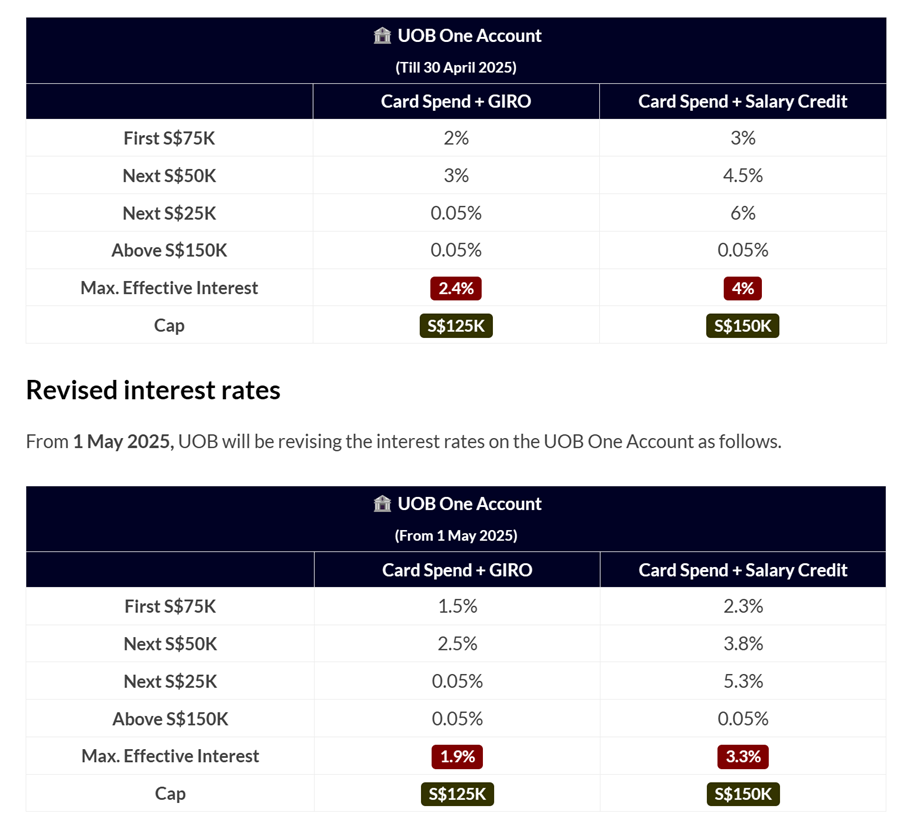

As you would know, UOB announced a drop in interest rates to their UOB One account this week (to 3.3% on $150,000, down from 4.0%).

With interest rates going down across the board, and plenty of volatility across stock markets globally.

I wanted to relook at the best places to park cash today.

Couple of things I wanted to discuss today:

- What are the Top Fixed Deposit Rates in Singapore today (Apr 2025)?

- Why are interest rates dropping?

- What are the alternatives to Fixed Deposit? T-Bills a better buy?

- Where would I put my cash today?

Top Fixed Deposit Rates in Singapore offer 2.58% yield (Apr 2025)

The full table is further below in the article, but I’ve summarised the best interest rates for the 3-, 6- and 12-month tenures below.

You’re looking at 2.58% for 3 months and 2.50% for the 6 months tenure.

