Weaker inflation numbers and recent comments from Jerome Powell have led to the market pricing in a lot of interest rate cuts over the next 12 months.

Because of that, the latest 6-month T-Bills closed at 3.64% yield.

This means that if the upcoming 1-year T-Bills has an interest rate of around 3.6%ish (where they are trading on the open market now).

They could be a pretty good buy actually – once you factor in the interest rate cuts in 2024/2025.

The next 1-year T-Bills auction is coming up on 25 July.

3 key questions I wanted to discuss:

- What is the estimated yield on the 1-year T-Bills on 25 July?

- Which is a better buy – the 6-month or 1-year T-Bills? Compared vs Fixed Deposits or Money Market Funds?

- What about for CPF-OA buyers?

And I will also take the chance to share whether I will be applying for the the 1-year T-Bills.

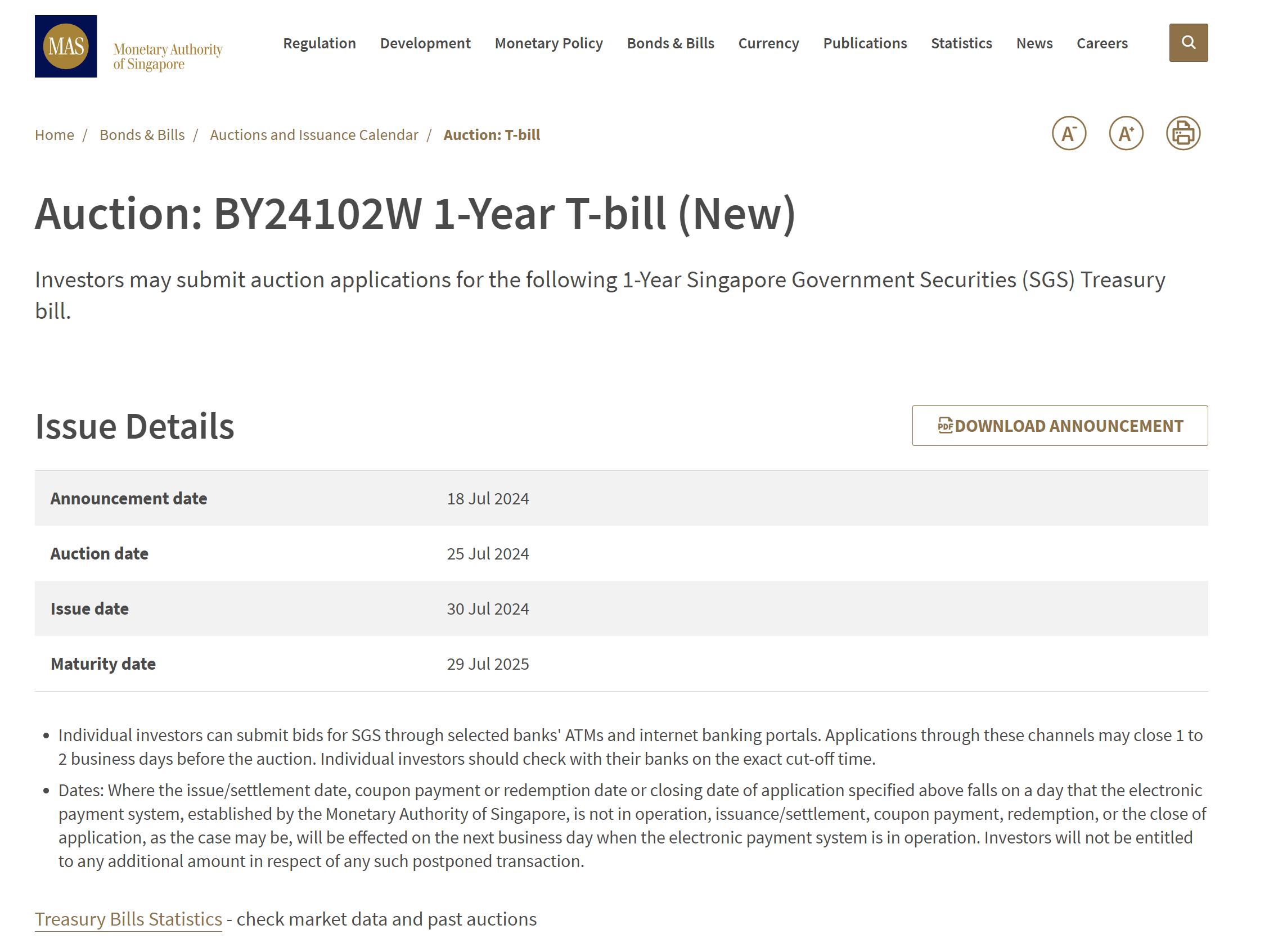

Next 1-year T-Bills auction is on 25 July (Thursday) – (BY24102W 1-Year T-bill)

The next 1-year T-Bills auction is on 25 July (Thursday).

