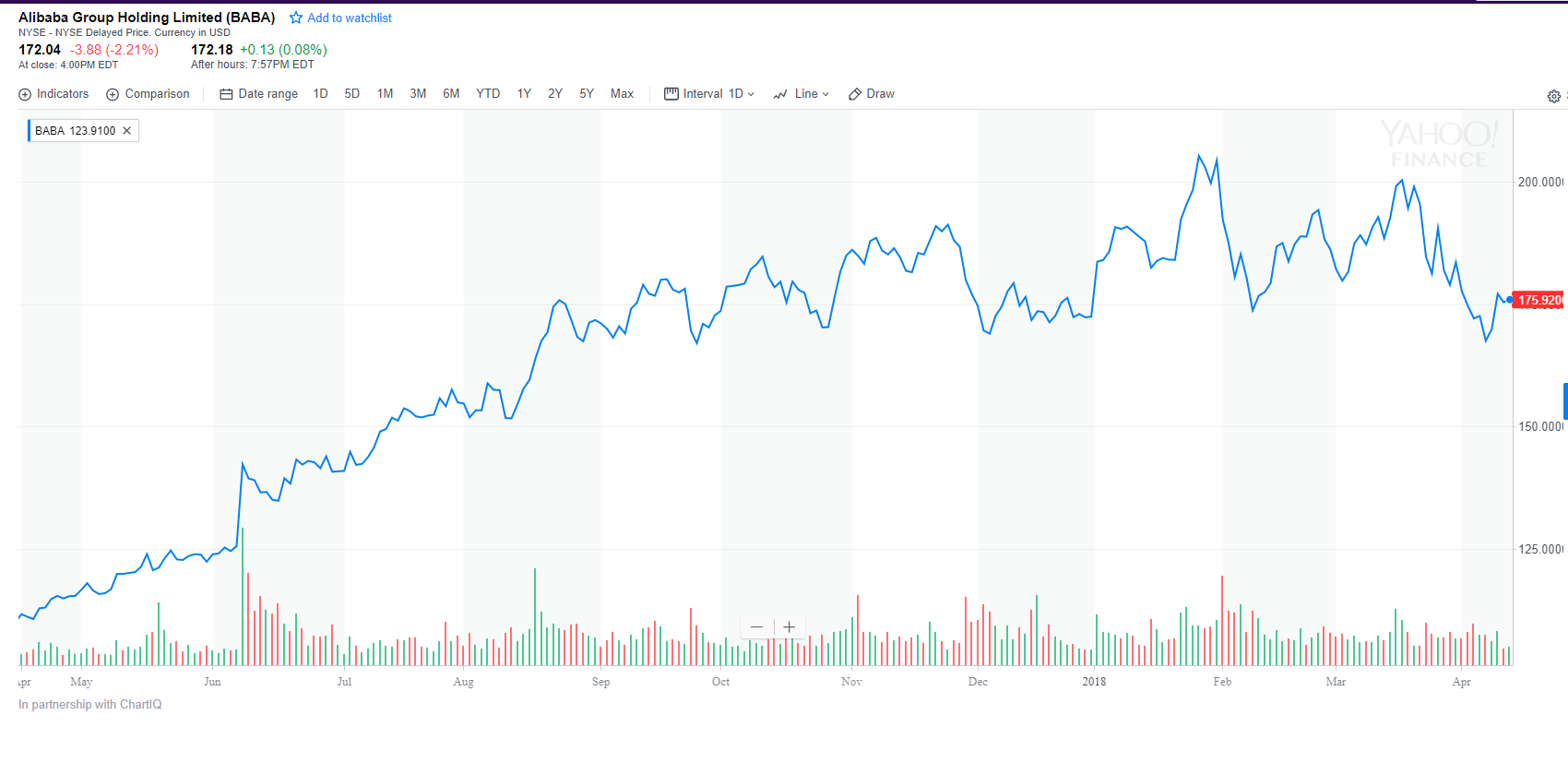

As at 13 April 2018, Alibaba Group Holding Limited (NYSE: BABA) closed at USD 172.04, which is 42 times trailing twelve month (TTM) P/E and approximately 26 times forward P/E. It’s had an amazing run-up from USD 110 12 months ago, but as the 12 month chart below shows, the price has been stagnating since about September last year. Comparatively, Amazon has gained about 42% in the same time period.