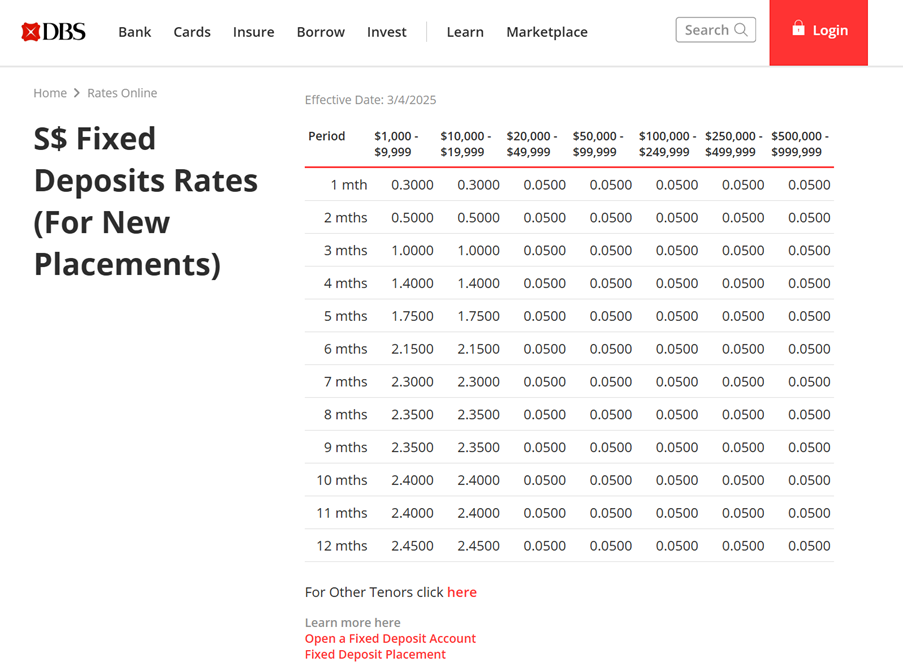

And 2.45% for the 12 months tenure (which very interestingly – is offered by DBS Bank).

| Tenure | Best fixed deposit interest rate (Apr 2025) | Bank |

| 3 months | 2.58% | GXS Bank |

| 6 months | 2.50% | State Bank of India |

| 12 months | 2.45% | DBS/POSB Bank |

GXS Bank:

DBS Bank:

Best Fixed Deposit Rates yield 2.60% if you deposit with Syfe Cash+ (to access institutional fixed deposit rates)

The rates above are assuming that you deposit with the bank directly as a retail customer.

Another way to do it is to use Syfe Cash+ Guaranteed.

The way this works is that you park the cash with Syfe, who will then deposit the cash into an institutional fixed deposit account.

This allows you access to institutional fixed deposit rates.

These are the latest interest rates from Syfe Cash+ below:

- 3 months – 2.60%

- 6 months – 2.55%

- 12 months – 2.20%

Note that Syfe Cash+ is not SDIC insured, but given that the underlying is fixed deposits risk should be on the low side (but not risk free).

Whether that is worth it for the additional yield, or whether you want the peace of mind that comes with being SDIC insured – I leave it for investors to decide.

