One of the most common questions I get on this site is “How to invest in Vietnam?” and “Are Vietnam stocks a good buy?”

Now I was in Vietnam the past week, and I must say, I really get the popularity of this question. Vietnam in many ways looks and feels like China was back in the early 2000s, and a lot of the economic and demographic data backs that up. If any of the promise about Vietnam turns out to be true, there’s going to be massive upside here for any foreign investor who invests in Vietnam.

Basics: Vietnam Stock Exchange?

The Ho Chi Minh City Stock Exchange or Ho Chi Minh Stock Exchange (HOSE or HSX) is the main stock exchange in Vietnam.

It’s basically the SGX of Vietnam.

How to Invest in Vietnam Stocks

There are 2 main ways to gain access to Vietnam stocks listed on the HOSE/HSX for Singapore investors:

- Open an account with a Singapore broker that has access to the Vietnam Exchange

- Buy a US listed Vietnam ETF

1. Use a Singapore broker with access to the Vietnam Stock Exchange

If you’re so inclined, you can actually open a brokerage account with a local Vietnamese broker. However you’ll need to sign some forms with them, and head down to the office in Vietnam to get everything sorted out, so it’s not exactly the most convenient thing in the world.

The next best thing, and what I would recommend, is to use an international broker in Singapore that has access to the Vietnam Stock Exchange.

I dug around the brokerage websites, and narrowed it down to a couple of main brokers that offer such services:

| Broker | Rates | Minimum |

| Maybank Kim Eng | 0.35% | USD35 (SGD 47) |

| Phillip Securities (POEMS) | 0.50% | USD50 (VND850,000) |

| UOB Kay Hian | 0.60% whichever is higher | Min US 100 |

| Broker | Rates | Minimum |

| Maybank Kim Eng | 0.35% (promotion till 30 June 2019, usual 1%) | USD35 (SGD 47) (promotion till 30 June 2019, usual USD50) |

| Phillip Securities (POEMS) | 0.50% | USD50 (VND850,000) |

| UOB Kay Hian | 0.60% whichever is higher | Min US 100 |

In terms of absolute fees, Maybank Kim Eng is the cheapest, but the rates are promo rates that are only available until 30 June 2019. There’s no way of knowing for certain if they’ll extend the promotion after that, so if you want to avoid the uncertainty going forward, it might be best to go with POEMs.

Do note that none of the brokers above allow online trading of Vietnam stocks. You’ll need to call in to get a human stock broker to assist in the trade, which is probably why the minimum trading fees are so high.

For the record, I also checked with a bunch of other popular brokers including Saxo Capital Markets, Standard Chartered online trading, DBS Vickers, OCBC Securities, CGS-CIMB Securities and FSMOne, but none of them offer access to Vietnam stocks, so we’re mainly stuck with the above list.

What to buy?

Once you’ve gained access to the Vietnam Stock Exchange (HOSE or HSX), you have 2 main options:

- Buy the VFMVN30 ETF FUND (E1VFVN30:VN) – This ETF is listed on the Vietnam Stock Exchange, and tracks the VN30, which is basically the top 30 companies listed on the Vietnam Stock Exchange. In other words, it’s the STI ETF, for Vietnam.

- Buy individual stocks – Of course, if you’re feeling more adventurous, you could always buy individual stocks directly, and the rules are no different from how you would pick stocks in Singapore.

2. US listed Vietnam ETF

Let’s be realistic. Even using the cheapest broker above at the promotion rates, the minimum transaction fee is still about S$47 per trade to buy a stock on the Vietnam Stock Exchange. And when you’re a retail investor investing S$5000 each time, a S$47 transaction fee works out to a whopping 1% fee per trade, which is money down the drain even before you’ve started.

The other way to invest in Vietnam, is to buy a Vietnam ETF. And there’s really only 1 ETF for this role, the “VanEck Vectors Vietnam ETF (VNM)”, listed on the New York Stock Exchange (NYSE).

The official description of this Vietnam ETF is set out below, but very simply, it invests in public companies (whether listed in Vietnam or internationally) that derive most of their revenue from the Vietnam market.

