Okay I know there are a lot of questions about the market price action, recession risk, and what this means for portfolio positioning.

I shared some quick thoughts over the weekend, but I wanted to elaborate on them in today’s article.

For ease of reading, I am going to split this article up into a series of FAQs.

If there are any queries, please leave a comment below and we can discuss further.

This is a premium article written exclusively for FH Premium subscribers.

I am making it public for all readers given the big moves in markets – in the hopes that it helps you understand what is going on.

Do note that this article was written on 5 Aug and will not be updated going forward.

My latest views on markets, and the changes I make to my portfolio – are shared on FH Premium. Do sign up for the latest updates as this plays out.

What were the key events last week that led to the market crash?

Broadly there were 3 key events last week that drove the market sell-off:

- Bank of Japan (BOJ) raises interest rates

- US unemployment rises

- Other data – Corporate earnings disappoint, Chicago PMI drops further

Bank of Japan (BOJ) raises interest rates – at a time when the rest of the world is cutting

The BOJ shocked everyone last week with 3 key moves:

- Raised interest rates to 0.25%

- Signalled the possibility of further rate hikes to come (beyond 0.5%)

- Tapered Quantitative Easing (monthly purchases of Japanese government bonds (JGBs) will be reduced to 3 trillion yen ($19.9 billion) by the first quarter of 2026 compared with the current pace of 6 trillion yen).

More colour from the Nikkei below:

“The policy rate is still very low even after a hike to 0.25%,” BOJ Gov. Kazuo Ueda said at a news conference. “It is still negative after inflation is taken into consideration. We do not view this as a strong brake on the economy.”

Ueda did not shy away from the possibility of further rate hikes. “I do not necessarily view 0.5% as a barrier.” Ueda did not rule out another rate hike by the end of the year, saying, “We will move on to the next step” if there is more data confirming the inflationary trend.

Only 26% of market players expected a rate rise, according to a survey of 181 bond investors conducted by Nikkei affiliate QUICK on July 23-25. Most investors expected a rate increase to take place either in September or October.

“The BOJ appeared to have kept its intentions under wraps to avoid raising expectations for policy tightening,” said Tomoaki Shishido, rates strategist at Nomura. He believes that the rate hike was aimed, at least in part, at supporting Japan’s embattled currency. “The idea of a rate hike may have been in the works since the suspected currency market interventions on July 11-12,” he said.

Why did BOJ surprise markets with a rate hike?

Few investors expected the rate hike from the Bank of Japan last week.

Market expectation was for the rate hike to take place in Sept or Oct.

In fact it appears that the BOJ intentionally engineered it this way, to shock markets.

The reason why central banks sometimes want to shock markets is for maximum impact.

The BOJ has been under pressure of late with a rapidly depreciating Yen, and by coming up with an unexpected rate hike they would have shocked the markets out of its complacency – strengthening the Yen.

And to that end – the BOJ actually succeeded in their goal.

Yen was trading as high as 162 a few weeks ago.

After the rate hike, Yen has strengthened to as low as 142, wiping out all of the 2024 move.

Why did the Yen move trigger so much havoc across markets?

The Yen is a major funding currency for carry trades (for speculators who borrow in Yen and buy USD assets).

So when the Yen strengthens against the USD, this leads to losses for speculators who borrowed in Yen to buy USD assets (as the USD assets are worth less in Yen terms).

This coupled with the selloff in US stocks the past few weeks, and the speed and magnitude of the move – led to a lot of pain for such carry traders.

So by itself, a strengthening in the Yen would typically lead to an unwind in risk positions across the board, and been negative for risk markets.

