Okay, so Wednesday’s FOMC was really, really important.

To the point where it requires a full article on it.

We spent all of 2022 talking about a Fed pivot, when it will come, and what to buy when it comes.

Many investors are taking Wednesday’s FOMC as a soft Fed “Pivot”.

And for what it’s worth, I’m inclined to agree with them on this.

Time to buy stocks and REITs?

That said, whether you buy this “Pivot” is a bit more nuanced.

Reason being that for the first time in 40 years, inflation is the limiting constraint.

So even if Powell wants to cut rates to zero and go back to infinite QE, whether he can do so will depend very much on the path of inflation going forward.

And investing is very much about risk-reward, so we also need to look at what is already priced into the current market.

But in any case I’m getting ahead of myself here.

Let’s break it down step by step.

Note: This is a premium Patreon article. I am releasing it to all readers given the importance of this topic.

Do sign up as a Patreon if you find such content helpful for your investments.

There are weekly macro updates just like this, together with a full stock / REIT watchlist of names I am keen to pick up.

Why does the market see this as the Fed “Pivot”?

The popular narrative is that the Feds are responding to slowing inflation data, and slowing economic data.

So the Feds have stepped down from the original 0.75% hikes, into 0.5% hikes, and this week into 0.25% hikes.

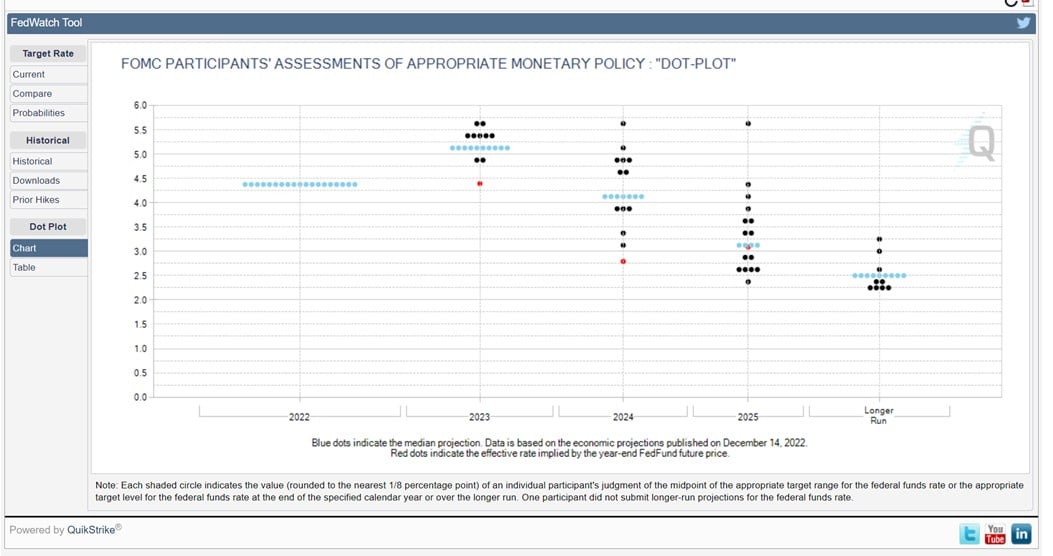

In fact the market is now only pricing in 1 more 0.25% rate hike from the Feds, to top out at 4.75% by mid 2023.

Before rate cuts in the second half of 2023:

Which for the record, is completely different from what the Feds are forecasting.

The Feds are expecting interest rates to top out at 5.0%+, and to stay there for all of 2023 before rate cuts in 2024.

Here’s the market reaction – very positive movement after the press conference, with a gap up for both the NASDAQ and S&P500.

In particular the interest rate sensitive NASDAQ (tech) has been doing very well post-FOMC.

Is a Fed Pivot the correct interpretation?

Funnily enough if you read yesterday’s transcript, it’s not so clear if Powell was so dovish.

My key takeaways on Powell’s views:

- Inflation is coming down, but too early to discuss inflation victory, or a pause in rate hikes

- Focus is on slowing the pace of rate hikes, and trying to find what is the appropriate path forward (in terms of ultimate level and duration)

- Thinks we are close to peak rates here, as policy is generally restrictive across the board

Some key snippets below.

