There are two fundamental rules in investing to abide by:

- Over the long run, a broad diversified portfolio of equities or real estate will give you the best total returns

- Never go bankrupt

Rule number 2 is perhaps the more important rule. The economy cycle, and global asset prices, are highly cyclical in nature. They go through 6 to 8 year periods of growth, followed by 2 to 3 years of recession which trims the excess, resetting the global economy and paving the way for another cycle of boom and bust. As long as you stay solvent at all times, you can live to fight another day. Your DBS shares may have fallen 50% in value, but as long as you have holding power, there is little doubt that one day it will return to, and surpass your original purchase price. If you are bankrupt however, it is effectively game over. Your liquidator will sell all your assets in a fire sale to repay creditors, and financially, that is a blow that will take you decades to recover from, if at all.

There are 2 ways to achieve rule number 2. The first is that you should never rely on leverage. Leverage can amplify your return in a bull market, making you wildly rich. When stocks are going down however, leverage can result in a margin call and your bankruptcy. The next way is to always maintain a cash buffer. I cannot stress how important this is. Every person should always maintain a portion of his/her assets in risk free, liquid assets, that can be drawn down at short notice, to tide through any emergency.

In this article, I will discuss the amount to put in a buffer, when is it permissible to draw on your cash buffer, and perhaps most importantly, where should you keep your buffer as a Singaporean.

Basics: Why do I need a buffer?

When I was researching this article, I came across numerous stories of Americans who had less than S$1000 in savings. They literally had no cash on hand to pay for an emergency such as a medical operation or car repair. If the following month’s paycheck failed to materialize, they were effectively insolvent.

I understand that there may be numerous circumstances why this had to be the case for them. Perhaps their family conditions meant they were struggling to make ends meet, perhaps they were suffocated by high rents in New York/San Francisco, perhaps they were working a lower paying job such as an internship to further their dream career. Financially however, this is a really risky move.

A cash buffer is vital for so many reasons:

Loss of Job – As a millennial myself, having grown up through the era of digitization, I think it is safe to say that no one’s job is safe these days. No matter how senior you are or how indispensible you think you are, the truth of the matter is that no one is irreplaceable. If your employer were to decide to cut costs one day, you could well be next on the chopping block. A cash buffer is therefore vital to tide you through to your next job.

Emergency – If an unexpected emergency happens, you may need a large amount of cash upfront to address an unexpected expense. Possible examples would include a major sickness where you have to pay the hospital before claiming from insurance, a fire to your home such that you need emergency cash while claiming insurance, a sudden divorce from your spouse etc.

Financial Crisis – The economic cycle, as its name implies, is cyclical. With a strong cash buffer, you are able to pick up fantastic blue chip stocks at ridiculous, fire sale prices, in a financial crisis. It also allows you to meet a rights issue/preferential offering by those pesky REITs, which is a virtual certainty in tight liquidity conditions. If nothing, a cash buffer in a financial crisis will give you a peace of mind, as you may be fearful for your job. A cash buffer allows you to make better investment decisions in such situations.

You never want to have to rely on your investments to address any of the above. These events (especially job loss) could well happen in the midst of a financial crisis, where your investments may have halved in value. To drawdown on your investments at that point in time would be a significant blow to your long term financial health, as it destroys the power of compounding.

How much buffer do I need?

“Financial experts” recommend a large range of buffers. I have seen recommendations ranging from:

- S$2000;

- 3 to 6 months’ expenses; to

- 6 months’ net income.

My personal take is that option 1 is too risky unless there are special circumstances why you can only maintain such a small buffer. For the average working adult, I would recommend something between options 2 and 3.

In my case for example, my cash buffer is based on a forward looking 12 months’ expenses. To calculate my 12 months’ expenses, I took a look at my rough expenses for the past 12 months, and buffered in any significant expense I see myself incurring in the next 12 months (eg. Buying a new house, having a baby etc). For myself, the numbers will work out at follows:

Monthly expenses:

- Food, transport, misc expenses – S$1,000

- Money to parents – S$1,000

- Holiday fund/Large ticket purchases – S$1,000

- Total – S$3,000

- 12 months’ worth = S$36,000.

Note: If you have a car, you should buffer in the car loan repayment, as well fuel and repairs. If you have a house, you should buffer in the mortgage repayment and monthly maintenance.