I’ve long been a fan of Jack Ma’s Alibaba, and I absolutely love the long term growth prospects of China and South East Asia. I decided to take a closer look at this E-Commerce juggernaut, to determine if I should be putting some of my hard earned money into this China company.

Basics: Alibaba Group Holdings

From Wikipedia:

Alibaba Group Holding Limited (阿里巴巴集团控股有限公司) is a Chinese multinational e-commerce, retail, Internet, AI and technology conglomerate founded in 1999 that provides consumer-to-consumer, business-to-consumer and business-to-business sales services via web portals, as well as electronic payment services, shopping search engines and cloud computing services. It owns and operates a diverse array of businesses around the world in numerous sectors, and is named as one of the world’s most admired companies by Fortune.

In other words, Alibaba is Asia’s answer to Amazon. In their home markets, these guys are absolute juggernauts that dominate Ecommerce and bully competitors into submission. Their solution to competition is to buy you out at a ridiculous valuation, or if you foolishly turn down the offer, they will pour limitless amounts of cash into your closest competitor.

Jack Ma has been very active in romanticising the company recently, tracing from to its historical roots when they were fighting e-bay in China, to its current role in modernising China. But don’t be fooled, at its core this is a company of alligators (to reference a popular quote from Jack Ma himself), with a relentless focus on profits and the bottom line.

What I like

Demographics of retail in Asia

I am a firm believer that this century will be the rise of China. China’s 1.3 billion population alone is equivalent to almost double the entire combined population of Europe and America. And unlike Europe, China is largely a homogeneous country which speaks the same language, and united under the same political banner (Xi Jinping).

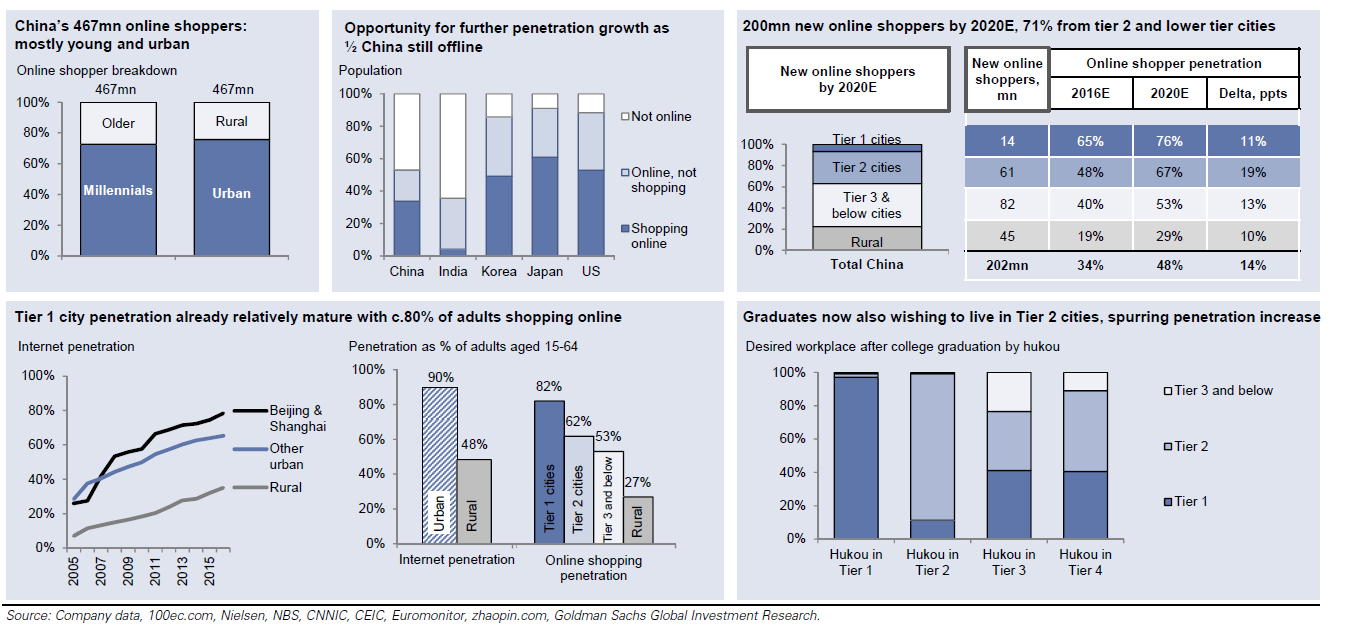

Goldman Sachs has a great report here that sets out the bull case for Ecommerce in China. It’s interesting enough to skim through it, but I’ve summarised the key arguments (and charts below).