Powell does not see rate cuts in 2023

When asked about how long he sees interest rate staying high, Powell said that he does not expect interest rate cuts in 2023:

“MR. POWELL: … if the economy performs broadly in line with those expectations, it will not be appropriate to cut rates this year, to loosen policy this year.

Of course, other people have forecasts with inflation coming down much faster; that’s a different thing. You know, if that happens, if inflation comes down much faster, you know, then we’ll be seeing that and it will be incorporated into our thinking about policy.”

Powell does not think inflation will come down so easily

When asked to comment on the difference between market pricing vs Fed expectation, he said that he was not concerned about the divergence, and sees it as due to difference in views over the path of inflation.

Ie. The market thinks that inflation will come down quickly and without fuss in 2023.

Whereas the Feds are less optimistic, and don’t see inflation coming down so quickly in 2023.

Consequently the path for interest rates in 2023, will depend very much on whether inflation comes down so quickly in 2023.

“MR. POWELL: I’m not particularly concerned about the divergence, no, because it is largely due to the market’s expectation that inflation will move down more quickly, I think…different participants have different forecasts, but generally those forecasts are for continued subdued growth, some softening in the labor market, but not a recession, not a recession, and we have inflation moving down, you know, into the—somewhere in the mid-threes or maybe lower than that this year. We’ll update that in March, but that’s what we thought in December.

Markets are past that. They show inflation coming down in some cases much quicker than that. So we’ll just have to see. And we have a different view and a different view—it’s a different forecast, really. And given our outlook, I don’t see us cutting rates this year, if our outlook turns true. As I mentioned just now, if we do see inflation coming down much more quickly, that will play into our policy setting, of course.”

Powell thinks key to inflation is the labour market

When asked to elaborate, he then explained that he doesn’t see a sustained return to 2% inflation without a balance in the labour market (which remains red hot right now):

“I would say overall, though, my own view would be that you’re not going to have a sustainable return to 2 percent inflation in that sector without a better balance in the labor market. And I don’t know what that will require in terms of increased unemployment, your question.”

BUT – Why does everyone interpret this as a “Pivot”?

So then why does everyone see this as a soft “Pivot” by Powell?

I think it ultimately comes back to his response to this question (posed to him at the press conference).

It’s important enough that I extracted it in full below.

“Q: Chris Rugaber, Associated Press. Thank you for doing this.

As you know, financial conditions have loosened since the fall with bond yields falling, which has also brought down mortgage rates and the stock market posted a solid gain in January. Does that make your job of combating inflation harder and could you see lifting rates higher than you otherwise would to offset the increase in—or to offset the easing of financial conditions?

POWELL: So it is important that overall financial conditions continue to reflect the policy restraint that we’re putting in place in order to bring inflation down to 2 percent, and, of course, financial conditions have tightened very significantly over the past year.

I would say that our focus is not on short-term moves but on sustained changes to broader financial conditions and it is our judgment that we’re not yet at a sufficiently restrictive policy stance, which is why we say that we expect ongoing hikes will be appropriate. Of course, many things affect financial conditions, not just our policy, and we will take into account overall financial conditions along with many other factors as we set policy.”

What does this mean exactly?

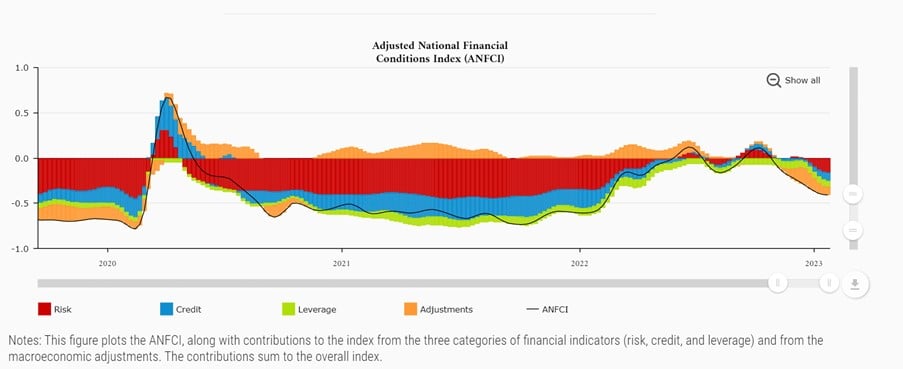

As I mentioned in last week’s article, it is very clear that financial conditions have eased since Q4 2022.