Deadline to apply is therefore:

- 9pm on 24 July (Wed) for cash applications (and CPF-OA applications via DBS or OCBC internet banking)

- 9pm on 23 July (Tues) for UOB CPF-OA applications

Note the next one is 17 October 2024, a whole 3 months away.

So if you want the 1-year T-Bills, don’t miss your chance.

What is the estimated yield on the 1-year T-Bills on 25 July? (BY24102W 1-Year T-bill)

1-year T-Bills trade at 3.57% on the open market

1-year T-Bills are trading at 3.57% on the open market.

But… T-Bill trading liquidity is incredibly thin, so this market pricing is not indicative

That being said the trading liquidity on the T-Bills is so thin that actually the market pricing is not indicative.

Market pricing actually takes its cue from the T-Bills auction, and not the other way round.

So I would caution against placing too much reliance on market pricing on T-Bills.

Market is pricing in a lot of interest rate cuts in the next 12 months

Note that because recent US inflation data has cooled.

And recent comments from Jerome Powell suggests he is likely to start cutting rates in Sep 2024.

The market has started to price in a lot of interest rate cuts over the next 12 months – anywhere from 5 to 6 interest rate cuts.

For 1-year T-Bills, this is not a good sign.

T-Bills Supply is flat at $5.1 billion (exact same amount as the April 2024 auction)

This auction sees $5.1 billion worth of T-Bills on offer, exactly the same as the previous auction.

Demand for 1-year T-Bills tends to be very high – so cut-off yields may come in below market yields

Demand for 1-year T-Bills typically tends to be very high, given that there are only 4 such auctions each year.

1-year T-Bills are particularly attractive for CPF-OA buyers, as you minimise the lost interest when you roll over the 6-month T-Bills.

Because of this most of the previous 1-year T-Bills auctions have cut-off yields that come in below market yields.

For reference:

- In the Jan 2024 T-Bills auction – market yields were 3.75%, while the final cut-off yield was 3.45% – a whole 0.3% lower than the market yield.

- But in the April 2024 auction – market yields were 3.60%, final cut-off yields was very close at 3.58%.

Demand for 6-month T-Bills is at record highs, and yields are on a clear downtrend

Note that demand for the 6-month T-Bills are close to record highs:

While yields are on a clear downtrend the past 4 auctions – dropping to 3.64% at the most recent auction.

Estimated yield of 3.30% – 3.60% on the 6-month T-Bills auction? (BY24102W 1-Year T-bill)

Let’s put it altogether.

Market yields on the 1-year T-Bills are 3.57%.

However the market is pricing in a lot of rate cuts over the next 12 months, so if rates stay at 3.57% they would be a very good buy compared to the 6-month T-Bills (which closed at 3.64%)

Because of that I do anticipate a drop in the 1-year T-Bills yields.

Gun to my head – I think the market yield of 3.57% is likely to be the upper end of the range.

I’m going to go with a conservative 3.30% – 3.60% anticipated yield for the 1-year T-Bills.

Which is a better buy – the 6-month or 1-year T-Bills?

The way I see it, it really depends on the yields you get on the 1-year T-Bills.

Let’s say worst case the 1-year T-Bills come in at 3.3% yield.

If you buy the latest 6-month T-Bills at 3.64% yield, as long as you can roll over the cash into 3.00% or more yields in 6 months time, you’re probably ahead.

Whereas the higher the yields on the 1-year T-Bills, the more attractive they are.

So for cash buyers, a competitive bid could be a good way around the issue.

Maybe at 3.30% you’re better off just sticking with 6-month T-Bills, but at 3.50% it’s a good buy… you get my point on the competitive bidding.

What about for CPF-OA buyers? Buy 6-month T-Bills or 12-month T-Bills?