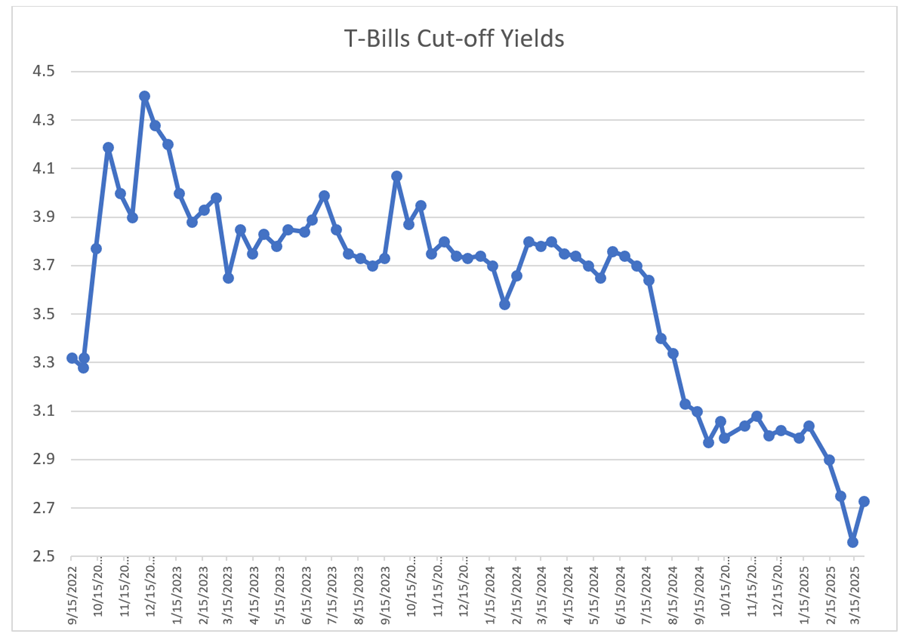

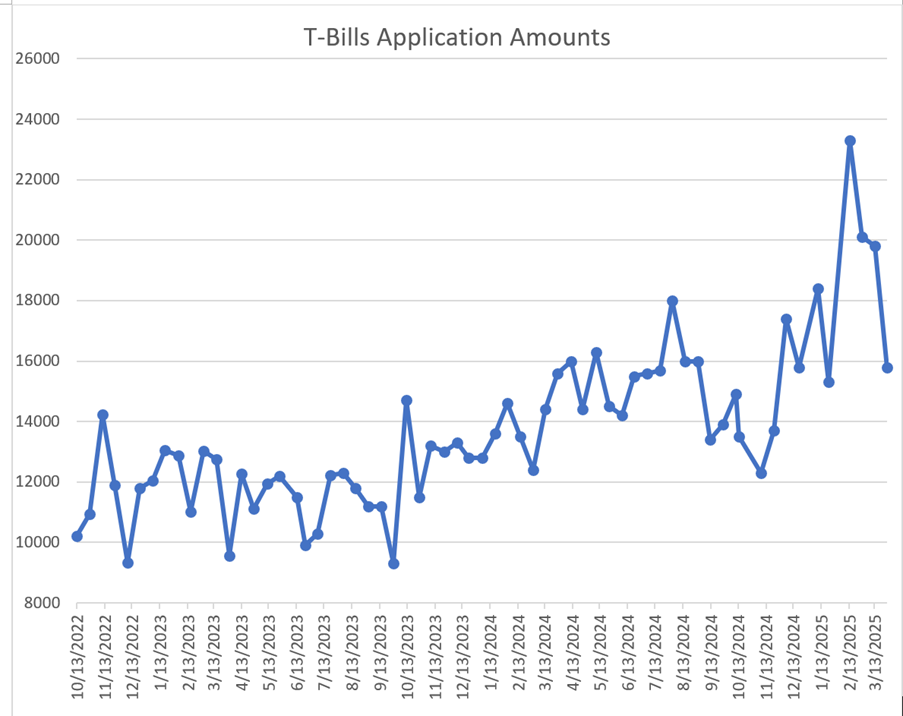

6-month T-Bills yields rise to 2.73% at last week’s auction – Will T-Bills yields stay up?

At the most recent T-Bills auction, the 6 month T-Bills rose to 2.73% yield.

This was a pretty sharp rise from 2.56% the previous auction.

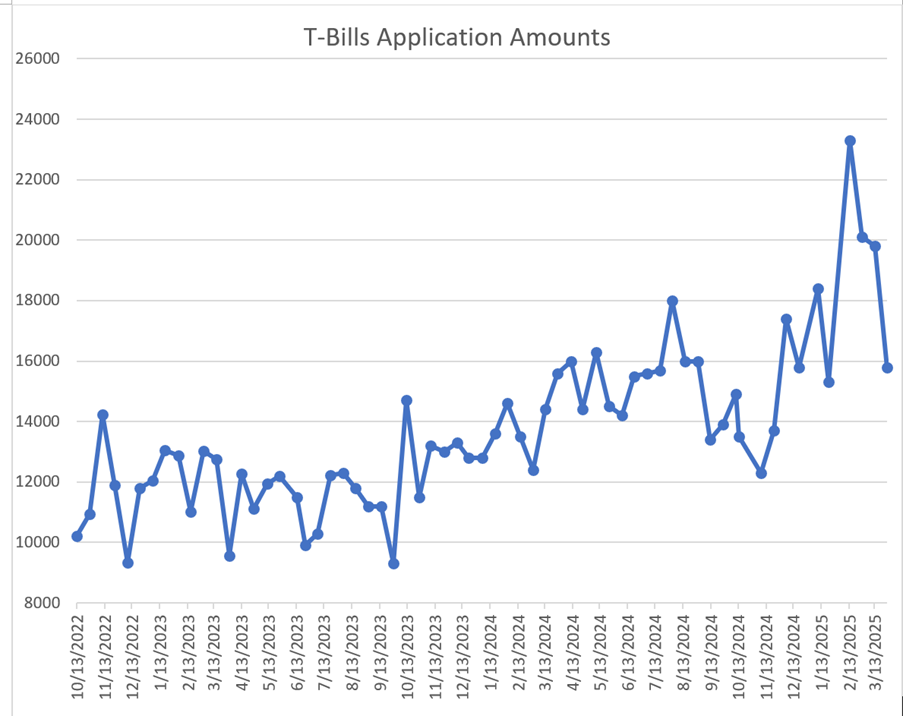

The reason – a sharp drop in investor demand for T-Bills.

Dropping from $19.8 billion to $15.8 billion.

Assuming T-Bills yields stay around this level (barring any sharp increase in investor demand).

Then actually T-Bills are pretty attractive again, compared to the yields from fixed deposits that we’re seeing above.

Comparing interest rates for T-Bills vs Fixed Deposits vs Syfe Cash+ Guaranteed across all tenures (Apr 2025)

I’ve tabulated the interest rates for the 3 cash options below, as well as with money market funds.

You can see how with the recent rise in T-Bills yields – T-Bills are back to being a pretty attractive option once again.

