For those who missed it, the balloting results for Astrea V were out on Wednesday, and the bonds started trading on the SGX on Friday. Because these bonds were so hot, and because they inspired so much debate, I wanted to do a simple debrief and take the opportunity to respond to some common criticism.

Basics: Balloting Results

The applications for Astrea V against Astrea IV are set out below:

| Astrea IV | Astrea V | |

| Offer Size (Retail) | S$120 million | S$180 million |

| Subscriptions | S$890 million | S$820 million |

| Oversubscribed | 7.4 | 4.5 |

The total number of subscriptions came in at S$820 million, slightly lower than Astrea IV’s S$890 million. The main difference though was the offer size, because Astrea V’s was 50% larger at S$180 million, so the public tranche was only 4.5 times oversubscribed versus Astrea IV’s 7.4

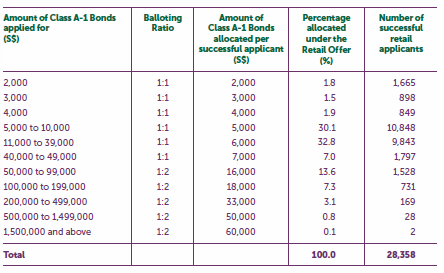

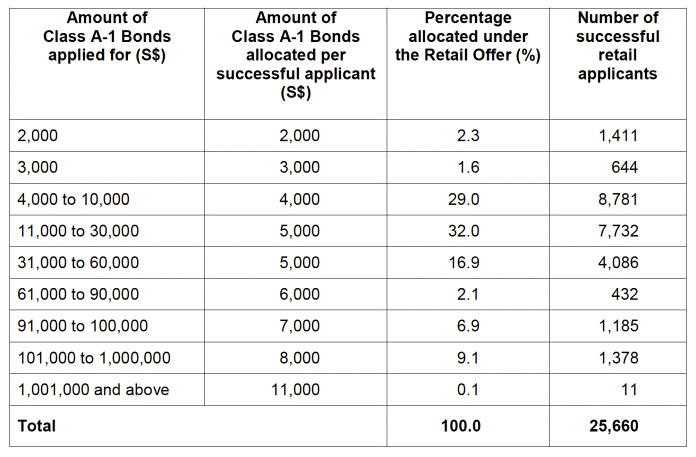

Balloting tables for Astrea V and Astrea IV are set out below. If you applied for S$10,000 in both (like me), you would have gotten S$5000 of Astrea V, and S$4000 of Astrea IV.

Astrea V

Astrea IV

Astrea V commenced trading on Friday 21 June, and closed at a price of 1.037. So that’s a nice 3.7% increase, just for doing nothing much. At it’s current price, it trades at about a 3.5% yield to maturity, very similar to where Astrea IV is trading.

All in all, this was a very strong showing by Astrea V at IPO, much much better than something like Eagle Hospitality Trust. It’s just that Astrea IV was incredibly strong, so by contrast, Astrea V doesn’t look as good. 4.35% for a low risk investment was a complete no brainer, 3.85% for a slightly higher risk invest… less of a no brainer, but still very good.

Criticism of the Bonds

Because Astrea V was so popular, it attracted a lot of great commentary as well. I’ve been reading a lot of them with great interest, and long story short, the main criticism is that the Risk-Reward is not attractive for a private equity investment

Risk Reward not attractive for PE investment

I though this argument was best articulated by this blogger. I’ve summarised it very simply below, but it’s well worth the read if you have the time:

- Structure – As a fund of funds, the fees and expenses are much higher than what you get with other equivalent products.

- High Price of Investment – The purchase price of the bond is based on the NAV of the underlying PE funds, which could be inflated due to private valuations (eg. Uber).

- Senior Priority Fallacy – Because this is a fund of funds, when one of the underlying PE Funds fail, the recovery in liquidation will go to debt creditors of the PE Fund first, and not the equity holder of the PE Fund, which is Astrea.

- Withdrawal of investment by other fund participants – PE is an illiquid investment, when a large number of investors withdraw at the same time, it will cause valuations in the industry to fall. Given the stage of the economic cycle, there is the possibility this happens in the near future.

And the conclusion is extracted below:

“Conclusion – Underwhelming Risk reward ratio

The minimum expected return for a PE investment via equity financing is around 15% on a CAGR basis. The Astrea bondholder is investing for merely 3.85% with the illusion of senior priority, risk of withdrawal by other investors and the high NAV price which is characteristic of an investment into a mature fund.

