I’ve been getting quite a few questions on mortgages recently.

The crux of it – whether it makes sense to repay your mortgage, instead of refinancing at ridiculous interest rates (latest rates are 4.25%).

The answer is not so straightforward and a bit nuanced, so I wanted to write a post exploring this dilemma.

45 year old investor – Should he repay his $300,000 mortgage now or invest the cash?

Here’s one of the questions that I received recently.

Details have been anonymised to protect the privacy of the individual:

“Thanks FH. Sorry for a really long mail but I appreciate if you can share your views on my below situation.

Recently after reading your post about rising mortgage rates I was fortunate enough to lock in my current mortgage at a fixed rate of 2.75% with UOB for 2 years before the big spike in mortgage rate. My outstanding mortgage is 290k for remaining 25 years. Monthly payment is about $1325 a month which I am paying mainly via cash instead of cpf. This is my only debt. I have 3 teenage kids and my wife is a homemaker. My 3 children will graduate from university in 10 years time if all goes well and I will be 55 by then.

I do have the means to repay my mortgage in full either via my cpf or cash when it is due for repricing in 2 years.

- I am a strong 1m65 believer and have been striving to build up my cpf accounts. My SA is fully maxed out and OA has a surplus now as well to be able to pay off my mortgage. When mortgage and SSB/T-bill yield were at lows, I was happy to let my OA compound at 2.5% pa. With equities on a correction now, I am actually considering to invest my cpf OA basis a split of 75% s&p 500 index fund and 25% in t-bills, but this will draw down my funds to repay my mortgage if need be. For now the cpf OA funds is on standby for signs of a Fed pivot over the next 2 years so I can invest them.

- On my cash reserves, other than keeping about 10-12 months of emergency cash for the family in SSB currently, I am also keeping more cash on hand via SSB/T-bill/ high interest savings account to buy into the U.S. and SG equities market when the fed finally decides to pivot. However in such an event, similar to my plan for my cpf, it will also draw down my cash funds to repay the mortgage in 2 years. On a separate note, I already have a SGD 300k portfolio of sg shares comprising of local banks/reits/singtel. Singtel unfortunately makes up 10% of my portfolio and it is still out of money by 20% net of dividends over the last 5 years.

The common advice I always receive is to stretch the mortgage to invest the spot cash in equities etc to get a better rate of return over the long term. I believe the theory has worked well over the last 12 years in a low interest rate environment. However every report I have read now says that is all dusted and done with. Higher for longer is the new mantra for the feds now.

- So I would like to seek your view at which point does it make sense to redeem the mortgage in full?

- Should I continue to stay invested at least for the next 10 years until my children graduate and I decide to really semi-retire with a big paycut? By then I should still have approximately 170k of mortgage left. If my portfolio can ride out the downturn and volatility with a 5-6% return pa, it will still have a net 2-3% gain over my mortgage if I can keep it at 3% pa over the 10 years. This is not taking into account of inflation. At this point I will cash out part of my portfolio (which should have grown more than my original sum) to repay the mortgage.

- What is the sweet spot to know it’s time to redeem the mortgage assuming no major life changing events?

Thanks again in advance for your time.”

There are 3 questions from the reader, so let’s tackle them individually.

So I would like to seek your view at which point does it make sense to redeem the mortgage in full?

The simple answer, is that you repay your mortgage when the mortgage interest rates is higher than what you can reasonably earn elsewhere on the money.

And the answer to this question, will depend very much on what you are doing with the money.

So by it’s very nature, only you can answer this question.

Does it make sense to repay the mortgage right now at 2.75%?