But if everyone realises this and we see demand for T-Bills soar, then well, we may see T-Bills yields drop back down to the 2.5ish levels.

| 3 months | 6 months | 12 months | Risk Free | |

| T-Bills yields | NA | 2.73% | 2.54% | Yes |

| Fixed Deposit (direct to bank) | 2.58% | 2.50% | 2.45% | Yes (if below $100,000 SDIC limit) |

| Syfe Cash+ Guaranteed (Institutional Fixed Deposit Rates) | 2.60% | 2.55% | 2.20% | No |

| Money Market Funds | ~2.6% | No | ||

Best Fixed Deposit Rates yield 2.58% – if you deposit directly with the bank (as of Apr 2025)

The full list of Fixed Deposit rates is set out below (bold being the most attractive for each tenure).

After the table I’ll share my views on:

- Why are interest rates dropping?

- What are the alternatives to T-Bills and Fixed Deposit?

- Where would I put my cash today?

| Bank | Interest rate per annum | Tenure | Minimum amount |

| GXS Bank | 2.58% | 3 months | $100 (maximum $60,000) |

| SBI | 2.50% | 6 months | S$50,000 |

| 2.40% | 12 months | S$50,000 | |

| Maybank | 2.45% (mobile placement) | 6 months | S$20,000 |

| 2.40% (mobile placement) | 9 months | S$20,000 | |

| 2.35% (mobile placement) | 12 months | S$20,000 | |

| Bank of China | 2.50% (mobile new placement) | 3 months | S$500 |

| 2.45% (mobile new placement) | 6 months | S$500 | |

| 2.40% (mobile new placement) | 9 months | S$500 | |

| 2.40% (mobile new placement) | 12 months | S$500 | |

| DBS/POSB | 2.45% | 12 months | S$1,000 (max S$19,999) |

| 2.35% | 9 months | S$1,000 (max S$19,999) | |

| ICBC | 2.40% (mobile placement) | 3 months | S$500 |

| 2.30% (mobile placement) | 6 months | S$500 | |

| Hong Leong Finance | 2.40% (mobile placement) | 9/10 months | S$5,000 |

| 2.35%(mobile placement) | 11/13 months | S$5,000 | |

| RHB | 2.20% | 3/6 months | S$20,000 |

| 2.10% | 12 months | S$20,000 | |

| CIMB | 2.30% | 3 months | S$10,000 |

| 2.15% | 6 months | S$10,000 | |

| 2.00% | 9/12 months | S$10,000 | |

| Citibank | 2.20% | 3/6 months | S$50,000 |

| UOB | 2.30% | 6 months | S$10,000 (fresh funds) |

| 2.00% | 10 months | S$10,000 (fresh funds) | |

| Standard Chartered | 2.20% | 6 months | S$25,000 |

| OCBC | 2.15% (mobile placement) | 9 months | S$30,000 |

| HSBC | 1.90% | 3/6 months | S$30,000 |

Why are interest rates dropping? Will this affect the next T-Bills yields auction?

There’s been a huge fluctuation in interest rate expectations of late.

First the market went to price in recession fears and more rate cuts.

Then less rate cuts due to inflation fears.

And then this week due to fears of tariff driven economic weakness, the market is now pricing 4 rate cuts in 2025.

This is massive, and likely to affect T-Bills yields.

So personally if you ask me, I would be surprised if we see T-Bills yields stay at the 2.73% range.

What are the alternatives to T-Bills and Fixed Deposit?

Let me outline the key alternatives to T-Bills and Fixed Deposits below.

Follow Financial Horse to avoid missing any post!

High Yield Savings Accounts – UOB One, DBS Multiplier, OCBC 360 etc

Interest rates for high yield savings accounts have been revised down of late.

UOB One has dropped interest rates

Just this week – UOB one announced a drop in their interest rates.

There’s a nice table from Milelion summarising the changes – effective interest rate on $150,000 has not fallen from 4% to 3.3%:

That said, if you can fulfil the criteria without too much trouble.

I still think it’s worth it, as the 3.3% is still higher than other options like fixed deposits, money market funds, or T-Bills.

That said, if you find it too much of a hassle, or don’t want to put the full $150,000 in, then just use the other options on this list.

Money market fund instruments (like MariInvest)

Alternatively there is MariInvest which is a money market fund that pays about 2.8% over the past 30 days for me.

This has definitely dropped, before it was 3.0% just a few weeks back.

There is some investor discretion required here as unlike T-Bills, money market funds are not risk free.