My theoretical minimum buffer is therefore S$36,000. Because I am extra kiasu, I added an additional 50% buffer to this to cater for any further unexpected situations, arriving at a final number of about S$50,000. This is my cash buffer, that I always have on hand at any time.

Why then, am I so conservative? First off, I recognize that such a large buffer is completely unnecessary. There is no need to buffer a buffer, much like there is no need to forecast a forecast. However, I do see myself incurring significant expenses for personal reasons in the near future. I also feel that the current market is slightly toppy, so I prefer to maintain a larger cash position. I enjoy the peace of mind that this offers me.

Ultimately, the amount that you choose to keep as a buffer is dependent on your own financial security and risk appetite. For the average working adult, I would recommend adopting one of the below:

1. 6 to 12 months’ expenses; or

2. 6 months’ net income.

When is it right to draw down on a buffer

Again there is no consensus on this. My personal take is that you can touch your cash buffer when:

1. There is a sudden emergency (medical or otherwise) such that you need to pay an unexpected expense urgently

2. When you lose your job, and you need to cover daily expenses

3. When you want to invest in a financial crisis

4. Pay off a large purchase

Items 1 and 2 are the very purpose of a cash buffer. Feel free to draw down in such situations.

Items 3 and 4 are more tricky. Investing in a down market can pay huge dividends in future. It is also tempting to dip into your cash buffer so you do not have to take up a large loan (eg. To cover renovation expenses). However, you should also keep an eye on your own financial security, to ensure your job and future income stream is not in danger, before going down this path. The worst possible scenario is to deplete your cash buffer investing in DBS stock in a crisis, only to get retrenched 3 months later (at which point the stock is down another 20%).

Where should I put my buffer

There are many websites out there that do a great job of summarizing the various savings accounts. In this article, I will only set out those that I consider using myself.

Note: I am not getting paid, nor will I get paid, for the following recommendations. All views expressed in this article are purely my own.

UOB One is the account I use for the majority of my cash buffer. As long as you spend S$500 on your UOB credit cards, and you credit your salary/pay 3 bills monthly via Giro, you enjoy a 2.43% effective interest rate on your first S$50,000. This is really attractive, as 2.43% is close to the 2.5% interest offered on the CPF Ordinary Account, or the 2% on a Singapore government bond. It even beats the 2.31% on a Singapore savings bond (which you only get after holding for 10 years).

This interest is credited into your account monthly, with no lock up period, and you are free to use the account like any other savings account. There really is no excuse for any young working adult not to have this account.

Open one, pair it up with a UOB ONE or UOB YOLO card, and not only do you earn extra interest, you also earn a rebate on your UOB Card. (Note: For the UOB Card to pick, use UOB YOLO if like me, you dine out on weekends often. Use UOB One if your expenses do not fall into any specific category.)

| Account balance in your UOB One Account | First S$10,000 | Next S$20,000 | Next S$20,000 | Above S$50,000 |

| Spend S$500 on your UOB One Card and/or selected Cards | 1% p.a. | 1.5% p.a. | 2% p.a. | 0.05% p.a. |

| Spend S$500 on your UOB One Card and/or selected CardsCredit your salary (min. S$2,000) or Pay 3 bills monthly via GIRO | 1.5% p.a. | 2% p.a. | 3.33% p.a. |

*Bonus interest is paid on first S$50,000 balance in your One Account.

