As you would be aware, I view the impact of Trump’s tariffs to be as large as the impact of COVID itself, and arguably one of the greatest shakeups to the post-World War 2 global world order.

Not so much for the tariffs themselves, but because the thinking behind the tariffs (America shifting from an upholder of global world trade to prioritising America’s own interests first), and the realisation from the rest of the world that America is no longer a reliable partner, will have huge ramifications for the global world order in the years to come.

I came across 2 great articles recently that I thought was well worth the time to discuss in further detail.

The first, was a note from Bridgewater CIOs discussing the big picture impact.

The second, is a more micro level chart deck from Apollo discussing the immediate impact of the tariffs (hint: impact on consumer and business sentiment has definitely been negative).

I figured we’ll discuss the Bridgewater deck today, and the Apollo deck tomorrow.

This is an FH Premium post written in late April.

I am making this available to all readers to keep you updated on my latest thinking given the current market volatility.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

Summary of the Bridgewater Deck

The report from Bridgewater is actually quite succinct and to the point, so I did not see much purpose in summarising it further:

**********************************************

Bridgewater: Connecting the Dots

To state the obvious: we are now facing a radically different economic and market environment that threatens the existing world order and monetary system.

We have been transitioning to this world for several years, but now the shift has sharply accelerated and become chaotic. This new macroeconomic and geopolitical paradigm is turning past tailwinds into headwinds and reshaping global flows of capital. If you were to list the defining characteristics of recent decades and compare them to today, you’d struggle to find much overlap. We have been through many big economic shifts over Bridgewater’s 50-year history, so we don’t speak lightly when we say that this looks like a once-in-a-generation one.

Facing a new reality, everyone must adapt. Those who adapt fast and well will gain at the expense of those who adapt slowly and poorly. Our approach to dealing with new realities has always been to embrace them. This starts with identifying which dynamics will matter the most. We then build a fundamental understanding of those dynamics, mapping the cause-and-effect linkages through which they impact the markets and economic machine, which allows us to reflect them in our investment systems and update our playbook. At the same time, we want to be realistic about what we don’t know and deal with that by designing portfolios that are diversified and resilient.

Today, we see three interrelated dynamics at the core of this new reality:

1. We’re in a new geopolitical and macroeconomic paradigm:

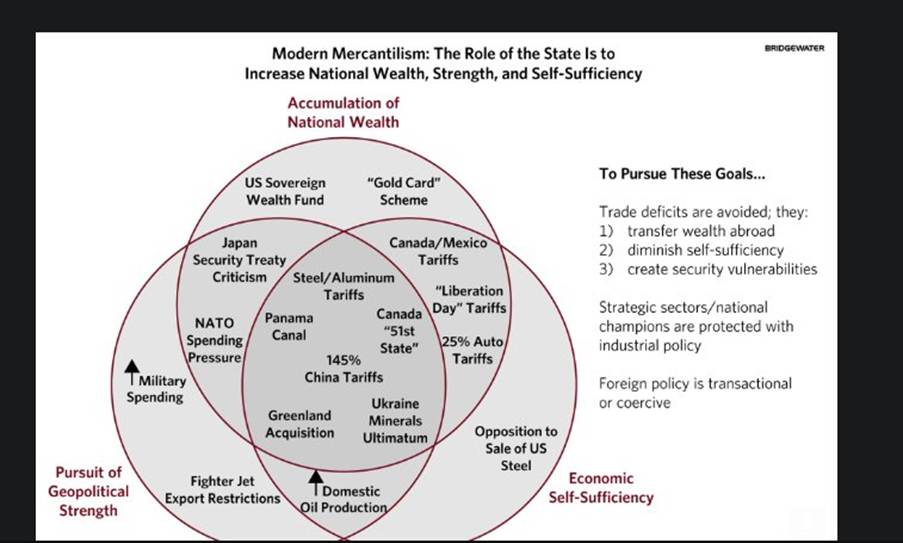

Globalization, rising trade, and capital liberalization was the dominant geopolitical and economic paradigm for decades. That paradigm is over and is being replaced with modern mercantilism. The Trump administration has chaotically accelerated this shift as it seeks to upend global institutions and rebalance trade and security relationships to pursue its “America First” priorities. Now, a global system of interdependency that has been woven together since the dawn of the US-led post-war era is being undone.