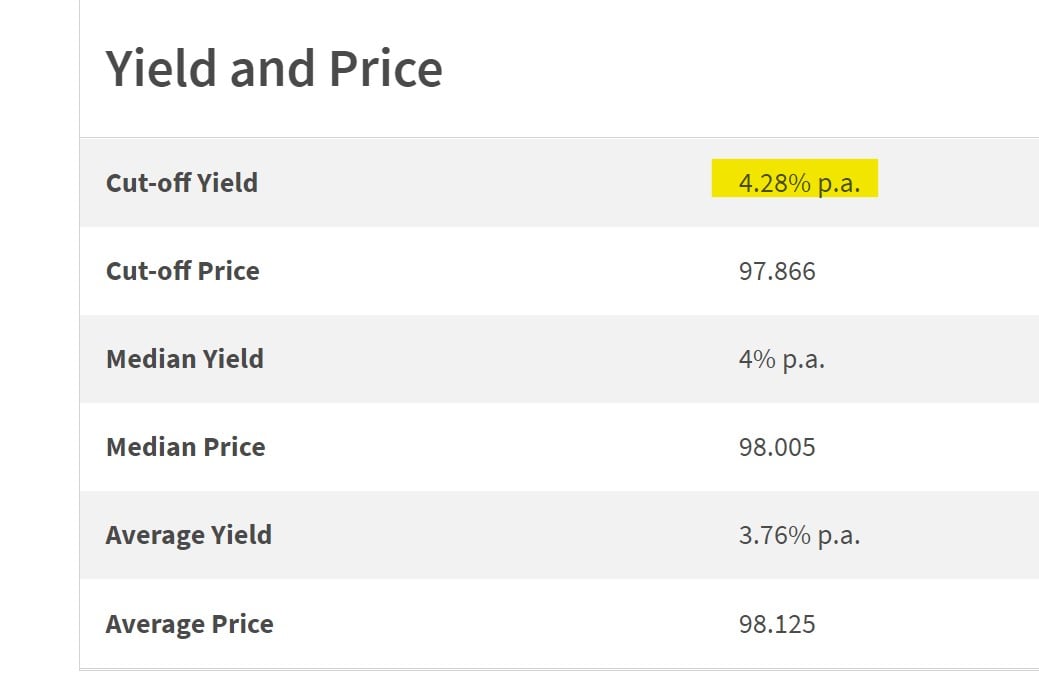

If you have completely no use for the cash, then the best benchmark would be to chuck it in a risk free T-Bill or Fixed Deposit.

The latest T-Bills yield 4.28%, so if your mortgage is at 2.75%, it’s just a complete no brainer to keep the mortgage, and put the spare cash into T-Bills to earn the spread.

In any case, if your mortgage is during the commitment period, you cannot prepay without incurring an early repayment fee.

So the answer for now, is quite straightforward.

You keep the mortgage, at least until the 2 years is up and you have to refinance.

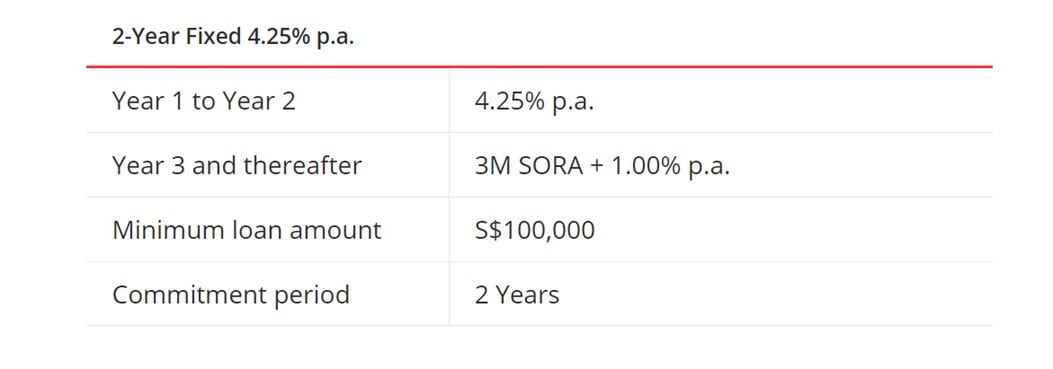

Does it make sense to repay the mortgage when it comes due, and you refinance at 4.25%?

Now imagine the mortgage is up, and you need to refinance at 4.25%.

Whether to repay the mortgage will depend on what you do with the cash.

If you’re a business owner who needs the cash to invest in their business – most of the time the mortgage will be your cheapest source of financing.

So business owners more often than not, will want to keep and even max out their mortgage.

What if you’re a normal salaried employee, who plans to invest the money?

Then I suggest to think about:

- Your level of investment knowledge / ability

- Macro conditions

Your level of investment knowledge / ability

Think about your level of investment knowledge.

Think about your confidence in stock picking / market timing.

Think about a realistic level of returns you can achieve on the cash.

And be realistic with yourself here.

Who are you trying to kid.

If your investment returns over the past 10 years was 4% annualised, do you really think you will suddenly achieve 10% a year in the next 5 years?

But if you’ve been pulling a 7% annualised return over the past 10 years, then yeah I would say it may make sense to continue investing the money instead of repaying the mortgage.

Macro conditions

Now this point is a bit more nuanced.

