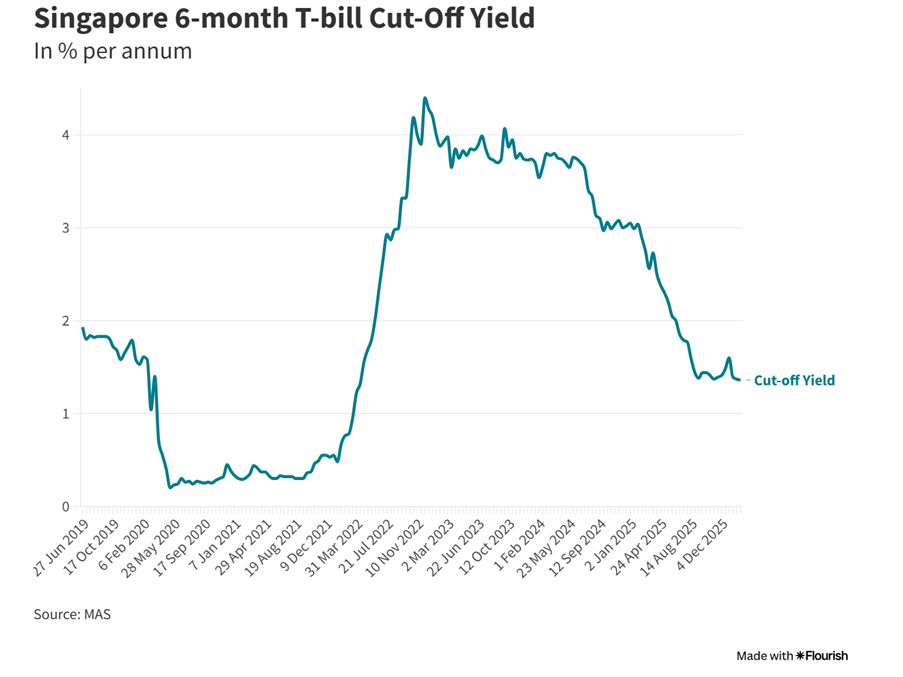

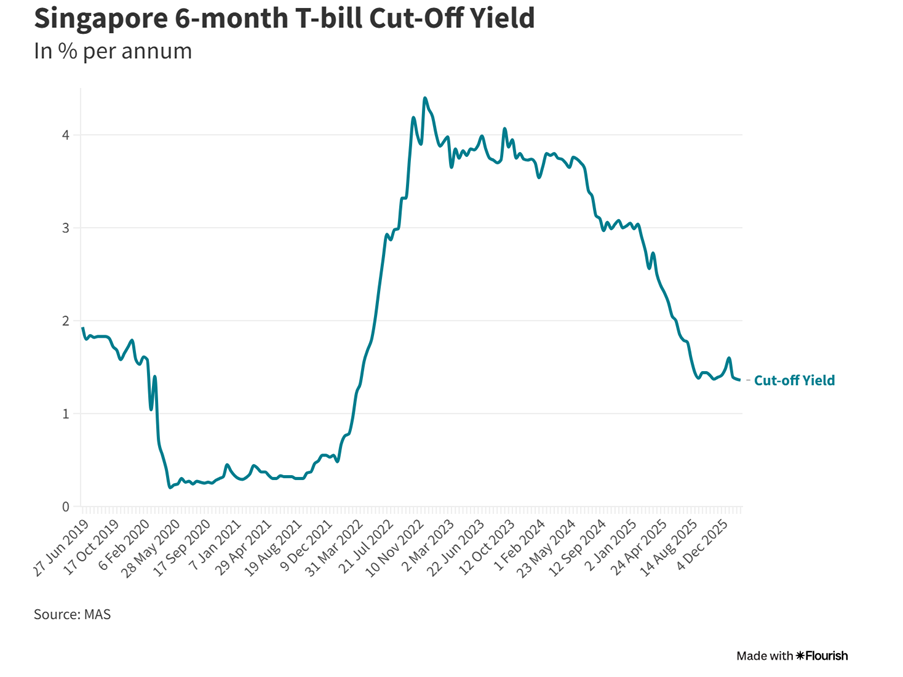

The latest 6-month T-Bills came in at just 1.36% yield at the 12 February auction.