In this new mercantilist paradigm, the role of the state is perceived to be to increase national wealth, strength, and self-sufficiency. The state takes a more active role in orchestrating the economy to pursue these goals using trade policy, transactional or even coercive foreign policy, and industrial policy to support companies and sectors it considers strategic to achieving these goals (e.g., domestic capabilities in AI/ML, manufacturing in key areas such as semiconductors, etc.). How these policies play out, and how global policymakers and the private sector respond, will have major implications for markets and economies.

2. This shift presents an urgent threat to markets and investment portfolios:

Today’s mix of global assets reflects the winners from the past paradigm, largely US equities that benefited from rising growth, a proactive Fed, and US outperformance.

This shift has created risks if the future is different from the past. Many portfolios are increasingly vulnerable to:

- Weakness in growth

- Central banks not being able to ease into problems

- Equity underperformance

- US underperformance relative to the rest of the world

The rapid shift to modern mercantilism presents imminent risks across each of these dimensions, which have begun to materialize:

- A policy-induced slowdown, with a rising probability of a recession.

- The Fed is less able to ease proactively into the slowdown as stagflationary risks rise; other central banks will lead the easing cycle.

- US corporates are under threat while strong earnings remain priced in.

- Exceptional risks to US assets, which are dependent on foreign inflows.

Table comparing vulnerabilities:

| Vulnerabilities | Yesterday’s Environment | In The New Mercantilist Paradigm |

| 1. Growth Weakness | Strong US Growth | Policy-Induced Growth Slowdown |

| 2. A Fed that Can’t Ease Into Problems | Flexible, Proactive Fed | Stagflationary Risks, Fading Disinflationary Tailwinds |

| 3. Stock Underperformance | US Corporates Globally Dominant | US Corporates Highly Exposed to RoW (Rest of World), While Continuing Outperformance Priced In |

| 4. US Equity Underperformance vs the World | Global Capital Surplus, Massive US Inflows | Loss of US as Reliable Trade and Security Partner Threatens US Capital Inflows |

3. Simultaneously, we’re in a once-in-a-generation technological disruption:

Every several decades, we experience technological evolutions that impact human productivity in profound ways, leading to structural and societal change; we are amid one of those now. AI/ML can now significantly outperform human experts in a range of fields. The economic, market, and societal consequences have only begun and will exponentially grow. Interrelations with geopolitics, policymaking, and portfolios will be complex and impactful.

For markets, it is too soon to say who the winners will be and if they will hold onto their winnings. Being on the leading edge of technology does not necessarily mean leading in deployment and monetization. It is not yet clear where in the AI value chain the profits will accrue (e.g., will the models become commoditized?).

The AI story today is analogous to the internet story of the late 1990s. We believe we are in the early stages of this story, akin to around 1998. Although technological progress fulfilled many promises of the dot-com era, US equities underperformed for the 15 years after 1998. Bets on market-leading internet names in the dot-com era broadly underperformed the market (Microsoft was a noticeable exception). Many ultimate winners, such as Alphabet and Meta, were small or non-existent at that time.

Follow Financial Horse to avoid missing any post!

My views?

Broadly, Bridgewater’s views can be split into 3 points:

1. New Geopolitical and Macroeconomic Paradigm

Globalization and liberalization are giving way to modern mercantilism, where nations prioritize national wealth, strength, and self-sufficiency through active state intervention. Global interdependency is breaking down, reshaping trade, capital flows, and markets.

2. Threats to Markets and Investment Portfolios

Portfolios built for the old paradigm — especially those overweight US equities — now face heightened risks: slower growth, limited central bank support, US corporate vulnerability, and declining US outperformance. Bridgewater sees growing stress across all these dimensions.

3. Once-in-a-Generation Technological Disruption

AI/ML is triggering a major technological shift, but the winners are not yet clear. Early dynamics mirror the 1990s internet era, where initial leaders often underperformed and true winners emerged much later. Navigating this disruption requires caution and diversification.