You can see this reflected in the financial conditions index below.

Yet when asked about short term financial conditions easing.

Powell chose very specifically not to push back on the easing.

But to emphasise that the Feds do not concern themselves with short-term moves but on broader financial conditions.

Effectively saying that they will NOT push back on the short term easing on financial conditions.

Is this what investing has come down to? Reading tea leaves from the Fed Chair?

Okay at this juncture I just wanted to break and make a point.

I know a lot of you may think that I am overthinking this, and spending too much time poring over FOMC minutes.

But hey – this is the game that we’re playing today.

Whether it is right or wrong is beside the point.

The fact remains that in the short term, the overwhelming driver of asset prices is the Federal Reserve.

And investing on shorter term timeframes has degenerated into a tragic game of watching the press conference and trying to figure out what Jerome Powell is trying to say.

But who’s to judge, it has been this way for the past 15 years.

Coming back to Jerome Powell

Coming back to Powell though.

Powell knows full well that financial conditions are easing.

Just look at crypto markets rebounding from lows, the flood of companies rushing to market to raise debt or equity financing, the huge rebound in stock prices.

High frequency data also shows a meaningful rebound in US home sales and car sales in January.

And if even this horse can see it, you bet that Jerome Powell knows it.

Yet when asked specifically on the issue, he chose not to push back on the easing of financial conditions.

One interpretation would be to view this as an implicit endorsement of the easing in financial conditions.

But at the very least, this is disingenuous from Powell in choosing not to push back.

So for the record, I do agree with the markets that this week should be viewed as a “soft Pivot” from the Feds.

What to buy when the Feds pivot will depend on where inflation goes after the pivot

The problem though, is that the Feds is only half of the equation.

For the first time in 40 years, inflation is the material constraint factor.

No discussion on the Fed Pivot is complete, without discussing the impact the pivot will have on inflation.

A couple of months back, I wrote for Patreons that there are 2 ways the Fed “pivot” can play out:

- Scenario 1 – Pivot too early – prioritize economic growth and pivot early. They risk getting it wrong, which means inflation comes roaring back, and Feds will get crucified for their mistake. They will lose credibility with the markets, which means more aggressive tightening down the road to address inflation when it comes back.

- Scenario 2 – Pivot too late – prioritize fighting inflation and pivot late. Wait for the economy / financial markets to get crushed before cutting rates. This way whatever happens next with inflation they are off the hook, as they already tried their best.

Of course there is a third Scenario 3 – that the Feds get the timing perfectly right and bring inflation down while avoiding a recession.

And here was what I wrote on how to invest for each scenario:

“How to invest for “Scenario 1 – Pivot too early”?

In this scenario, stocks will do very well short term when the pivot happens. But they will get crushed later on as inflation roars back with a vengeance, and the Feds are forced to hike even more aggressively to combat inflation when it comes back.

In this scenario, you could probably do a short term playbook of tech, real estate and banks (financials) to play the pivot.

But at some point in time the market will realise that an early pivot means that inflation will come back, and you will start to see long end interest rates and inflation expectations going up to price this in.

This would not be bullish for interest rate sensitive sectors like tech or real estate.

So a better play mid term in this scenario might just be to run a more inflationary playbook – Buy the new winners for this decade.

Think value stocks – energy, commodities, metals, energy services etc.

Think names like XLE (Energy ETF), XME (Metals ETF), Schlumberger (Oil services) etc.

Key buying signal is when the Feds indicate an early pivot, prioritizing growth concerns over fighting inflation.

Next signal is when the market starts to price in higher inflation, as seen from higher long term interest rates and rising inflation expectations.

How to invest for “Scenario 2 – Pivot too late”?

This will be a more classic deflationary bust.

So you play this like any big recession the past 40 years.

You short it on the way down (for those who are short – you must have proper risk management due to bear market rallies, while long only investors will stay heavy cash on the way down).