VanEck Vectors® Vietnam ETF (VNM®) seeks to replicate as closely as possible, before fees and expenses, the price and yield performance of the MVIS® Vietnam Index (MVVNMTR®), which includes securities of publicly traded companies that are incorporated in Vietnam or that are incorporated outside of Vietnam but have at least 50% of their revenues/related assets in Vietnam.

It’s the largest Vietnam ETF (or rather the only acceptable ETF) out there with an NAV of about US$418 million, and liquidity is pretty decent. Expense ratio is 0.68%, which to me is acceptable given the difficulty of accessing Vietnamese stocks anyway.

Which is the best way to invest in Vietnam?

If I were to pick between the two, I would definitely go for the latter approach (the US listed Vietnam ETF – VNM).

If you couple this with a US broker like Saxo, you cut the minimum trading fee down to 4USD versus a ridiculous 47USD if you go with the direct route via the Vietnamese Stock Exchange. This allows you to have much greater flexibility when dollar cost averaging in, or trading in and out of positions. I also like that the VNM ETF includes companies listed outside of Vietnam, and isn’t constrained only by companies listed in Vietnam.

Of course, if you don’t want the broad exposure to Vietnam and you only want to buy 1 or 2 stocks on the HOSE/HSX, you’re pretty much stuck with the first option.

Are Vietnamese stocks a good investment?

The million dollar question though, is whether Vietnamese stocks are even a good investment?

The bull case for Vietnam has been repeated many times, and I’ve extracted a good summary from POEMs below:

Three Drivers of Growth

Population Demographics

Economic growth comes from two sources: Population growth and productivity growth.

Shifting demographics in part drives economic growth. While population growth is falling in many major economies like China and Japan, potentially resulting in a reduction in the labour pool and weakening productivity over the long term, it is forecasted to rise in other parts of the world like Vietnam.

With 45% of the population under 30 years old, Vietnam’s economy has strong reason to be optimistic.6 Booming labour force participation will serve as a catalyst for higher productivity and economic growth.

Low Labour Costs

Vietnam’s low labour costs mean it is able to attract jobs from countries like China, where labour costs have been rising. Vietnam’s minimum wage per month, at US$180, is a fraction of that in other countries within the region like China (US$355) and Indonesia (US$246).7 Due to the low cost of labour, Vietnam has become a big exporter of electrical equipment, electronics, coffee and apparel.

Growing Middle Class and Increasing Consumption

Vietnam’s retail market is the fastest growing in Southeast Asia, driven by rapid urbanization and a growing middle class population. Vietnam has recently surpassed Thailand as the second largest retail market within the region, just behind Indonesia.

The middle class and wealthy segments in Vietnam are poised to grow by 88% between 2010 and 2020. Together with a growing population in urban areas, along with an average age of 30 years, these factors provide powerful demographic tailwinds to support a consumption boom. Indeed, retail sales grew by 10.7% in the 1st half of 2018, with non-discretionary spending growing at a higher rate than discretionary spending; driven primarily by the food and beverage sector. With relatively low GDP per capita compared to neighbouring countries, this trend looks set to continue as GDP catches up to its peers.

In other words, the population growth, the productivity growth, the low labour cost, and the massive growing middle class looks a lot like Shanghai in the early 2000s, and we all know how Shanghai turned out. A lot of people also point towards the US China trade war as a boon for Vietnam, because big MNCs are forced to move manufacturing centers out of China, and the most obvious alternative is Vietnam which already has the existing infrastructure, and offers manpower costs significantly lower than China.