My views on each:

1. New Geopolitical and Macroeconomic Paradigm

I’ve been saying this in different words, but Bridgewater probably puts it more succinctly than me.

Long story short – I agree.

Exactly as I said with COVID – I do not think we are going back into a pre-tariffs world.

Sure the US may cut deals with China and EU, but we are never going back to the pre-liberation day position where there is fully unfettered free trade.

For 2 simple reasons.

First – it’s fairly clear that Trump’s administration is no longer with the US led post-WWII world order, where the US guarantees free trade, free security, freedom of passage, and free access to US markets, simply out of the good of their heart.

In this new world, the US will adopt an America first policy. If you want to have access to the US markets, or want the US military to defend you, you need to pay the price.

Secondly – Even if Trump completely rolls back all of the Liberation Day tariffs (which is exceedingly unlikely). You cannot put the genie back in the bottle, in the sense that the whole world has now woken up to the fact that America is now an unreliable partner.

And once you see this, you cannot unsee this.

The soaring price of gold to me, is one of the results of this realization from global investors – as they move out of USD into the safety of gold.

2. Threats to Markets and Investment Portfolios

For this point, I am less inclined to agree with the conclusion from Bridgewater that US assets will underperform.

I think that ultimately it is a case of the cleanest dirty shirt.

Sure the US may not be the by far the premier investment destination anymore.

But it still retains many qualities such as very deep and liquid capital markets, some of the world’s most competitive companies, and continues to lead the world in technological innovation.

That said, it would be foolish to expect that the past decade of US stock performance will definitely continue going forward.

It would be wise to at least consider the possibility that US stock outperformance is no longer a sure thing going forward, and think about how your portfolio would perform in such a scenario.

Personally I diversify via China stocks, Singapore stocks and Bitcoin/gold, which to me can deliver independent and uncorrelated returns (to the extent you can get in this hyperconnected world) in the event that US underperforms.

3. Once-in-a-Generation Technological Disruption

Here I agree with Bridgewater.

Although to be fair, Bridgewater isn’t saying all that much that is really actionable.

The more I use and interact with AI, the more I realise this is without a doubt a transformational technology whose impact in time to come will be as profound as the internet itself.

But go back to 2000 and try to pick a basket of stocks that would make you money – and boy that is a really hard challenge.

Most of the really big winners – FAANG + Bytedance, were not even public companies in 2000.

And many of those that were public like Microsoft / Amazon, they still went on to suffer horrendous losses before the eventual recovery, and it was never all that clear that they would be the obvious winners they are today.

This one is similar to China in some ways.

I am bullish on China, and I believe that China will grow to become one of the world’s dominant economies in the 21st century.

Likewise I am bullish on AI, and I believe AI will transform the world.

But as an investor – how to translate that belief into actionable returns, boy that is much harder.

This is an FH Premium post written in late April.

I am making this available to all readers to keep you updated on my latest thinking given the current market volatility.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

With persistent extended high interest rates starting from the biden administration, and present Trumps import tarriffs the market is already pricing in a global slowdown and shedding the most affected Energy sector due to low volume shipping, transports and distrbution and the “perceived” move to cleaner energy solutions in this mid decade stage.

The high yield aversion on markets started in 2022 post covid with the theme to battle high inflation, making it harder to borrow dampening demand and business sentiment every sectors mostly started taking a hit, ok between tangibles and intangibles , consumer discretionary and defensive, with the exeception of banking, insurance making a bigger cut out of the widened borrowing and savings profit margins everything points to humans spirit of moving forward in adverse conditions for example real estate prices,borrowing costs, loan volume and duration, rental yields it seems that no one priced in a possible recession on banking stocks and between tangibles and intangibles namely healthcare and big tech, i am saying its a long way ahead of continual mis-adminstration

Recent data does suggest the economy is slowing. The question is whether Trump will deliver on the stimulus to offset the slowing growth (eg. by appointing a dovish fed chair who will cut rates, or by delivering on fiscal stimulus – tax cuts etc). At these valuations, market is pricing in a yes.