Key buying signal is when the Fed injects sufficient stimulus to offset the deleveraging (think 2008 or 2020 bottom).

At which time you run the classic recovery portfolio of long tech, real estate, banks.

In this scenario depending on whether the Feds successfully contain inflation, you may also decide to allocate some to the inflationary playbook set out above.”

That call looks spot on

For what it’s worth, the playbook I set out above looks spot on.

With Scenario 1 playing out as we speak.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Why do I see this as the Feds pivoting too early?

I set out the detailed arguments in last week’s article.

But to sum up, it is because:

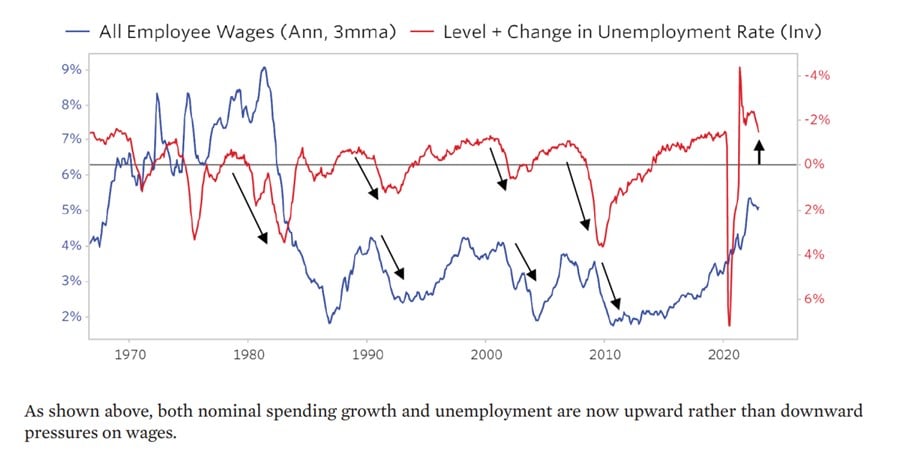

- The labour market is still too strong (wage growth is still very high)

- US GDP growth still very high

Or to put it simply – demand is still too high, relative to supply.

The labour market is not rolling over, and until labour rolls over there is unlikely to be a sustained drop in inflation.

By pivoting this early, this is a serious risk of inflation returning.

All of this was compounded by the “soft Pivot” that we had this week.

The rapidly easing financial conditions will result in a reacceleration of economic growth, and the likely reacceleration of inflation.

So what happens next?

In last week’s article, I said that the most likely path forward is a repeat of the 1970s start stop inflation.

A world in which the Feds ease (or pause) to support economic growth, resulting in a resurgence in inflation, followed by further tightening to combat inflation.

Playing out in alternating cycles until inflation is finally tamed for good.

With the events of the past week, I think the probability of that playing out just went up a whole lot.

How do you invest in this scenario?

I shared the high level playbook in the excerpt above.

Short term – interest rate sensitive classes like tech, real estate, banks.

Mid term – inflation hedges like commodities.

You want to be very careful on timing though, because once the market realises inflation is coming back and interest rates are going higher, it could get messy for interest rate sensitive assets.

Which also means another opportunity to whip out the 2022 playbook to short long duration assets.

Once you have the broad macro framework to understand how 2023 might play out – there are many ways to make money within that framework.

You can follow me on Patreon for more specific trading ideas.

