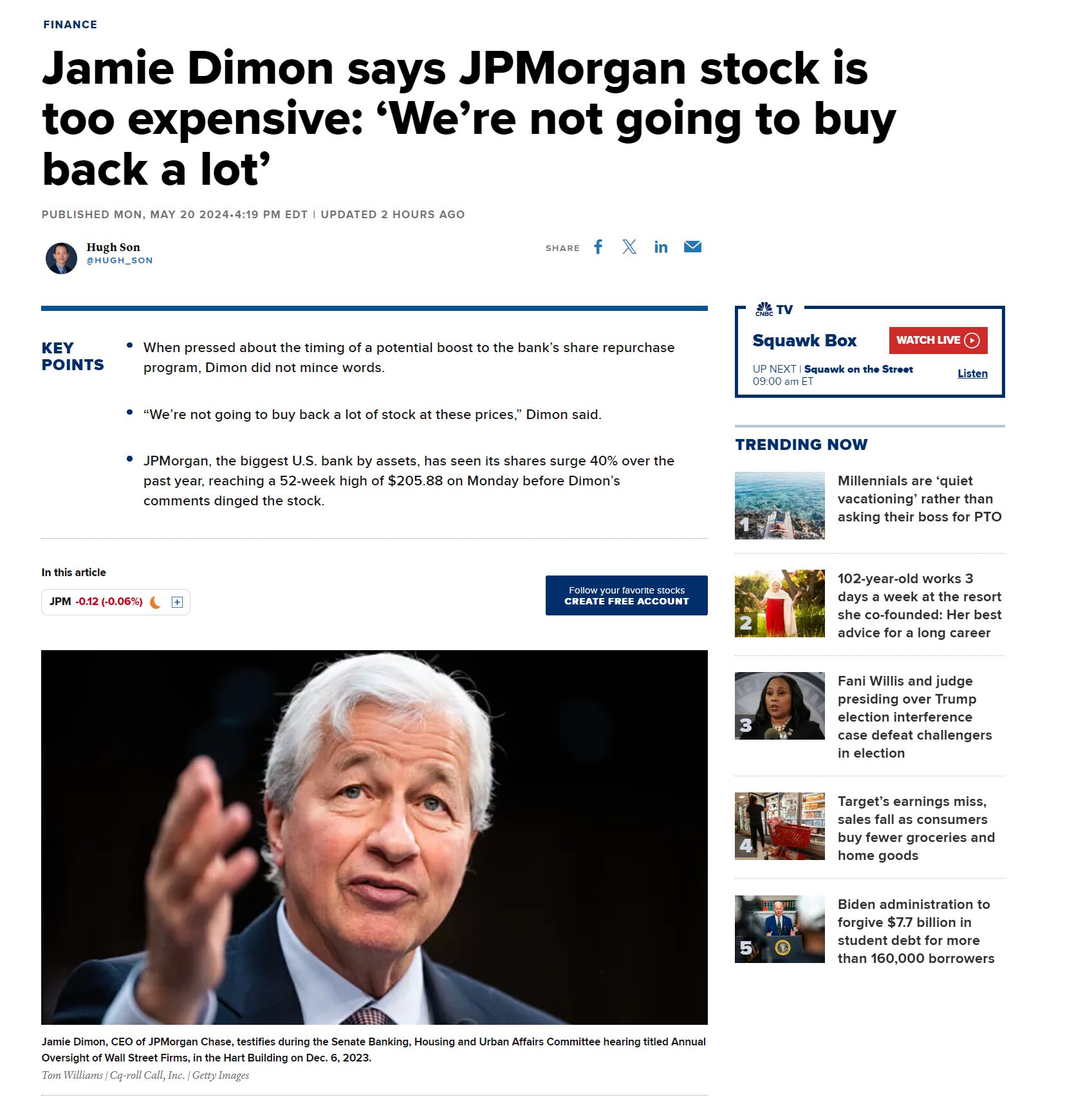

JP Morgan’s Jamie Dimon – Not buying back JP Morgan stock at this price

In fact, another great name in banking was doing the exact opposite this week.

Here’s what JP Morgan’s Jamie Dimon had to say, when asked whether JP Morgan would do a share buyback (emphasis mine):

“I want to make it really clear, OK? We’re not going to buy back a lot of stock at these prices,”

“Buying back stock of a financial company greatly in excess of two times tangible book is a mistake. We aren’t going to do it.”