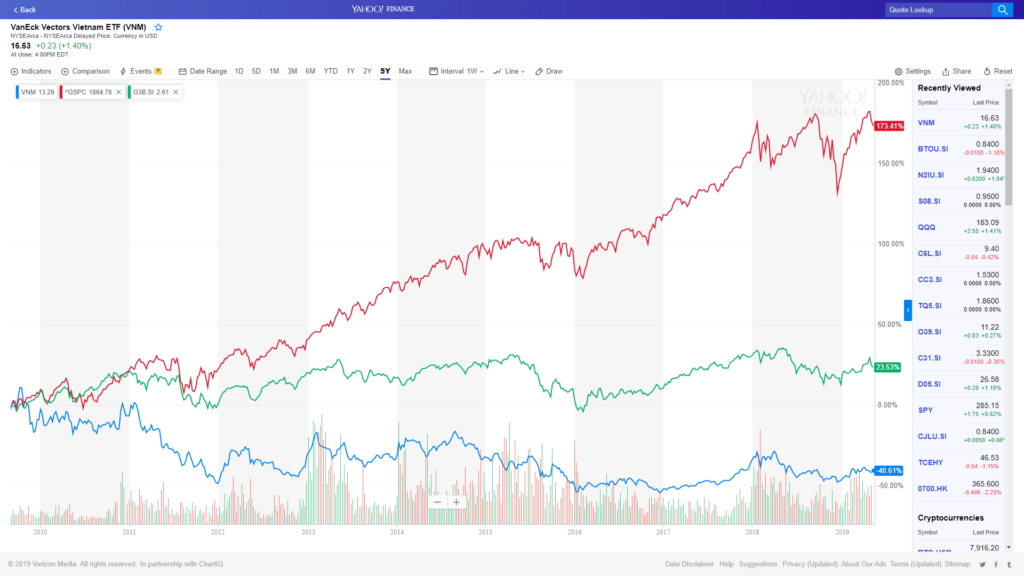

So that’s the bull case. But when we take a look at the 10 year performance of the Vietnam ETF (VNM), the performance is very interesting. In the chart below, blue is the Vietnam ETF (VNM), Green is the STI ETF, and red is the S&P500.

So what explains this massive underperformance of the VNM versus other main indexes? I narrowed it down to a couple of main reasons:

- Market Expectations

- Emerging Market credit cycle

Market expectations

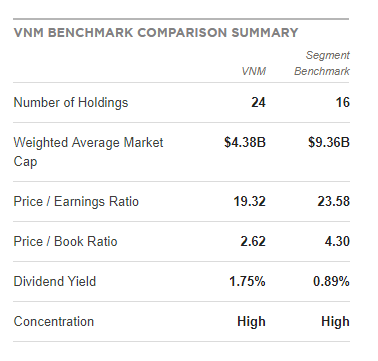

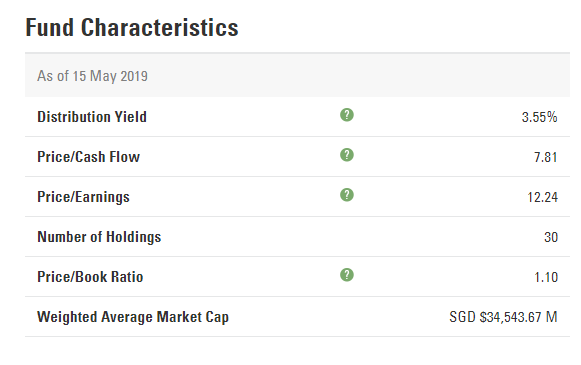

The bull story behind Vietnam is well known by now. Because of that, investors have been pouring money into Vietnam, and the largest companies that comprise the indexes have been bid up to premium valuations. Today, the VNM ETF has an average P/E Ratio of 19.3, a Price/Book Ratio of 2.62 and a dividend yield of 1.75%.

By contrast, the STI ETF trades at a 12.2 times P/E, 1.1 times book value, and a 3.5% dividend yield, which really goes to show how much more expensive Vietnamese stocks are, and how much growth investors are pricing into Vietnam stocks.

If we take a look at the individual stocks in the VNM, this is true as well. For example, Vinamilk, one of the largest dairy companies in Vietnam, trades at a lofty 25 times trailing P/E ratio. Vingroup, a Vietnamese conglomerate focusing on real estate development, retail, and services ranging from healthcare to hospitality, trades at 50 times P/E.

And the price action of stocks ultimately reflect their performance versus market expectations. With expectations for future growth this high, it becomes harder and harder for Vietnamese companies to grow fast enough to keep up with market expectations.

The key question going forward, is whether Vietnamese stocks will continue to perform in line or better than market expectations.

Everyone will have their own take on this, but personally, I’m not bullish. I think that if you take a 10 to 20 year perspective, Vietnam is going to be bigger than where they are today. But how they get there matters as well. The global trade tensions, and the nearing of the end of this longer term debt cycle, may be problematic for emerging market economies like Vietnam over the next few years. With valuations of Vietnamese stocks where they are now, I would be slightly wary of going in too heavily.

