A lot of you have asked where to park cash today.

How do you know how much cash to put into each of the following options:

- T-Bills

- Fixed Deposits

- Money Market Funds

- High Yield Savings Accounts

And how to best approach the issue?

So I figured I would share some thoughts on this, and take the opportunity to round up the latest fixed deposit rates.

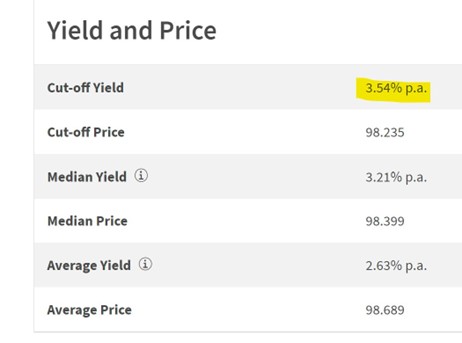

Especially given the sharp drop in 6 month T-Bills yields to 3.54% this week, Fixed Deposits are looking quite attractive once again.

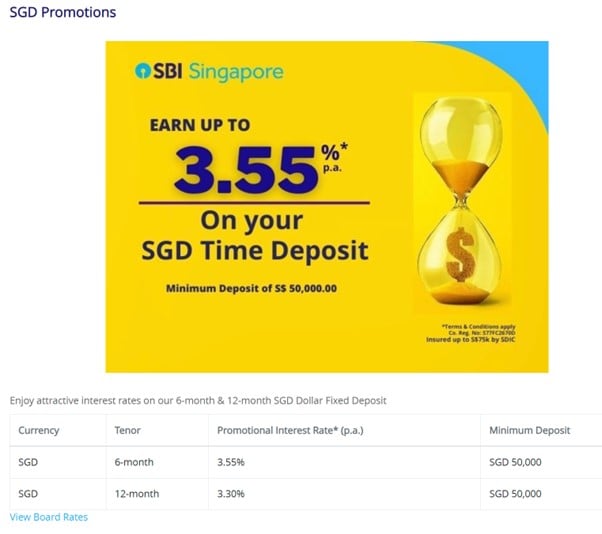

Best Fixed Deposit Rates yield 3.55% for 6 months – Better buy than T-Bills?

First off – the latest list of Fixed Deposit rates are set out below.

To summarise quickly, the best fixed deposit option for:

- 3 months – Citibank at 3.50%, but minimum deposit of $50,000

- 6 months – State Bank of India at 3.55%, but minimum deposit of $50,000

- 12 months – DBS/POSB Bank at 3.20%, minimum deposit of $1,000

Fixed Deposit a better buy than T-Bills?

Compared vs T-Bills yields:

|

|

6 months |

12 months |

|

T-Bills yields |

3.54% |

3.45% |

|

Fixed Deposit |

3.55% |

3.20% |

With the sharp drop in 6-month T-Bills yields this week, fixed deposits suddenly looks attractive vs T-Bills again – especially at the 6 month mark.

Which makes you wonder whether the banks are going to slash interest rates again after this week…

If you’re looking to put some money into fixed deposit, you might want to do it soon.

Best Fixed Deposit Rates yield 3.55% for 6 months

Latest list of Fixed Deposit rates are set out below, after which I’ll share my views on how to divide your cash between the various options available today – T-Bills, Fixed Deposit and Savings Accounts etc.

|

Bank |

Interest rate (per annum) |

Tenure |

Minimum deposit amount |

|

3.55% |

6 months |

S$50,000 |

|

|

3.50% |

3 months |

S$50,000 |

|

|

3.50% |

6 months |

S$10,000 |

|

|

|

3.45% |

3 months |

S$10,000 |

|

|

3.35% |

9 months |

S$10,000 |

|

3.45% (mobile placement) |

3 months |

S$5,000 |

|

|

|

3.35% (mobile placement) |

6 months |

S$5,000 |

|

|

3.30% (mobile placement) |

9 months |

S$5,000 |

|

|

3.15% (mobile placement) |

12 months |

S$5,000 |

|

3.25% (mobile placement) |

6 months |

S$20,000 |

|

|

|

3.15% (mobile placement) |

12 months |

S$20,000 |

|

3.35% (mobile placement) |

3 months |

S$500 |

|

|

|

3.20% (mobile placement) |

6 months |

S$500 |

|

3.20% |

12 months |

S$1,000 (max S$19,999) |

|

|

3.10% |

5/6/8 months |

S$20,000 |

|

|

3.10% |

6 months |

S$25,000 |

|

|

3.10% |

6/10/12 months |

S$10,000 |

|

|

3.10% (internet banking) |

6 months |

S$30,000 |

|

|

3.05% (deposit bundle promotion) |

12 months |

S$22,000 |

|

|

3.00% |

3/6 months |

S$30,000 |

T-Bills, Fixed Deposit and Savings Accounts? How to split cash between these options?

At a high level, these are the options available to you today for a cash / low risk investment:

|

|

Yield (indicative) |

Liquidity |

Risk Free? |

|

High Yield Savings Account (Eg. UOB One) |

Good (4 – 5%) |

Good |

Yes if below SDIC limit ($75,000) |

|

Money Market Funds (Eg. MariInvest, Fullerton SGD Cash Fund) |

Good (3.8 – 4.0%) |

Good |

No |

|

T-Bills |

Average (3.5%) |

Low |

Yes |

|

Fixed Deposit |

Average (3.2 – 3.55%) |

Average |

Yes if below SDIC limit ($75,000) |

|

Singapore Savings Bonds |

Low (but can lock in for 10 years) (2.7%) |

Good |

Yes |

What to ask yourself – split cash between T-Bills, Fixed Deposit and Savings Accounts?

