Goldman Sachs issued a bearish report on China banks earlier this month.

The reaction was swift – not in a good way.

China bank stocks have plunged since the report was released.

Here’s ICBC, trading very close to it’s 2022 lows.

At this price, it pays a 9.1% dividend yield, and a 65% discount to book (if book value even means anything for a China bank).

You know the saying to be greedy when others are fearful?

And also another saying not to catch a falling knife – because markets are generally right?

So what do we have here – are the markets right on China banks, or are they horribly wrong?

Are China banks at a 9% dividend a good buy?

Goldman Sach’s report on the China Banks

Let’s start with the report from Goldman Sachs that triggered this latest sell-off.

Titled “Testing the ‘Impossible Trinity’”, it is a 3 part series on the China banks issued on 4 July 2023.

I extract the summary of each of the 3 reports below, and you can read in full if you are keen.

Summary of Goldman’s views

The short version though, goes like this:

Because of China’s slowing economy, banks are likely to be “forced” to extend policy loans to support local governments, which may never be repaid in full.

So China banks are going to suffer losses both on their current exposure to government debt, and future exposure going forward.

Throw in the downturn in China real estate, and bad corporate debt due to the slowing economy, and a lot of loans for the China banks may go bad.

Because of this, Goldman thinks earnings for China banks may drop going forward.

And because of lower earnings, Goldman predicts that the China banks will need to cut their dividend rate going forward.

Goldman predicts a 2% point dividend cut (8% to 6%) for the China banks, and multiple compression going forward.

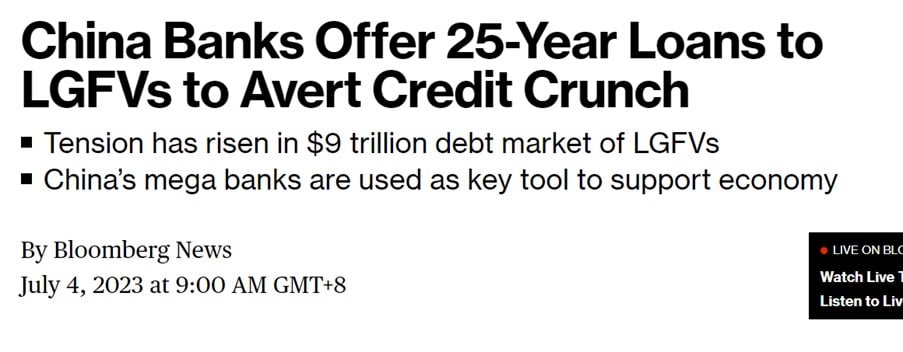

Bloomberg’s Report on China Banks

Bloomberg’s Report on China Banks

Purely by coincidence, on the exact same day, Bloomberg issued a report saying that China banks are giving 25 year loans to LGFVs to avert the credit crunch.

LGFVs, or Local Government Financing Vehicles, are basically government financing vehicles, that have been facing a cash crunch ever since the real estate slowdown (their primary source of revenue before this was government land sales which have since dried up).

It specifically named banks like ICBC and China Construction Bank as banks that are offering such loans.

Giving a 25 year loan to LGFVs is basically a way of saying that the banks are being forced to support the local governments and do “national service”.

After all, if left to their own devices, why would any bank manager grant a 25-year loan to a local government given their current state of finances?

So this basically corroborated what Goldman was trying to say – that the China banks may be forced to support the local economy.

Which would hit their profitability, and the dividend going forward.

ICBC Share price plunged on this news

Now the main reason why investors buy China banks is because of the juicy 8-9% dividend.

So if the dividend is cut, you can understand why investors are going to freak out.

ICBC has plunged close to 15% since Goldman’s report first came out.

Current prices are very close to the lows reached in late 2022.

You can see the 20 year chart of ICBC below, which is simply unbelievable.

Current prices are close to the lows reached in 2009 after the Global Financial Crisis.

You’re buying ICBC close to the price it IPO-ed at in 2007 (HK$3.07).

Dividend Yield of ICBC – 9.1%

ICBC paid a 0.3292 dividend last year.

At current price of 3.6, that’s a 9.1% dividend yield.

At a mere 31% payout ratio.

If it drops to 3.3 (2022 lows), that’s a 10% dividend yield.

Do note that Singapore investors are subject to a 10% withholding tax, so the net dividend is about 8.2% at current prices.

