As subscribers on the Financial Horse tier (access to my personal portfolio) will know.

I recently picked up a small speculative position in Sea.

Now just to provide some background.

The way it works with some of these speculative positions for me.

Is that if I see a position I like, I may just buy a small position first – then I will do the deeper analysis (to decide whether to buy more / sell).

I find this works for me because:

- Having skin in the game helps me crystallise my views in a way nothing else can

- Given the speed of the market these days, it allows me to catch the upside if the stock makes a big move (and makes it easier to average in psychologically)

- But at the same time, the position will not be big enough that the loss hurts if I get it wrong

So that was why I opened a position in Sea.

And with that in mind – I wanted to share deeper views, on whether I will increase the position or sell it.

This is a FH Premium article first released in early Jan.

For updated views since then, do sign up for FH Premium for more premium articles like this.

You can also get access to my personal stock / REIT watchlist, and my full personal portfolio (with updates when I buy/sell positions).

High beta stocks like Sea have the potential to outperform in a Fed rate hike cycle

Part of the reason why I’m starting to look at high beta stocks like Sea.

Is because if we do indeed get a fed rate cut cycle in 2024, with rapid easing of monetary policy.

Then the liquidity driven names like crypto, or high beta tech stocks like Sea, could stand to benefit.

But.. will we get a torrent of liquidity in 2024?

Now whether we do indeed get a torrent of liquidity in 2024 – is a completely different question.

I address this in further detail in other macro articles.

But the long and short is that the range of possible futures in 2024 is very high.

You can easily see anything from a bad recession to a liquidity driven melt up in stocks in 2024 – depending very much on how policy makers react in an election year.

So for investors, it’s important to be nimble in positioning, and keep alive to all possibilities.

Chart of Sea Ltd – down 90%, key support at $35

The chart of Sea is pretty unbelievable.

Pre-COVID, the stock traded in the 30s.

By late 2021, the stock had gone as high as 360, close to a 12x gain.

And after the Fed rate hikes and slower earnings growth post-COVID, the stock has collapsed back to $35 today – down a whopping 90%.

Here’s the daily chart for the past 1.5 years.

The stock went as high as 88 in early 2023, but a series of bad earnings since has led to the stock collapsing back into 35.

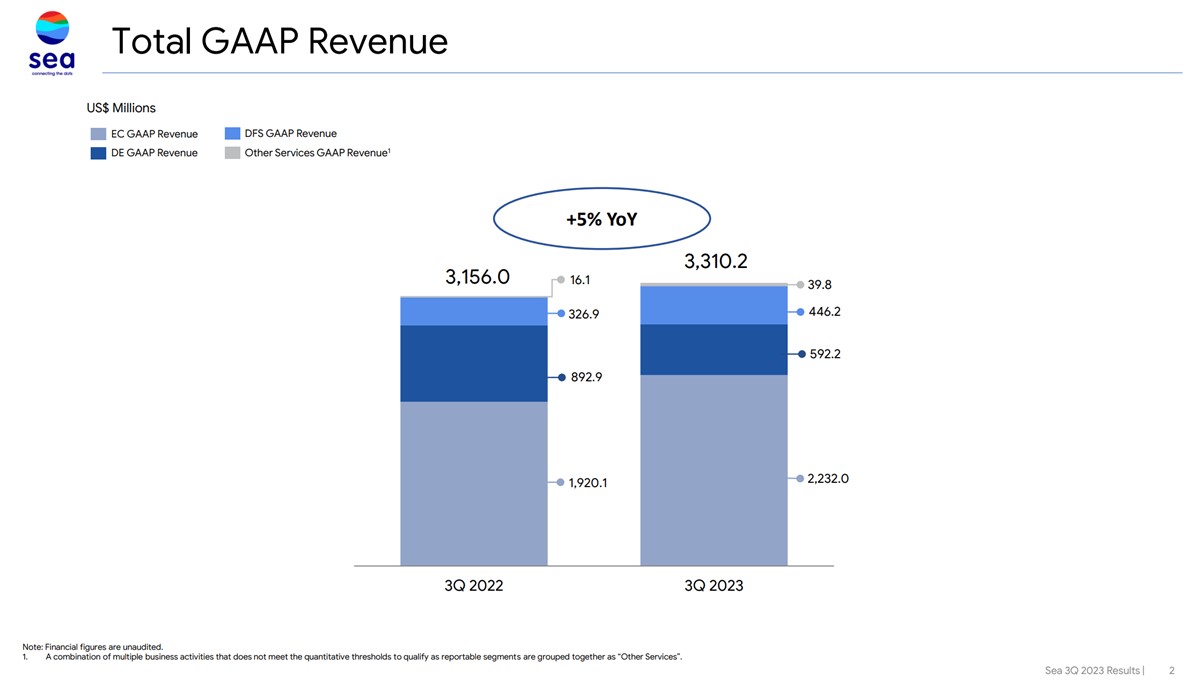

Fundamentals of Sea Ltd – Latest financial results

Here are the latest financial results.

Topline GAAP revenue is up 5% year on year.

A far cry from the COVID days where revenue was doubling year on year.