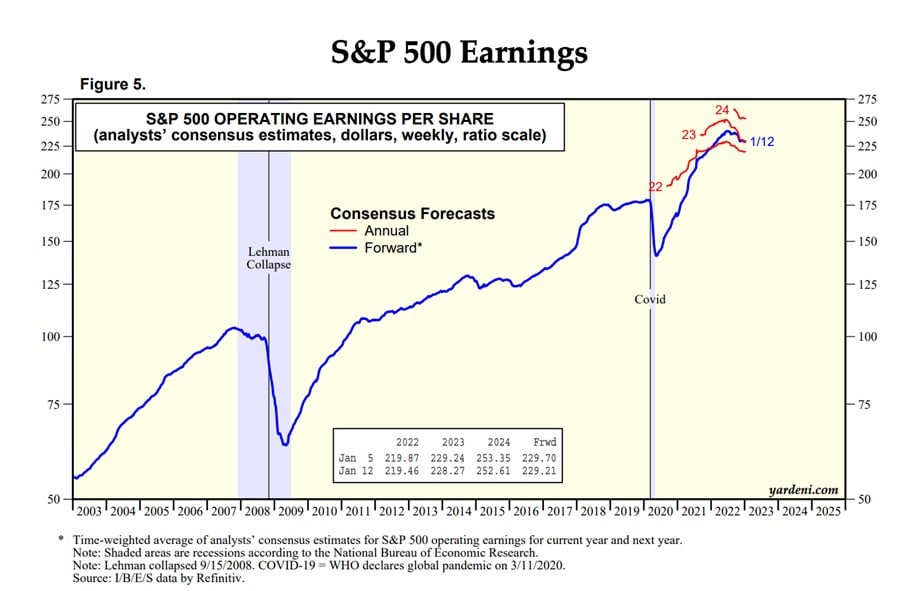

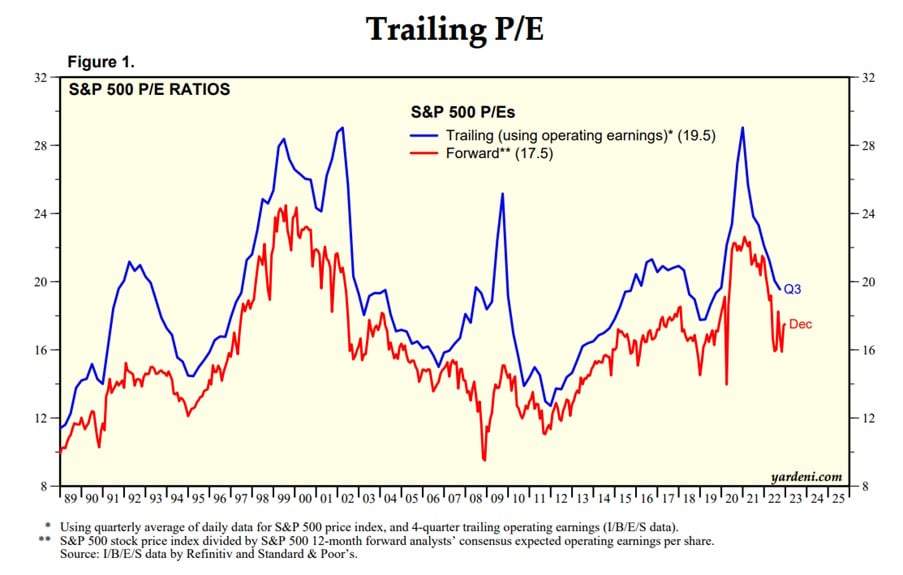

What is a fair value on the S&P500 using 2024 earnings (assuming no recession)?

What I wanted to add though, was that unlike other cycles, the starting valuations for stocks this cycle is very high.

2022 earnings for the S&P500 was $219.

With the events of this week I don’t think you’ll see a meaningful recession in 2023.

Let’s say we assume 10% earnings growth from 2022 -> 2024.

That gives us $240 earnings on the S&P500 in 2024.

Breaking that down:

A 17x P/E multiple would give you 4100 on the S&P500

A 18x P/E multiple would give you 4300 on the S&P500

A 19x P/E multiple would give you 4600 on the S&P500

How high can the S&P500 go?

The S&P500 is at 4176 currently.

Can we hit 4300?

Absolutely.

But at 4300, you’re basically valued at a 18x multiple on 2024 earnings.

And don’t forget in this new regime, you don’t get a 2023 recession, which means no interest rate cuts in 2023.

More likely you will see an even higher terminal interest rate in 2023 to respond to inflation.

So does an 18x multiple make sense in a world where terminal rates are going to 5% and beyond?

My simple view – at 4300, all your growth upside from earnings will be priced in. But none of the mid term interest rate risk.

Equity risk premium remains too low for this new regime of higher interest rates.

Closing Thoughts: Powell did have an out this week

This article is getting long, and I want to wrap up.

The final point I wanted to make, is that Powell did have an out this week.