The problem was that the BOJ’s move came around the same time as:

- US jobs report came in weak

- US corporate earnings started to disappoint

- US companies (and data) started warning of weakening consumer sentiment

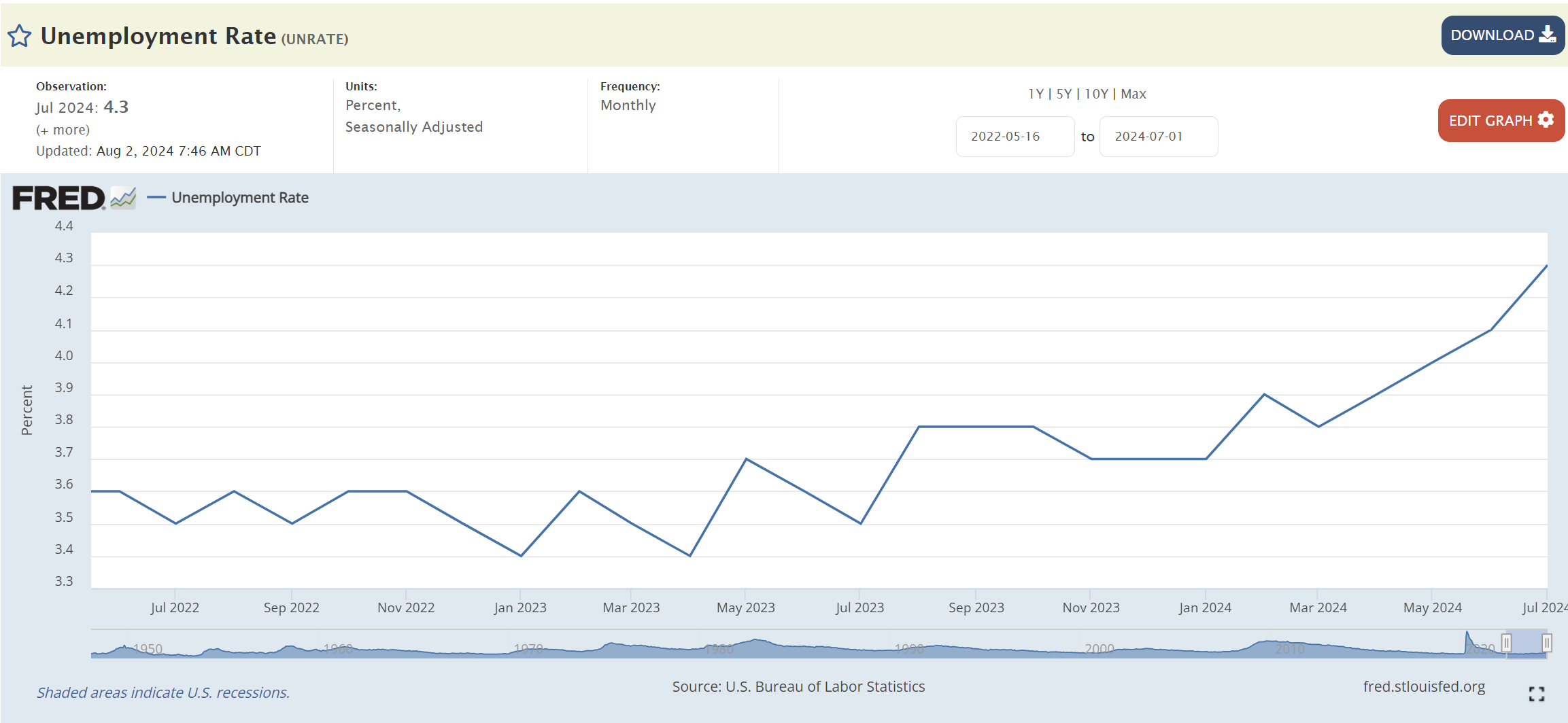

What happened with the US jobs report?

I extracted the Bloomberg summary below.

- Payrolls increased by 114,000, less than the 175,000 median forecast and undershooting all but one of 74 forecasts in Bloomberg’s survey. That weaker reading also came after a 29,000 cumulative downward revision to payroll gains for the previous two months. Average hourly earnings rose 0.2% on a monthly basis, also less than forecast, and on an annual basis increased by 3.6% — the least since May 2021.

