Earlier this week I wrote a piece for Patrons discussing how to invest for the next 3 to 5 years (in a world of higher geopolitical tension).

In today’s article, I wanted to take a more short term perspective.

As a Singapore Investor – how would I be positioning my portfolio over the next 12 – 24 months?

Why 12 – 24 months?

12 – 24 months is long enough to filter out all the short term noise from market fluctuations.

Yet not long enough to focus exclusively on valuations / secular geopolitical moves.

Over a 12 – 24 month timeframe, the overriding factor you will be looking at is be the coming recession (if any).

And how the Feds will respond.

What is the stock market pricing in?

Let’s start by discussing valuations.

A lot of you have asked how to calculate what is priced into the market, so lets walk through that.

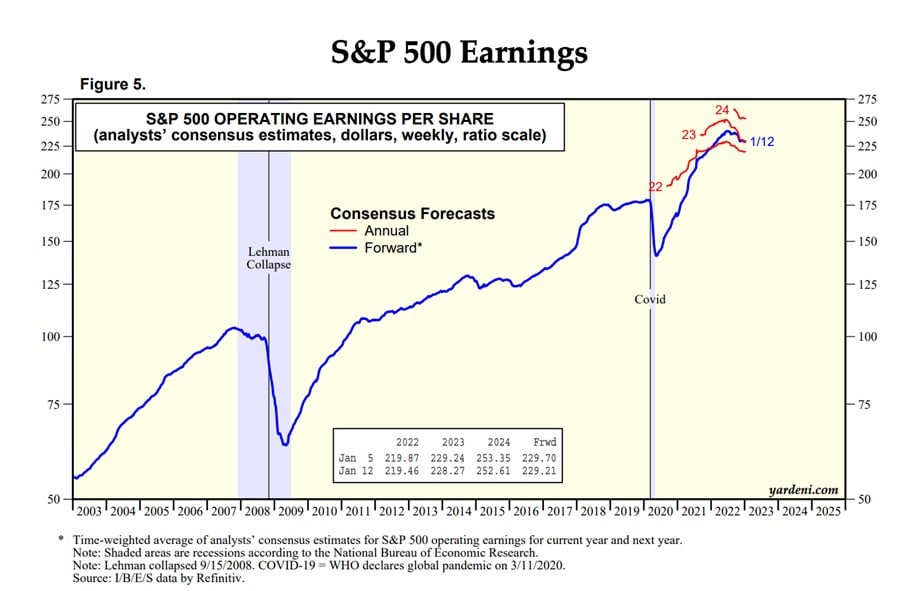

Analysts are estimating $229 earnings for the S&P500.

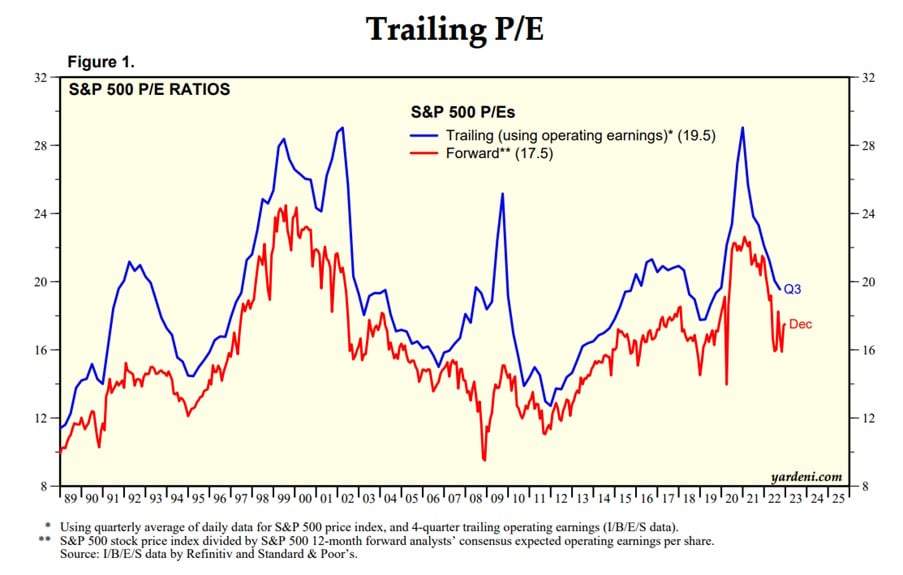

Working backwards – that works out to a 17.5x forward P/E.