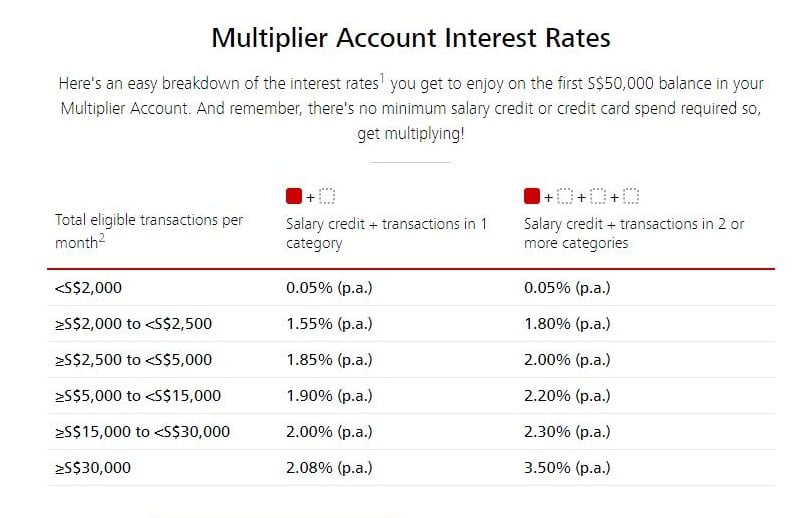

A lot of other bloggers and financial sites out there recommend DBS Multiplier. Yet DBS multiplier seems a lot less attractive to me (are these guys getting paid to promote DBS Multiplier?). Referring to the table below, you need to credit your salary, and do 1 of the following (credit card spend, repay home loan with DBS/POSB, repay insurance from DBS/POSB, or invest with DBS/POSB). If your combined spend/credit exceeds S$15,000, you will earn a 2.30% interest on your first S$50,000. This is ludicrous.

For me personally, I will fall within the S$5,000 to S$15,000 category, earning a 2.20% interest on my first S$50,000, which is lower than UOB One, for a lot more work.

DBS multiplier makes a lot of sense if your combined spend/credit exceeds S$30,000, after which you earn 3.50%. However if your combined spend/credit is that high, you probably have better things to worry about than your interest on a paltry S$50,000.

Source: DBS Multiplier website

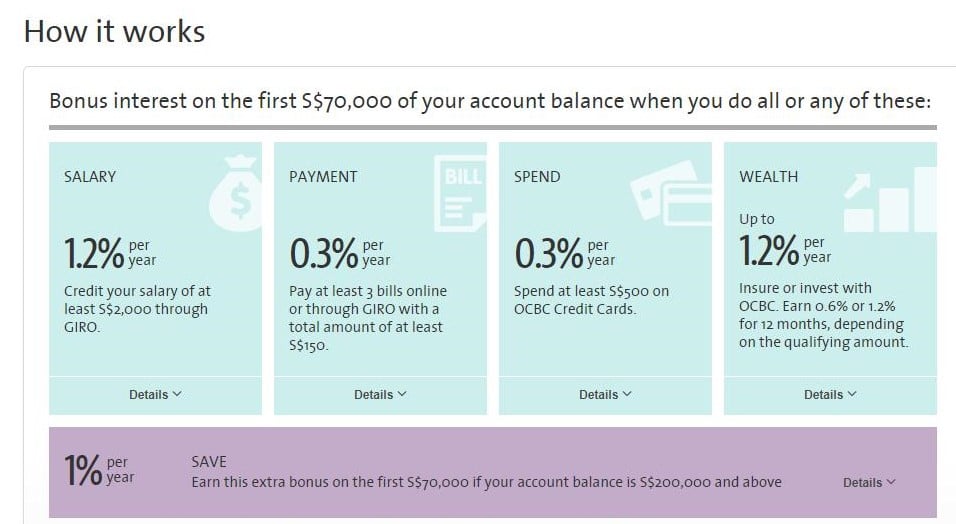

OCBC 360 was the account that sparked this craze of high yielding savings accounts. But oh how the great has fallen. When it first started, OCBC 360 offered a 3+ % interest and was the best in town. A number of revisions since has significantly reduced their interest. If I were to use OCBC fully today, I would only get a 1.8% on my first S$70,000. This doesn’t match up to the 2.43% on UOB one.

I continue to use OCBC 360 for spare cash beyond the S$50,000 in UOB due to legacy issues, as my salary is credited there and I have a number of GIRO payments linked to OCBC, so I enjoy a 1.5% interest. For new customers however, I recommend that you use UOB One, or if you really detest UOB’s user interface, the DBS Multiplier is an acceptable alternative.

Source: OCBC 360 website

One problem with the UOB/DBS accounts is the number of hoops you have to jump for the interest. For example, UOB requires that you spend S$500 on their credit cards, and either credit your salary or charge 3 GIRO payments to the account. There are many people who can’t be bothered to ensure that they meet this criteria, or that will not meet this criteria (eg. Their spend is less than S$500, or they do not have a salary credit (freelance work)). For such persons, the SSB is a fantastic alternative.