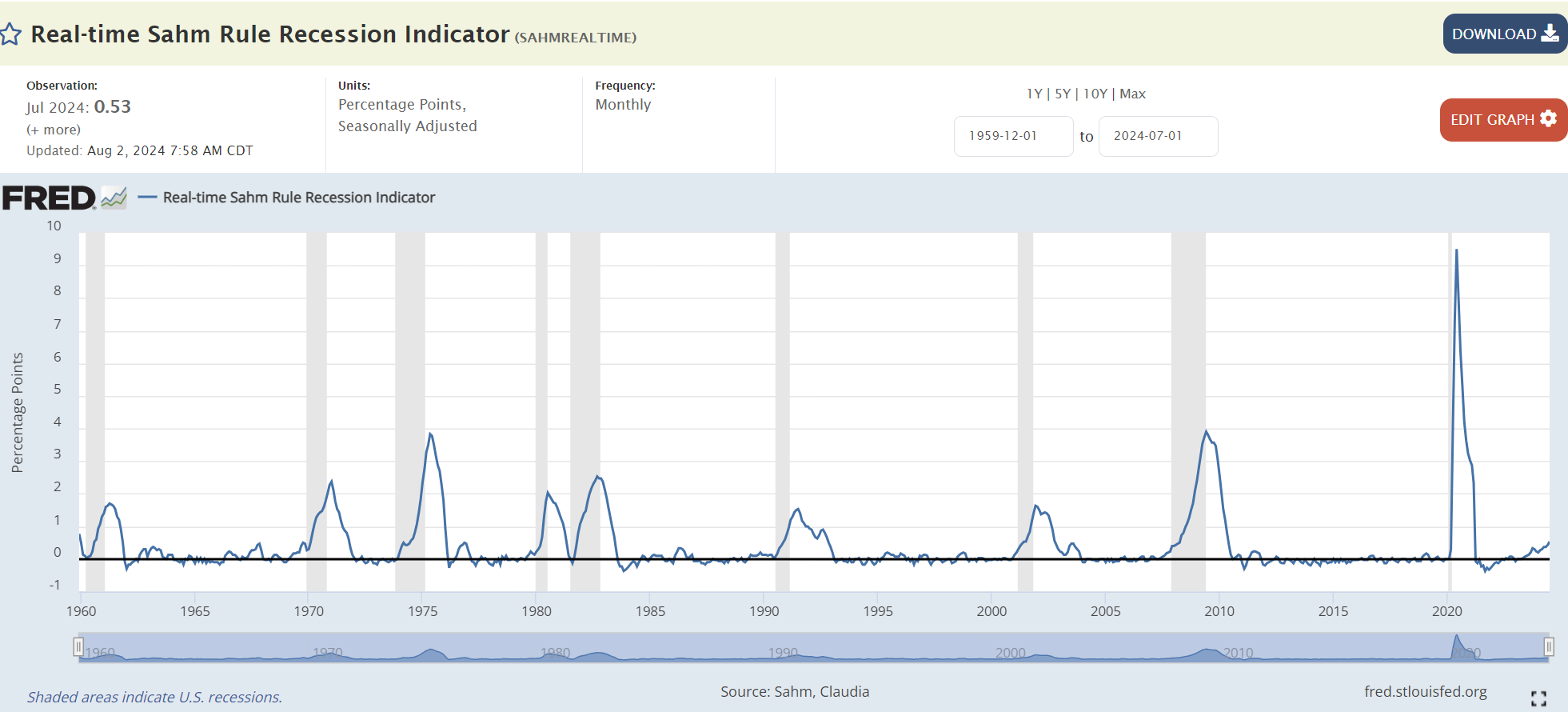

- The unemployment rate unexpectedly climbed to 4.3% in July, exceeding all 69 estimates in the Bloomberg survey. The 0.2 percentage point increase on the month means that the so-called Sahm Rule has been triggered. Coined by former Federal Reserve economist Claudia Sahm, it says that when the average jobless rate over three months is 0.5 percentage point above the 12-month low, a recession is coming. Sahm said on Bloomberg Radio Friday that “we’re not headed in a good direction.”