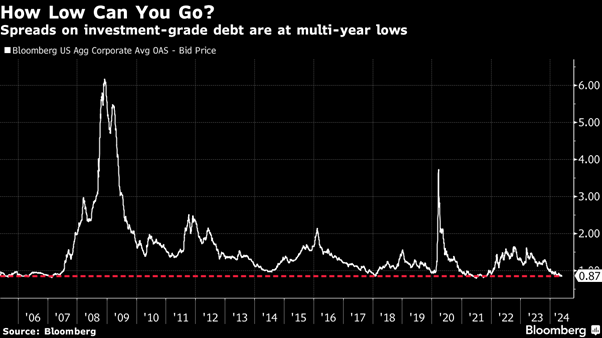

He went on to say that markets are currently underappreciating recession risks, and that prices of high-quality corporate bonds do not adequately reflect the potential for financial stress.

“The investment grade credit spread, which is almost the lowest it’s ever been, will be dead wrong… It’s just a matter of time.”

For the record – the chart below is the investment grade credit spread Jamie Dimon is referring to.

Helen Wong (OCBC CEO) vs Jamie Dimon – who is right here?

It never looks good when you’re doing the exact opposite from Jamie Dimon.

You’re either going to be right, or you’re going to be very wrong.

But to be fair to OCBC, I can see the line of reasoning here.

I’ve set out the relative valuations of OCBC Bank vs DBS Bank and JP Morgan below.

|

|

OCBC Bank |

DBS Bank |

JP Morgan |

|

Market Cap (billion) |

64.6 |

100.9 |

772 |

|

Dividend Yield |

5.70% |

6.05% |

2.1% |

|

Price to Book |

1.22 |

1.70 |

1.87 |

|

Return on Equity |

13.4% |

17.5% |

15.6% |

You can see how OCBC Bank at a 1.22x book value, is very much “cheaper” than either DBS Bank or JP Morgan, which are closer to 2x book value.

So by this logic, the buyback may make sense in that relatively speaking, OCBC shares remain “cheap”.

And the buyback is a way of “unlocking shareholder value”.

You could also argue that OCBC Bank operates in Singapore, which is a fundamentally different (and safer) market from JP Morgan in the US.

So I get what OCBC Bank is trying to do with their share buyback.

But only time will tell if this is the right decision.

I like their decision to buy Great Eastern.

Buying back OCBC stock at all time highs – I’m much less of a fan.

But… it is wise to pay caution to the fact that we are very late in the interest rate cycle

Back to the point that Jamie Dimon was talking about.

We are very late in the interest rate cycle.

The market seems confident on a soft landing scenario, but I’m a bit more realistic on this.

I think the more likely outcome is Jerome Powell is going to overshoot on this.

Either he is going to cut too early and inflation will return (together with an asset bubble).

Or he is going to cut too late and the economy will weaken / unemployment will go up (which leads to him cutting panic).

The former would be good for banks, the latter less so.

OCBC Bank pays a 5.7% dividend yield – Better buy than DBS or UOB Bank?

For what it’s worth.

After the huge run up in DBS Bank stock, personally I like OCBC Bank more here.

I think the 1.22x book value is more reasonable than DBS Bank at 1.70x.

And the 5.70% dividend is not much lower than DBS Bank either.

|

|

OCBC Bank |

DBS Bank |

UOB Bank |

|

Market Cap (billion) |

64.6 |

100.9 |

50.5 |

|

Dividend Yield |

5.70% |

6.05% |

5.62% |

|

Price to Book |

1.22 |

1.70 |

1.16 |

|

Return on Equity |

13.4% |

17.5% |

11.9% |

Will I buy more bank stocks in 2024? As a Singapore Investor?

The question that concerns me is how much to allocate to bank stocks, when we are this late in the interest rate / business cycle.

On that I have no easy answers.

As shared above, I can see a future where Jerome Powell cuts too early and reignites a financial asset bubble.

I can also see a future where Jerome Powell cuts too late and unemployment surges.

So it really goes back to risk management for me, and proper asset allocation.

You want the right mix of assets that will do well if Powell cuts early (inflating an asset bubble), yet also do okay if Powell cuts too late (with an economic slowdown / rise in unemployment).

You can see how my personal portfolio is positioned on FH Premium.

I’ve also just updated my stock & REIT watchlist to share the list of stocks I am keen to pick up, with rough target pricing.

This article was written on 24 May 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

WeBull Account – Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.