Is this a realistic earnings estimate?

You can decide for yourself if the earnings estimates are realistic.

2022’s earnings was $219.

So the $229 earnings for 2023 is a 5% growth from 2022.

Now does that make sense?

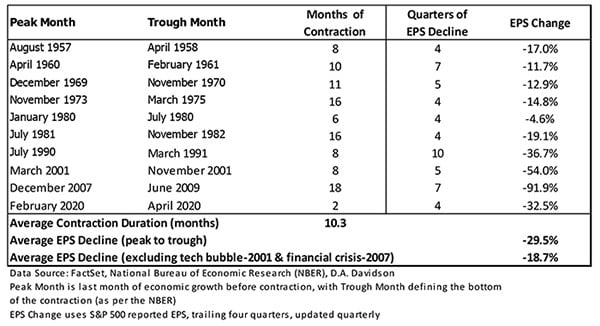

Here’s the typical earnings decline in a recession.

Over the past 40 years, the typical recession resulted in earnings declines anywhere from 20% – 90%.

But let’s be conservative and assume a 18% decline in EPS (the average excluding 2001’s tech bubble and 2008’s financial crisis).

That gives us an earnings estimate of $170 if we do get a “typical” recession.

What is a “fair” value for the S&P500 (using revised earnings)?

If we assume an 18x P/E multiple, that’s 3074 on the S&P500.

If we are generous and assume a 20x P/E multiple, that’s 3416 on the S&P500.

At current levels of 4000, that’s anywhere from a 15 – 25% drop in the S&P500.

BUT – This is just valuations

Just to be 100% clear.

I am NOT saying that the S&P500 is going to 3000.

All I am saying, is that a lot of you say that stocks have priced in a recession.

But when you actually run the numbers, you’ll find that stocks are barely even pricing in any earnings decline.

So FH… is this a bear market rally?

Unfortunately, the reality is seldom so straightforward.

I know it will be controversial, but my view is that the current rally could have legs, driven by a few key factors:

- There is a lot of money on the sidelines

- There are very meaningful technical indicators triggered from this rally

- Economic data remains red hot

1) There is a lot of money on the sidelines

There is a lot of cash on the side ready to be deployed into the market.

Normally this wouldn’t be a factor by itself.

But this matters because of the second point:

2) There are very meaningful technical indicators triggered from this rally

What is a Breadth Trust?

From Investopedia:

- The Breadth Thrust Indicator is a technical indicator which determines market momentum, signaling the start of a potential new bull market.

- The idea is based on the principle that the sudden change of money in the investment markets elevates stocks and signals increased liquidity.

Breadth Thrusts are powerful technical indicators and should not be ignored.

I’ve ignored Breadth Thrusts in the past to my own peril.

And we have quite meaningful breadth thrusts that triggered earlier this month.

Coupled with all the cash on the sidelines, this could result in a lot of cash coming into the markets in the weeks ahead.

3) Economic data remains red hot

This is backed up by economic data.