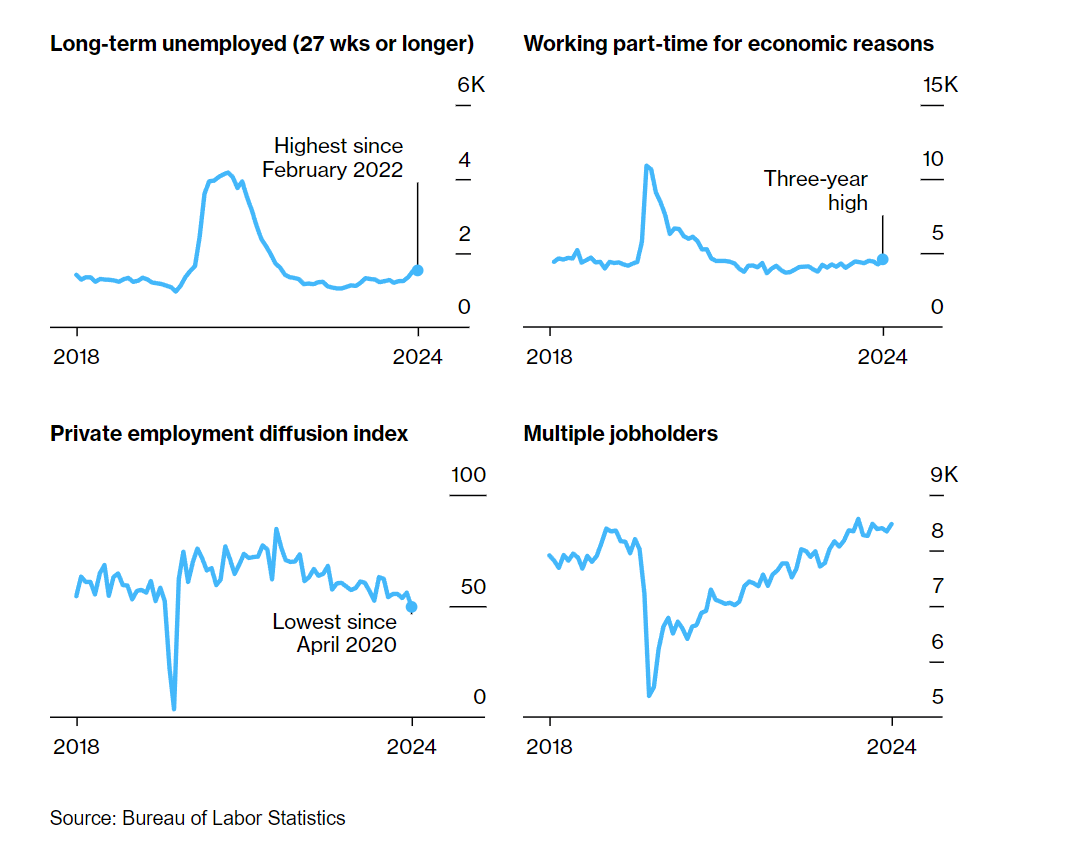

- Private education and health contributed about half of the July payroll gain, with leisure and hospitality and government also adding jobs. Overall, private sector payrolls recorded their second-weakest increase since 2020.

To sum up – the jobs report came in weaker than all estimates.

Showing a continued weakening in the US jobs market – unemployment up to 4.3%.

While under the surface, the jobs data continues to weaken.

The Sahm rule also triggered on Friday (the Sahm Recession Indicator signals the start of a recession when the three-month moving average of the national unemployment rate (U3) rises by 0.50 percentage points or more relative to its low during the previous 12 months).

The Sahm rule has a 100% hit rate over the past 40 years, and did not trigger in other soft landings like the 1995 rate hike cycle.

