As shared in yesterday’s FH Stock Watch (download here), I see value lying in 3 areas of the market at the moment:

- Oil & Gas

- Cyclicals (eg. Banks, industrials, possibly semiconductors)

- China Banks

As promised, let’s do a deeper dive into all 3 of them.

1. China Banks

Let’s start with the most controversial one – China banks.

The Big 4 China banks – ICBC, CCB, BOC, ABC, now trade at ~8.5% trailing dividend yields.

The chart of ICBC is set out below, but frankly you can pull up any of the other 3 China banks and they look the same.

These are very, very long term support levels – going back to 2012.

If we lose these support levels it’s probably lights out.

Are China banks a falling knife?

The arguments against buying China banks have been covered exhaustively in my older articles.

To recap, they are:

- Possibility of China going down a more insular path cut off from the world (with Xi as a tyrant)

- Geopolitical risk premium from a potential cold war with the US this decade

- Slowing economy due to COVID zero and rising inflation

- Real estate bad debt issue is playing out like a slow motion train wreck (China banks have a lot of real estate exposure)

- China banks being called upon to make “Policy” Loans to bail out the economy

For the record, I agree with all the points above, I think they are perfectly valid.

Are China banks a good buy?

On the flip side though, you do get an 8.5% dividend at current prices.

The arguments against China banks are not new, and have been peddled since the start of this century.

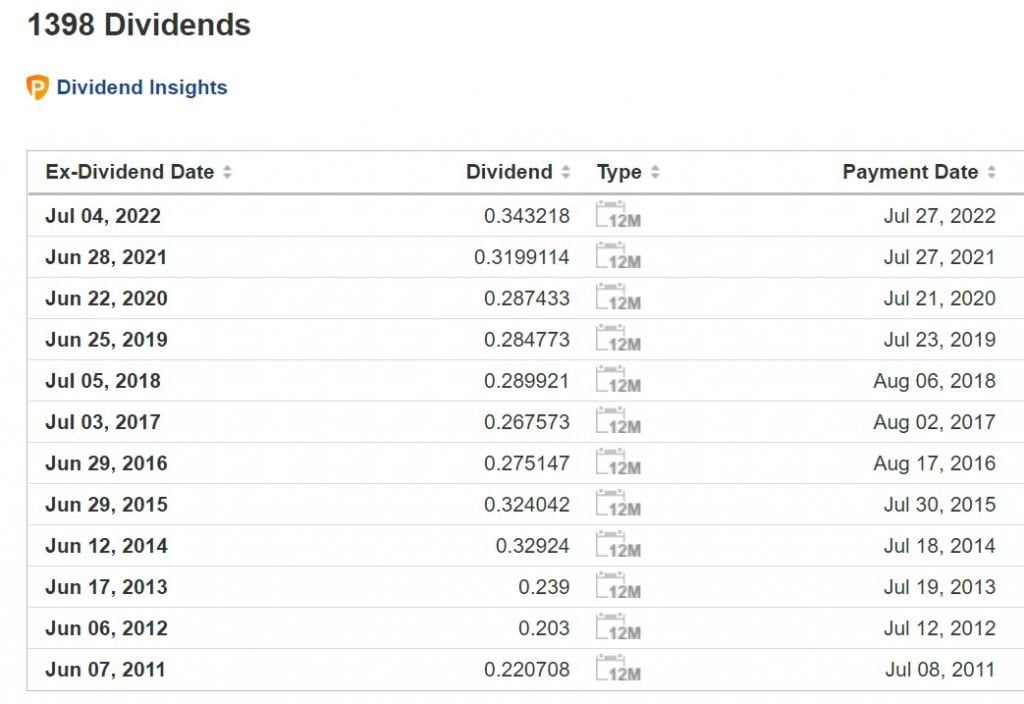

Yet here’s the 10 year dividend history of ICBC – up every year.

Full disclosure that I decided to take the plunge and added to my ICBC position today.

It’s a small position that I added, and I fully expect to lose some fingers catching a falling knife.

But the way I see it, Xi needs a strong economy heading into year-end (Party Congress in Oct).

Xi is not going to allow the China banking sector to fail, not when he is so close to his “re-election” for life.

Say what you want about China, but they are an authoritarian, top down political system, with the majority of their debt denominated in RMB. This means they have the policy tools to do what it takes to fight the debt crisis.

Will it come at the cost of inflation and longer term competitiveness? Possibly.

