As regular readers will know, unlike 6 month T-Bills which come by every 2 weeks or so.

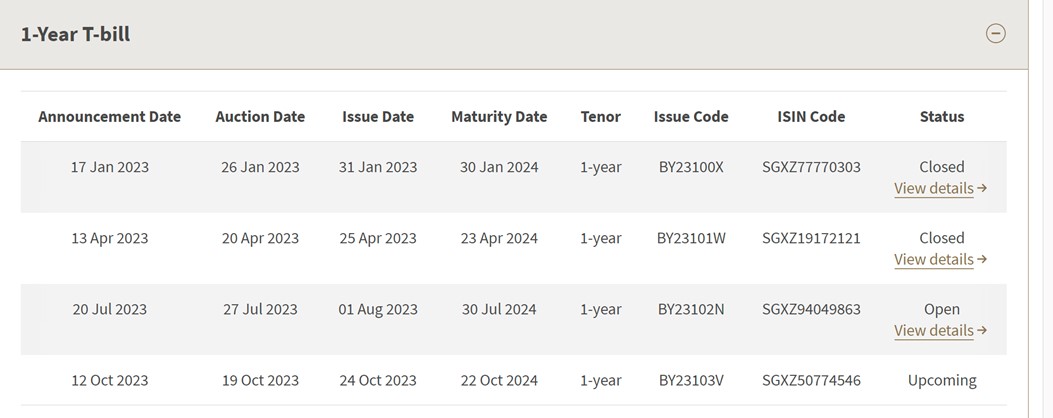

1 year T-Bills are quite rare – there are only 4 a year.

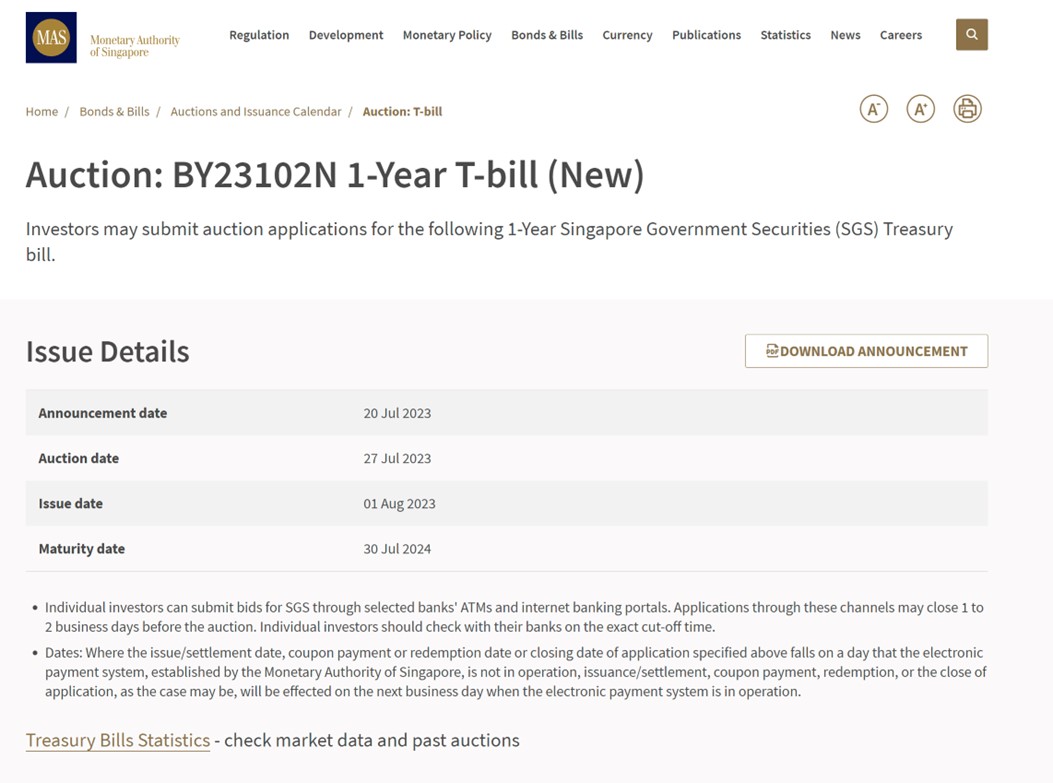

The next 1 year T-Bill auction is coming up on 27 July 2023.