He had an option to deliver a 0.5% rate hike when the markets were pricing in only 1% chance of that happening.

In doing so, he would have shocked the markets, meaningfully tightened financial conditions (vs expectations), and tempered animal spirits for the immediate future.

He would have showed the markets who’s boss so to speak.

Which for the record, was what Mohamed El Erian called for in quite a thoughtful piece.

But as history would have it, the Feds chose not to do it.

They chose to go with a 0.25% hike, and failed to push back on easing financial conditions.

By becoming so predictable, they are allowing animal spirits to run wild.

This will come back to haunt them

Now I’m going to put it out there that in 6 – 12 months time, you will see the events of this week as the point this cycle when the Feds lost control of the narrative.

Where they came very close to being able to regain the initiative on inflation, but decided to throw it all away.

Throwing away all the good work of 2022.

And so we start 2023, the exact same way we start 2022.

With inflation about to accelerate, and a Fed that will in time, be forced to take further measures to combat inflation.

It’s funny that for all the advances in information technology and economics the past 50 years, we look to be repeating the exact same mistake of the 1970s.

But I suppose that’s just how life works sometimes.

The players change, and the setting changes.

But human nature never changes.

Afternote: I was asked by a Patreon to elaborate on this last closing paragraph and why this could be dangerous for the markets (Feds letting the markets run to increase the possibility of a soft landing). I thought it was a great question, so I shared my responses below – hope that this provides additional colour:

I think the problem is that this is like playing with fire. Markets have been conditioned over the past 15 years to buy every dip because of the Fed Put. They know that if going gets tough, the Feds will come in to bail them out.

This is fine when inflation is at 2%, but very dangerous when inflation is at 6%. The Feds spent much of 2022 trying to convince the markets that the Fed put is gone, and they risk damaging all that good work in one fell swoop.

Assuming I am right and inflation comes back because of this easing of financial conditions, they will then need to reconvince the markets later this year that they are serious about combating inflation. Each time this plays out they lose a bit of credibility, and need to tighten even harder to convince the market.

This was exactly what happened in the 1970s with waves of inflation. Until towards the end the markets just did not believe central bankers anymore, and it took Paul Volcker hiking interest rates to kingdom come (20%) to finally break inflation.

So this is a dangerous path to go down. Inflation expectations (and long end interest rates) are currently well anchored because the market believes the Feds will control inflation. If the markets start to doubt this, then long end rates (and inflation expectations) will shoot up, and then all hell will really break loose.

I mean from an investing standpoint all this is fine because as investors we just call it as we see it and position accordingly. But a lot of these things we talk about about – interest rates, asset prices, cost of living, they have very real impact on people’s livelihoods.

Note: This is a premium Patreon article. I am releasing it to all readers given the importance of this topic.

Do sign up as a Patreon if you find such content helpful for your investments.

There are weekly macro updates just like this, together with a full stock / REIT watchlist of names I am keen to pick up.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- Sign up here and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Great analysis FH! I was expecting the Fed to push back on easing financial conditions in the latest FOMC (and positioned accordingly :/). I agree that there is a real danger of the Fed losing control of the inflation narrative. From the latest jobs report there’s no sign of the job market slowing down!

Exactly my point – 517k job print shows a labour market that is on fire right now. With a china reopen and loosening financial conditions.

Keep this up and we’ll start to see meaningful reacceleration in economic growth (and inflation)!

Thanks for releasing this article to non-Patreon members Horse. Fwiw, $219 for 2022 S&P500 earnings is consensus estimate not actual, since Q4 reporting is still under way. It’s highly likely it will be lower than that, and 2023 is likely to be even lower. So $240 for 2024 is extremely optimistic given all the leading indicators pointing to a severe recession in 2023 or 2024 (LEI, 90% of yield curves inverted etc).

Actually the point I might add is that the high frequency data is showing a pickup in economic activity. If this keeps up, and coupled with a Feds easing off the pedal, we could avoid a 2023 recession.

This means the earnings estimates above could be reasonable. BUt it is the equity risk premium would that be mispriced then, because such a scenario will call for higher interest rates.