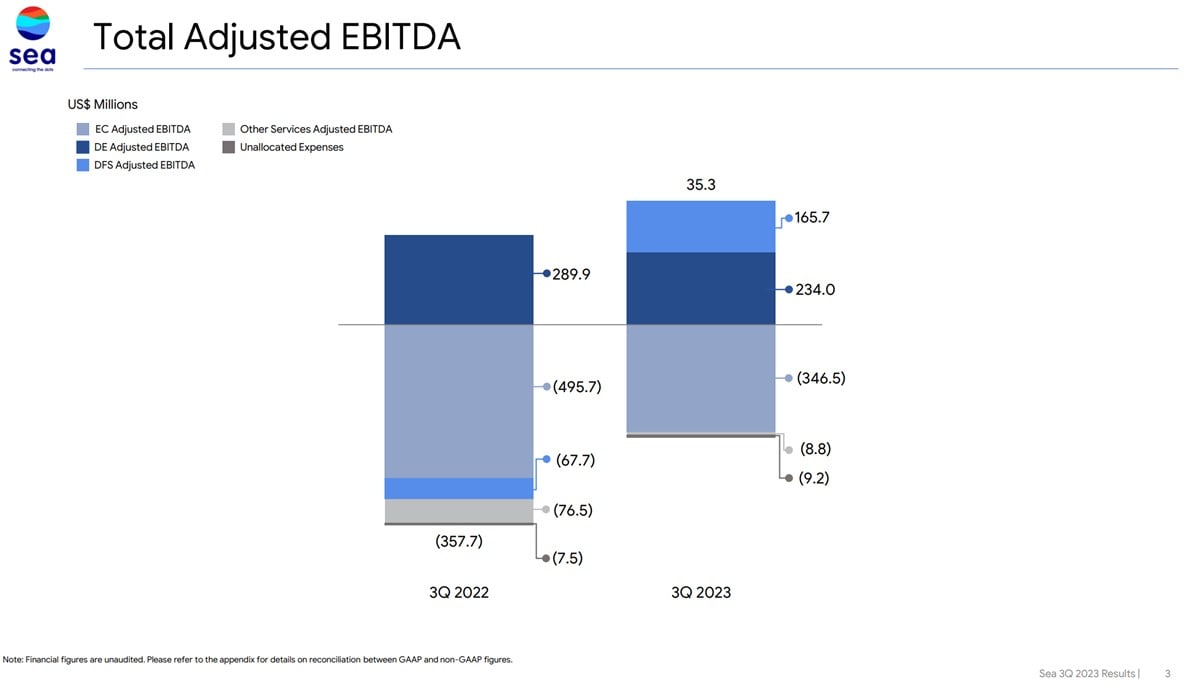

Adjusted EBITDA tells a story of:

- E-Commerce losses narrowing

- Gaming profit dropping

- Fintech profit starting to contribute meaningfully, almost 70% of gaming’s profit

But EBITDA earnings are always subject to a lot of manipulation.