A lot of you have asked what to consider when deciding how much cash to split between each of the following options:

- T-Bills

- Fixed Deposits

- Money Market Funds

- High Yield Savings Accounts

The way I see it, it’s broadly a 2 step process:

- How much liquid cash do you need?

- Rest goes into highest yield options – based on your comfort level on risk

Key question to ask – how much liquid cash do you need?

I would say the key question to ask is how much liquid cash you need, to meet your spending needs the next 6 months.

Think about how much you need to spend.

Then think about how much cash you are expecting to come in over the next 6 months.

The difference is the amount of liquid cash you would need.

So if all of your spending needs are going to be met by your salary, or if a big bonus is coming in – then you can actually run very little liquid cash.

Whereas if you’re going to buy a house, a new car, or a big renovation, you’ll need to plan ahead and have that amount of cash set aside in liquid cash.

Some guidelines on liquidity – better safe than sorry

As a general note I would say don’t be stingy with liquidity.

It’s one of those where it’s better to be safe than sorry.

So after you run the analysis above – you’ll want to buffer for unexpected scenarios too.

For example a big medical bill that you need to pay upfront, then claim from insurance after.

A big car repair bill.

A decline in stocks that leads you to want to buy some stocks / REITs.

A loss of job, meaning no income in the short term.

Things like that.

As a general note I would say you always want to have enough liquid cash on hand to cover 6 months worth of expenses, as a worst case scenario.

Liquid Cash should go into options accessible on short notice – savings accounts, fixed deposits, money market funds

Once you have the number above.

That amount of liquid cash, should go into options that you can get back with ideally a day or two’s notice.

That will include:

- High yield savings accounts (eg. UOB One, OCBC 360) – as a savings account you can withdraw any time

- Fixed Deposits – can break anytime by telling the bank, although you will lose accrued interest

- Money Market Funds – they are T+1 liquidity

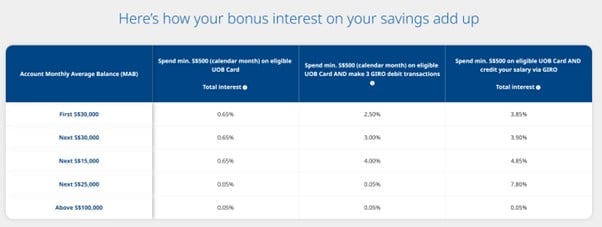

Number (1) tends to have the highest interest rates, with accounts like UOB One paying a 5.0% effective interest rate on $100,000.

So that should be the priority – and you shouldn’t move on to fixed deposits or money market funds until you’ve maxxed out this option.

Singapore Savings Bonds is an outlier, because technically the money only comes back at the start of the next month.

In a worst case scenario if you just missed the redemption window, you might need to wait a whole month to get the money back:

I would say some Singapore Savings Bonds is fine as you can get the money back reasonably quickly, but don’t overdo it and put 90% of your liquid cash into Singapore Savings Bonds.

Rest of the cash goes into highest yield options – based on your comfort level on risk

Once you have the above – the rest just goes into the highest yielding option.

As of today, that’s probably Money Market Funds like MariInvest or Fullerton SGD Cash Fund.

But Money Market Funds are technically not risk free, so I know not everyone is comfortable putting their entire nest egg into something that is not zero risk.

In which case you can consider T-Bills or fixed deposits.

But… how much cash to hold, vs stocks or REITs or real estate?

Do note that the discussion above only addresses where to put your cash.

It doesn’t address the question of how much cash to hold, vs stocks or REITs or real estate.

That’s a much harder question (that we try to answer on the rest of Financial Horse).

But long and short, I would say it depends on 2 factors:

- Individual risk appetite

- Market conditions

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

Individual Risk Appetite

Individual risk appetite is how much risk you can take.

If you’re a 62 year old approaching retirement, the amount of risk you can take is very different from a 25 year old starting his career.

Life goals matter too.

If you’ve saved up over a lifetime and finally have enough to afford a comfortable retirement, you may not want to put all that into high risk stocks and risk losing it all.

Whereas if your current capital is very low, you might not mind taking on higher risk for the chance to get great returns.

How much risk to take – only you can answer this question for yourself.

Market conditions

The other factor to consider is market conditions.

Yes I know this is market timing and all.

But I would say there are some times in markets like March 2020 or 2008/2009.

That as long as you have enough cash set aside for spending needs and contingencies, it probably makes sense to increase risk exposure given how cheap valuations are.

And vice versa.

But I know not everyone is comfortable with market timing, and some prefer to just dollar cost average regardless of market conditions.

In which case you can ignore this factor and focus on risk appetite above.

So there you have it!

Do you agree with my analysis above on how to split cash between T-Bills, Fixed Deposit and Savings Accounts?

– Get up to USD 3000 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 3000 free shares.

You just need to:

- Fund SGD 2,000

- Maintain until 31 March

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

you shld mention syfe FD too.

Thanks – will include in future comparisons.