In addition, there are also the list of risks disclosed in the prospectus which are unique to a PE investment and applicable to you even as a bondholder.

Given the slowing global macro environment which have been agreed by various global central banks statements and reports in the past 6 months, we urge investors to be cautious in aggressive investments due to possible devaluation of asset prices which would directly affect the underlying value of the assets and the cashflows for the Astrea V bonds.

Therefore, it is beyond our understanding as to why one would agree to a 3.85% return.”

And for the record, the blogger himself agreed that creditworthiness of the Astrea V Bonds is not an issue:

“At the time of writing, we like to state that we think Astrea will be able to meet all coupon payments on a timely basis. We think the worst case scenario would be an under fulfilment of 1-2 tranches of reserve payment and a minor delay in the mandatory call. This is not attesting to the strength of the underlying investment but because the reward is a very small portion of the entire available pie.”

To be fair to him, I actually agree with a lot of his points above.

But where I disagree, is the conclusion.

I think a lot of people are looking at the underlying PE Funds and securitisation structure and this is clouding their judgment. But let’s try to separate both issues.

Imagine that I want to borrow money from you at a 3.85% yield for 5 years. After 5 years, there is a 99.5% chance that I repay your principal, together with an extra 0.5%. There is a 0.5% chance that I can’t pay up after 5 years. In which case, I will pay you 4.85% a year from then on, until the day I can pay up. And the chance that I cannot pay up after 10 years, is around 0.001%.

If offered this product now, would you invest? Well I absolutely will.

The thing about debt investing, is that you cannot think like an equity investor. The nature of the investment is fundamentally different.

When you’re investing in equity (like stocks), your potential upside is unlimited. If you invest in Tesla and the company does well, the sky is the limit as to returns. So when you invest in equity, you have to think about how well the company will be able to grow in future, because that determines your returns.

But when you’re investing in debt (like bonds), your upside is limited to the yield on your debt. No matter how well the company does, all you’re going to get paid is your yield. So when you invest in debt (like Astrea), you don’t really need to bother about how well the company can grow, all you care about is whether the bonds will default.

So yes, I agree that the Astrea bonds can be a way for Azalea to really juice their returns. They’re basically borrowing money from investors to invest in Private Equity. If they borrow from you at 3.85% and the PE Funds returns 15% a year, they’re just made a 10.15% return. But hey, what does it matter to you what Astrea does with the moneys?

Think about it this way. Imagine that a bank gives you a mortgage to buy a property at 2% a year for 10 years. After 5 years, the property goes up in value by 100%. Now the bank is upset, and complains that he should have a bigger share because the property went up in price. Really?

Debt investing is about creditworthiness. Full stop. Once you’ve determined the chance that the issuer will default, the next question is whether the yield is worth the risk. What the issuer decides to do with the money, is entirely up to them.

So all I’m saying, is that you should view the issues separately. Evaluate the risk of default of the bonds, based on the underlying PE assets, and securitisation structure. And the general consensus here, is that the chance of default is incredibly low. Once you know this, then decide whether the yield is worth it, for the risk you are taking on.

Pricing of the bonds

Word on the street is that Astrea again left some money on the table for these bonds. Apparently they could have priced it much higher and they still would have fully filled their books from institutional investors, but they deliberately priced the yield slightly higher for retail investors.

I know it seems like a trick (why would a government linked entity be so kind), but if you look at the recent SIA bonds which listed at 3.03% yield, this theory actually makes a lot of sense.

SIA’s creditworthiness isn’t significantly better than Astrea V, so there’s absolutely no reason why SIA is borrowing from retail at 3.03% when Astrea is doing it at 3.85%.

What’s next

When I was at the Management presentation by Astrea, they kept talking about how they’re trying to open up private equity to the public. So they’re starting with these Class A PE bonds, eventually move on to the Class B bonds, and in the extreme long term, they may even open up the equity tranche to retail investors.

Viewed this way, there is massive incentive for Astrea to ensure that these bonds succeed, to give the public a favourable impression of private equity as an asset class, and Astrea as an issuer. Which could explain why they “left some money on the table”, and went out of their way to structure a sound product.