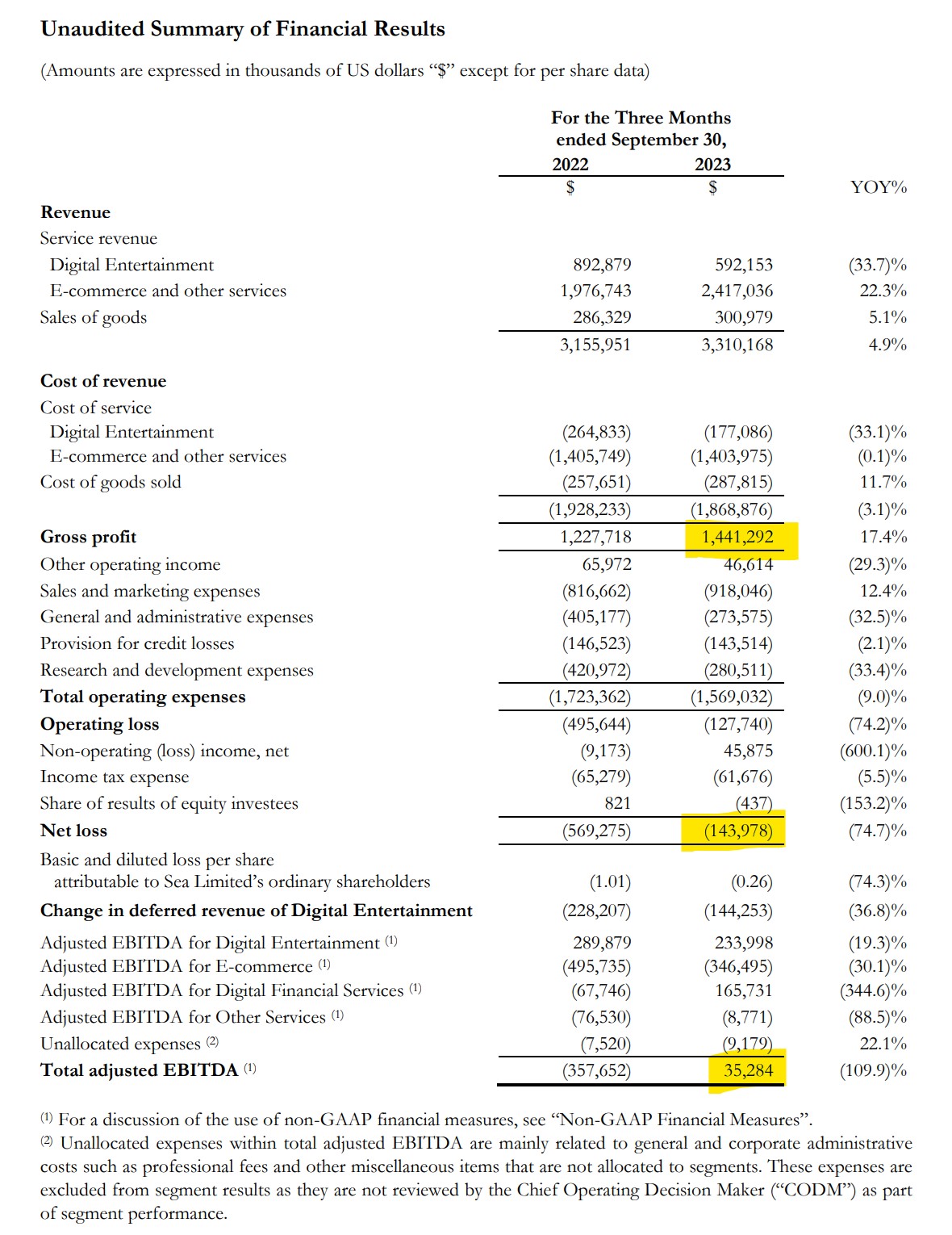

So let’s look at the actual financial statements.

Key summary is:

- Gaming revenue is down 33% yoy, but eCommerce + Fintech revenue up 22%

- Gross profit is $1.4 billion, up 17% yoy

- Net loss is $143 million, which is 74% lower yoy (569m loss last year)

Looking at these numbers you can kind of see why the stock is trading at 3 year lows.

Nobody pays a tech stock multiple for a company that is loss making, and growing revenue at 5%.

Performance from each segment?

Breaking down performance by each operating segment.