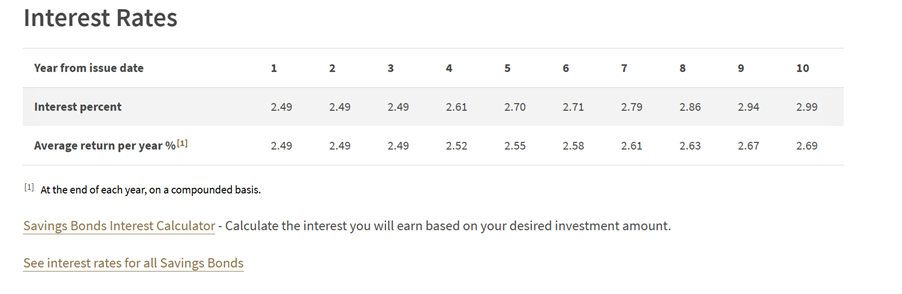

Singapore Savings Bonds are an acceptable alternative too

Interest rates on the latest Singapore Savings Bonds below.

You’re looking at 2.49% for the first 3 years, stepping up to 2.69% over 10 years.

I don’t think this is amazing, but you can see that it’s still comparable to the other fixed deposit style options above.

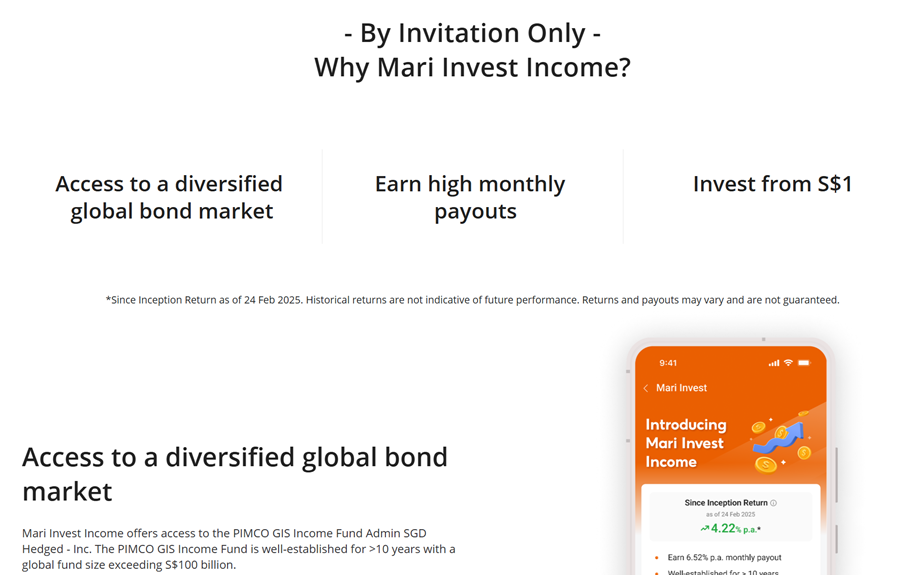

PIMCO GIS Income Fund via Maribank

For more duration, you can consider buying a bond fund.

One example is the PIMCO GIS Income Fund, that you can access via Maribank.

It’s known as Mari Invest Income, and is by invitation only for now.

I wrote a detailed review so do check it out if you are keen.

Bottom line is that these bond funds are quite a complex instrument, and not for everyone.

Because if interest rates go up, you can suffer mark to market capital losses.

And there is no way to hold to maturity as the bond fund will automatically reinvest proceeds.

So effectively there is some timing element involved here, in that you want to buy the fund when yields are high, and sell when yields are low, and if you do it the other way around you could see mark to market capital losses.

Best used only if you have a mid to longer term investment horizon.

Where would I put my cash today?

With the recent pickup in T-Bills yields, T-Bills are looking pretty attractive again.

The problem of course is that the recent rise in T-Bills yields is largely due to a drop in demand.

Now that yields are back up, I do worry that demand will jump again and yields drop back down to the 2.5ish range.

On top of that – the market pricing in a lot more interest rate cuts in 2025 could spill over and affect T-Bills yields.

Whatever the case, I haven’t really touched fixed deposits or T-Bills in a while, and most of the new funds I have are mostly parked in money market funds for now (I do have T-Bills, Fixed Deposit, and Singapore Savings Bonds purchased previously at higher yields).

Given the current market volatility, I also like keeping the liquidity on hand as I may choose to deploy the funds into the market any time.

But that’s just me – and I would love to hear what you guys think!

Where are you parking your cash for yield today?

This post is written on 4 April 2025 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.