So if you’re keen to buy the 1 year T-Bills, you probably don’t want to miss this round.

Let’s discuss 2 key questions:

- What is the estimated yield for the 1 year T-Bills?

- Are the 1 year T-Bills worth buying – for cash or CPF-OA buyers?

What is the estimated yield for the 1 year T-Bills? (27 July 2023 Auction)

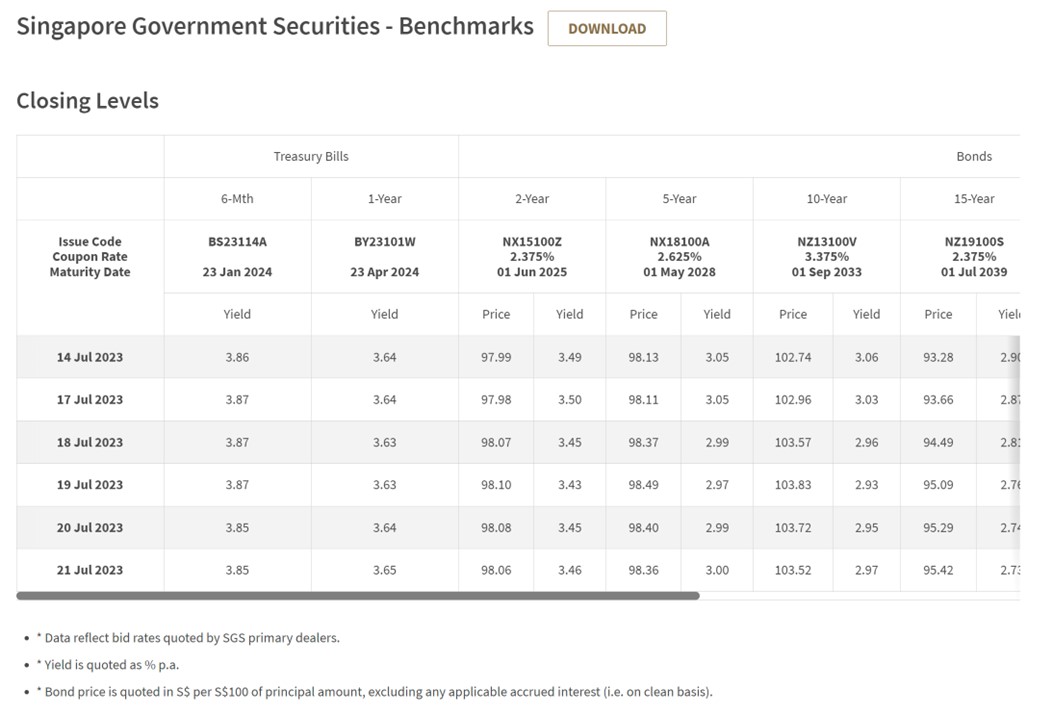

1 year T-Bills trade at 3.65%

First off- the 1 year T-Bills trade at 3.65% on the open market.