200 million new online shoppers by 2020 from lower tier cities – China’s Ecommerce penetration still has room to grow. While the first wave of Ecommerce arose from millennials in Tier 1 cities, the next wave will come from lower tier cities. This is estimated to add 200 million new online shoppers by 2020. As a benchmark, 200 million shoppers is more than half the entire population of the US.

China Ecommerce to double in size to become a US$1.7 trillion market by 2020. China’s Ecommerce is still in its infancy, and less saturated than other mature markets like US and Europe. The new growth will come from greater penetration into lower tier cities, and greater penetration within existing categories of merchandise (such as electronics and appliances). At the same time, China as a market is growing, and consumers are becoming wealthier, which grows the pie for everyone.

The bottom line is that barring a major economic crisis in China, no one is really disputing the growth of Ecommerce in China. In fact, I am bullish enough on China to say that an economic crisis will only delay the inevitable. This century is the rise of China, and the Chinese consumer will prove its dominance in the decades to come.

The more important question however, is what is Alibaba’s place in this Ecommerce pie?

Alibaba owns everything

The recent moves made by Alibaba since their 2014 IPO have been interesting. They have been investing in almost every single promising China and South East Asian startup. I know many friends who have advised Alibaba (or been across the negotiating table from Alibaba) in such acquisitions, and they always tell a story of an aggressive and shrewd dealmaker. Alibaba executives would offer you a generous valuation with a simple catch, if you don’t take the offer, we make the same offer to your competitor. This leaves the young CEO with a hard decision, take Alibaba’s money, or fight an Alibaba funded competitor. There is no choice really.

Which is really interesting, because these moves have positioned Alibaba as a tech juggernaut/hedge fund, with a finger in every pie.

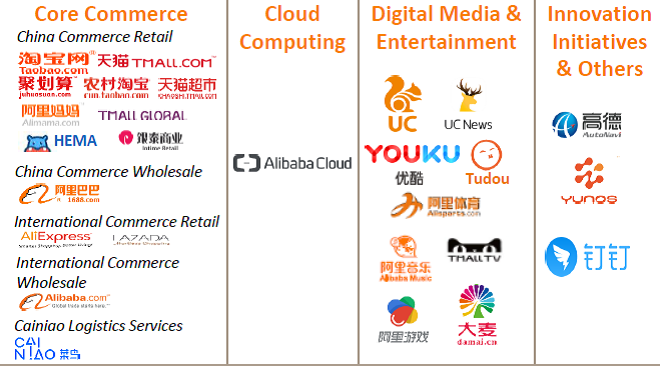

I’ve extracted the bigger businesses below, but broadly, what I am highly interested in are Alibaba’s stakes in:

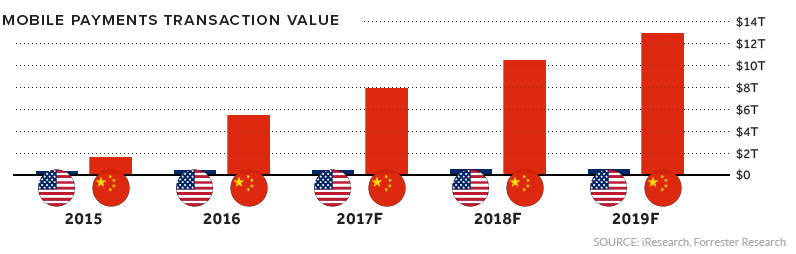

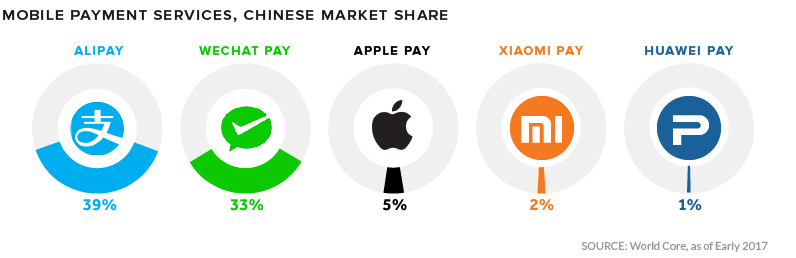

33% of Ant Financial – This is the crown jewel, with a latest valuation of US$150 billion. It controls about 40% of the China mobile payment market, and I don’t need to tell you how valuable that is. Take a trip down to Beijing these days, and you will realise that cash is the exception rather than the norm. If this can proliferate to the lower tier cities, a US$150 billion price for Ant Financial is going to look like an absolute bargain. Alibaba’s stake in Alipay itself can take up an entire article. I won’t dwell on this too much, but I will leave you with a chart below on the potential of cashless payment in China.

83% stake in Lazada –South East Asian Ecommerce platform, that I am sure all Singaporeans will be familiar with.

100% stake in Ele.me – Food delivery service, formed after a merger between Alibaba backed Ele.me and Baidu Waimai. It has about 50% market share, with the second largest player being Meituan Dianping at about 40% market share. It’s the China version of Deliveroo, but so much more robust (with review functions etc).

100% stake in homegrown Alicloud – Personally I feel that AliCloud is the dark horse in Alibaba’s stable. Amazon Cloud has shown that there is massive potential for cloud services, and this industry is only in its infancy. The growth numbers for AliCloud are through the roof (100% YOY increase), and I am keeping a close eye on this space.

100% stake in Youku Tudou – China’s YouTube, ‘nuff said

Taobao/Tmall – And of course, not forgetting, its core business, Taobao/Tmall.

And this is just the tip of the iceberg. There is a stake in Hema (a new concept supermarket), AutoNavi (GPS navigation, rumoured to transition into self-driving), Alibaba Music (streaming), Alibaba Mybank (micro-lending service leveraging on data anlytics) etc. Many of these companies are dominant in their own right, and parked under the Alibaba umbrella, they enjoy ridiculous synergies, and the benefits from data analytics are insane. Don’t forget, this is China where the boundaries over use of personal data are different for now.

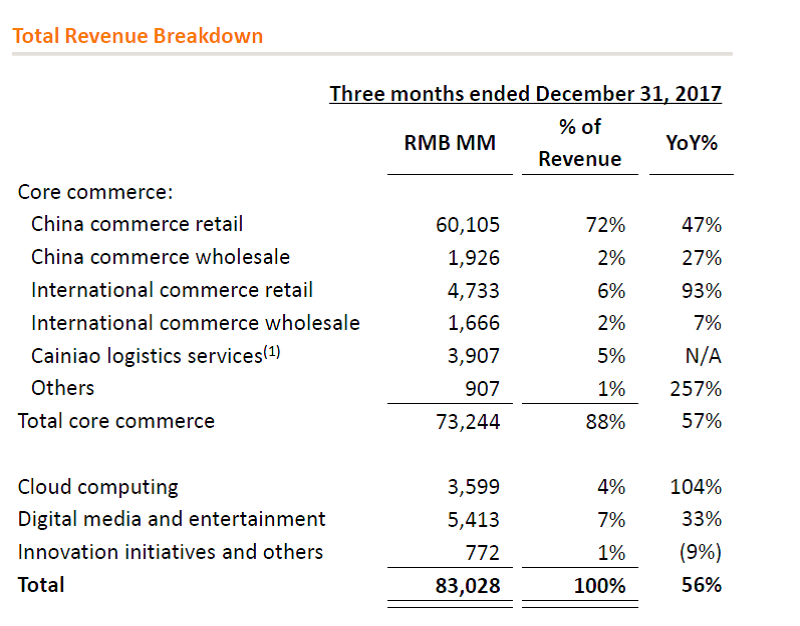

Source: Alibaba Financial Results

I really like how Alibaba has positioned themselves as a technology hedge fund, vacuuming up startups. I see this as having multiple benefits:

Combat potential competition – This is China, where if you are not careful, a competitor can spring up overnight and destroy your business model within 12 months. By actively taking up stakes in startups, Alibaba is not only keeping themselves well appraised of the startup environment in China (by being very close to the ground), it also allows them to take up a stake and monitor the progress of any competitor, before they become too large.