There are many who argue the Sahm rule is no longer valid in this post-COVID world due to COVID disruptions.

While this is definitely possible (we won’t know for certain until later), whatever the case this shows continued weakening in the US jobs markets and not a good sign.

Other data – US corporate earnings started to disappoint, US companies (and data) started warning of weakening consumer sentiment

At the same time, the Chicago PMI fell 2.1 points to 45.3 in July, below expectations of 47.4.

Big tech earnings last week were also unspectacular, leading to concerns about a weakening corporate earnings.

While companies like Mcdonalds and Diageo warned of weakening consumer sentiment.

So by itself the BOJ rate hike may not have triggered such a big move.

But it came in a week when a lot of data suddenly came in and pointed towards underlying weakness, all while market pricing has been weak since mid July.

This amplified the move and led to forced selling, which is where we are today.

What was the market reaction for stocks?

Taken together – this triggered a huge risk off across markets.

Here’s the Nikkei, down 12% today alone, back to late 2023 levels:

Closer to home – DBS is down almost 7% today, back to April 2024 prices:

While the S&P500 is now down more than 5% from highs (this is as of Friday).

While the NASDAQ is down 10% from highs (this is as of Friday).

What is happening in interest rates?

There are some pretty unbelievable movements in interest rates, as investors price in:

- Rapid rate cuts from the Fed to respond to weakening economic growth and market price action

- Flight to safety for bonds

The Singapore 10 year yield has plunged to 2.65%, the lows we saw in Jan 2024.

Note that much of this move took place over the past few days – the 10 year was at 3.0% as recently as last Wed.

US 2 year yields have plunged to 3.7%.

Given that the Fed Funds rate sits at 5.5%, the market is pricing in almost 2% in rate cuts to come.

While the US 10 year has broken below the 3.8% support from early 2024.

Again, much of the move coming since the BOJ rate hike.

What happens next? (short term)

We’ve been talking about this for a while, but market positioning has been very one-sided for a while now.

Complacency was high across the board, and many investors were long the same stocks.

When positioning gets this one-sided, a sell-off was bound to happen at some point, although this sell-off was magnified by a confluence of factors as we discussed above.

The speed of the sell-off has been very sharp though, and when the market has a big move like that it can typically lead to forced selling (from margin calls or programmatic risk reduction), which then further exacerbates the move.

So short term, it would make sense to let the move play itself out, until such time as (a) the move exhausts itself, or (b) policy makers step in to support markets (eg. An announcement by the BOJ or Feds might do the trick).

I suppose this is self-explanatory, but this is a big reminder of why you do not want to use leverage in times like that.

As long as you are holding cash positions you can afford to wait and let the market move play out without fear of margin call, whereas if you’re in leverage you could get forced liquidated.

What happens next? (mid term)

That’s the short term though.

The mid term goes back to the fundamentals.

