As many of you are aware, the US Federal Reserve recently raised interest rates by 0.25%, and projected another 2 rate hikes for the year. At the same time, the ECB announced that QE bond buying will halve to €15bn from €30bn per month from September 2018, end in December 2018, and interest rates will start going up in mid-2019.

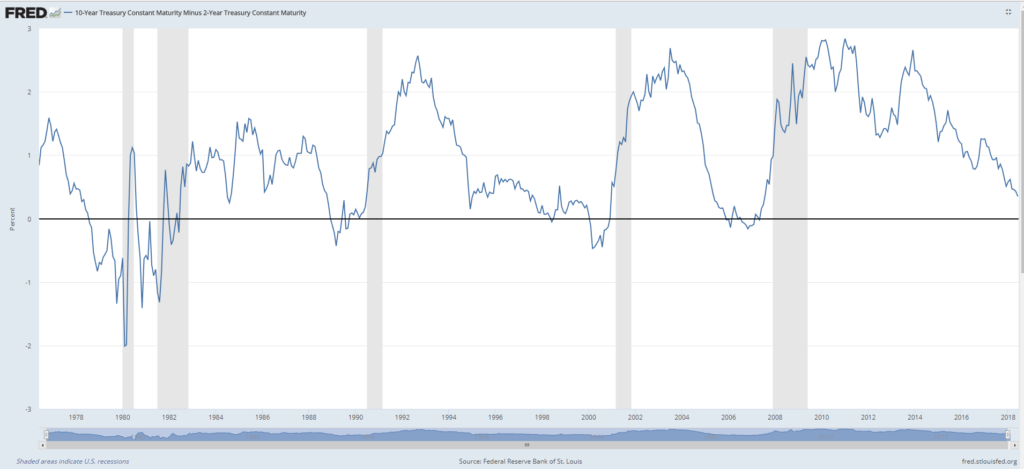

The US 2s10s Treasury yield curve has also fallen to its lowest point since 2007.

In fact, a recent study by JP Morgan showed that the global yield curve has inverted for the first time since 2007. With financial stress starting to build up in the system, I think it is a matter of time before the next recession hits. In fact a lot of the recent movements in financial markets looks like smart money is pulling out of Emerging Markets (including Asia and Singapore), and back to the US. My personal theory is that this explains the recent fall in Singapore stocks, especially the STI constituents, but I don’t have any concrete evidence to back up this thesis.

How then, should retail investors respond in such a situation? I read a recent article by Financial Samurai on how to make lots of money during the next recession, which makes these points: (1) Be OK with no longer making money, (2) Be at least neutral when the cycle turns. (3) Take some risk and go net short. (4) Go Long Volatility (5) Go Long US Treasuries (6) Go Long Gold (7) Go Long Yourself.

It’s a pretty nice read, and I would recommend readers to take a look if you have the time. Unfortunately, my personal gripe was that some of the strategies advocated require a bit of of market timing, as they require tactical asset reallocation prior to a recession. This means that you have to be able to roughly pre-empt when a recession is going to hit.

Historically, the yield curve inversion has preceded every single recession by about 12 to 18 month, but not every yield curve inversion has been followed by a recession. Or in other words, positive correlation does not necessarily imply causation. There have been instances where the yield curve inversion proved to be a false alarm, and there was no recession.

The problem then, is that if you sell all your assets to prepare for a recession, and no recession comes, you are going to very silly indeed.

In true Charlie Munger fashion, I decided to “Invert, always Invert”. The question I asked then, was what should an investor not do when preparing for a recession?

Sell all your stocks and move to US Treasuries/Gold

Not everyone may agree with me here, but I think that an investor should not sell all their stocks and move to safe haven assets like US Treasuries or Gold simply because of a yield curve inversion (or an impending one). As mentioned, one may not always be right in being able to call a coming recession, and the risk of getting it wrong is in sitting out the tail end of a roaring bull market, which could see you leaving massive gains on the table.

Personally I think the current bull market isn’t over yet, and we are going to see new highs before the end of this cycle, so I will continue to remain in my equity long positions. The UST 2s10s yield curve has also not inverted yet, so I think it’s a little premature to start calling for a recession.

Short Stocks

Shorting the market is a dangerous task. There is a saying that the market can remain irrational longer than you can remain solvent, which is why personally I never practice short selling strategies.

I know for a fact that a recession will eventually come around. But trying to predict exactly when that happens is a fool’s errand. Many number of events can be the catalyst that sparks off the next market sell-off.

Successful short selling requires you to identify the correct stock to short, and also get the timing right. That’s easier said than done.