And hey, if government wants to give out some free handouts, I’m happy to oblige.

Anyway, based on the rough timeline of Astrea I to V, and communication from their management team, it seems like they generally try to launch a new Astrea product every 12 to 18 months. So stay tuned to this space, because with the success of Astrea V, I’m absolutely sure there are going to be more products coming in future.

Hopefully we’ll start getting access to the Class B bonds, because it would be incredibly exciting to evaluate the higher tier bonds, and watch the investor takeup.

Closing Thoughts: Do I regret buying these bonds?

Do I regret buying Astrea V? Absolutely not.

I still believe that the chance of default after 10 years is incredibly low. I have no plan to sell these bonds before maturity, so as long as I keep holding them, the minimum return here is 3.85%.

And when the 5 year SSB now yields 1.98%, and a blue chip REIT like Mapletree Commercial Trust yields 4.5% (with serious risk of capital loss), that 3.85% yield looks pretty great.

Are you guys pleased with your investment in Astrea? Share your thoughts in the comments section below! I respond personally to all comments!

Enjoyed this article? Do consider supporting the site as a Patron and receive exclusive content. Big shoutout to all Patrons for their generous support, and for helping to keep this site going!

Like our Facebook Page and join the Facebook Group to continue the discussion! Do also join our private Telegram Group for a friendly chat on any investing related!

I didnt buy because I thought it was like taking the risk of a PE fund equivalent to returns of 15 20% but getting the returns of 3.8%.

Fair enough, I can see where you’re coming from. What alternative investment would you make though, instead of Astrea V?

Its taking the risk of a PE investor that gives you 15 to 20 % return viz high risk high return but getting 3.85% instead.

Astrea will get 15- 3.85% = 11.15% if it wins but lose only 50% capital if it loses ( max debt 50%)

Bond investors take higher risk than Astrea but only get 3.85%. The risk is that of a 15% vehicle although it’s a basket of funds but in a globalised world, in a crash, the entire basket goes down. Leading to a crash, Astrea can sell off their PE share but bondholders may not be able to sell their bonds so easily.

Basically they get triple your the return with half the money ventured (borrowed half from bond holders) but bond buyers get 1/3 Astrea return for full 100% investment.

Astrea owners lose half their capital but investors lose all in worse case.

If Astrea sells off their underlying PE funds, wouldn’t the sale proceeds go through the waterfall mechanism, and flow down to bondholders?

Risk-reward element is a very subjective matter. To each his own or one man’s meat is another man’s poison.

No, I too decided to skip this tranche. Psychologically, I don’t feel ‘shiok’ being short-changed by 50 basis points. Glad the tranche attracts only 4.5x, an important signal otherwise Astrea VI would be 3.3%?

Agreed that risk-reward is highly subjective.

Haha… I get your point on this. Hopefully, Astrea VI would prove more attractive in terms of yield (would the yield environment recover by then?).

Cheers.

In response to FH’s reply, Astrea may not be able to get good selling prices for the PE Funds anymore when a crash happens…

Yep, that I agree with. So in that case they will continue holding the PE Funds (which are all subject to lockups on capital), and any money that floats up from the funds will go towards the bond redemption fund per the waterfall and LTV mechanism. This *should* greatly reduce the risk of default in the event such a scenario crystallises.

I think the author of the blog you have referenced needs to go for some financial literacy training. Here are my rebuttal to his points:

Senior Priority Fallacy – The valuation of the funds were presented based on its net asset value. This means that the valuation had factored in the debt taken up by the funds. So what you are seeing is essentially the equity portion of the fund which you own, and no further deduction of debts from the valuation is required when you are simulating a liquidation event

Withdrawal of investment by other fund participants – PE fund investments have a fund life of 10 years. The fund investors cannot pull out of the funds. The only way for the investors to prematurely exit would be to sell its fund interest in the secondary market. For PE secondary markets, the valuation is again based on net asset value.

Now the main issue with everyone being so unhappy boils down to:

1. the coupon is lower than Astrea IV

2. they feel that the 3.85% returns pales in comparison with the returns from PE investments.

3. they just like bashing the government (let’s be honest, Government owns Temasek, who in turn owns Azalea).