At 1.36% yield, T-Bills have now fallen to their lowest level in recent years. Considering your cash is locked up for 6 months with no option to exit early, T-Bills are just not a great deal anymore.

And fixed deposits start looking pretty attractive once again – especially since rates at some banks have actually ticked up in February, with Chinese New Year promotions driving some short-term offers.

In fact, REITs or bonds offering 5.5% yield look like a pretty good buy in this interest rate climate, if you’re look for yield.

Couple of points I wanted to discuss:

- What are the Top Fixed Deposit Rates in Singapore today (February 2026)?

- With T-Bills yields dropping to 1.36%, are REITs, Bonds or Fixed Deposits a better buy?

- Where would I put my cash today?

Top Fixed Deposit Rates in Singapore (February 2026)

The full table is further below in the article, but I’ve summarised the best interest rates for the 3-, 6- and 12-month tenures below.

You’re looking at 1.35% for 3 months and 6 months tenure. And 1.40% for the 12 months tenure (requires $200,000 minimum at Bank of China).

For more accessible minimums, Bank of China offers 1.35% at 3 and 6 months from just $500 – which is the standout deal this month.

| Tenure | Best Fixed Deposit Rate (Feb 2026) | Bank |

| 3 months | 1.35% | Bank of China / ICBC ($200K+) |

| 6 months | 1.35% | Bank of China / Standard Chartered |

| 12 months | 1.40% | Bank of China ($200K+) |

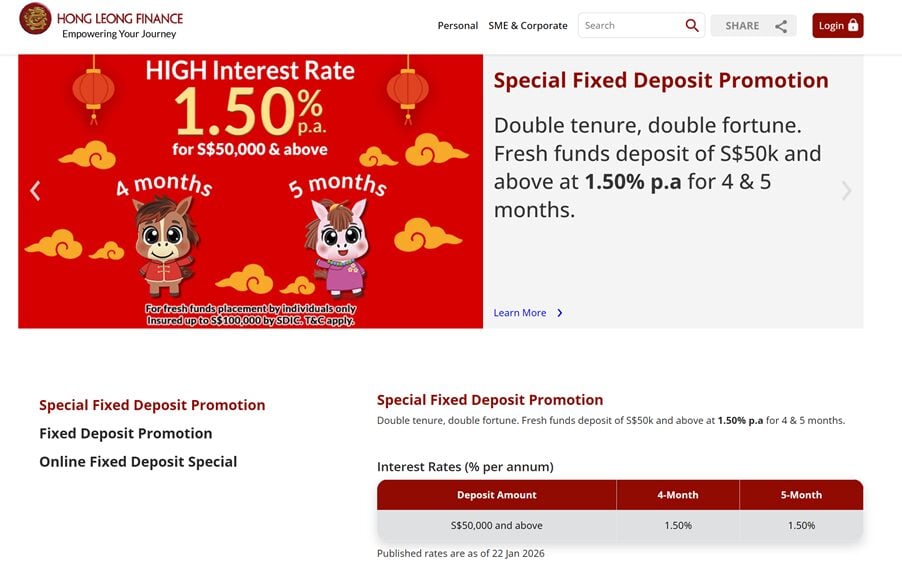

Note that if you’re using fresh funds, you can get 1.50% with Hong Leong Finance with a promotional rate today (4 & 5 months).

Which is probably the best rate on the market now.

Syfe Cash+ Guaranteed (Institutional Fixed Deposit Rates)

The rates above are assuming that you deposit with the bank directly as a retail customer.

If you park the cash with the bank as an institutional customer via channels like Syfe Cash+ Guaranteed, you actually get lower interest rates this time around.

Syfe Cash+ Guaranteed is currently offering up to 1.20% p.a. on the 12-month tenure (as of February 2026). This is below the best retail fixed deposit rates, which is a reversal from previous months when institutional rates were marginally higher.

In this rate environment, you’re probably better off just going direct to a bank like Bank of China – which has the added benefit of being SDIC insured up to $100,000.

6-Month T-Bills Yields Drop to 1.36%

Meanwhile, 6-month T-Bill yields continue their decline, coming in at 1.36% at the latest 12 February auction. This is down from 1.37% on 29 January, and significantly below the 1.6% level seen in December 2025.

The trend is clear – T-Bills yields have been steadily falling since the peak in late 2022, and there is no near-term catalyst for reversal.