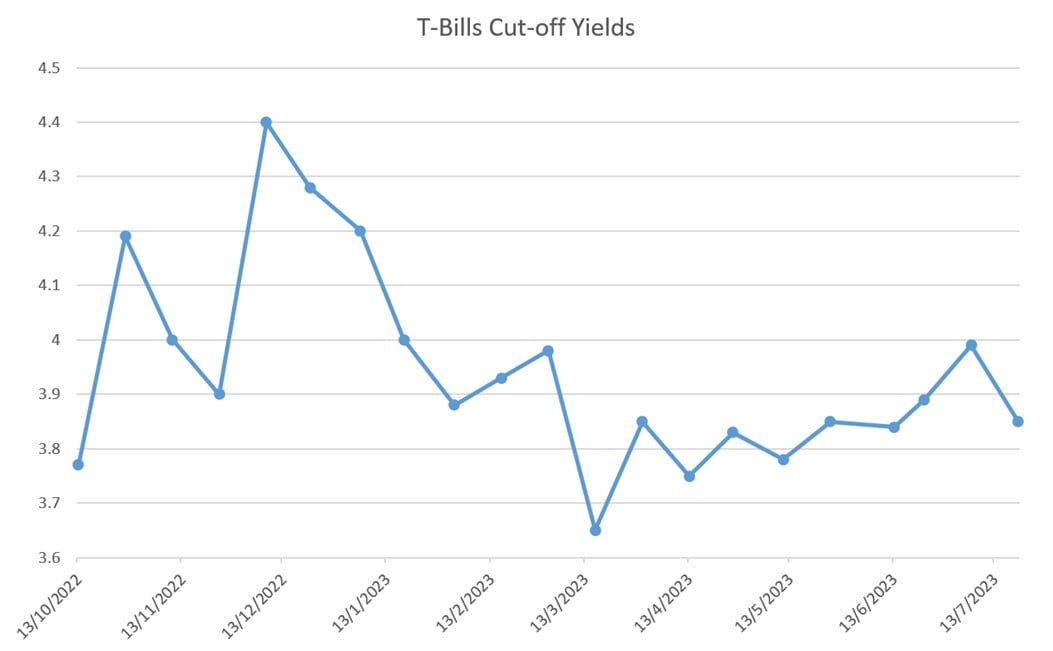

Past 1 year T-Bills cut-off yields come in below prevailing market prices

If you look at the past few 1 year T-Bills auctions though.

You’ll find that the final cut-off yields come in below prevailing market prices.

This is likely due to demand from CPF-OA buyers, given that the 1 year T-Bills are an especially good buy for CPF-OA buyers.

Namely because (1) you lock in interest rates for 12 months, (2) you minimise the amount of lost CPF-OA interest, and (3) you don’t have to bother rolling over the CPF-OA funds into new T-Bills in 6 months’ time.

If this holds true again, then 3.65% might be a good benchmark for the 1 year T-Bills auction.

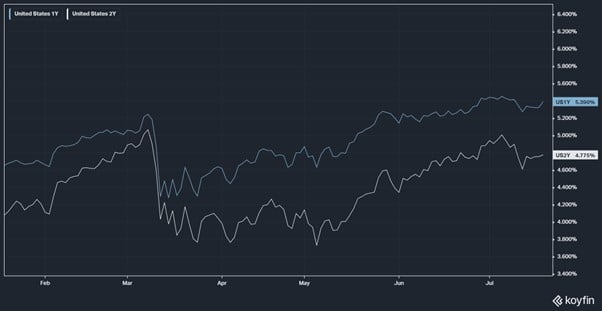

There is a downtrend in US and Singapore yields

Unfortunately, there’s a bit of downtrend in US and Singapore interest rates of late.

US 1 and 2 year interest rates have come down since the start of July.

This is mainly because of weaker inflation data in the US that has led the market to price in fewer rate hikes from the Fed.

There’s a broadly similar trend in Singapore as well, as the most recent 6-month T-Bills closed at 3.85% cut-off yield (vs 3.99% from the previous auction).