The labour market is red hot – employee wage growth is still growing very strongly:

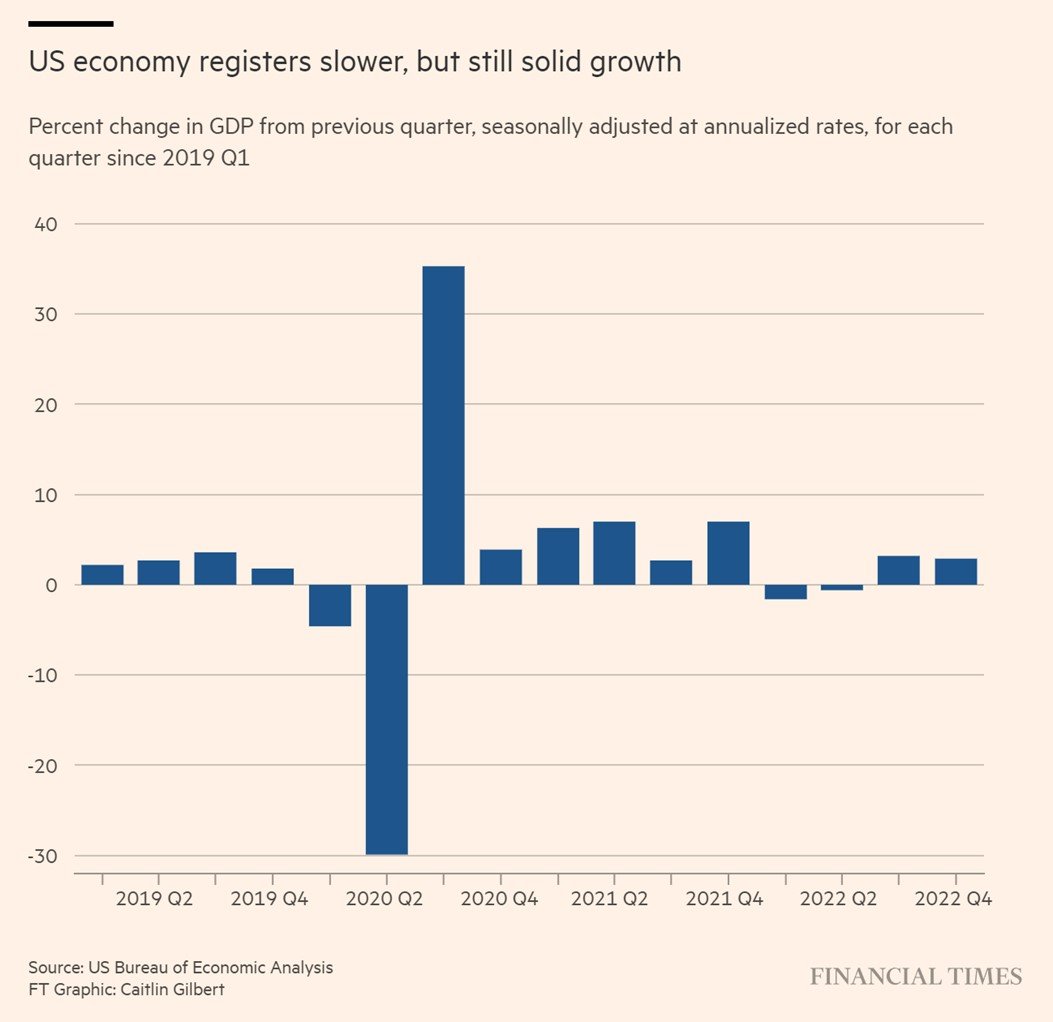

Aand US GDP growth for Q4 came in at 2.9% (firmly in growth).

All while consumer spending is holding up very well.

FH… what are you trying to say?

I suppose what I’m trying to say.

Is that yes – the market is not pricing in any earnings declines.

But if you look at the economic data, you’ll be hard pressed to find any data showing an imminent recession.

In fact the story seems to be that after the fastest rate hike cycle in 25 years and with 4.0% of rate hikes behind us – GDP growth barely ticked down from 3.2% to 2.9%.

All while financial conditions are loosening, liquidity is expanding, China is reopening, and consumer spending and labour markets are still strong.

Commentators expecting the stock market to collapse 20%.

Or calling for Feds to cut interest rates in second half of 2023.

That just doesn’t make sense when you look at the economic data coming in, which remains red hot.

In the markets, being early, is as good as being wrong.