Data Analytics – By owning a large stable of startups and corresponding userbase, it allows cross sharing of information between apps, to generate a holistic profile of a consumer. This can be used for better ad-targeting on taobao, or better credit scores on a lending service such as Alibaba Mybank. Data is the new currency of our generation, and he who controls data will control the future. All the big players such as Tencent, Google, Facebook are rushing to grab user data in anticipation for this upcoming arms race.

One of these could grow into the next unicorn – Don’t forget that these are hungry startups. You never know which may grow into the next Tencent or Alibaba. By buying into them early, Alibaba is setting themselves up for huge potential returns if one of these grows into a unicorn. This is already paying dividends with the likes of Ele.me.

Valuation

I’ve set out a comparison of Alibaba’s valuations against its Chinese counterparts Tencent and Baidu, and the American FAANG stocks.

It’s incredibly hard to compare these companies, because each operates in a slightly difference technology niche, with very different characteristics.

My personal thoughts are that Alibaba is trading in line with its peers. But the problem with comparing valuations is that this is ultimately beyond your control. I prefer to understand the fundamentals of a company and where its future revenue is coming from, and invest on a multi-decade basis. As the saying goes, in the short run, the market is a voting system, in the long run, it is a weighing scale.

| Alibaba | Amazon | Tencent | Baidu | Apple | Netflix | |||

| Market Cap (intraday) | 452.92B | 701.4B | 496B | 80.35B | 722.9B | 886.43B | 478.42B | 134.61B |

| Enterprise Value | 419.32B | 693.44B | N/A | 66.13B | 631.52B | 899.61B | 417.08B | 129.02B |

| Trailing P/E | 43.35 | 235.59 | 45.36 | 27.75 | 57.66 | 18.01 | 30.55 | 248.16 |

| Forward P/E | 26.71 | 94.14 | N/A | 20.00 | 21.40 | 13.34 | 18.76 | 72.65 |

| PEG Ratio (5 yr expected) | 40.79 | 8.38 | N/A | 57.54 | 1.00 | 1.14 | 0.83 | 1.51 |

| Price/Sales (ttm) | 12.58 | 3.94 | 103.78 | 5.97 | 6.52 | 3.71 | 11.77 | 11.51 |

| Price/Book (mrq) | 8.16 | 25.31 | N/A | 4.39 | 4.73 | 6.33 | 6.43 | 37.53 |

| Enterprise Value/Revenue | 11.65 | 3.90 | N/A | 4.91 | 5.70 | 3.76 | 10.26 | 11.03 |

| Enterprise Value/EBITDA | 29.55 | 46.11 | N/A | 15.19 | 17.65 | 12.13 | 17.96 | 141.69 |

Profitability

| Profit Margin | 29.56% | 1.70% | N/A | 21.58% | 11.42% | 21.13% | 39.20% | 4.78% |

| Operating Margin (ttm) | 31.28% | 2.31% | N/A | 18.50% | 26.05% | 26.87% | 49.70% | 7.17% |

Management Effectiveness

| Return on Assets (ttm) | 7.38% | 2.39% | N/A | 4.52% | 9.90% | 10.89% | 16.89% | 3.22% |

| Return on Equity (ttm) | 17.63% | 12.91% | N/A | 16.03% | 8.69% | 37.07% | 23.86% | 17.85% |