Buy the VIX for extended periods of time

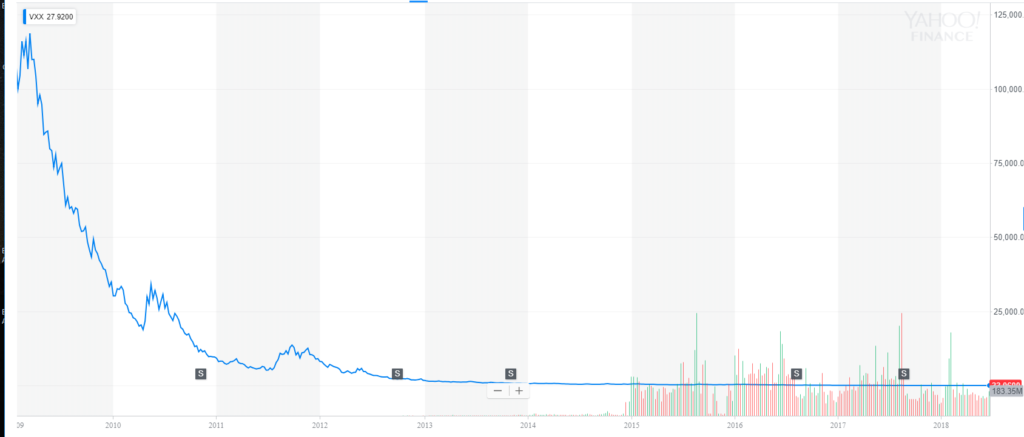

Another common trading strategy to profit from rising market volatility in a recession is to bet on the CBOE Volatility Index (VIX). There are many VIX ETFs out there that go both short and long (see eg. VXX, SVXY, VIXY), so the safest way to play the VIX is to buy an ETF. This way, your losses are limited to the amount invested in the ETF, as opposed to shorting the VIX directly where losses are theoretically unlimited.

I briefly dabbled in VIX ETFs during the Brexit and Trump election periods of turmoil, but I found that the main problem with VIX ETFs is decay. This deserves a full article by itself, but for the sake of simplicity, it is the problem where the VIX gradually falls in value over time, all things remaining constant. Just take a look at the long term chart for the VIX below.

This means that VIX ETFs should only be used for short term positions, and you should not be holding a VIX ETF for more than a few weeks.

This means that VIX ETFs should only be used for short term positions, and you should not be holding a VIX ETF for more than a few weeks.

Coming back to our original question, if you really want to bet on a market crash, VIX ETFs are probably a safer way than shorting stocks directly, but you really need to nail the timing, otherwise you are going to lose from the decay.

A note of caution, VIX ETFs were the ones that went bankrupt earlier this year due to a spike in volatility, so please be careful when trading with such instruments.

Go all in on risk assets without a liquidity buffer

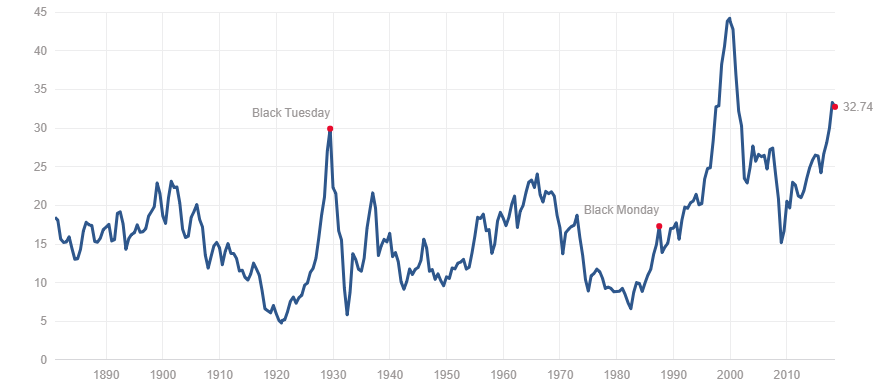

While the tail end of a bull market can see global asset prices soar to lofty valuations, it is important to stay grounded and not pour new money to chase after new highs. The higher that stocks go, the lower the future returns (historically at least). This is especially true when stock valuations are at the higher end of historical ranges, as can be seen from the Shiller PE Ratio below:

If you really want to continue throwing new money into the market that’s fine, but at least maintain a decent cash buffer so that you don’t go insolvent during a market crash. I wrote a previous article on how to calculate an appropriate buffer, so do check it out if you haven’t already.

Take up excessive leverage

A reader recently reached out to me with the question on whether he should use leverage to boost returns. Very simply, this is the idea where you borrow new funds at 2%, reinvest it in fixed income that generates 4%, and collect a nice 2% spread.