To put it very simply – in the immediate short term, this rally could have legs.

Until the market resolves this either way, it’s not a good time to be short.

And if you are long, just let it play out, and consider locking in profits at some point.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Will there be a recession in 2023 / 2024?

But now let’s look forward a bit more.

Over the next 12 – 24 months, are we going to see a recession at some point?

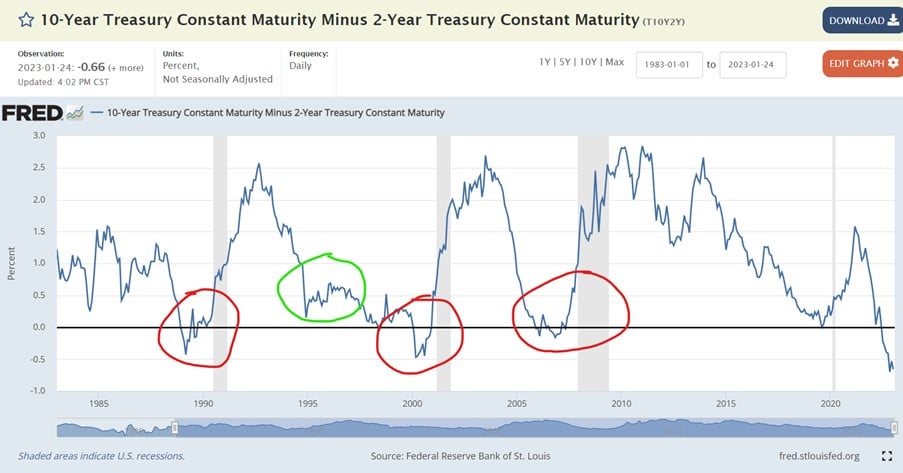

Here’s what the bond market is telling us (which I shared on Twitter this week – do follow me if you haven’t already).

This is the 2s10s yield curve going back into the 1980s.

Every single fed hiking cycle the past 40 years has resulted in a recession (red circled area).

Only exception is 1994 – circled in green.

What does the bond market tell us?

First – the 2s10s yield curve inverts before every recession (red circle).

Where it does not invert (green circle), the market avoided a recession and achieved a “soft landing”.

2s10s is deeply inverted today – Showing that market expects a recession to come eventually.

Second – the 2s10s will steepen sharply about 2 to 6 months before a recession (red circle).

But 2s10s have not steepened sharply yet – Showing that the market does not see a recession as imminent.

Which I suppose is in line with the analysis above.

In plain English – bond markets think a recession will come at some point in the future, but not so soon…

Financial Conditions have eased meaningfully – The Feds are caught between a rock and a hard place

But look beyond the immediate term though, and you start seeing deeper problems on the horizon.

Namely – this easing of financial conditions unwinds a lot of the good work the Feds have put in to combat inflation.

You can see this below, where financial conditions have loosened noticeably in Q4 2022.

Now monetary policy works with a bit of a lag.

With financial conditions easing in Q4 2022, you might only start to see the effects in say – Q2 to Q3 2023.

Just when the Feds are about to pause on their rate hikes.

What then if inflation comes back?

Let’s say it’s mid 2023, and inflation goes back up on a month on month basis – what next?

Do the Feds (a) continue to pause rate hikes but keep rates up for longer, or (b) raise interest rates beyond 5%?

Or do they still cut interest rates like the market is expecting?