Will T-Bills Yields Continue to Drop?

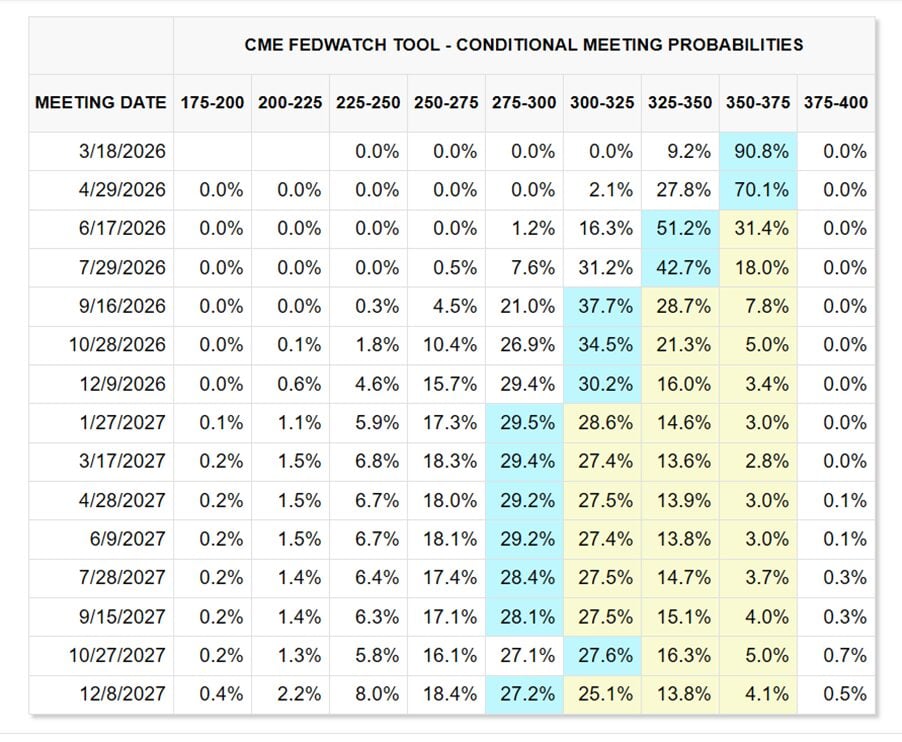

The Fed held rates steady at 3.50–3.75% at the January 2026 meeting. Markets are pricing in at most two further cuts in 2026, with futures pointing to potential moves in mid-year and late 2026 – though J.P. Morgan Research now sees the possibility of no cuts at all this year if the labour market holds up.

Kevin Warsh has been nominated as the next Fed chair (replacing Powell in May 2026), and while he is historically more hawkish, early indications suggest he may initially lean dovish to support the current policy trajectory.

Bottom line: the bias is still towards lower rates, but the pace of cuts has slowed dramatically. For Singapore, this means T-Bills and fixed deposit rates are likely to stay in this low range for a while, with gradual downward pressure.

Comparing Interest Rates: T-Bills vs Fixed Deposits vs Money Market Funds vs SSB (February 2026)

I’ve tabulated the interest rates for the key cash options below.

You can see how with the continued drop in T-Bills yields – retail fixed deposits are a pretty decent option.

Fixed deposits are SDIC insured, can technically be withdrawn any time unlike T-Bills, and the interest rates are v competitive vs T-Bills.

| 3 months | 6 months | 12 months | Risk Free | |

| T-Bills yields | ~1.35% | 1.36% | ~1.35% | Yes |

| Fixed Deposit (direct to bank) | 1.35% | 1.35% | 1.40% | Yes (if below $100K SDIC limit) |

| Money Market Funds | ~1.4% | ~1.4% | ~1.4% | No |

| Singapore Savings Bonds | N/A | N/A | 1.38% (1-yr avg) | Yes |

Full List of Fixed Deposit Rates (as of 13 February 2026)

The full list of Fixed Deposit rates is set out below (bold being the most attractive for each tenure).