If this sounds like a free lunch in investing, that’s because it is, and its a highly risky strategy. It works fine and dandy when market are on escalator mode up, but when they start going down, you’re going to have a lot of sleepless nights.

The cheapest cost of funds is going to be via a refinancing of your existing mortgage, so if your investments don’t pay off, and you dont have cash lying around, you’re probably going to lose your house. If you’re taking margin from the bank, that’s even worse, because with a fall in stock prices they’re going to do a margin call.

I would only be comfortable with leverage strategies if I had sufficient liquidity lying around to meet any potential margin calls. However, if that’s the case, the question arises as to why would I not just invest my liquidity buffer directly, instead of taking up leverage.

I find it hard pressed to think of a situation where leveraging up is a good idea, especially given where we are in the current economic cycle. I would stay away.

Follow the strategy of anonymous blogger on the internet

And lastly, what you most definitely should not do as a retail investor, is to blindly follow the advice of an anonymous financial blogger on the internet.

With that in mind, this is what yours truly would do: I will not exit my existing equity or REIT positions. I will continue to invest over the next 2 to 3 years (focussing on blue chips stocks/REITs or ETFs), but I may gradually reduce the amount of new money I am putting into the market. At the same time, I may start to increase the portion of my risk free assets. With accounts such as DBS multiplier are yielding 2.3% these days, and SSBs yielding 1.72% for the first year, cash is starting to look pretty attractive.

| Year from issue date | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|

| Interest, % | 1.72 | 2.19 | 2.35 | 2.42 | 2.56 | 2.77 | 2.91 | 3.06 | 3.22 | 3.41 |

| Average return per year, %* | 1.72 | 1.95 | 2.08 | 2.16 | 2.24 | 2.32 | 2.40 | 2.48 | 2.55 | 2.63 |

Top Weekly Links

All Financial Horse does in his free time during the week is read financial news. With this new initiative (“The Weekly Horse”), hopefully some good can come out of it. During the week, I post articles that I enjoyed on the Facebook Group (do join if you want a sneak peak), and every Sunday I will collate the links for readers. I also take the opportunity to address queries from readers, or share any thoughts that I have for the week. If you enjoyed this post, do share your thoughts in the comments below!

The Ultimate Review Of All The REITs In Singapore And Here’s How You Can Learn To Invest.

Nice high level overview of the valuation metrics of S-REITs.

Interesting take on the viability of P2P lending.

Great article on the role of stocks and bonds in investing.

Nobody Likes the Micros (The Gambler Bias)

https://www.thegamblerbias.com/…/06/10/Nobody-Likes-the-Mic…

Success is like an iceberg. Everyone sees the top, but no one understands the hidden years of hard work and failure to get there.

Are you investing or speculating (Pension Partners)

https://pensionpartners.com/are-you-investing-or-speculating/

Quite enjoyed this article on the differences between investing and speculating.

“Whether you’re excited or nervous when your favorite asset falls in price marks whether you’re investing or merely speculating.” – Naval Ravikant

I’ve got some things to say (Romelu Lukaku)

https://www.theplayerstribune.com/en-us/articles/romelu-lukaku-ive-got-some-things-to-say

Okay this isn’t an investment article per se. But it’s the story of how one man’s tenacity allowed him to prevail in the face of adversity. And that’s a powerful lesson for all of us.

And also… WORLD CUP!!!

P.S. I didn’t realise Lukaku could write so well. Who said footballers are dumb?

Top Tech Talent is losing interest in working for Facebook (Business Insider)

https://www.businessinsider.in/Top-tech-tale…/…/64650851.cms

Peak Facebook?

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

One thing to be mindful of is that gold is increasing losing its status as a safe haven in uncertain times : https://www.marketwatch.com/story/heres-why-gold-isnt-acting-like-a-haven-despite-trade-turmoil-rattling-stock-market-2018-06-21?link=sfmw_fb

Interesting, why do you think that is the case?

But to be fair, these are the good times. I would be curious to see whether gold prices continue to trend downwards during a liquidity crisis when all hell is breaking loose.

Hi FH,

Good article. It is getting harder to forecast when the next recession will strike and I have avoided equities for the past 4 years. I still believe in gold. But nevertheless, like you, interest rates of SSB had caught my attention lately. Look forward to your next article!

Regards,

Gerald

http://www.sgwealthbuilder.com

Hi Gerald, thanks for the kind words. Yes, it can be hard to predict when markets will turn. 🙂

Hi FH,

Below is what I feel a good video about perspective of yield curve inversion. It also gives an overview of asset / sector ratio analysis for major turning points in the markets.

https://www.youtube.com/watch?v=G-xZeE2oXDs

Cheers!

Great video!