Source: Yahoo Finance

Core business

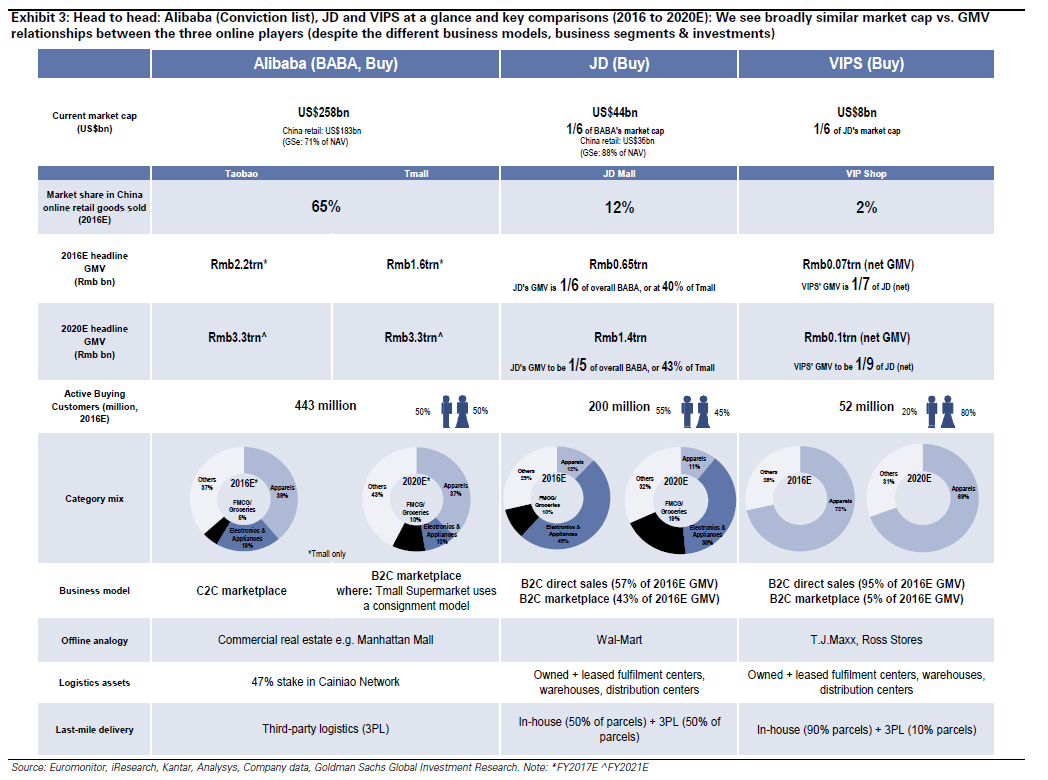

In this entire analysis so far, I have not touched on Alibaba’s dominance within its core market, China Ecommerce. To me, Alibaba has reached a point that its dominance has allowed it to enjoy huge economies of scale, brand recognition, and strong pre-existing supplier relationships that are hard to disrupt. It’s closest competitor, JD.com, has a 12% market share versus Alibaba’s 65%. Of course, all these can slowly be eroded away by poor decisions from Alibaba’s part, but so far I don’t see this happening.

What I see is a lean and mean management team, who is not content with what they’ve built so far, and are hungry for further success. Jack Ma has done a great job in building himself into a personality cult, which is good because all great companies need a larger than life personality to rally around. Apple had Steve Jobs, Tesla has Elon Musk, Facebook has Mark Zuckerberg, Virgin has Richard Branson, Alibaba has Jack Ma. Never underestimate the power of a strong personality to attract investors and deter competition.

The fact that Lucy Peng (one of the original 18 co-founders and trusted Jack Ma lieutenant) gave up an executive chair role in Alipay to become Lazada CEO also speaks volumes to me. This is a management team who is not content to rest on their laurels. They are willing to take risks and make personal sacrifice to conquer new markets. All companies reach a point where the core management team tires and looks to consolidate their existing position. Alibaba is not there yet.

Tail Risks

Funnily enough, when compiling the list of tail risks to Alibaba, the list actually starting going into double digits. I’ve cut it down for this article, but the point is this: At the end of the day, this is China.

Opaque financial statements

I strongly recommend readers to take a look at the attack by Deep Throat IPO, which was endorsed by famous short seller Muddy Waters (they were responsible for taking down Noble). It alleges opaque financial statements, financial engineering, and a whole host of other China related problems.

I agree with them totally. My personal view is that at the end of the day, this is a China company. China companies do not have the same history with corporate governance and capital markets disclosures that US investors and US companies are accustomed to. China will get there eventually, but in the meantime, this is what you are going to get. I don’t necessarily see this as intentional obfuscation on Alibaba’s part (I don’t agree with the comparison to Enron as alleged by the short-seller), more of an innocent misstep. After all, in China, this is how things are done.

China

The next tail risk can be grouped simply into one word: China. In China, you cannot do business without a friendly political climate. There is always the risk of political relations souring (see Wanda) or fraud/nationalisation (see Anbang Insurance). There is also the risk that the bad debt situation in China can worsen and affect the Chinese economy. The corporate governance in China is also not as robust as what you would expect from a Singapore or US company.

These are all risks that come with investing in a China company.