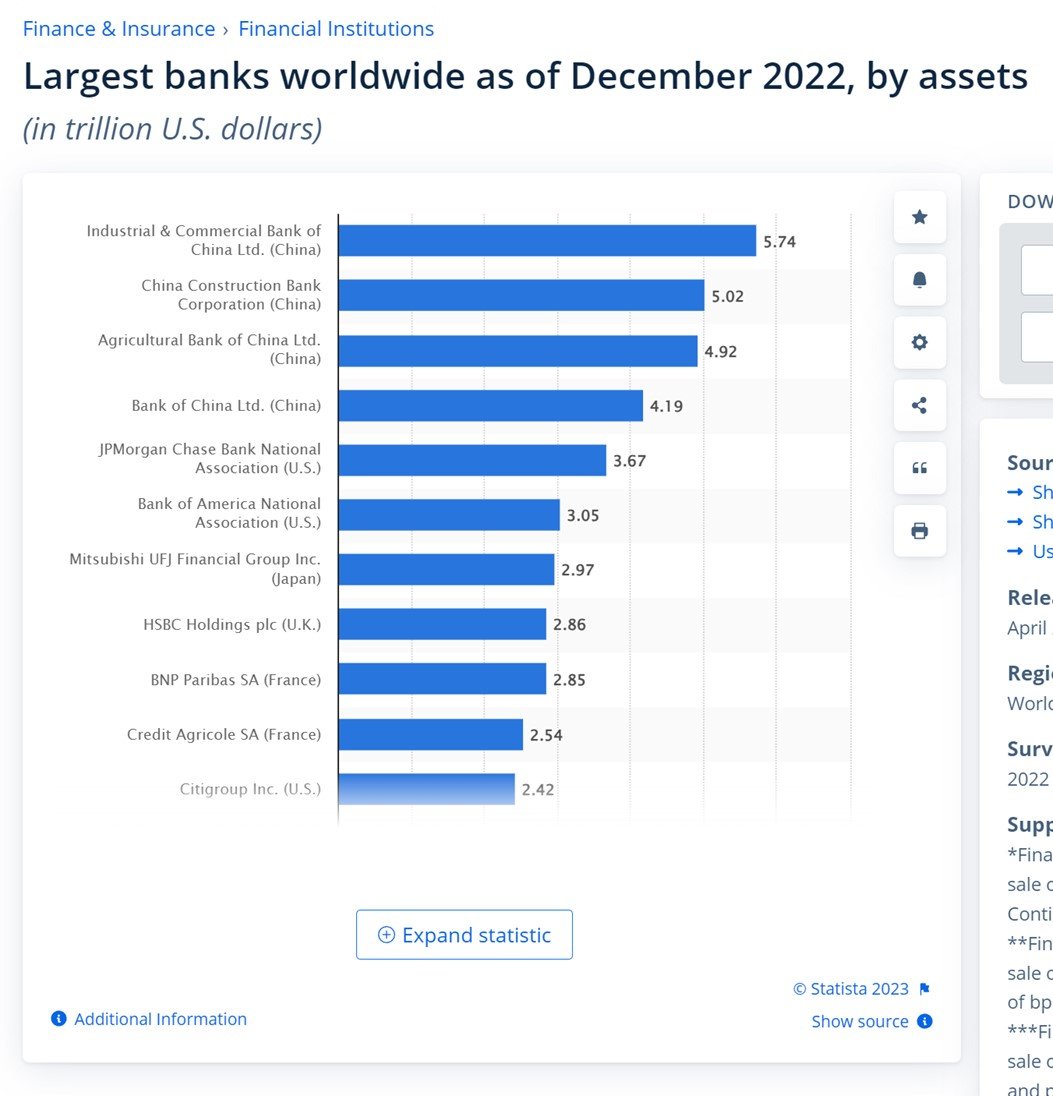

ICBC is the world’s largest bank

Just for the record, this is not some second rate bank like Silicon Valley Bank.

This is ICBC, the largest bank in the world.

By asset base alone, ICBC is close to 60% bigger than JP Morgan.

And more than double the size of HSBC.

If ICBC were to go under, this would make 2008 look like the appetiser.

My views from a fundamental perspective

Let me cut to the chase, and share my views on a fundamental perspective.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Risks with China

The risks of investing in China are not new.

Yes you have a real estate crisis playing out like a slow motion train wreck, that may play out like Japan’s lost decade (1990s).

Yes Xi is cracking down on private businesses and entrepreneurship in China, and it’s not clear whether we return to the pre-COVID days of capitalist China, or if China is even a good place to do business after this.