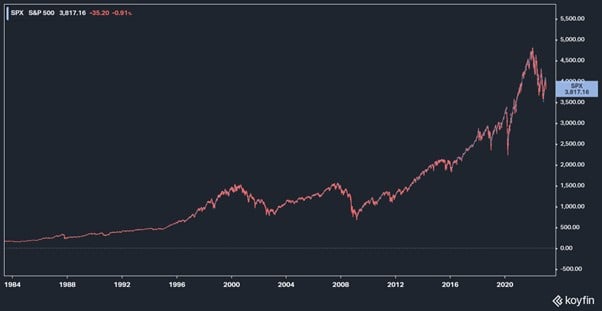

The past 40 years, was a single regime of falling interest rates:

And when interest rates go down, asset prices go up.

Which means most investment strategies you see today, including most buy and hold advice, are backtested using a 40 year regime of falling interest rates:

My personal belief, is that this regime is now over.

And we are moving into a new regime of higher interest rates, with more sticky inflation.

The implications for investing are going to be massive, requiring more active positioning.

So the point here is – be very realistic with yourself on what kind of returns you can achieve going forward.

If you keep the mortgage, you are guaranteed to pay 4.25% a year.

The markets going forward might be much more volatile and harder to navigate.

Even if you did well in the past 10 years of low interest rates, doesn’t necessarily mean you will do well in the next 10 years.

It’s clear the reader himself is aware of this dilemma, as per his quote:

“The common advice I always receive is to stretch the mortgage to invest the spot cash in equities etc to get a better rate of return over the long term. I believe the theory has worked well over the last 12 years in a low interest rate environment. However every report I have read now says that is all dusted and done with. Higher for longer is the new mantra for the feds now.”

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Should I continue to stay invested at least for the next 10 years until my children graduate and I decide to really semi-retire with a big paycut? By then I should still have approximately 170k of mortgage left. If my portfolio can ride out the downturn and volatility with a 5-6% return pa, it will still have a net 2-3% gain over my mortgage if I can keep it at 3% pa over the 10 years. This is not taking into account of inflation. At this point I will cash out part of my portfolio (which should have grown more than my original sum) to repay the mortgage.

Back to the point above.

You can have a perfect plan on how you want to invest, and when you intend to cash out.

But markets don’t work on your timeline.

Markets work on their own timeline.