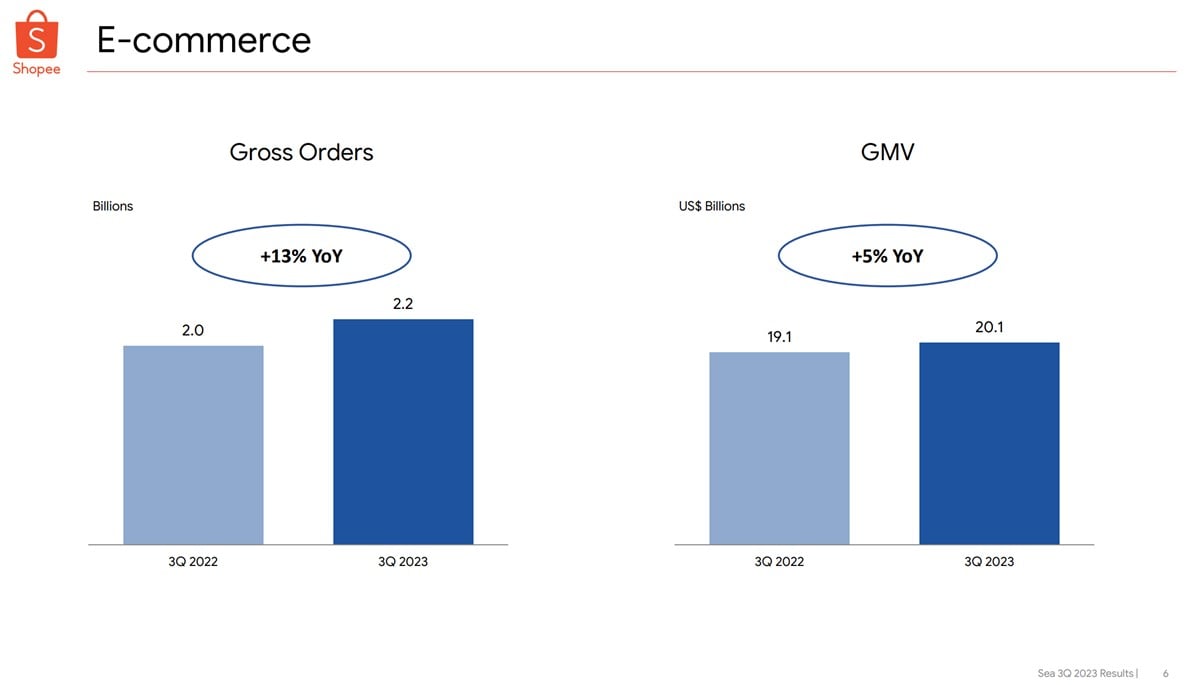

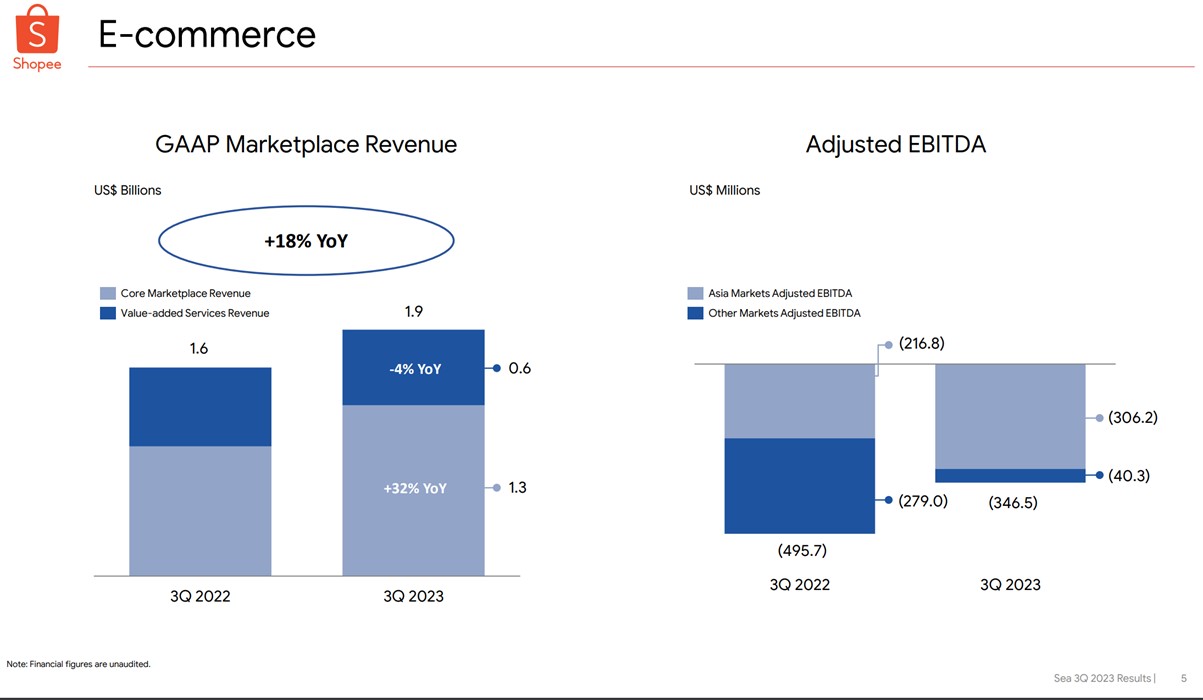

E-Commerce revenue is generally flattish – gross merchandise value up 5% year on year.

Growth has slowed down massively from the COVID days.

E-Commerce is still losing money, but the losses have narrowed.

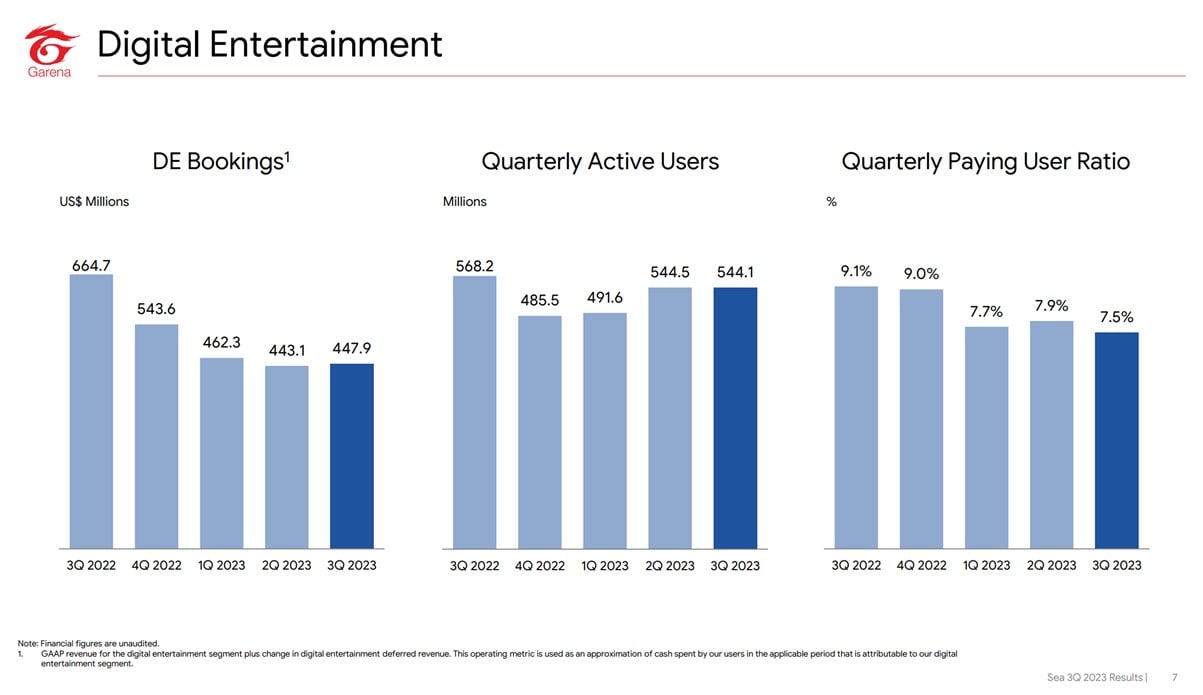

Gaming has been bleeding for a while now.

But this seems to have stabilised in the most recent quarter.

It will be crucial to watch if this holds, or if the decline continues.