There are however, a few notable drawbacks to the SSB. The first is the yield. The SSB has a built in step up, so over 10 years, your average return a year is 2.31%, which compares favorably with UOB One. However in the first year, this is a mere 1.42%, and in the second it is 1.77%. The full numbers are reproduced below (for the March SSBs), but the essence is that If you need to redeem your SSBs before the 10 year mark due to an emergency, you are earning way less interest than if you had left the money in UOB One.

| Year from issue date | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Interest, % | 1.42 | 1.77 | 2.02 | 2.25 | 2.41 | 2.51 | 2.59 | 2.67 | 2.79 | 2.97 |

| Average return per year, %* | 1.42 | 1.59 | 1.73 | 1.86 | 1.96 | 2.05 | 2.12 | 2.19 | 2.25 | 2.31 |

Another issue is the timelag to redeem money from a SSB. As seen from the procedure below, the earliest possible time to redemption is by submitting a request on the 4th last business day of the month, with receipt of the proceeds by the end of the 2nd business day of the following month. That is a gap of 6 business days (8 calendar days minimum, realistically) before you can get your money. This also assumes ideal conditions when you submit your request on the last possible day. If you were unlucky enough to submit on the first business day of the month, you would need to wait an entire month to receive your money. This can be tricky where all of your cash buffer is in SSBs, as you may not have the liquidity on hand to make an emergency payment. For this reason, if you are primarily in SSBs, you will need to still maintain at least a few thousand in a savings account for any immediate drawdown.

Do note that there is no longer a need to time your withdrawal of the savings bond. The Government has kindly amended the structure to pay “accrued interest”, such that if you redeem before the half yearly interest payment, you will be paid “accrued interest” being the amount of interest that has accrued but not been paid.

To redeem your bond:

- Submit your redemption requests through the DBS/POSB, OCBC or UOB ATMs, or Internet Banking portals.

- Redeem in multiples of $500 up to the amount you have invested for each bond. You can redeem more than one bond per month.

- A $2 transaction fee will apply for each redemption request.

- Please note that you will not be able to amend or cancel submitted redemption requests.

- The redemption period opens at 6pm on the 1st business day of each month and closes at 9pm on the 4th last business day of the month. Redemption proceeds will be paid by the end of the 2nd business day of the following month.

Will I receive any interest?

- Savings Bonds pay interest every 6 months. If you redeem your bond when there is a scheduled interest payment, you will receive the scheduled interest together with your redemption amount. If you redeem before the scheduled interest is paid, you will receive a pro-rated amount, called the accrued interest, which is the interest you have earned but have not been paid.

Source: Singapore Savings Bonds Website

If you have a housing loan, your CPF Ordinary Account can be used to pay mortgage repayments. You can adjust your cash buffer accordingly, on the assumption that in an emergency, you can always draw down on your CPF OA to cover monthly mortgage repayments. CPF OA earns a nice 2.5% (extra 1.0% for first S$20,000), higher than even the 2.43% from UOB One, so you should always try to leave some money in CPF OA to earn the extra interest. At the minimum, always try to keep S$20,000 in your CPF OA as it earns 3.5%, and this can serve as the emergency fund for your housing loan.

Closing Thoughts

A comfortable cash buffer is about the best thing you can do for your financial health. It gives you a peace of mind, it allows you to tide through unexpected situations, and it helps you remain solvent if you were to lose your job or if there is a financial crisis. In fact, I would even go as far to say that you should never invest money in the stock market, until you have built up a cash buffer. This builds on the rule that before you can think about your potential gains, you first have to manage risk. If you cannot survive 6 months without your job or without selling investments, you should not be investing.

With your cash buffer, stick it all into a UOB One account (or DBS Multiplier if you have to). This earns a nice 2.43%, payable monthly with no lock up period, and in what is effectively a savings account. If you hate jumping through hoops to earn the extra interest, or if you cannot meet the criteria, put them in SSBs, while leaving a small sum in a savings account.

Once this is done, and your risk/downside is managed, you can then look to the stock market or REITs, to invest your “risk on” capital, and reap investment returns.

Enjoyed this article? Like our Facebook Page for more great articles!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. I share this with all my email subscribers at absolutely no cost. Sign up for the newsletter now!

[mc4wp_form id=”173″]

Hi FH, I’m a fresh graduate and am about to start my first job soon. I have been reading up on finance matters during the past week and have found your blog to be really useful by providing a general guideline on the things we should look out for as well as your way of doing it.

Cheers!

Thanks for the kind words! Hope it has been helpful. If you want me to write on any specific topi, just leave a comment! 🙂