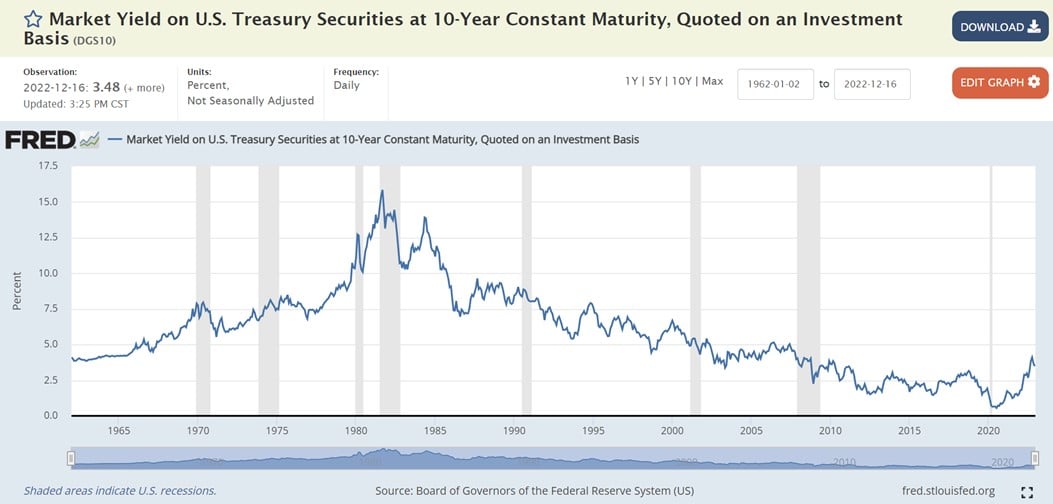

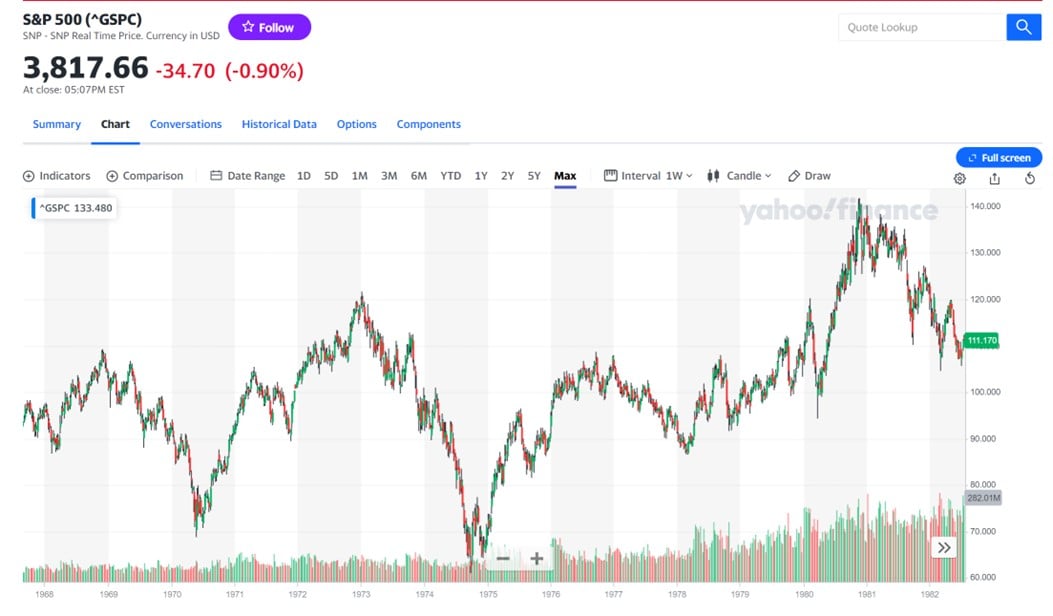

I extracted a 15 year chart from 1968 to 1983 below, the last time inflation was a problem.

The S&P500 basically went nowhere for a 15 year period, with massive volatility along the way.

Imagine hypothetically that something like this repeats over the next decade.

Whether you can cash out, and what returns you see, will depend very much on market conditions.

Including the exact timing you decide to cash out.

So yeah… it’s not only about what you want.

Because the markets work on their own timeline.

I would always err on the side of caution in things like that.

If you need the money to pay your kid’s university fees soon, better to just cash out and chuck it in risk free T-Bills at 4.4%, than to keep it in equities hoping for an extra 2% return and losing sleep.

What is the sweet spot to know it’s time to redeem the mortgage assuming no major life changing events?

As shared above, the sweet spot is when you are no longer confident that you can earn a return higher than the mortgage rate (4.25%).

I will share more thoughts on the investment side of the equation below.

But I do want to stress that this is ultimately a personal decision.

Think about your life goals

As I keep saying on Financial Horse, think about why you are investing.

Some people do it because they love the game, and can’t imagine doing anything else.

Some people do it so they can make a ton of money, and retire with a $10,000 a month passive income.

Some people do it so they can give the next generation a comfortable life.

The key question I suggest you to think about – is whether you want to get even richer, or if you are comfortable maintaining your current level of wealth.

Paying off the mortgage is a low risk, low reward kind of move.

It is safe, sensible, and you won’t go bankrupt doing it.

But neither will you get filthy rich.

Borrowing at 4.25% to invest is a much higher risk higher reward kind of move.

You have a chance of losing a lot of money, but you also have a chance of making a lot of money.

Think about the effort

Think also about the effort required to manage money.

Even if you can hit a 5% return, how much time and effort is required to generate that return – and is it worth it?

If you’re not the kind that enjoys reading financial reports and keeping track of Powell’s every single word, paying off the mortgage and saving that 4.25% a year is frankly not a bad idea.

Especially if you’re the kind that will lose sleep if your equities portfolio is down 30%.

The reader himself knows the feeling of losing money on his Singtel shares.

Imagine if that repeats this decade, with your new investments.

Is that something you can live with?

What if you wanted to go the investing route?

Let me just put it out there and say that I think investing in this decade is going to be a lot harder than in the past decade.

Without Fed fuelled easy liquidity, a lot of passive strategies may not work so well.

I think if you want to do well this decade, you need to be a lot more active in your approach.

You’ll want to watch macro conditions closely for market timing, because the central bank dance between growth and inflation will be crucial.

You’ll want to be careful with stock picking, because a lot of last decade’s winners like tech and REITs may not do so well in a regime of higher interest rates.

A lot of you have asked what to buy to outperform the 4.25% mortgage rate, with low risk.

If only it were that easy!

I don’t think there will be any magic formula in this new regime. It will require a more active approach.