That being said for CPF-OA buyers the 1-year T-Bills are pretty attractive because:

- You lock in interest rates for the next 1-year (in fact you get the interest upfront)

- You minimise the lost interest from when you roll over 6-month T-Bills

The logic above on where yields will be in 6 months continues to apply.

But because of the lost interest dynamics on CPF-OA, I think the 1-year T-Bills are comparatively much more attractive for CPF-OA buyers.

Especially if you don’t need to use the CPF-OA money, and even something like 3.40% is higher than the 2.5% paid if you leave in CPF-OA.

OCBC has a CPF Fixed Deposit – but only pays 2.8% for 1 year on CPF-OA

Do note that OCBC has a CPF-OA Fixed Deposit.

However the interest rate is not attractive – 2.80% for 12 months.

You’re better off just buying T-Bills.

Even if demand is very high, I doubt the 1-year T-Bills would come in below 2.80%.

Which is a better buy – T-Bills vs Fixed Deposits or Money Market Funds?

For cash buyers, I compared against some alternative options below.

You can now follow Financial Horse on Google Chrome to avoid missing any posts!

Just:

- Click the 3 dots on the top right of Google Chrome

- Click Follow!

- And Financial Horse posts will now appear on your home page, under Following:

You can also follow Financial Horse on:

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

Singapore Savings Bonds pay 3.19% for 1-year

The latest Singapore Savings Bonds pay:

- 3.19% for the first 6 years

- 3.22% for 10 years

This makes the SSBs a pretty decent buy if you think the 1-year T-Bills yields are going to drop this auction.

Money Market Funds pay about 3.5% – 3.8% yield – but not risk free, and yields can change any time

Money Market Fund yields have been sitting at the 3.5% – 3.8% range for a while now.

Money Market Funds are technically not risk free though – so this is a big point to note.

And Money Market Funds invest in short term instruments, so the interest rates will fluctuate from time to time.

This is unlike a 1-year T-Bill where you are “locking in” interest rates for the full 1-year.

The benefit though, is that you can get your money back with T+1 liquidity, which is a big plus vs T-Bills.

Best Fixed Deposit option? 3.20% for 1-year with DBS/POSB Bank

The best fixed deposit option for 12-months is 3.20% with DBS / POSB Bank (or State Bank of India).

If you’re comfortable using Syfe Cash+ Guaranteed (where you deposit with Syfe who parks the funds in an institutional fixed deposit account for higher yields).

Then the yields are 3.45%, but do note that this is NOT SDIC insured (and therefore not risk free).

Will I buy 1-year T-Bills vs Money Market Funds vs Singapore Savings Bonds vs Fixed Deposit vs Savings Accounts?

At this point in the interest rate cycle, I think you want to spread your cash around various tenures, given the risk of interest rate cuts going forward.

You want to hold some instruments that can lock in yields:

- T-Bills (both 6-months and 12-months)

- Singapore Savings Bonds

- Bonds (eg. Astrea Bonds)

While also retaining some liquidity:

- High yield savings accounts

- Money Market Funds

Personally I think I will apply for the 1-year T-Bills.

But I will use a competitive bid.

I think that if the 1-year T-Bills yields come in at the lower end of my projected 3.30 – 3.60% range, they’re not super attractive when you factor in the fact that this money is completely locked up for 12 months.

But if they came in at the higher end of the range, they could be pretty attractive given all the uncertainty over interest rate cuts going forward.

That’s just my view though, would leave to hear what you think!

This article was written on 19 July 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

4.20% on first $20,000 if you deposit to Chocolate Finance

I wrote a detailed review on Chocolate Finance, so do check if out if you are keen.

Long story short is that Chocolate finance pays 4.2% on the first $20,000, withdrawable instantly.

The funds are invested in a selection of bond and money market funds, and Chocolate Finance will top up any returns if they are lower than 4.2%.

To be clear this is not SDIC insured and not risk free.

So I leave it for investors to decide if you are comfortable with the risks (see my full review here).

Chocolate Finance currently is invite only, but you can use the FH invite link below if you are keen to try it out:

https://share.chocolate.app/nxW9/ep4q7wxp

– Get USD 400 cash voucher

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 400 cash voucher.

You just need to:

- Deposit USD 2000 (or 10,000 for higher rewards)

- Execute 5 trades (for higher rewards)

Note that Webull is also offering zero commission for US options trading right now.

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.