And to top it off, you have a US-China great power conflict that is likely to play out for the better part of this decade (and possibly next).

Even our very own Temasek has said that they “We won’t invest in areas that are in the crosshairs of US-China tensions.”

Investor sentiment on China is overwhelmingly bearish.

That being said… the best investments are those that nobody wants

That said.

Some of my best investments were made when nobody in the market wanted to touch that asset class.

Think energy stocks in April 2020, when oil prices were going negative.

Banks in 2008/2009, when the financial system was imploding.

You get the idea.

So I look at this 20 year chart of ICBC.

And it just gets me thinking.

Is this one of those times?

But… sometimes the market is right

I just want to put it out there that you don’t want to be a contrarian just for the sake of being a contrarian.

99% of the times, the market is right.

Most of the time, a stock going down is going down because the fundamentals are poor, and if you buy into it you’ll end up losing money.

Hence the falling knife analogy.

So it’s important to have some humility as an investor.

99% of the time the market price is the right price.

Yet it’s the 1% of the time where the market is wrong, where you make the majority of your money.

So… how do you know which it is?

My personal views on ICBC or the China banks?

The way I see it.

The concerns flagged by Goldman Sachs are not new.

This horse is old enough to remember in the early 2000s when westerners were flagging the exact same concerns that the loan books for the China banks are a black hole, and how they may be forced to extend policy loans that may never be repaid.

The same concerns continued to be talked about over the next 20 years as China’s economy powered higher.

With China, it’s pretty much understood that the China banks (or any company in China) is required to prioritise the interests of the state over profits.

You can’t think of ICBC the same way as you would JP Morgan.

The closer proxy might be DBS, if Singapore’s economy weakens materially.

If that happens – will DBS, with its Temasek ties, still be making decisions purely from a profit making perspective?

The faustian bargain with China banks

The faustian bargain with China banks has always worked like this.

You close one eye on the quality of the loan book, and you don’t ask too many questions on whether the loans can ever be repaid.

But you will get your 8 – 10% dividend paid to you, year after year.

That’s really what it came down to, for investors in China banks.

In fact the same China banks that trade at a 8% dividend in Hong Kong would trade at a 6% dividend in China.

Partly because the local Chinese investors understood this faustian bargain and were more willing to accept it vs foreign investors.

And partly also because RMB trapped onshore doesn’t have the same investment opportunities available.

China has a lot of levers to stimulate growth… if they choose to

Unlike in the West which trades on economic cycles.

China’s business cycles are man made.

Since 2020, China has been actively taking steps to tank their economy.

First with the China tech crackdown.

Then with the real estate debt crackdown.

Then by keeping money tight.

So yes, growth in China is slow, but it’s also slow by choice.

Conversely this also means that if China decides to stimulate growth.

There are a lot of levers they can pull – They can cut interest rates, they can print a lot of money, they can cut bank reserve ratios, they can raise government spending and so on.

Of course the question then is when will China stimulate growth (and if at all).

And there your guess is as good as mine.

Apart from Xi, nobody really knows the answer.

Technicals of ICBC

In times like that I like to use technical analysis to help guide the decision making.

Here’s the RSI, which at 29 is at oversold levels.

Look closer though, and you’ll find that if ICBC goes to a 20 level on the RSI that would be a strong buy signal.

At 29, it’s still not that strong a signal.

Share price has broken below the 50 and 200 day simple moving average, which is not good.

Exponential moving averages also show the stock in a downtrend.

So the technicals generally suggest that more downside may come – that the short term doesn’t look so great.

Investors keen to pick up long term positions can probably let this play out a bit more first.

It’s going to come down to this

The way I see it, it’s going to come down to 2 questions (for long term investors).

First – Do you see China as a superpower in 2050 (on par with or surpassing the US)?

Secondly – Do you think the China banks will be forced to cut their dividend in the short term?

First – Do you see China as a superpower in 2050 (on par with or surpassing the US)?

The first forces you to think about how you see China long term.

If you think China will emerge stronger by the middle of this decade, on par with or surpassing the US, then you can start to think of ICBC as an investment.

If you think that China will never surpass the US, and will muddle along with its domestic problems for the next decade or two, then I say you should skip the China banks.

What do I think?

I get that most westerners think that China will no longer surpass the US.

They think what with Xi China has lost its dynamism, and will be mired in domestic troubles for the next decade.