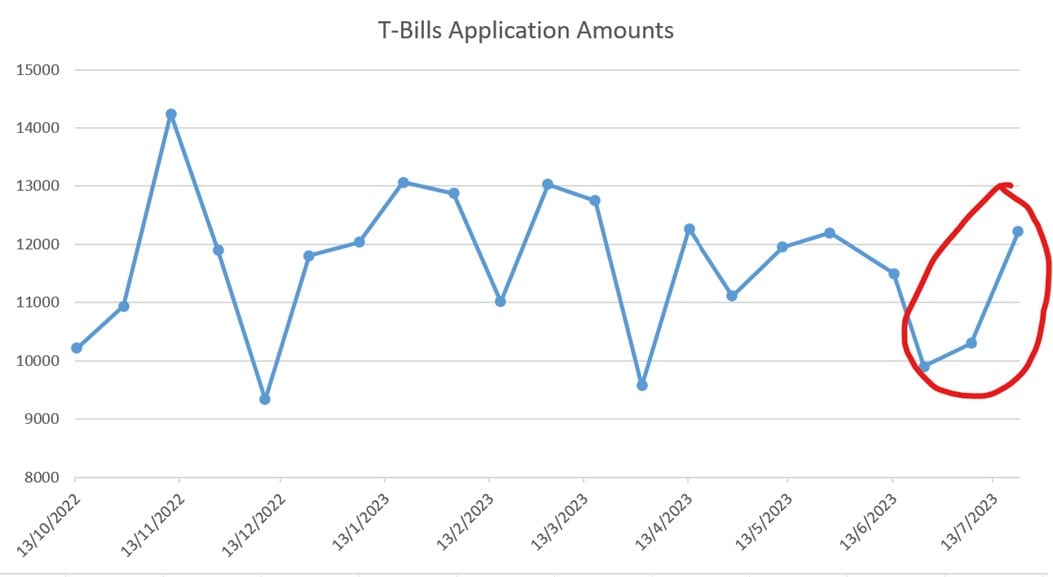

Demand for T-Bills is the Wildcard

The wildcard is always demand.

Investor demand for the most recent 6 month T-Bills auction jumped 18%, which partly explained the decline in yields.

Will we see that for the current 12 month T-Bills auction?

Frankly your guess is as good as mine.

Estimated yield of 3.60 – 3.70% on the next 1 year T-Bills Auction?

Put all of the above together, and I probably going to go with an estimated yield of 3.60% – 3.70%.

As always, I encourage investors to put in a competitive bid, just to avoid any freak results.

Are the 1 year T-Bills a good buy?

Whether the 1 year T-Bills are a good buy will depend on whether you’re buying using cash or CPF-OA.

Let’s discuss each individually.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Cash Buyers – Are the 1 year T-Bills a good buy?

The main advantage of 1 year T-Bills vs 6 month T-Bills is that it lets you lock in interest rates for 1 year.

The main disadvantage of course, is that you are locking the money up for 1 year, and it is not easy to get the money back prior to maturity.

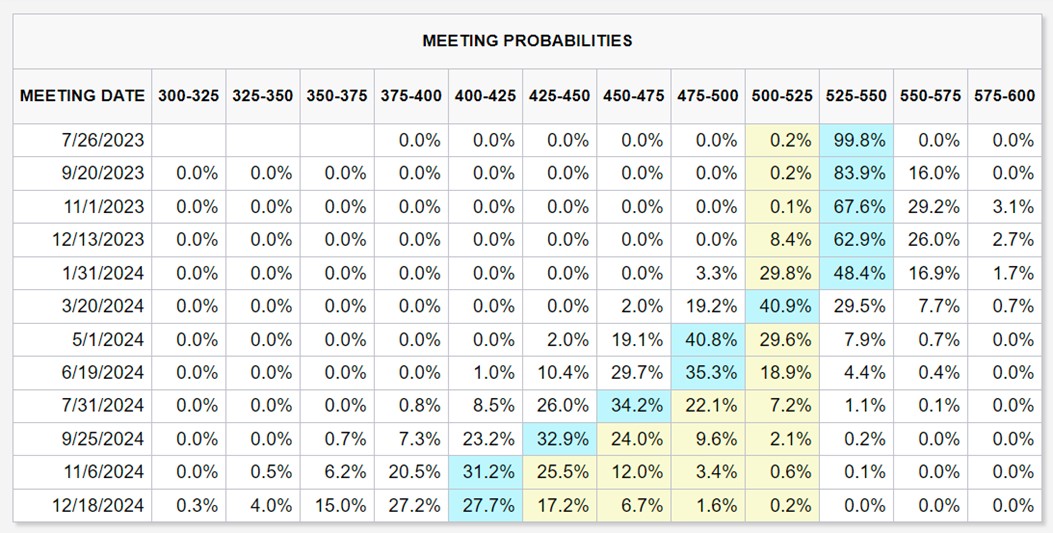

If you look at interest rate curve pricing, the market is pricing in:

- 1 more interest rate hike this month

- No more interest rate hikes (and no cuts) until March 2024

My Personal Views? I’m probably not buying 1 year T-Bills with cash.

