Want to retire early?

Here are 5 important facts of early retirement you should take note of.

This article was written by a Financial Horse Contributor.

1. Retirement vs Re-employment age

Do you know the difference between retirement and re-employment age?

Our current statutory minimum retirement age is 63 years old. This means that employers are not allowed to dismiss any employee below age 63 because of the employee’s age.

The retirement age will be raised gradually to 65 by 2030.

What about re-employment?

Currently, employers must offer re-employment to eligible employees who turn 63, up to the re-employment age of 68. This provides older workers with more opportunities to work longer, if they wish to do so.

The re-employment age is currently 68, and will be raised gradually to 70 by 2030.

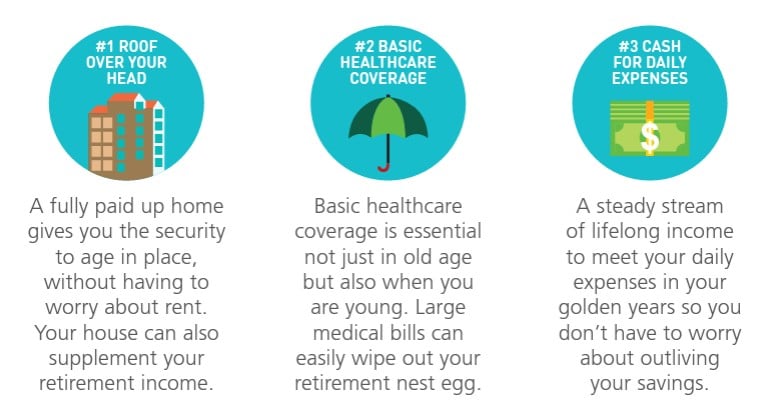

2. Can CPF cover your basic needs?

The three most important pillars to have a comfortable retirement are:

- housing

- healthcare

- expenses

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

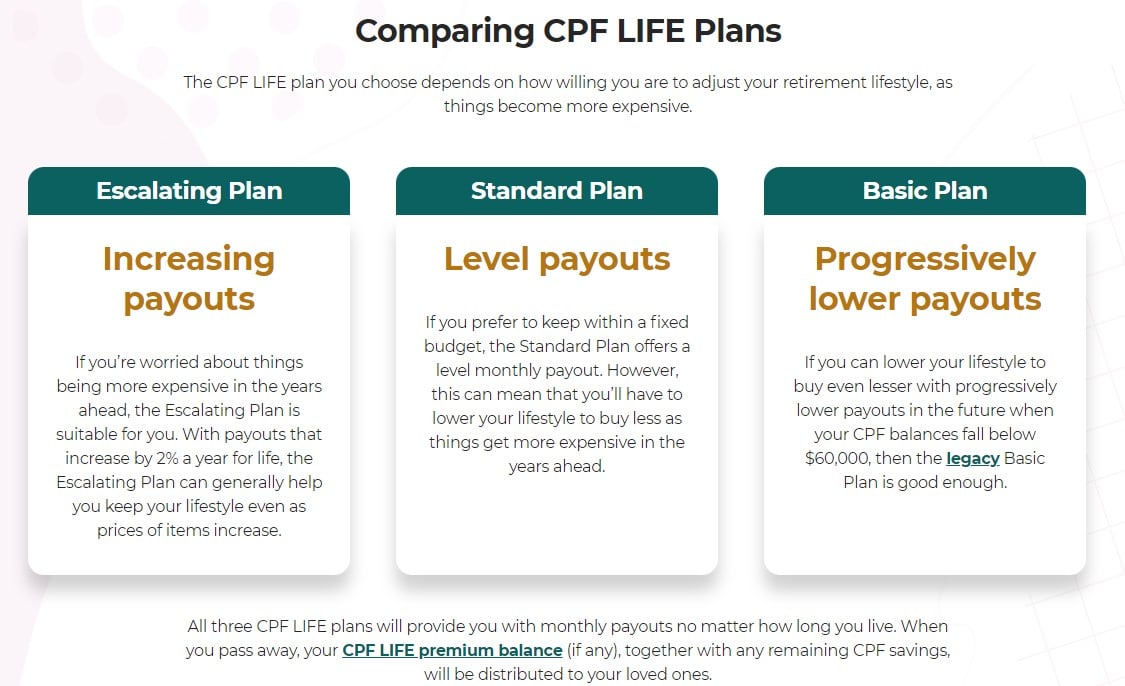

How much do you need to have in CPF to help you have a comfortable retirement?

