You know how everyone regrets not buying more in 2008?

They say that if 2008 ever comes around again, they will go “all-in”.

And when 2008 actually comes around again.

Everybody is rushing to sell to raise cash.

You see the irony.

China’s “Lehman” / 2008 moment is here

Well in today’s article, I’m going to share my views on how I think China today is going through a Lehman / 2008 style deleveraging today.

And how this is opening up unbelievable opportunities in China stocks / REITs / real estate.

How exactly to play this is not an easy question to answer.

But I think for investors with the right framework (and guts), there could be some huge opportunities in the months / years ahead.

Just ask the guys who actually bought in 2008.

They’ll tell you that it was as much about blind guts as it was about macroeconomics analysis.

China stocks are cheap – nobody is denying that

I shared on Twitter this week a bunch of charts showing how cheap China real estate / stocks have gotten of late (I do share great content on Twitter, do follow me if you haven’t already).

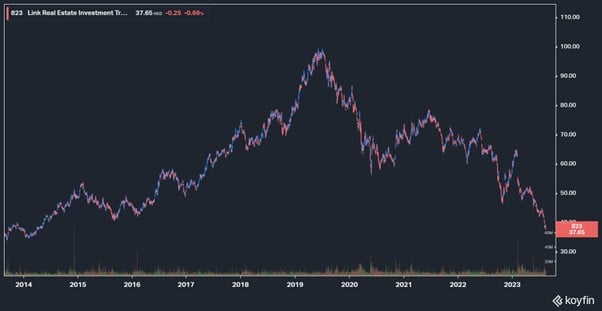

Here is Link REIT – plunged to 2014 prices.

Trading at a 50% discount to book (book value $73), and a 7.2% dividend yield.

This isn’t some small cap REIT mind you, this is Asia’s largest REIT by asset size.

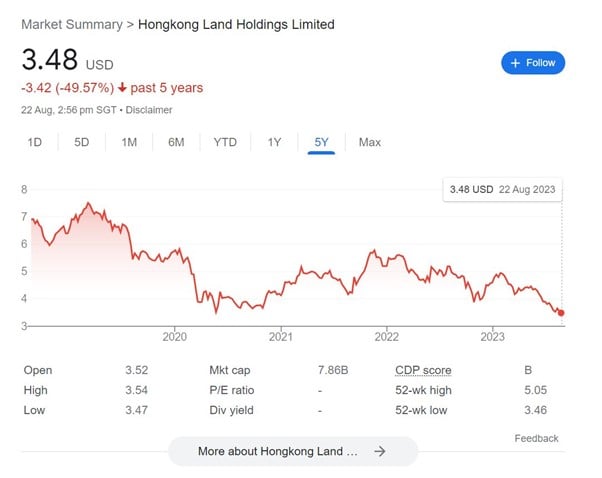

Here’s Singapore listed Hongkong Land.

Trading below COVID prices, a 6.3% dividend yield at these levels.

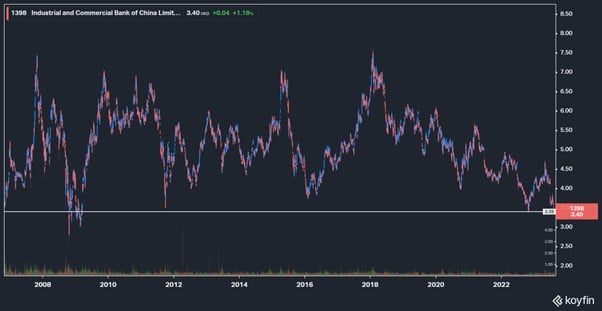

Here’s ICBC, one of the world’s largest bank and bigger than JP Morgan by asset size.

Trading at 2008 prices – last hit during the depths of the Financial Crisis.

A 9.6% dividend yield at these levels.

Here’s FXI, the China large cap ETF – close to 2008 prices.

I could go on and on and on.

But you get my point.

China stocks are very cheap today, and trading at close to 2008 levels.

Why are China stocks doing so poorly?

China contagion accelerated the past week

China contagion risk accelerated the past week with:

- Country Garden defaulting on their bonds

- Evergrande filing for bankruptcy

- Zhongzhi (one of the largest wealth managers) missing payments on certain wealth management products.

This sparked a risk-off for all China/HK related assets.