The way I see it, if this market pricing is right.

Then I don’t really see the need to lock in 1 year T-Bills at this level of interest rates.

I might as well just buy the 6 month T-Bills with cash.

I enjoy the 3.85% yield for 6 months, after which I evaluate where the market is – and decide what to do with my cash then.

If the market pricing is right (no interest rate cuts until March 2024), I should be able to roll over the cash into 6 month T-Bills in Jan 2024 at pretty decent interest rates.

The only scenario I come out ahead on the 1 year T-Bills is if interest rates are slashed rapidly (vs what the market is pricing in), over the next 12 months.

And right now that’s just not my base case.

Yes I think the economic is slowing, and we’re going to have a period of economic slowdown (and possibly recession) in 2H 2023 – 1H 2024.

But I don’t think it will happen fast enough for rapid interest rate cuts in the next 12 months.

Could be wrong though.

Alternatives to T-Bills for cash buyers?

GXS Bank – 3.48% on cash

For cash buyers, I just wrote about GXS Bank yesterday which I think is very attractive.

You’re getting paid 3.48% on cash, on up to $75,000.

With no minimum deposit, and no lockup period.

And no hoops to jump through.

You just put money in, it earns 3.48% pa accrued daily.

And you can take it out anytime.

I think it’s a fantastic deal, and a very strong alternative to T-Bills or Fixed Deposits or Singapore Savings Bonds.

Yes yields are not as high, and GXS may decide to cut interest rates down the road.

But as long as it lasts, it’s a very good deal.

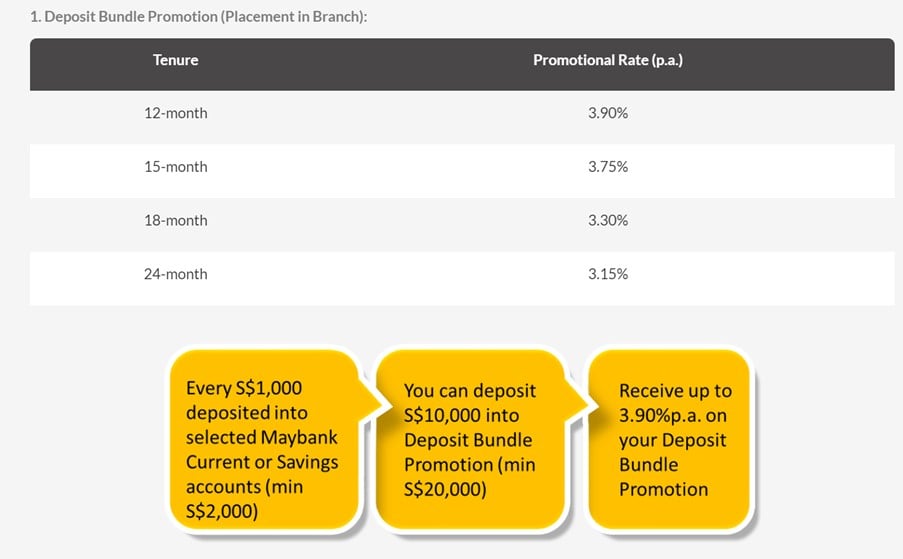

Best Fixed Deposit – 3.5%ish blended rate with Maybank

Alternatively you can use the Maybank Fixed Deposit which pays 3.90% for a 12 month deposit.

Do note that you do need to deposit $1,000 for every $10,000 in fixed deposit.

This brings the blended yield down to about 3.5%-ish, which is in line with other banks like ICBC or BOC.