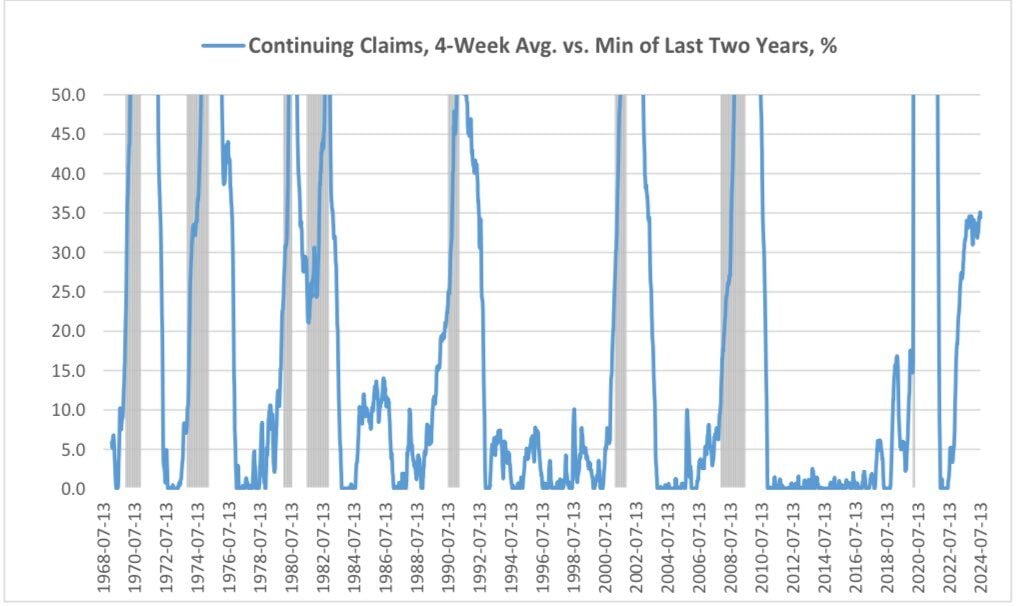

The key question being the economy – and whether we see a recession or not?

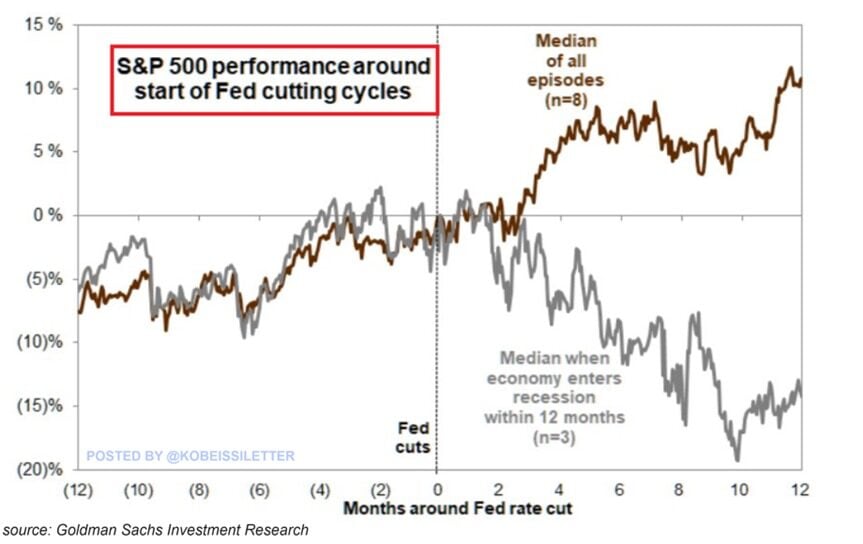

The chart below sums up the 2 possibilities.

If we don’t get a recession, Fed cuts are a buying opportunity.

If we get a recession, Fed cuts are a selling opportunity.

So the million dollar question for the mid term – will we see a US recession?

You can now follow Financial Horse on Google Chrome to avoid missing any posts!

Just:

- Click the 3 dots on the top right of Google Chrome

- Click Follow!

- And Financial Horse posts will now appear on your home page, under Following:

You can also follow Financial Horse on:

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

Is a recession a done deal?

We’re at a potential turning point in the cycle, where the macro data may come in a bit mixed (some data may show strength, some may show weakness, this is what happens at turning points).

The other complexity this cycle is that the impact from COVID (while fading), continues to distort the data.

So over the next few months you may see the data come in mixed, with possible improvement in economic data.

But let’s take a step back and stay big picture for now.

US unemployment has increased a full percentage point from cycle lows (to 4.3%):

While many different models and business surveys are showing a weakening US economy and elevated recession odds.

All while the Feds are poised to start cutting interest rates (historically the recession only hits after Feds start to cut).

So no doubt the US economy is weakening.

But whether the slowdown weakens further into a recession or not will depend very much on how policy makers react in the months ahead, in particular:

- How quick the Feds cut interest rates

- Who wins the elections in Nov, and what steps does the govt take to counter the economic slowdown

Some may argue recession is a done deal, some will say aggressive Fed cuts + govt spending will turn things around.