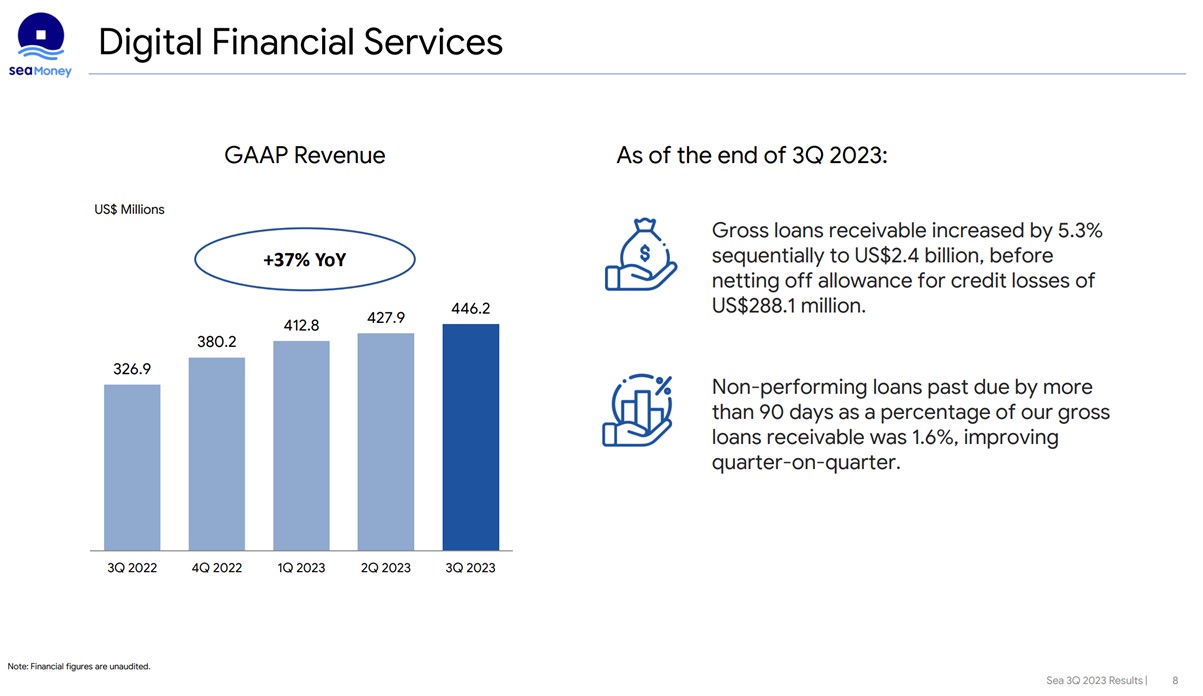

Fintech (Sea Money) is the standout performer though.

Revenue is growing nicely, but the question of course is whether they can keep this up, and how big a contributor can Fintech become.

Pivot to focus on the business

CEO Forrest Li had a very interesting sharing on the latest conference call.

I extract the relevant section below, which is interesting enough that I recommend reading in full if you have the time.

To summarise, Sea has been focussing on profitability the past few quarters due to higher interest rates.

But now, they want to shift focus back into investing in the business to increase market share and leadership, because of 3 reasons:

- Balance sheet has improved tremendously – less reliant on external financing

- Competition has gone up

- Industry trends have changed – live streaming

Let’s discuss each of these 3 points, which in my view is crucial to understanding Sea going forward.

Quote from Forrest Li:

“Our strategy for e-commerce is driven by the principle that maximizing the long-term profitability of the business will generate the greatest returns to our shareholders in the long run. And, maximizing long-term profitability requires scale and strong market leadership.

To achieve this long-term objective, we look at three key operational factors: growth, current profitability, and market share gain. While all are important and positively correlated in the long-run, near-term focus on one can create trade-offs for another. As business conditions change, sometimes rapidly, we need to decide which factor to prioritize for that period.

During the pandemic, we focused on growth first, ramping up rapidly to meet surging demand for ecommerce despite the great operational difficulties created by lockdowns. This allowed us to achieve significant scale and strong market leadership when growth was very efficient. Subsequently, capital became very expensive and less available. So we made a rapid turn to achieve immediate profitability for Shopee as a first priority, while sustaining the platform’s scale and market leadership. In both cases, we believe we made the right decisions in response to the shifting business environment.

As we focus on long-term profitability and adapt to changes in the business environment, some short-term fluctuations in our results is inevitable. However, our demonstrated ability to adapt quickly and execute major transitions effectively is a core strength for the long-term success of our business. We are now deploying this strength to realize the next shift in our operational focus in e-commerce.

In this period, we will prioritize investing in the business to increase our market share and further strengthen our market leadership. We made this decision in view of three recent developments.