After which I’ll share my views on the alternatives to Fixed Deposits.

| Bank | Interest rate p.a. | Tenure | Minimum amount |

| Bank of China | 1.40% | 12 months | S$200,000 |

| 1.35% | 3 months | S$500 | |

| 1.35% | 6 months | S$500 | |

| 1.32% | 12 months | S$500 | |

| 1.20% | 9 months | S$500 | |

| Hong Leong Finance | 1.50% (Special Promo) | 4/5 months | S$50,000 (fresh funds) |

| 1.25% (online banking) | 5/6/8/11/13 months | S$20,000 and above | |

| 1.20% (online banking) | 5/6/11/13 months | S$5,000 to < S$20,000 | |

| Standard Chartered | 1.35% (Fresh Fund Promo) | 6 months | S$25,000 (fresh funds) |

| ICBC | 1.35% (E-banking) | 3 months | S$200,000 and above |

| 1.15% (E-banking) | 3 months | S$500 to < S$200,000 | |

| 1.15% (E-banking) | 6 months | S$200,000 and above | |

| 1.00% (E-banking) | 9/12 months | S$500 | |

| Maybank | 1.32%^ (Deposits Bundle) | 9/12 months | S$20,000 |

| 1.30% (online banking) | 6/9/12 months | S$20,000 | |

| MariBank | 1.58%* (CNY Promo) | 3 months | S$10,000 to S$50,000 (selected users) |

| 1.30% | 12 months | S$100 (max S$100,000) | |

| 1.20% | 6 months | S$100 (max S$100,000) | |

| GXS Boost Pocket | 1.30% | 3/8/12 months | S$100 (max S$85,000) |

| CIMB | 1.30% | 3/6/12 months | S$10,000 |

| RHB | 1.25% | 12 months | S$20,000 |

| 1.20% | 3/6 months | S$20,000 | |

| UOB | 1.20% | 6 months | S$10,000 (fresh funds) |

| 1.00% | 10 months | S$10,000 (fresh funds) | |

| OCBC | 1.20% (online banking) | 12 months | S$20,000 |

| 1.15% (online banking) | 9 months | S$20,000 | |

| DBS/POSB | 1.00% | 9/12 months | S$1,000 (max S$19,999) |

| 0.80% | 6 months | S$1,000 (max S$19,999) | |

| SBI | 0.90% | 6 months | S$200,000 |

| 0.80% | 12 months | S$200,000 | |

| HSBC | 0.85% | 6/12 months | S$30,000 |

| 0.80% | 3 months | S$30,000 | |

| Citibank | 0.70% | 12 months | S$10,000 |

| 0.60% | 3/6 months | S$10,000 |

What Are the Alternatives to T-Bills and Fixed Deposits?

Let me outline the key alternatives below.

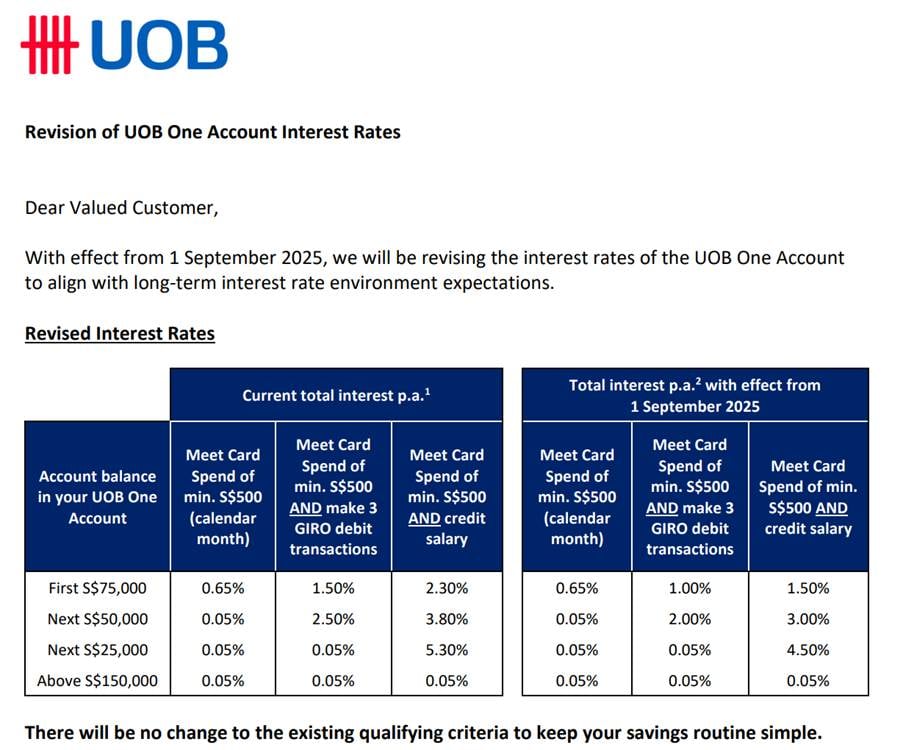

High Yield Savings Accounts – UOB One, DBS Multiplier, OCBC 360 etc

Interest rates for high yield savings accounts have been revised down of late.