Dear FH, even though I’m not interested to know what type of stocks to invest in in which type of scenarios, I really enjoy reading your articles, not so much for the specific content itself (even though, yes, the specific content is interesting and valuable) but more for learning from you how to think. To me, you appear to be a rigorous and thorough thinker, assessing things from various angles and scenarios. The last paragraph in your article: “I mean from an investing standpoint all this is fine because as investors we just call it as we see it and position accordingly. But a lot of these things we talk about – interest rates, asset prices, cost of living, they have very real impact on people’s livelihoods.” And I thought: Wow, not someone who coops up in his ivory tower crunching numbers to assess the economy and write about investing. But someone who also has a heart for the people who make up the economy.” Thank you for teaching me how to think….and also to have a heart!

Wow, thanks very much for this thoughtful message blur blur. It means a lot to me – truly appreciate it!

I try my best to share my thinking with the community.

Does take a lot of effort to churn out the content week after week, but I do hope that it helps others out there.

Dear FH

Thanks for this brilliant article

The way I see it, all the 11 odd sectors of the SPY are almost either fully valued or even slightly overvalued

Analyst expectations were muted to start with and this game of having beaten expectations happens each quarter ! It is a joke!

The bond markets are to be trusted and the minute the Friday jobs report came, they reacted with the ten year touching 3.5 again and the two year going higher

Yield curve inversion persists at the same depth and in fact, the not so well discussed 3 month to 10 year spread is at its highest in multi decade period of time

The markets are disregarding this for puzzling reasons except for that very basic human instinct of “ hoping for a better tomorrow “!

I consider this as a market for short term trading and erring on the side of caution with a 2:1 or 3:1 allocation favouring dividend and value : growth and tech

Though not guaranteed to work, this will limit capital erosion with some modest returns over a 12-24 month period

For SG investors, the volatile U.S. market can be used to trade and reinvest into safer dividend stocks here like OV8 KIT Banks and others like F34 S63 Etc at pullbacks, licking into 4-5% dividends that will flow in as we wait without any tax issues

Of course, currency conversion needs to be factored in but still worth it

With even modest price gains, we can eke out a 6-10% annualised return with the proceeds

The other option of fixed income is fast closing with falling rates here

Regards

Garudadri

Well what I would say is that I agree with you that this calls for a much more active strategy. This is no longer the decade of the 2010s, where buy and hold, and long SPY / QQQ / FAANG was the surest and quickest way to profit!

In fact such a strategy this decade might result in much more mundane returns.

Hi FH you are totally right. “To sum it up

The labour market is still too strong (wage growth is still very high)

US GDP growth still very high

Or to put it simply – demand is still too high, relative to supply.”

Instead, Powell, while maintaining (as he did when the Fed again hiked the federal funds rate last week) that the Fed would “probably need to do further rate increases,” also said that there should be a significant decline in inflation this year, and it was likely that inflation would fall to around the Fed’s 2 per cent target next year. US inflation was running at 6.5 per cent in December, down from 9.1 per cent in June.

https://www.morningstar.com.au/insights/markets/231543/hot-us-jobs-data-means-fed-has-further-to-go

Janet Yellen: ‘You don’t have a recession’ with unemployment at 50-year low. In this article:

https://www.msn.com/en-us/money/markets/janet-yellen-you-dont-have-a-recession-with-unemployment-at-50-year-low/ar-AA17atan

You are talking about “the pivot” reversing course in 2024. It might seem the “soft landing” is perfectly engineered. Inflation goes back down to 2%-3% in Dec 2023 with interest rates at 5% but I kinda noticed a lot of the prices of the ASX individual big names have been shed individually in 2023 and has since bounced back. What is your opinion of what is actually happening?

Well if you look at the economic data, you have a situation where economic growth is reaccelerating, while the pace of interest rate hikes is decelerating. That’s about as goldilocks as it gets for stocks, so not surprised to see a rally in stocks.

Of course, the question is how long this can continue, before inflation starts to rear its head again.

That’s not so easy a question to answer but Q2/Q3 2023 would be worth monitoring closely if this keeps up.

We must work together for my good of my plate

If you’re an individual investor, why bother following interest changes? Why not just buy the S & P or get a good mutual fund and ignore the market changes?

No I think that’s perfectly fine. Passive investors who do not want to time can just DCA.