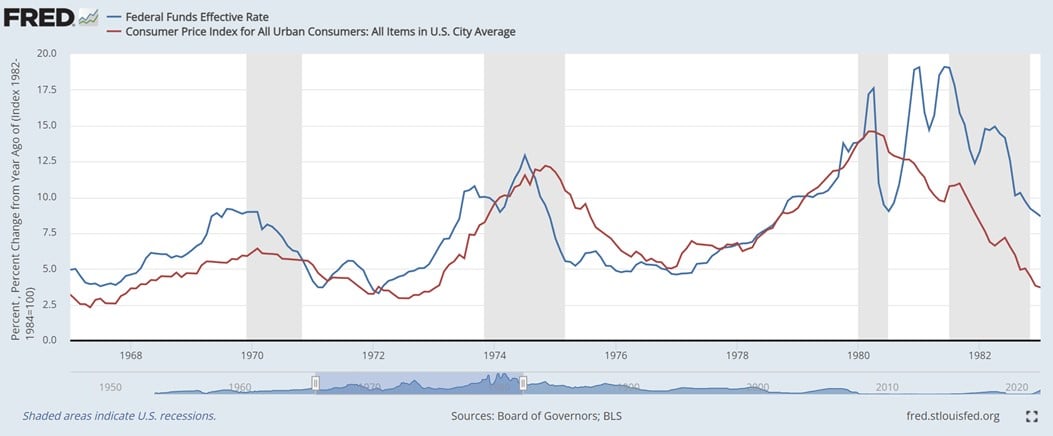

It’s very tricky – which by the way, was the exact same mistake made by Arthur Burns in the 1970s, when he eased monetary policy too early.

This resulted in a decade of start-stop inflation in the 1970s.

You can see this mistake below – where the Feds raised interest rates and inflation came down, but then they cut rates and inflation came back.

This played out over 10 – 15 years during the 1970s, with inflation coming back more viciously each time, requiring ever more drastic monetary policy.

A mistake that Jerome Powell is so desperate to avoid by invoking the legacy of Paul Volcker.

In case you’re wondering – this was the S&P500’s performance during that decade.

Stock prices kept going lower and lower for 10 years – and never really recovered until inflation was solved for good.

And really – I think this is probably the biggest thing you need to worry about right now.

If this loosening in financial conditions continues.

And stocks continue their march up.

And the Feds don’t do anything more to contain inflation.

I would be really worried of a repeat of the 1970s style of start stop inflation.

Don’t believe me?

Take it from Bridgewater (emphasis mine):

Going forward, the policy choices will be far more challenging when the goals of full employment and stable prices are at odds and the contraction in employment has not been sustained for long enough to bring down wage growth. For most central banks, at that stage there is a tendency to pause and see how things transpire.

Such a pause tends to give markets a celebratory reprieve, producing a period of very good asset returns and a pickup in growth, both of which conspire to prevent wages and inflation from settling at the desired level, which necessitates the next round of tightening.

A near-term economic downturn, an extended period of above-target inflation, and a second round of tightening are not discounted in the markets at all.

What the markets are now discounting is that the first round of tightening is nearly over, that growth will not slow much and yet inflation will quickly fall to desired levels and that this will allow a cut in interest rates in 2023 and 2024 that restores a normal risk premium in bonds. There is a lot of room for markets to be blindsided by what we see as the normal sequence of events which typically follows the conditions that exist today.

Update: 3 possible ways I see this playing out

Organised in what I see (for now) as the most likely outcomes:

- A repeat of the 1970s start stop inflation

- A deep and sustained recession that ends inflation for good

- A soft landing – inflation comes down to 2% without a deep recession

A quick note on each of them.

1. A repeat of the 1970s start stop inflation

This is basically the 1970s style scenario discussed above.

Inflation comes down, the Feds ease (or pause), inflation comes back, the feds tighten.

An extended period where monetary policy switches between tightening to bring down inflation and easing (or pausing) to support growth.

The way things are shaping up with the Fed Pause and the huge rally in risk assets, I think this might be the highest probability outcome for now.

In the 1970s it resulted in 3 different rate hiking cycles before finally taming inflation.

I’m not saying it repeats exactly the same way as the 1970s, I’m saying to be alive to the risk that inflation could have multiple peaks, and multiple tightening cycles to combat inflation.

2. A deep and sustained recession that ends inflation for good

The next possibility is for a deep and sustained recession that is sufficient to end inflation for good.