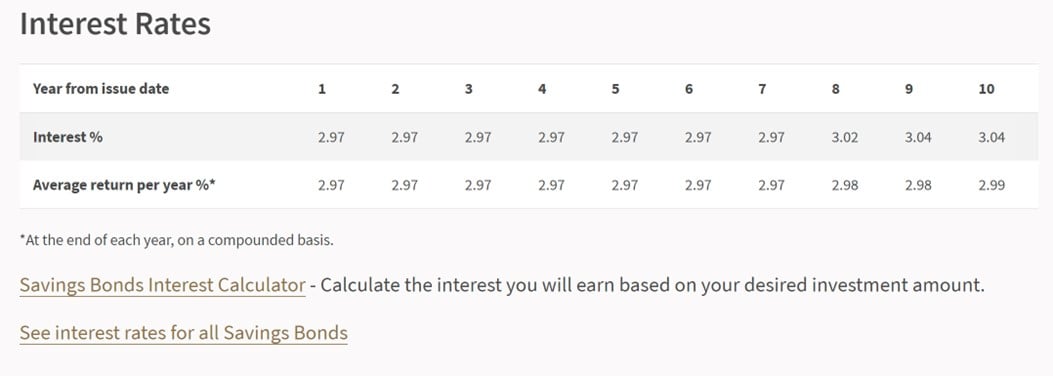

Singapore Savings Bonds yield 2.97%

Latest Singapore Savings Bonds yield 2.97% all the way up to 7 years.

The benefit with Singapore Savings Bonds is that you’re locking in interest rates up to 10 years, and can get your money back any time (money comes back the next month).

With T-Bills you get a higher interest rate for now, but you only lock in rates for 1 year, and you cant get the money back easily before maturity.

CPF-OA Buyers – Are the 1 year T-Bills a good buy?

For CPF-OA buyers it’s a completely different story.

Do note that the auction date is 27 July 2023, which means successful CPF-OA buyers will see moneys deducted from CPF-OA on 28 July 2023.

This means you’ll lose the July 2023 CPF-OA interest as well, even though the T-Bills are only issued in August 2023.

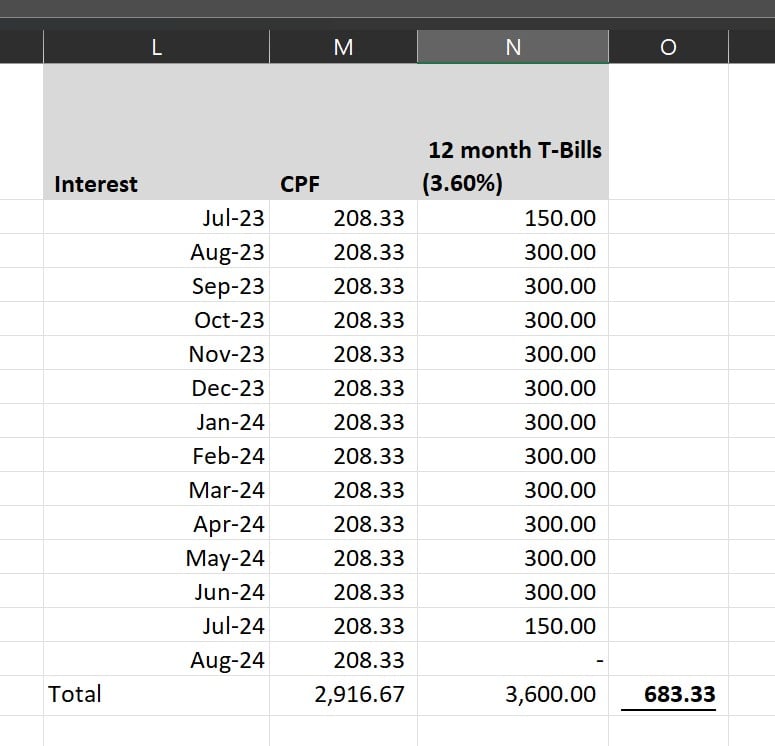

Crunching the numbers – CPF-OA buyers of 1 year T-Bills

I’ve crunched the numbers below for you.