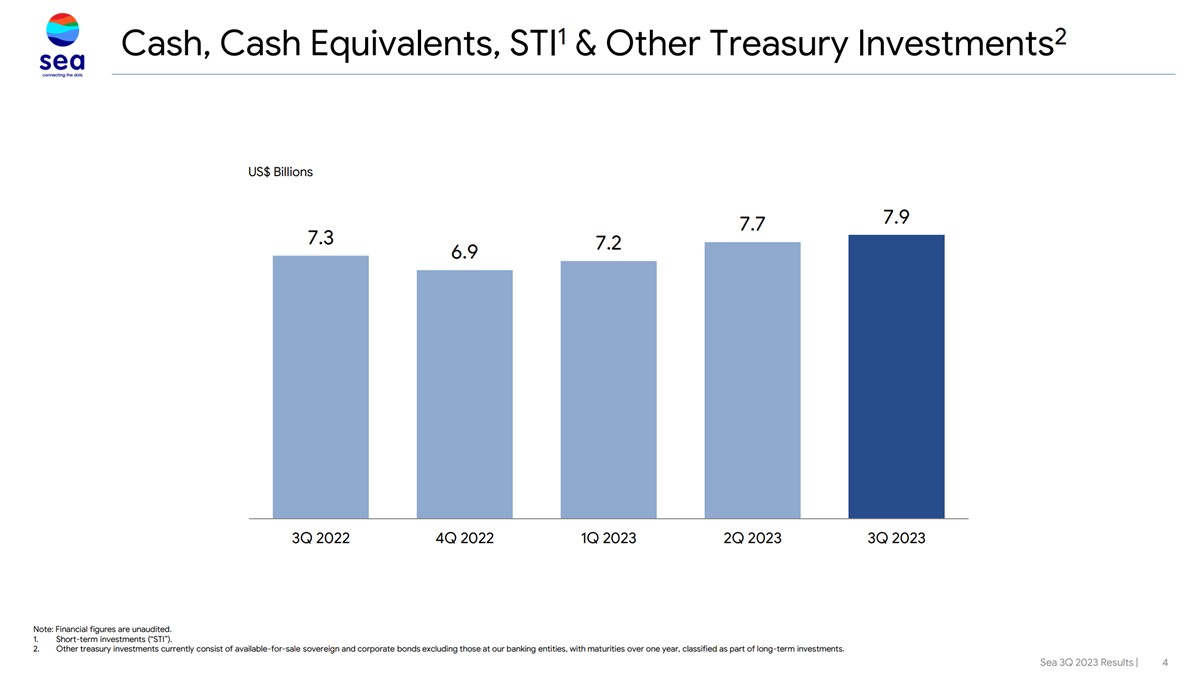

First, our move to self-sufficiency and profitability has significantly improved both our cash reserves and operational efficiency. Our group cash position has increased by around 600 million dollars from a year ago to more than 7.9 billion dollars at the end of the third quarter. This puts us in a strong position to pursue more competitive and growth-focused strategies, while maintaining financial discipline and a strong balance sheet over the long run.

Second, the entrance of new players has intensified competition in our markets. Competition may accelerate market share consolidation, and when markets stabilize, each remaining player will have sustainable profitability. Investing in market share gain now will position us better with even stronger market leadership when that happens. We thrive in a competitive environment. We competed aggressively and effectively in our markets for years to emerge as the clear market leader from an underdog position. We now have scale, a deep understanding of our markets, and strong localized execution across diverse geographies. This gives us a wide competitive moat, and we intend to grow it further.

Third, live streaming has become increasingly popular among sellers, buyers, and creators in our markets. These tailwinds give us a very good opportunity to build our e-commerce content ecosystem efficiently. We believe live streaming e-commerce will become a sizable and profitable part of our platform and extend our long-term growth potential.

I want to emphasize that in making investment decisions, we are committed to maintaining a strong cash position, not relying on external funding, and investing within our means at a time and pace of our choosing.

At the same time, given that e-commerce penetration remains low in most of our markets, we as the market leader have a responsibility to help grow the whole e-commerce ecosystem. Shopee will remain committed to doing so in a healthy and sustainable way and driving value creation for all stakeholders.”

Balance sheet has improved tremendously – less reliant on external financing

Looking at the balance sheet tells a pretty unbelievable story.

Sea Ltd, a stock with a $20.2 billion market cap.

Holds a whopping $7.9 billion cash on the balance sheet.

At their current burn rate of $144 million per quarter, that can last more than a decade.

Hence Forrest’s point about being self-sufficient, and no longer subject to the mercy of external financing.