Competition

The competition in China is brutal. I’ve been to China many times over the past 5 years, and every time I am amazed by the pace of transformation. It’s hard to comprehend truly how vibrant and competitive this market is without being there yourself. It is always foreseeable that a new startup can come up and disrupt Ecommerce itself.

Personally I see this as a longer term threat, because Ecommerce is still in its infancy and has many years to go to reach maturity. Alibaba’s moves to acquire stakes in competitors and young startups also alleviates this risk somewhat.

Global Macro

This last point is out of our control. A trade war between Trump and China would severely affect the valuation of Alibaba. Tech as an industry could fall out of favour, and you could see P/E compression. The economic cycle may end causing an equity bear market.

I have my views on each of the above, but at the end of the day, these are short term factors that will pass. If you like the long term prospects of Alibaba, there is no point timing the market. Buy a small stake now, and if the price falls, add to your position.

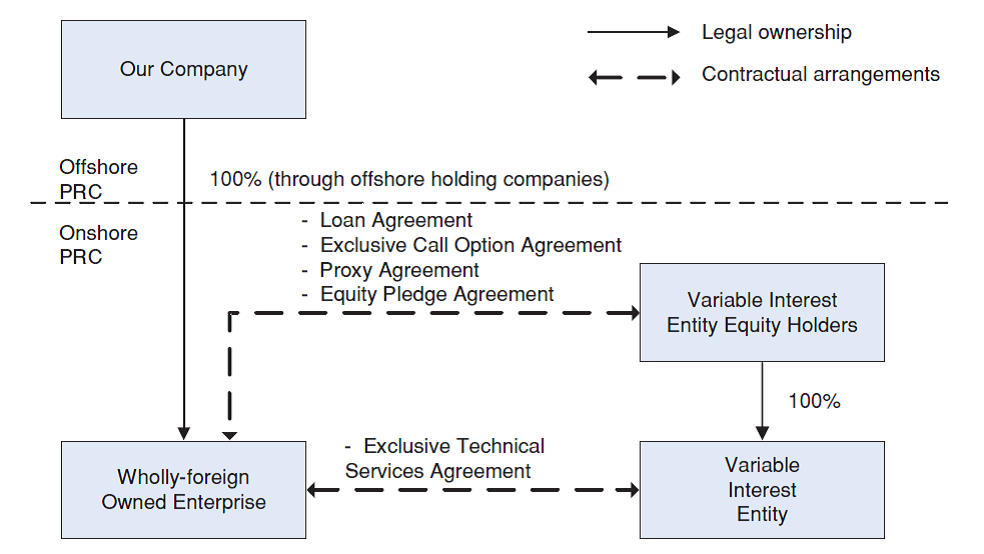

What I am less concerned about: VIE Structure

There’s been a lot of talk about how Alibaba’s variable interest equity (VIE) holding structure may become illegal if they fall out of favour with the China government. There have been many doctoral dissertations written on this, so I will not labour the point.

My take is that while from a pure, legal point of view, the VIE structure many not be entirely enforceable, such a reading ignores the political considerations in play. An inability to enforce this structure would render a US$400 billion market cap NYSE listed company worthless overnight. The ramifications of such a move, both politically and economically, are massive. No Chinese company would ever be allowed to touch Western capital markets again for the foreseeable future. The Chinese government is not stupid. To me, the risk of such an event materialising is remote.

Source: Alibaba Annual Report

Closing Thoughts

The long term growth prospects of Alibaba are amazing. Their core market, China, has plenty of room to grow with the twin engines of (1) greater penetration into rural parts of China and (2) Chinese consumer becoming more wealthy. They are also investing heavily in South East Asia, which is a massive opportunity with largely fragmented players thus far. Their holdings in AliPay, AliCloud, Ele.ma and Youku Tudou can pay massive dividends in future, as many are still in their infancy.

However, this is not a sleep well at night stock. There are many potential risks to this stock, including opaque financials, China political risk, intense competition and global macroeconomic conditions. A trade war between US and China can easily take 20-30% off this stock.

At the end of the day, you need to weigh the long term growth of the Company with the potential risks, and decide whether this stock is for you.

Personally, I am bullish on Ecommerce both in China and South East Asia. I like the core management team and their strength in execution. I like how Jack Ma has made himself a personality cult (like Elon Musk). I like the growth prospects of AliPay and AliCloud a lot. I am interested to see how Alibaba leverages on its data analytics to disrupt traditional lending.