UOB One pays an effective interest rate of 2.50% on $150,000, if you hit the criteria of $500 credit card spend and salary credit.

If you can fulfil the criteria without too much trouble, I still think it’s worth it, as the 2.5% is still meaningfully higher than fixed deposits or T-Bills.

That said, if you find it too much of a hassle, or don’t want to put the full $150,000 in, then it probably doesn’t make sense. And you’re better off with the other options on this list.

Money Market Fund Instruments (like MariInvest)

Money market funds are paying about 1.4% based on the Fullerton SGD Cash Fund’s 7-day annualised yield as of 12 February 2026.

Given T-Bills are yielding 1.36%, money market funds are a pretty decent option right now, especially as you can get the money back any time with T+1 liquidity.

There is some investor discretion required here though, as unlike T-Bills, money market funds are technically not risk free.

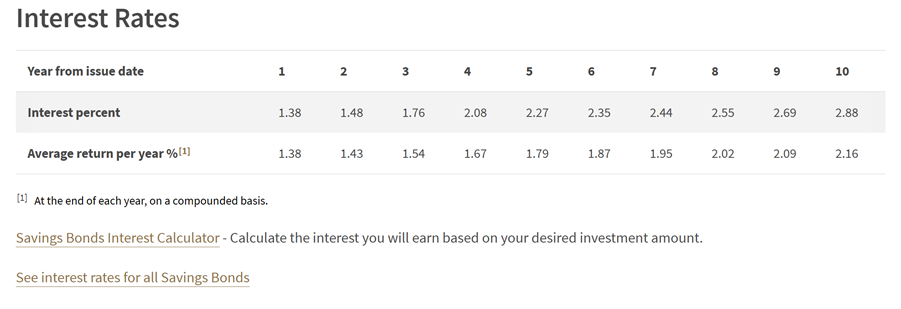

Singapore Savings Bonds – A Solid Alternative

The latest SSB (March 2026 tranche, SBMAR26) offers 1.38% for the first year, stepping up to 2.16% over 10 years.

This is actually competitive vs fixed deposits and T-Bills. And being risk free + able to withdraw with 1 month’s notice, it’s actually well worth checking out.

The February 2026 SSB (SBFEB26) was even better at 1.35% for Year 1 and 2.25% over 10 years – the first time the 10-year average climbed back above 2% in months. If you believe rates will continue falling, locking in a 2%+ 10-year return via SSB is a smart move.

What About REITs or Bonds?

Long story short – I think REITs are a pretty decent buy today, especially with the sharp drop in interest rates.

But after a big rally in 2025, at current prices, don’t expect the same capital upside any more.

That said.

A blue-chip REIT pays about 5.5% dividend yield.

This was a lot less sexy when you could get 3% on a T-Bill (2.5% yield spread). But when a T-Bill is at 1.36%, you’re getting a whopping 4.1% spread vs a T-Bill.

Not risk free though, and at these prices, there is risk of mark to market losses if interest rates go up.

So there’s no free lunch.