But I find it hard to see Xi sitting by and allowing the financial situation blow out of control right before his Party Congress.

Just this morning, it was announced that China banks are being urged to support the real estate sector to tackle the mortgage crisis. And to allow a “mortgage” grace period.

Which is broadly in line with my thesis.

So if you think China will backstop their banking system, you’re getting a 8.5% dividend at current prices.

But like I said, I do not deny this is a risky trade, and I would be careful to position size properly.

Any money going into the China banks should be prepared for significant to complete capital loss if things head south.

2. Oil & Gas

Funny how quickly the tables turn.

3 months ago Oil & Gas was the hottest sector around.

And suddenly nobody wants to touch Oil & Gas because of a potential recession.

The argument against Oil & Gas of course, is that in the short term, the Feds are going to hike us into a recession, which will crush demand, and tank oil prices.

And Biden speaking to the Saudis to get them to pump more isn’t helping sentiment.

The argument in favour of Oil & Gas, is that in the mid term, there just isn’t enough supply to keep up with demand. Once demand recovers, expect oil to make new highs.

And you can’t rule out a tail risk event like Russian oil supply going offline.

Oil – Many shades of Grey

So may people think of oil as a binary outcome – either it goes up, or it goes down.

But in reality, you need to ask yourself what is the probability of oil going up, vs the probability of oil going down.

And how much do you make in each scenario.

And what is your timeframe.

To illustrate – let’s say you think there is a 20% chance oil goes to $150 by year end. Higher oil prices mean sticky inflation means a lower chance of a Fed pivot. That means higher interest rates for longer, which will crush stocks. How much does your portfolio suffer in that scenario?

On the flipside, if oil goes to $75 by year end. That means a more dovish Fed, which means a huge rally for risk assets. How much does your portfolio go up in that scenario, vs how much do you lose on your oil stocks?

My personal view on Oil?

My personal view on oil is to not try to get cute with predicting oil’s short term movements.

A tail risk event like a Ukraine ceasefire can drive big movements in the price of oil, and are incredibly hard to predict accurately.

But mid term, looking 2 years out, I still think supply will not be able to keep up with demand.

So any short term weakness could be interesting for me to add to mid term positions.

And not forgetting the potential hedging benefits of oil.

If there is a 5% chance of $200 oil by year end, that’s a risk of a big crash in the rest of your portfolio, that even treasuries will not hedge (because of rising rates).

Oil could be used to hedge such an event.

3. Cyclicals – Banks, Industrials, Possibly Semiconductors

In early Jan I wrote an article about selling DBS because of a coming recession.

Since then – DBS is down 20%.

And funnily enough, at current prices and with the current macro outlook, I’m starting to flip dovish on the banks again.

The reason why, is that I think the market is mispricing recession risk.

As shared in previous macro articles, I think this economy may be able to withstand higher interest rates for longer than investors are expecting, simply because of (1) tight labour market, and (2) strong household balance sheets.

Which means there could be a bit more to go, before the economy tips into a recession.

With rising interest rates, that could lead to windfall profits for the banks in the short term.

The analogy is broadly the same with industrials and semiconductors.

A recession might be slightly further off than investors are expecting, while current prices are already pricing in an immediate recession.

Remember, in investing it’s always about what is priced in vs what actually happens. So if we don’t get a big recession so quick, there could be upside here.

Some names like Citibank are trading at 0.4x book value, which is pretty ridiculous when you think about it.

That said, this is definitely not a trade without risk, because you are literally buying cyclicals into a global recession.

Long duration assets – Tech, Treasuries, REITs

For the last sector, I wanted to talk about long duration assets.

These are assets that are very vulnerable to changes in long term interest rates – mainly tech, REITs and Treasuries (or fixed income).

My simple view, is that because the economy may prove more resilient than expected, the Feds may have to hike hiker and longer than the market is pricing in.

Am starting to think there is a possibility that the terminal rate of interest rates could be 4% (possibly higher).

Which would mean it is still too early to buy into long duration assets.

What about rate cuts?

That being said – the market is starting to price in the possibility of Fed rate cuts in early Jan.

A lot of investors out there are starting to believe we are very close to a Fed pivot.

That’s driving the current rally in long duration assets, which may have legs.

If indeed you believe this view, then you’ll probably want to buy now or over the next few months, ahead of a early 2023 Fed rate cut.

Personally I think it’s too early to make this trade, but I do not deny that I could be wrong on this.

As always – love to hear what you think!