You’ll be automatically included in CPF LIFE if you’re:

- A Singapore Citizen or Permanent Resident;

- Born in 1958 or after; and

- Have at least $60,000 in your retirement savings when you start your monthly payouts

Check out the CPF Life estimator to estimate your payouts.

3. Changing the equation

People often underestimate how much they need for retirement.

FIRE (financial independence retire early) proponents aim to save 70% or more of their full-time income. The holy grail is to save 25 times of one’s annual expenses and make 4% annual withdrawals for living expenditures.

However, this equation often doesn’t account adequately for changing circumstances.

Lifespan is increasing and many things in the future decades ahead cannot be predicted.

According to the latest data from SingStat, the average life expectancy in Singapore is 83.5 years. Women have a longer lifespan of 85.9 years, compared to men at 81.1.

Assuming you retire at 63, that adds up to about 18 to 22 years that you’ll need to plan for.

You may have thought $50,000/year was plenty to live on when you embarked on your FIRE journey in your 20s, but by the time you’re 45, your needs may have changed drastically. You may need to adjust your number upward before you can have the retirement you were envisioning.

Check out NTUC’s retirement calculator to estimate your expenses.

“We know we’re living in increasingly uncertain times. I see a lot of people under-saving and overestimating the potential future performance of the stock market. The past five or 10 years is not a good measure of what the next 30 to 40 years might hold,” says Lubinski, a financial adviser.

This is especially true as the last decade has been the longest bull market in history.

Err on the conservative side and model your portfolio with a lower rate of return e.g. 5%.

4. Income-yielding portfolio

In your 20s and 30s, you may have a portfolio centered on growth stocks and capital gains.

Near retirement, you probably won’t have a portfolio invested entirely in equities.

Experts says that investors should focus on “reliability of income” instead of return on investment.

This means adjusting your investments to a capital-preservation and income-centric approach.

This is why many Singapore investors aim to have a high-yield income portfolio consisting of quality dividend stocks and REITs.

Check out FH’s REITs Masterclass to learn more about how to create such a portfolio!

Lubinski also suggests creating a 10-year financial buffer.

5 years before retirement + 5 years after retirement

“At least five years before their early retirement date, investors should set aside the amount of money required to provide income for their first five years of retirement,” says Lubinski.

“This will effectively put a 10-year buffer between the money they need for early income and any market volatility that could take place during their five-year countdown to retirement.”

By separating your funds you’ll need early in your retirement, you give yourself some buffer should the market experience volatility. Under this model, your remaining investments will have years to bounce back from any losses before you’ll need to tap them.

5. Post-career identity

Do you know what you want to do after early retirement?

Grant Sabatier, creator of finance website Millennial Money and author of “Financial Freedom,” retired early with USD $1.25 million at 30 years old.

Sabatier recommends to think about your post-career identity.

“So much of our identity is tied up to our work and the things that we do in our professional life,” says Sabatier. “A lot of people spend all this time working and saving and investing in order to retire early, then they don’t have an idea of what they want to do after.”

If you’ve accumulated enough cash savings to cover a year or more of expenses, try a “mini retirement” to get a sense of how life away from the office actually feels, Sabatier suggests.

If you do a mini-retirement or short-term sabbatical while you’re younger, this helps you get clear on what kind of retirement lifestyle you desire – and importantly, the type of expenses and/or income you’ll likely be generating.

This helps you to better estimate your post-retirement lifestyle and the finances required to get you there.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.