Emerging market credit cycle

The exchange rates of the Vietnamese Dong (VND) against the USD are set out below.

The price of the VNM is set out below, split into a number of boom and bust cycles (emphasis mine).

And to me, this really illustrates one of the main risks of investing in an emerging market like Vietnam.

When times are good, like it was in 2011 to 2013, or 2016 to 2017 (or pre-2008), there is a huge inflow of foreign investment into Vietnam. Stocks and real estate prices go up, investors get more and more bullish and flood the market with cash, which further inflates asset prices and the domestic currency, create a boom cycle.

Eventually the market gets overheated and the boom turns to bust, like in 2009, or 2015. The foreign capital floods out of Vietnam, tanking the stock market and real asset prices, and taking the exchange rate with it.

If you’re a short term flipper, all this works great for you. You just wait until the next bust cycle, invest heavily in an index fund, ride the cycle up, and try not to get too greedy and exit before the next bust cycle.

If you’re a longer term investor though, the key question is whether Vietnam can escape this boom bust Emerging Market credit cycle, and transition to a domestic, consumption driven economy much like what China is doing. Making that transition is much easier said than done, with Singapore and South Korea being some of the few success stories in Asia. Even China which is 10 years ahead of Vietnam is facing difficulties in executing this transition properly.

Would I invest in Vietnam?

As I like to say on this site, investing is ultimately about risk-reward. Sure, because Vietnam is an Emerging Market economy, the risks here are big, but so are the potential rewards.

But would I invest in Vietnam Stocks right now? Probably not.

I don’t like how expensive the valuations of Vietnam stocks are, especially given that these are Emerging Market stocks. And unlike Singapore stocks, their dividend rates are also low (around 1.75%), so you don’t even get paid to hold the stocks. Given a choice between the VNM and the STI ETF right now, my money is still on the STI.

I also don’t like the stage of the economic cycle we are at. With the Feds at the end or near the end of their tightening cycle, we look to be very late in the debt cycle. The biggest tail risk to emerging market economies, especially export driven ones like Vietnam is always the global economy and global investor sentiment. If the global economy slows, export growth slows, and investors start pulling cash from Vietnam, things can get really ugly really fast, just like it does in every single credit cycle.

So while I really like the long term bull story for Vietnam, I think the risks outweigh the reward at this point in time. I’m going to stay on the sidelines for now.

What do you think? Share your thoughts in the comments section below! I respond personally to all comments!

Enjoyed this article? Do consider supporting the site as a Patron and receive exclusive content. Big shoutout to all Patrons for their generous support, and for helping to keep this site going!

Like our Facebook Page and join the Facebook Group to continue the discussion! Do also join our private Telegram Group for a friendly chat on any investing related!

why not use IB?

Does IB have Vietnam access? When I checked the website it didn’t include Vietnam specifically.

https://www.interactivebrokers.co.uk/en/index.php?f=37908&p=asia

You need to take into account accounting standard when coming to P/E ratio. Vietnam is currently adopting their own accounting standard (Vietnamese Accounting Standard), which is significantly different from the common IFRS and US GAAP accounting standard.

VAS has different method to record P/L which eventually impact bottom line earnings.

Whether or not VN equities are over-valued or under-valued, my view is that its first need to be standardized into international common reporting standard under IFRS or US GAAP.

2nd, putting aside accounting standard, starting at a lower base would mean that earnings will be easier to double on a relative basis, which will cut down the P/E ratio by half.

I am not here to judge ur decision not to invest at this stage. Merely providing different perspective.

to invest or not to invest boils down to investors information and confidence in that particular market and companies.

That’s an amazing comment, thanks for the share! If I may ask, are you bullish on Vietnamese equities as a broad market going forward? Always love to hear from readers!

Bro, google tooke me to this page, thanks for putting all the information together! Actually I also spent some time to look into the weird performance of VNM over the last decade and all of sudden, after I managed to retrieve the ETF’s annual reports in 2010 and 2011 when the NAV was at all time high, the composites of the index was almost completely different from the current one! Many of the largest component companies in the index right now IPOed long after the bust period and many composites at that time already removed from the index completely, I believe the magnitude of the reshuffle probably explained why the index performed so so from 10 to 19.

Really great comment, thanks for the share!