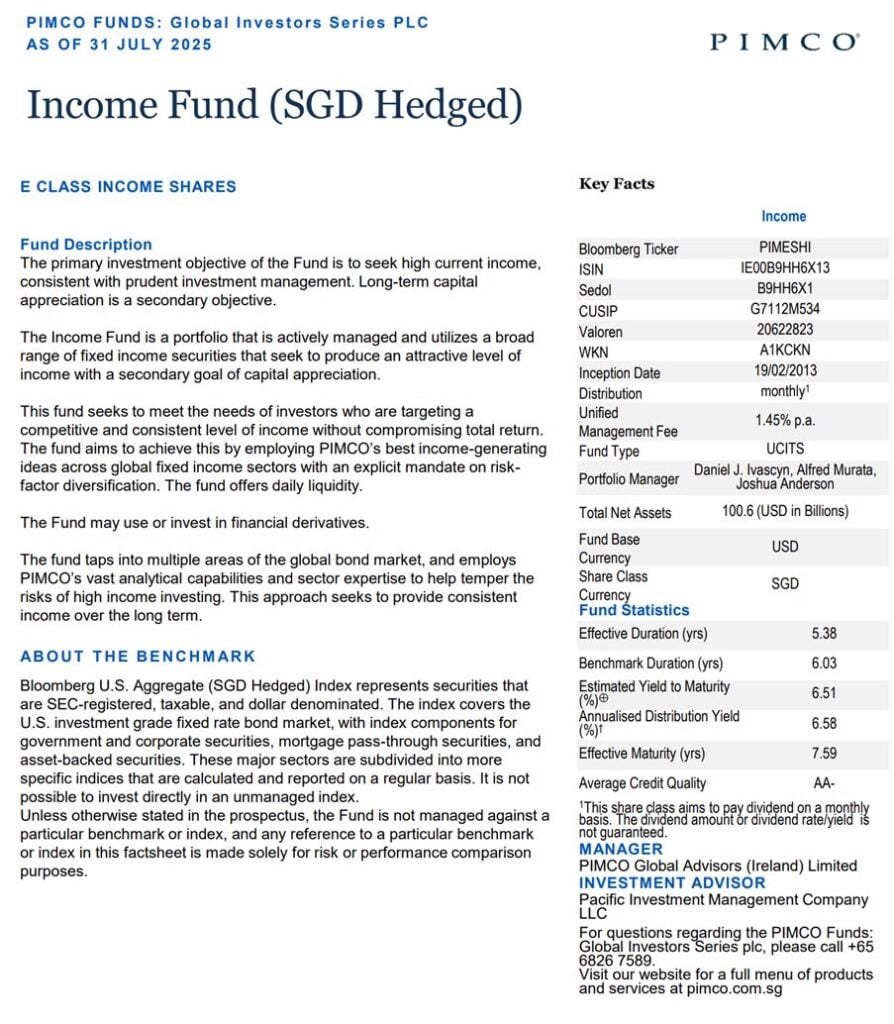

PIMCO GIS Income Fund via Maribank

Alternatively, if you are comfortable with some risk and duration, but don’t like REITs, you can also consider buying a bond fund.

One example is the PIMCO GIS Income Fund, that you can access via Maribank.

I wrote a detailed review so do check it out if you are keen.

Bottom line is that these bond funds are quite a complex instrument, and not for everyone. Because if interest rates go up, you can suffer mark to market capital losses. And there is no way to hold to maturity as the bond fund will automatically reinvest proceeds.

So effectively there is some timing element involved here, in that you want to buy the fund when yields are high, and sell when yields are low. Best used only if you have a mid to longer term investment horizon.

But that being said – the thought process here is similar to REITs. If you are comfortable with some risk of capital loss, then you can get a 5%ish yield on something like the PIMCO GIS Income Fund today. That’s worth considering.

Digital Banks – MariBank and GXS Boost Pocket

One new development worth noting is that digital banks are getting more competitive in the fixed deposit space.

MariBank is running a Chinese New Year promotional rate of 1.58% p.a. on a 3-month fixed deposit for selected customers (S$10,000 to S$50,000). If you’re one of the lucky ones who received this offer, it’s the highest FD rate in the market right now. Their standard rates are also decent at 1.30% for 12 months from just $100.

GXS Boost Pocket is offering 1.30% for 3-, 8- and 12-month tenures, with no penalty for early withdrawal (you still get the base interest of 1.08% p.a. up to the date you withdraw). The minimum is just $100 with a cap of $85,000. Not bad for the flexibility it offers.

Where Would I Put My Cash Today?

Personally I haven’t really touched fixed deposits or T-Bills in a while, and after today’s article I don’t really see much that would lead me to change my mind.

Most of the cash that I want in low risk instruments – I’m parking in money market funds, or UOB One (or Singapore Savings Bonds purchased previously at 3%+ yields).

But that’s just me – and I would love to hear what you guys think!

Where are you parking your cash for yield today?

CFA & PIMCO

CFA & PIMCO

I also bought the PIMCO Low Duration Income Fund, which has a duration of less than 3 years, hence less susceptible to interest rate hike. Pretty good yield.