Assuming you buy the 1-year T-Bills at 3.60%.

With $100,000 CPF-OA funds.

You’ll still make $683 extra buying the 1-year T-Bills, as compared to leaving them in CPF-OA.

This is of course assuming that there are no changes to the CPF-OA interest rates.

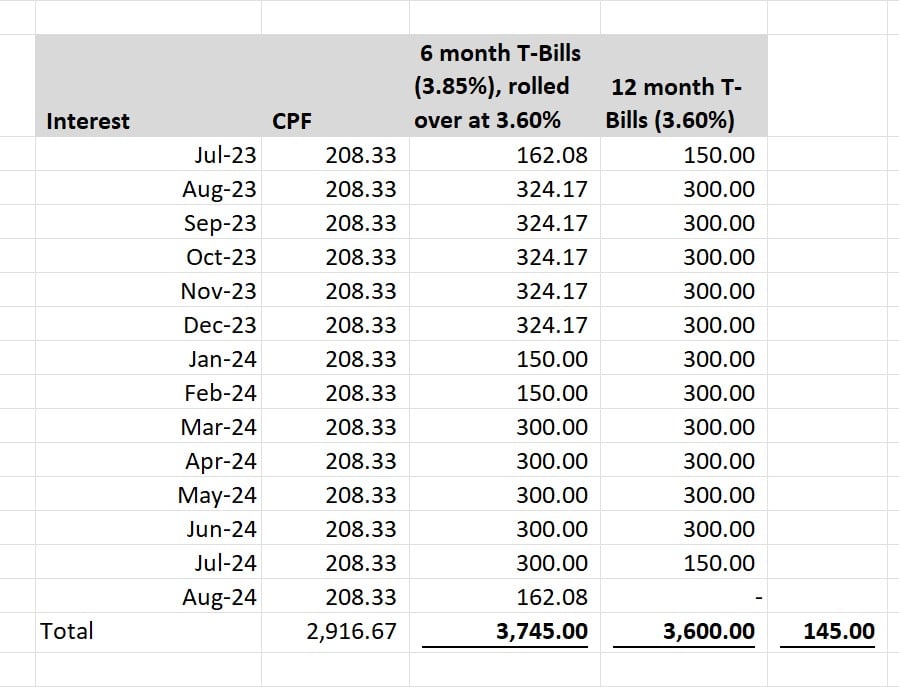

What about 6 month T-Bills vs 1 year T-Bills?

What about 6 month T-Bills instead?

Assuming that you buy the 6 month T-Bills at 3.85%.

Roll them over at 3.60%.

Then the 6 month T-Bills come out slightly ahead – $145 extra.

So… buy 1-year or 6 month T-Bills with CPF-OA?

As you can imagine, there’s a lot of assumptions that go into the numbers above.

Where will T-Bills interest rates be in 6 months?

Can you roll over in the same month or the following month?

Whatever the case, it’s fairly clear that the numbers for 6 month and 1-year T-Bills are very close.

Close enough that it will come down to factors beyond your control.

So for CPF-OA investors who want the peace of mind and don’t want to have to bother applying for T-Bills again for the next 1-year.

I think the 1-year T-Bills are worth considering actually.

Most of my CPF-OA funds (that are not earmarked for mortgage repayment) is already locked up in 6 month T-Bills.

Otherwise I would definitely consider doing a competitive bid on the 1 year T-Bills with CPF-OA funds.

This article was written on 21 July 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

WeBull Account – Get up to USD 800 worth of shares (expires 31 July)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund $300 SGD

- Execute 1 buy trade within 30 days of funding

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

What about seniors-those over 65. Is it still good to use CPF to buy Tbills for 1 year? Is it those over 65 have another extra 1% interest for the cpf saving.

If your CPF is earning 3.5% then I dont think T-Bills look that attractive. Don’t forget with T-Bills you will lose the extra month (or two) of CPF-OA interest, which brings the effective yield down about 0.2-0.4%.