Personally I want to believe that China will regain it’s growth after the short term struggles.

But hope is not a strategy, so risk-reward and position sizing matter too.

Secondly – Do you think the China banks will be forced to cut their dividend in the short term?

Even if you think China will prevail in the longer term.

It doesn’t necessarily mean you’re going to make money on your ICBC shares.

How China gets there still matters.

This second question forces you to think about the path to get there.

If China get there by running their local banks into the ground and nationalising everything, you may see your ICBC investment wiped out.

If China invades Taiwan some time this decade and the US responds with overwhelming sanctions (and military force), you may not see much of your ICBC investment.

In investing, the path matters as much as the destination.

So… will the dividend be cut?

Talk to any onshore investor, and they’ll tell you that the dividend on a Big 4 China bank is sacrosanct and highly unlikely to be cut.

That is why onshore investors are so comfortable holding large stakes in the Big 4 China banks.

But I’ve been investing long enough to know that a lot of things investors take as sacred, can change overnight.

So again, it’s a case of hoping for the best, but preparing for the worst.

Position Sizing is important

The other thing to learn about investing.

Is that you always want to bet big enough that if you’re right, you make meaningful money.

But you never want to bet big enough that if you’re wrong, you get carted out.

No matter how certain you are of something, plan and prepare for the possibility that you are completely wrong.

Live to fight another day.

This lesson is especially important here, when you think about all the ways an ICBC investment can go wrong.

Will I buy the China banks?

For me personally – points of extreme fear are interesting for me.

So if ICBC goes to a 20 RSI, or it goes to 3.3 (2022 lows).

I’m probably buying.

I don’t know how this decade is going to play out for China.

But at that price, and at a 10% dividend, I think risk-reward is decent.

But don’t follow me into this, because I can change my mind on a dime and dump all positions (Patreons will get updates if and when I change my mind).

I could also easily be wrong on this – so for obvious reasons I am position sizing well, such that even if my China investments go to zero I am still fine.

But let’s see.

This could turn out to be the buy of the decade.

Or the dud of the decade.

This article was written on 14 July 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

– Get up to USD 800 worth of shares (expires 31 July)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- and fund $300 SGD

- Execute 1 buy trade within 30 days of funding

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Hi FH,

Thanks for ghe insightful article. For me, I will steer clear of China banks. Too many uncertainties in terms of regulatory risks and lack of clarity on major catalyst that will drive the share prices upward.

Regards,

Gerald

https://sgwealthbuilder.com

Fair enough. China risk is not easy to evaluate here, there is a geopolitical element to it as well.

How abt 3988, bank of China?

Broadly same analysis as ICBC. The big 4 China banks are kinda like UOB/OCBC/DBS – the same macro factors will impact all of them in broadly the same way.

Hi FH,

“At this price, it pays a 9.1% dividend yield, and a 65% discount to book (if book value even means anything for a China bank).”

How did you get this 9.1% dividend yield? i look up google finance and it says 6.69% div yield. Did i miss something?

Might be an issue with Google Finance’s numbers. If you pull the actual dividend paid it works out ato about 9% yield at current prices.

Seems highly risky. As you have pointed out, the ccp and the chinese economy is a black box. No one knows its real status. I think no one really thinks china will be a superpower in 2050 anymore – except Singaporeans who bought into the kly/kishore/George yeo talking points from 20 years ago (still repeating them) or the ccp. China is caught in the middle income trap. They are demographically shrinking for the first time in modern history. Xi has departed from previous policy set by DXP to set up an existential red line around taiwan which will force conflict. The western world is strategically decoupling from china at great expense. There are already soft sanctions against china in terms of technology and finance. It would be fair to say they are on a gentle downward trend. I dont see how the banks will recover

meaningfully in a sustainable way. Doesnt it follow that they will be range bound much like sg stocks are?

Yes fair enough. I think there’s really 2 schools of thought now. One that China is done for, one that China is merely consolidating for the next phase of growth.

Which view will turn out to be right, will define how the next few decades play out.

Hi FH,

Great analysis as usual and enjoy it!

The question on my mind for China is how bad is the property downturn and how long will they be able to come out of it ? Lost decade ?

Thanks

Thanks! Hope it helps.

Yes – that’s exactly the questions worth asking. Everyone has their views, but who is right only time will tell.

There are signs of policy bottom, but whether the CCP follows through with tangible actions remains to be seen.

As investors, it goes back to risk reward. Never risk more than you can afford to lose if you’re wrong.