That call is where the money will be made.

My personal views? Will we see a US recession?

I would not say that a recession is a done deal at this point as the reaction from the policy makers will be crucial to determine the final outcome.

How policy makers respond to the current bout of economic slowdown / rise in unemployment is absolutely crucial.

It is very easy for Powell to talk tough on inflation when the US jobs market was humming along.

Now that the US jobs market is starting to weaken, this is where we get to see what he’s made of.

Does he stick to his guns to only cut interest rates in September.

Or does he step in with an emergency rate cut to bail out markets.

The days ahead will be crucial to watch.

If the past 18 months were any indication, then it is likely that Powell/Yellen will not sit by and watch if the market crash continues to play out.

If we get a recession, will it be a mild one or a deep one?

I received this question from a FH Premium subscriber:

Hi FH,

Thank you for the quick thoughts.

Reports elsewhere continue to suggest that US economic fundamentals remain robust.

If recession should occur, do you foresee a mild one given the other factors listed above in your article?

The complexity is that some of these sell-offs are self-fulfilling.

In China, much of the household balance sheet is in real estate, so a real estate slowdown was devastating for consumer sentiment (if 50% of your wealth is in your home, and your home price falls 20%, you’d be spending a lot less).

The same logic holds in the US – only that much of the US household balance sheet is held in stocks.

So a stock market sell-off could damage consumer sentiment, leading to reduced spending, leading to lower corporate earnings, leading to layoffs, and so on,

So the complexity is that the outcome is also dependant on what happens to stocks.

Whereas if Powell comes out and does a 50 bps rate cut tomorrow, and stocks recover to all time highs, that could boost consumer sentiment and really change the outcome.

So while I don’t think the recession is a done deal.

Reaction from policy makers here is crucial.

There is no doubt that the US economy is weakening, and that if not properly handled there is a risk that the current slowdown would evolve into a broader recession.

Which sectors stand to benefit if this move continues to play out?

Friday’s price action offers some clues on what sectors might benefit.

The biggest relative winners on Friday were:

- Consumer Staples

- Utilities

- Real Estate

- Health Care

While the biggest losers were:

- Consumer Discretionary

- Tech

- Energy

- Banks

That seems about right to me.

You know I hate to say it, but if the market pricing is right on the rapid interest rate cuts to come.

Real estate / REITs may actually be a potential beneficiary.

Commercial Real estate valuations are generally quite cheap across the board as investors have been pricing in higher interest rates.

If interest rates are going to come down sharply, that could really boost real estate valuations due to lower cap rates.

All while lower interest expenses, and lower yields on cash boost the attractiveness of real estate / REIT plays.

My full watchlist on REITs I would be keen to pick up are shared on FH Premium.

How would I position my investment portfolio?

FH Premium subscribers will know I have been running healthy cash levels for a while now, which gives me plenty of dry powder to buy into declines.

That said, the market moves this morning look like forced selling – Nikkei down 12% is not an orderly move and is bound to have ripple effects.

When the market is in forced liquidation made, it’s probably best to let it play out until (a) the selling exhaust itself out, or (b) policy makers step in with some kind of support.

Frankly don’t see a need to step in and be a hero here, as I don’t see a need to time the bottom perfectly.

If and when things stabilise though, we could see a pretty big rally from very oversold conditions.

But the mid term question of whether this is a buying opportunity goes back to the chart below – do we have a US recession or not.

And really, I think the jury is still out on that one, until we see how policy makers respond.

This is a premium article written exclusively for FH Premium subscribers.

I am making it public for all readers given the big moves in markets – in the hopes that it helps you understand what is going on.

Do note that this article was written on 5 Aug and will not be updated going forward.

My latest views on markets, and the changes I make to my portfolio – are shared on FH Premium. Do sign up for the latest updates as this plays out.