In any case, the answer to this question is what the rest of Financial Horse is about. And my full stock / REIT watchlist is available on Patreon.

What would I do… in the same situation?

I know many of you want a straight answer from me.

So here goes.

If I were in the same situation above?

I think it’s clear I won’t repay the mortgage until the 2 year commitment period is up.

And whether I repay the mortgage 2 years later is a decision I will only make in 2 years later, because market conditions (and personal conditions) may have changed materially.

But knowing what I know today?

I think I might just pay off a third to half of the mortgage (100k – 150k).

And for the rest I will switch to a shorter duration mortgage of 15 – 20 years.

While investing the spare cash.

I think for me, that would probably be the best balance between risk and reward. I don’t want to take on too much risk to jeopardize my retirement and family’s future. But I also don’t want to be too cautious and have my purchasing power eroded away by inflation.

But frankly – that’s just me.

I cannot stress enough – this must, must, must be a personal decision.

Only you can make it for yourself.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there

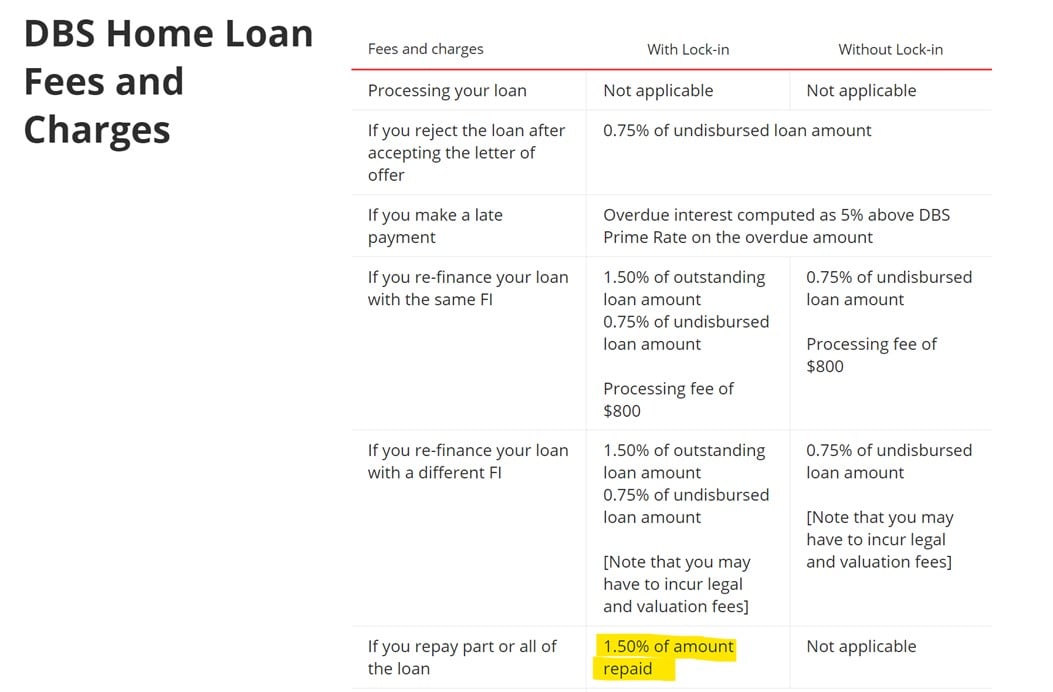

Hi, tx for yr article as always. I’m on dbs house loan of est 600k and the loan interest rate is going up to 3.55% in 3 months time. More increase likely in 2023. In yr view, should I switch to a fixed 2yrs interest package of est 3.9% now?

Hm that’s not an easy question to answer because it will depend on your interest rate outlook, and your risk appetite.

Short of knowing exactly where interest rates go in the next 2 years, it’s all about balancing risk-reward for your individual personal situation.

That was a really a ‘well-put’ response to the original query.

Am also in a similar situation, just turned 55….my outstanding loan is 300K @1.45% pa; loan tenure 8 years, 2 year lock-in period ending in Jun 2023. Am thinking to pay-off the outstanding loan amt either by cash or CPF-OA. My RA is at ERS and have enough in OA to pay the outstanding loan amt.

My dilemma…..should I use OA amt or cash to pay the outstanding loan amt.

One option is to use CPF-OA to pay the outstanding amt and put the excess cash in to FD at 4% for a year. After a year when FD matures, transfer the money into CPF-OA under ‘voluntary housing refund’ and continue to earn standard OA interest.

Will appreciate your thoughts on the above.