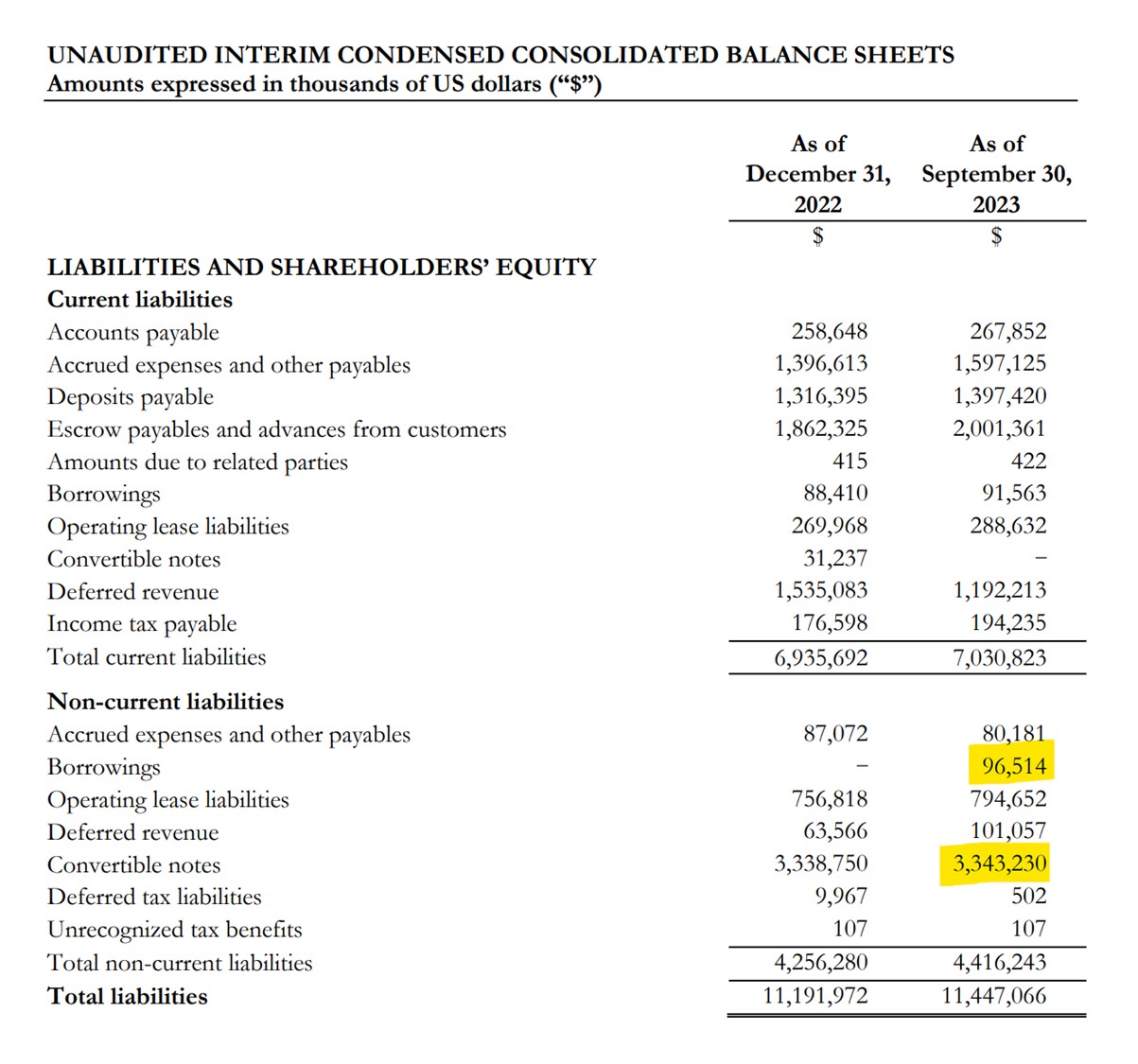

How much debt is there though?

Looking at the balance sheet – there is $96 million in borrowings.

And $3.3 billion in convertible notes.

Digging up the press release from 2021 tells another unbelievable story:

“…offerings by Sea Limited of $2.875 billion aggregate principal amount of its 0.250% convertible senior notes due 2026, as well as an aggregate of 12,650,000 American depositary shares at a price to public of $318.00 per ADS.

The Notes will be senior, unsecured obligations of the Company, bearing interest at a rate of 0.25% per year, payable semiannually in arrears on March 15 and September 15 of each year, beginning on March 15, 2022. The Notes will mature on September 15, 2026, unless repurchased, redeemed or converted in accordance with their terms prior to such date. … The initial conversion rate of the Notes is approximately US$477.01 per ADS and represents a conversion premium of approximately 50.0% above the public offering price per ADS in the ADS Offering, which is US$318.00).”

What does this mean in plain English?

In late 2021 when the share price was sky high, Sea issued $4 billion worth of shares at $318 per share.

And $2.8 billion on convertible debt.

That convertible debt will mature in Sept 2026, pays an interest rate of 0.25% interest, and is convertible into Sea shares at a price of $477.

That’s basically just free money at this point.

Long story short – Sea Ltd has $7.9b cash on their balance sheet, and very little debt against it that is due in the next 2.5 years.

Their balance sheet is pretty much rock solid here, which gives management a lot of runway.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

Competition has gone up

The second point by Forrest Li – competition has heated up.

In my view the biggest competitor for Sea in eCommerce.

Isn’t really the traditional players like Lazada or Amazon.

Rather, it’s the livestreaming players like Tik Tok.

Industry trends have changed – live streaming

Which ties into the third point.

Industry trends are changing rapidly.

Live streaming has become incredibly popular, and is growing rapidly.

And Sea Ltd recognises this.

Here’s the move by arguably their biggest competitor, Tik Tok:

JAKARTA, Dec 11 (Reuters) – China’s TikTok has agreed to spend $840 million to buy most of Indonesian tech conglomerate GoTo’s (GOTO.JK) e-commerce unit – a move that appears to allow it to restart its online shopping business in Southeast Asia’s largest economy.

It also said it will invest further in the business, Tokopedia, which is Indonesia’s biggest e-commerce platform, for a total outlay of $1.5 billion.

Sure, Tik Tok bought out Tokopedia because Indonesia had banned them from doing e-Commerce, so they were pretty much boxed into a corner.

But the fact remains that the merged Tik Tok Tokopedia will be a key challenge in Indonesia (a key market for Sea).

And you bet that Tik Tok will eventually want to compete with Sea in its other markets as well.

Other insights from the conference call

Management shared other interesting insights in the conference call as well.

I summarise my key takeaways below.

Management believes that:

- They have the ability to switch from growth to profitability at any time, as demonstrated the past few quarters

- They want to focus on growth now and reinvestment in the core business

- They see their competitive advantage coming in 2 forms: (1) lower unit cost arising from economies of scale (eg. Delivery, logistics costs), (2) stronger execution team that is close to the ground

Whether you agree or not is another question, but it’s good to know how they see themselves.