This was done by Germany in the 1970s, but the amount of pain required is high, and I’m not sure if today’s central banks have the stomach to persevere with this route.

Hence it’s the second most likely outcome.

3. A soft landing – inflation comes down to 2% without a deep recession

The third outcome is what risk assets seem to be pricing in.

Inflation coming all the way down to 2% without a deep and sustained recession.

Looking at the economic data, I think this is the lowest probability outcome of the three.

The key reason being that the economy is running too hot for this to be realistic.

Had the Feds starting hiking in 2021, this might have been possible.

Unfortunately they waited until 2022 – by which time the starting position for the economy was too hot to bring inflation down without something big, because the gap between demand and supply was already too big by that point in time.

You see this right now – after 4% of rate hikes in the fastest hiking cycle for 25 years – and economic growth remains strong, consumer spending remains strong, and the labour market remains tight.

I don’t want to say that the Feds are f***ed, but the options sure don’t look good here.

For inflation to come down to 2% for an extended period of time will require a meaningful decline in demand, and a meaningful weakening in the labour market.

I just dont think you can achieve it without a prolonged recession.

Which is why for now, I see Scenario 1 as the highest probability outcome.

Which would be a real nightmare for investors, and a real tough one to trade.

How I will invest my money in 2023?

For the record, I think this is one of the hardest markets to invest in in a long time.

Look at the discussion above, and you realise one possible path is for a vicious short term rally, followed by a second peak for inflation, followed by tighter monetary policy and a decline in stocks.

I mean… what a mess, and trying to time it perfectly is not going to be easy to say the least.

My views on the markets?

The main problem with going long now (if you plan to hold for the mid term instead of just trading), is that stocks are not pricing in any meaningful earnings declines.

They are pricing in a soft landing.

Which means that if we do indeed get a soft landing, how much upside is there?

Whereas if we don’t get a soft landing, how much downside is there?

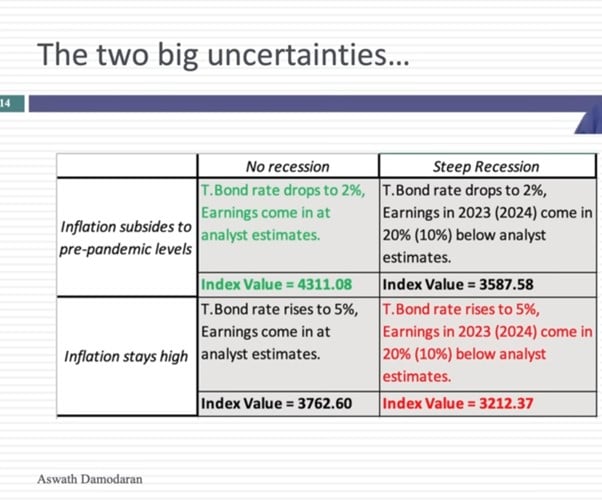

NYU Corporate Finance Professor Aswath Damodaran charts out the fair value on the S&P500 on the various scenarios below.

You may not agree with the exact numbers (I probably don’t myself), but the direction is clear.

Best case you’re looking at limited upside in a soft landing.

But there’s a fair bit of downside if we don’t get the soft landing the market is pricing in.

How I am investing my own money?

I’ve been writing to Patrons that while 2022 was a year of top down macro investing.

2023 is starting to look a lot like a year of bottom up stock picking.

The analysis above applies for the index generally.

But if you look through that into individual stocks, there are many pockets of opportunities to buy / sell.

Take REITs for example.

A blue chip like CICT trades at a sub 5% yield after the recent rally.

I mean I don’t know where the market is headed exactly over the next 12 months.

But I know that if someone is going to buy CICT from me at a sub 5% yield when the global risk free is going to 5% and beyond – I’m probably going to sell to them.

At the same time, a lot of the smaller oil services players are still trading at close to equipment replacement cost.

Some of the commodities names have come down a fair bit from their peaks too.