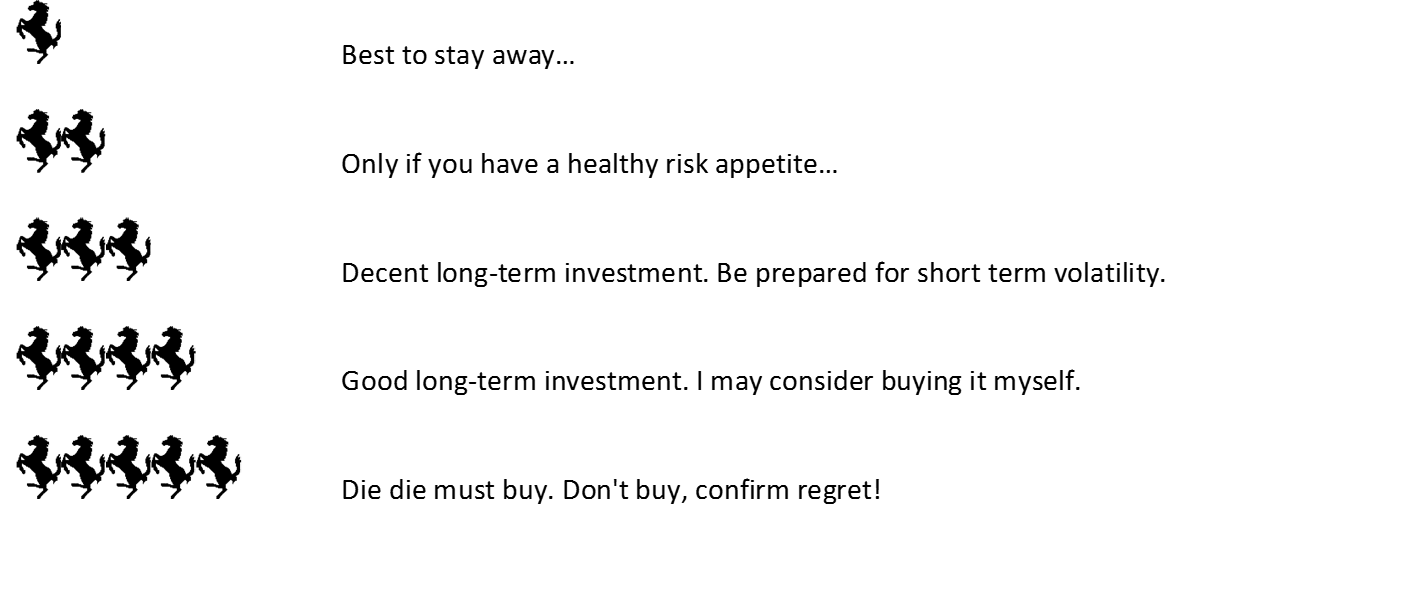

I will give Alibaba a 3 Financial Horse rating, because of its bright long term prospects, while recognising that in the short term, the share price can go anywhere. I will look to initiate a position in the coming weeks, with a view to averaging into a long term position over the next 6 to 12 months.

While we are on the topic of China commerce, check out my thoughts on offline ecommerce in this article on Sassuer REIT, which owns China outlet malls.

Alibaba Group Holdings – Financial Horse Rating

Rating Scale:

Enjoyed this article? Like our Facebook Page for more great articles!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. I share this with all my email subscribers at absolutely no cost. Sign up for the newsletter now!

[mc4wp_form id=”173″]

Any peers comparison with Eg Tencent?

That would take an an article all by itself! But jokes aside, I see Tencent and Alibaba coexisting, much like Google and Amazon, with each being highly dominant in their own sphere of influence. The pie is large enough for Tencent, Alibaba, Baidu and Weibo etc to split. Any specific area of comparison you are focused on?

Incidentally, after your comment, another blogger released a great article comparing Tencent and Alibaba. Link below, really good read.

https://seekingalpha.com/article/4163188-alibaba-better-buy-tencent

[…] Is Asia’s E-Commerce juggernaut worth a buy? – Financial Horse. [online] Available at: https://financialhorse.com/alibaba-is-asias-e-commerce-juggernaut-worth-a-buy/ [Accessed 25 Feb. […]