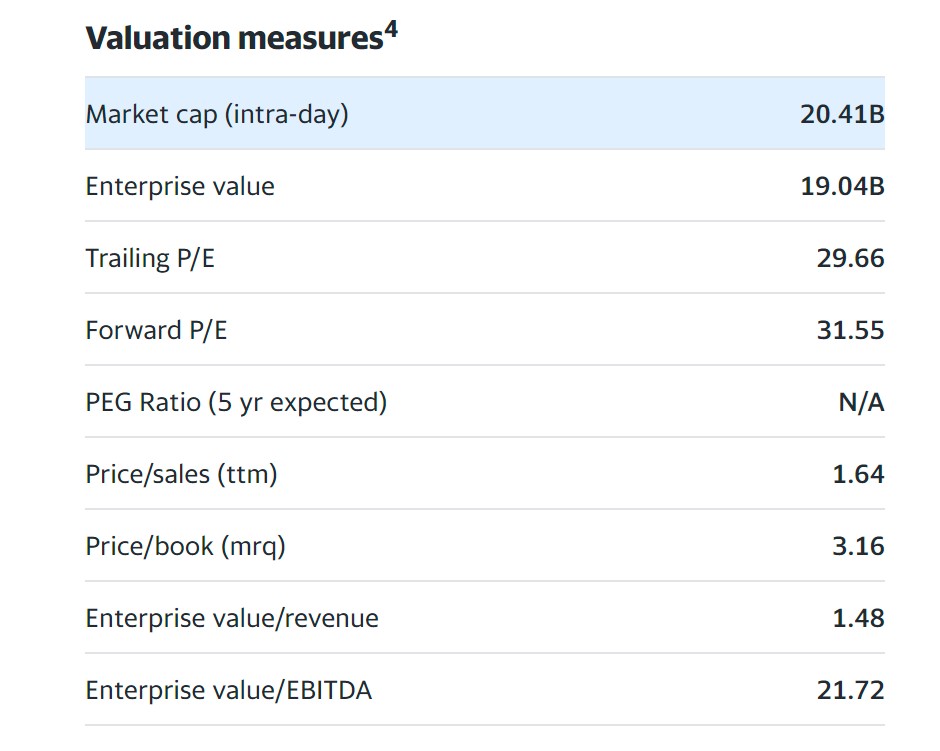

Valuations of Sea Ltd?

Throw in all of the above.

And you would appreciate trying to value Sea Ltd is an unbelievably hard task.

To the point where I don’t even think it’s meaningful to come up with a valuation for Sea, given all the uncertainty above.

Some benchmark comparisons:

- GoJek is 6b USD

- Grab is 12b USD

- Sea is 20b USD

Sea’s valuations are per below:

While Grab’s valuations are below.

Again, not very helpful because Grab is still loss making, and really Grab/Gojek-Tokopedia are just such different businesses from Sea.

Back of the napkin valuation?

Let’s say simplistically we take the latest quarterly revenue and annualise it – $13.2 billion a year.

Let’s assume a long term 5% margin – works out to $660 million profit a year.

At current $20b market cap that’s a 30x P/E.

Not exactly cheap by these metrics, but you can see how the assumptions used are just a wild guess.

If the market values it like a tech stock.

And you apply a 2x Price/Sales, to a revenue that grows 50%.

Suddenly you’re looking at a $40 billion market cap which is a 100% return from here.

So the range of possible outcomes here is very broad.

My views on Sea Ltd? Is risk-reward compelling?

For what it’s worth, I think risk-reward for Sea after a 90% collapse in its share price is actually pretty interesting.

At $20 billion market cap today, maybe worst case you lose 50% from here if things don’t turn out well (the $7.9 billion cash should cushion downside).

Best case, you could see pretty attractive upside if it returns to the $50 – $100 range or beyond.

Risks with Sea Ltd Stock?

Not to belittle the risks here though.

Sea faces significant challenges in eCommerce going forward from Tik Tok, which will surely expand to compete with Sea in its key South East Asian markets.

Existing competition from the likes of Lazada and Amazon are also not going away.

The gaming business has stemmed the bleeding for now, but it’s hard to see where future growth will come from unless they can come up with another hit title.

Fintech is growing nicely, but it remains to be seen whether they can sustain the growth, and how big it can grow to eventually.

And don’t forget psychologically – this is a stock down 90% from the top.

That means a lot of investors are underwater here.

Which means that if we get a rally, you may see a lot of investors start to sell positions once they “break even”.

This is big, and could hang over the stock for years to come.

Opportunities with Sea Ltd Stock?

On the flip side.

I have been very impressed with Forrest Li and how his management team has grown Sea since it first started with Garena in 2009.

And with $7.9 billion in cash on the balance sheet, that’s buys a lot of time and flexibility for the management team.

And at $20 billion market cap today, valuations are a lot more reasonable than where they were a year or two ago.

If Sea can hold onto or grow its market share in eCommerce, I could see the stock recovering to the 30 – 40b market cap range, which is a 50 – 100% return from here.

The problem of course – is when.

The challenges for Sea require reinvestment into the business, a pivot to live streaming – moves that will not bear fruit overnight.

Closing Thoughts

Technical wise though, there is strong support at the $35 level for Sea stock, so this could be an interesting point to add, although do watch out for downside risk if the $35 level breaks.

Personally I think the risk-reward is interesting enough that I may look to add to the position.

But I do think you have to be very aware of the risks here, so this is not a position for everyone.

Because of that I will also likely size the position well, to limit downside if I am wrong.

Would love to hear what you think though?

Do you think Sea stock will recover in the months / years ahead?

This is a FH Premium article first released in early Jan, and has not been updated since.

For updated views since then, do sign up for FH Premium for more premium articles like this.

You can also get access to my personal stock / REIT watchlist, and my full personal portfolio (with updates when I buy/sell positions).

WeBull Account – Get up to USD 3000 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 3000 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund SGD2000

- Maintain until 31 March

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.