If we are moving into a period of higher structural inflation and demand/supply imbalance for commodities – this is going to require massive investment into new commodities supply.

You can check out my full stock watch on Patreon if you’re keen, will be updating it this weekend.

General Positioning?

As a general rule, I would think to avoid the previous decade’s market leaders for now.

At least until the inflation / interest rate picture clears up.

Anything long duration like crypto, tech, REITs, long duration government bonds (>10 years) – I think you use those mainly as trading positions for now.

Flip it for a profit, don’t get too married to your positions.

And focus your long positions more on the secular winners for this decade – commodities, industrials, cyclicals.

And cash, given the ridiculously high risk free yields you’re getting now.

Asset allocation wise, I discussed a possible 20/40/20/20 earlier this week for Patreons – 20 cash, 40 stocks, 20 commodities, 20 bonds.

That could be an appropriate starting point to build around.

You can sign up as a Patreon if you’re keen, where I share my personal stock watch and weekly macro updates like this one.

Cash is not a bad idea if you are out of ideas

What I would add though, is that with the current inverted yield curve (short term yields higher than long term yields), cash is not such a bad idea.

With cash you’re getting 4%+ risk free on a 6 month T-Bills.

You take no duration risk because whichever way interest rates go, you can just hold the T-Bills to maturity with no capital losses.

And cash gives you optionality – to buy into the market if there is a decline.

That optionality alone has a value.

Sure, cash doesn’t work long term because it will underperform inflation longer term, but for as long as the yield curve is inverted (like right now), higher cash allocations can still make sense.

Have stocks bottomed?

Coming back to this question – I think it really depends on your timeframe.

With a breadth thrust, meaningful momentum signals across the board, and a ton of money on the sidelines this rally could have legs (short term).

I would not be surprised to see this rally continue to run.

But a meaningful rally would create other problems – in that loosening financial conditions will result in a growth recovery, and a resurgence of inflation.

Which could require the Feds to raise interest rates even higher, or keep them there even longer.

So if the market goes up in the short term, it means it will probably have to go down in the mid term.

If it goes down in the short term, then maybe it can go up in the mid term.

Markets are funny like that.

Closing Thoughts: Markets are a game of poker, not chess

One final point I would want to make, is that this discussion above is using a 12 – 24 month timeframe.

If you’re a decades long investor, then frankly just ignore all the short term fluctuations as noise and continue your dollar cost averaging.

But investors who want to market time, should at least have a view on the points I raised above.

And what I want to emphasise again – is that market timing is a game of poker, not chess.

Just like poker, no player has perfect information of the future.

At any point in time, you’re betting based on how much you stand to win, vs how much you stand to lose (risk-reward).

You’re betting based on your probabilities of win.

And perhaps more importantly, you’re betting based on what you think other investors are thinking.

When the facts change, don’t be afraid to change your mind

And just like poker, when the next card opens and you probabilities of winning change, don’t be afraid to change your positioning.

Don’t be afraid to change your mind.

Poker is a game where even the best players only win 60% of their hands. This is not chess where the best players win 100% of the time against weak players.

So a healthy dose of humility is in order.

Whatever you think you know, think again.

And don’t forget – the best players know when to bet big, and when to bet small.

And when to not bet at all.

As always, this article is written on 28 Jan 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Agree with cash bring a good option 🙂

Can’t say I disagree 😉

Hi FH,

Could you explain what do u mean when you mention financial conditions loosening ?

I like to reach out to you , can u tell me where do I go to like email ?

Thanks

Yau

Financial conditions basically indicate how tight money is – and how hard it is to raise financing.

A loosening would indicate that it has become easier to raise money of late, which you are starting to see being reflected in the economy and asset prices.

Sure – you can leave a comment here, or drop me an email at [email protected] if the matter is private.