What they fail to see is the NAV of the underlying investments (1.3bn) is more than double of the total Tranche A issuance (0.46m). I am ignoring the Tranche B since it is lower in ranking. With a net asset value of 1.3bn, we are looking at a ~300% LTV ratio. Meaning the investments must have done so badly (losing 66% of its value) to cause a possible impairment of Tranche A debts. I am definitely comfortable with a 300% LTV coverage debt investment yielding at 3.85%, but most Singaporeans are apparently not.

A man after my own heart! I absolutely agree with your comments above.

Well said sir! Much better than my own rebuttal I must say.

3.85% is so low!

Yah, I agree with that haha.

I think another question worth considering is: what’s the opportunity cost? In the event of a downturn when you would like to invest in devalued equities (as you have pointed out as a strategy); Azealea would probably be devalued as well.

It provides stability and as you’ve said, you would have to hold it for 5-10 years. In light of the opportunity costs in the event of a real downturn, is it worth it?

Well, the natural response would be if you didn’t invest in Astrea V, where would the money be? Cash has it’s own opportunity cost as well because of the lower yield.

My gut feel is that the Astrea V bonds may actually hold up quite well in a downturn also, because investors will recognise the safety of these bonds (of course, I could be wrong). If for example these bonds are ever trading at a 5% yield in a downturn, I would be loading up on them heavily, because to me the risk of a default is incredibly low. So I don’t think they’ll fall much in a recession, unless it’s a financial crisis that destroys PE as an asset class for extended periods of time. In such a scenario, just about every other asset class would be killed anyway, so there’s no safe hiding spot apart from US treasuries, Gold, and cash.

The only reason why I applied for this bond (Applied 5k, got 5k), is that I really can’t find a better place to put my money. To me, REITs seems to be super overpriced and idk why people are still buying REITs, and I’m already heavily invested in local banks. So a bulk of my money is just sitting in SSBs making a meagre 2%. Hopefully this turns out well.

I agree. There really are no good alternatives at this point in time.

Does it still make sense to lookout for opportunities to top-up Astrea V from the market? 3.5 yield still not very bad looking at other options. Of course of one is confident of the creditworthiness.

What’s the yield for earlier Astrea listings, if buy from the market? Considering they will have shorter lockins too before the call.

It’s about 3.5% yield to maturity. I think even if you wanted to buy, you probably wouldn’t have the liquidity to buy them in bulk. Personally I wouldn’t do it, I think at market price they’re quite fully valued.

How about the series IV bonds? They would be 4 years holding left and if i calculated correctly, the YTM is about 4%. Isnt that even better than buying Series V at launch and holding to maturity?

Will the top up options (beyond 5 year call period) hold for people who buy from open market?

Hm the YTM for the Astrea IV is 3.5% last I checked. Unless the bond prices have moved significantly. The redemption at 5 year mechanism is baked into the structure of the bonds, they apply to any holder of the bonds regardless of how you get them.

Hope this helps! 🙂

Why is it not exactly 3.85% if you have from start to end but “the minimum return here is 3.85%.” Are there special bonus ?

If certain performance conditions are met, there is a bonus payment of 0.5% after 5 years. If not redeemed after 5 years, the interest steps up to 4.85% So 3.85% is the minimum return assuming no default. 🙂

hi Mr Horse, what is your opinion now that it’s trading below par? Do you think we should continue to hold or just sell this off at a loss in case the PE funds go belly up

Well I can’t comment on what you should do, that will depend on your own risk appetite.

For me personally, I’m continuing to hold. I think that for now, the securitisation structure is likely to provide some security to Astrea. Even in 08 the highest tier of mortgages never defaulted. So I’m sanguine here.

To add – the underlying securities are a black box, so the comfort will come from the securitisation structure, because we can’t really analyse the underlying securities. Try to decide what works for you. What I’m doing with my own portfolio wouldn’t help much because my risk appetite and objectives are very different.

Hi Financial Horse, have been following your blog for a while. While doing my own portfolio reallocation. I thought of adding this bond since the current yield at a price of 1.06 would be around 3+%. What are your thoughts on this, given the low interest yield, this could be an alternative to a ‘bond’.

I think they are alright, a reflection of the low yield environment we are in today. But if one is able to take on the risk/volatility, I think dividend stocks actually have much better risk-reward. I don’t see a strong case for owning bonds in this climate unless I can (1) get them at a fantastic price, or (2) they are long term government bonds (to play capital gains if global rates go even more negative).