Dear FH

Thanks once again for a lovely article that is very relevant to investors at this critical juncture

I fully agree with what you have written and the possibility of this being a up down situation that will go on

The fed will struggle as china reopening, oil surge and persistent wage and service sector inflation will be tough to tame

The current market valuations already appear stretched as far as growth names are concerned and money is rapidly surging into tech and growth from the “safe” consumer staples, health care and utility sector

The staples, some of which are safe and dividend growing blue chips, are already down 5-12% YTD

Good quality healthcare- ideal for long term investment, is also falling

Utilities, the bond proxies, are slowly falling as a response to the perceived Fed put plus money piling into “risk-free” fixed income

To me, this is the time to accumulate long positions in XLV XLP XLU or market leaders from these sectors and wait

This will have two advantages

– Limits downside if markets correct and to an extent protects capital

~ Rock solid dividends help and relatively recession proof earnings

I have padded up my portfolio over the recent months this way

As regards the local market, you might recall my contrarian post in response to your article in autumn 2022

I invested heavily in good SG REITS and intend to hold on

Locked in 6% plus yields plus they are all up 10-20%

I know that they might drop if rates go higher and or stay higher but I will be compensated for that by dividends

The local market is surging and I might take profits to raise cash levels

Difficult but doable

Prof Aswath’s valuations are reasonable and can be applied

As rates peak, global investors sense that fixed income yields might start dropping and there is so much liquidity here

Every decline will be bought into and therefore selling out and staying in cash is certainly not an option

I am still in 5-10% liquid cash though and will certainly buy declines

Regards

Garudadri

Hi Garudadri,

Thanks for a lovely comment yet again.

I must commend you on taking a contrarian position and buying REITs in late 2022. That move looks to have paid off very well indeed!

Broadly agree with your points frankly. A few points I would add:

1. I was actually inclined to use the current rally to take profit in some of my REIT positions. CICT for eg. is my biggest holding, and at a sub 5% yield it’s looking very fully valued to me. Might be looking to trim my position. That said, it’s probably a difference in approach. With that prices that you likely bought at, I can see why you would want to just hold instead of trying to trade the short term movements.

2. On buying the dip – yes I agree with you in the mid term that staying in cash is not an option. I also agree that with current positioning and momentum triggers, buying pressure could be very strong and propel this market up short term. It’s the interim period between the short and mid term, say 6 – 12 months, that I’m a bit more worried about. With current loosening in financial conditions and the strong asset price rally, growth will surely recover, and with such a tight labour market, inflation may pick up as well. A powerful headwind for inflation in late 2022 was declining gas prices, and that is slowly reversing.

Market pricing looks a bit too optimistic on the path for inflation (and rate cuts) going forward. I see potential for the market to be blindsided by the development on inflation and interest rates in the short-mid term.

Mr Horse, informative article and its good to reassess the macro every few months to get a bearing.

You had done an article on commodities in November.

Would you suggest beginners to use some ETF(s) to get exposure to commodities instead of direct trading in them?

For example XLE for energy (which seems to be very high priced currently).

MOO, GNR etc?

Thanks for the kind words Raul.

I think it really depends on the individual investors.

For those who want to play broad macro trends, and dont want individual stock risk – ETFs are perfectly fine. But more active stock pickers may want to pick individual names for higher risk-reward, at the expense of individual stock risk, and more effort + research. Even more sophisticated investors may consider buying commodities futures directly.

So it really depends, all are viable approaches.

Dear FH,

Interesting analysis as always. What I don’t like about holding a lot of cash is that even with fixed interest rates of 4%, you are getting less than the level of inflation so your purchasing power is guaranteed to shrink.

There are many stocks out there with +6% dividend, which gives you an inflation-beating yield and some prospect of capital appreciation over the medium term. I am thinking that may be a better medium term investment.

Haha just to be clear I’m not saying don’t buy a 6% yielding dividend stock.

I’m just sharing a macro framework for how I think the next 12 – 24 months may play out, and where inflation (and consequently interest rates) may go.

What investors choose to do with that framework, I leave it up to the individual investor.

I dont disagree that cash will not sufficiently hedge inflation over the mid term!