But truth be told – those are all just symptoms of the underlying problem.

They’re like Bear Sterns in 2008.

Sure, Bear Sterns caused stocks to drop, but to say Bear Sterns “caused” Lehman and the Financial Crisis is not accurate.

Rather it was subprime mortgages as the underlying problem that took down the financial system – and everything else like Lehman was just a manifestation of the problem.

So what is China’s “subprime” equivalent?

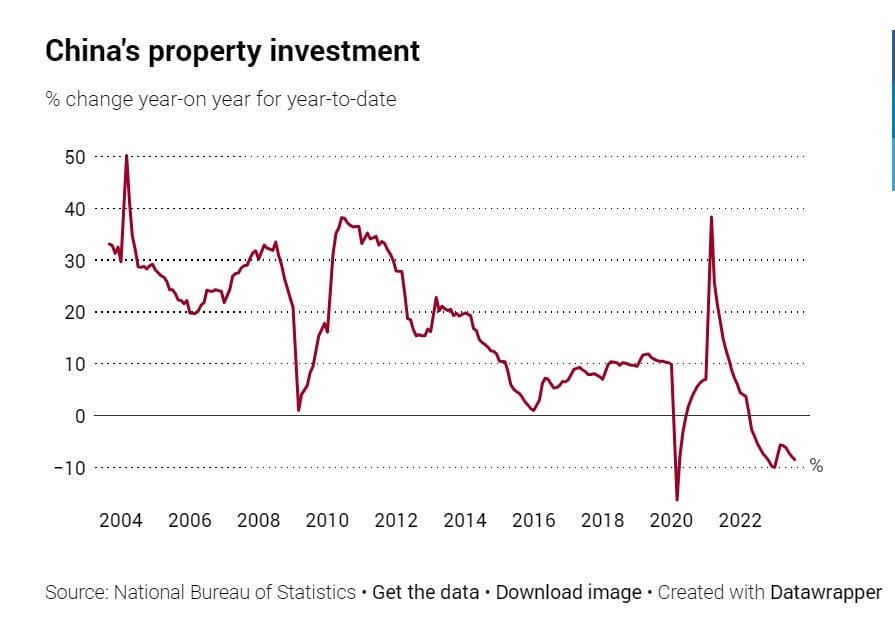

The underlying problem China faces – is too much real estate debt.

In the early days of 2000s, debt worked like a miracle for the Chinese economy.

Debt was used to build roads and buildings, this drove employment for the construction sector, real estate prices went up, households became richer because of rising real estate prices and spent more – in a virtuous cycle.

After 2008, China supercharged the debt growth to counteract the sharp drop in global economic growth (and was one of the factors pulling the world out of 2008).

But you see, debt is like a drug.

Over time, the economy builds up an “immunity” to debt.

Inefficiencies build in the system, and eventually you need ever increasing amounts of debt to achieve the same level of economic growth.

Either (a) increase debt exponentially, or (b) deleverage

So the decision is simple.

Either you:

- Increase debt levels exponentially to fuel economic growth

- Cut debt and deleverage

In 2018, after Xi secured his second term in power, he started to deleverage.

Now remember – the real estate debt growth was pro-cyclical on the way up, supercharging the economic growth.

Which meant that on the way down, it is pro-cyclical as well, supercharging the decline.

Less real estate debt growth means less construction jobs, means falling real estate prices, means poorer households due to falling house prices, which cut back on spending.

All these problems were already in place since 2018.

Everything was put on pause from 2020 – 2022 due to COVID, as the economic shutdown masked the underlying problems.

But the COVID period further devastated household balance sheets, as they drew down on savings to meet spending requirements (remember China did not unleash QE and stimulus to the same extent as the west).

So in 2023, after COVID restrictions were lifted, China faces the exact same underlying problems as they did since 2018, only worse.

What are the long term options available to China?

Let’s take a 40,000 ft view here.

If China wants to solve their overreliance on real estate debt.

There are 5 options:

- Keep doing what they’re doing

- Replace real estate with productive investments

- Replace real estate with consumption

- Replace real estate with more trade

- Don’t replace real estate

(1), (4) and (5) are not feasible

(1) Keep doing what they’re doing – means inflating the bubble forever, which is not sustainable.

(4) Replace real estate with more trade – sure China will try.

But China’s trade surplus with the world is already massive, you’re not likely to be able to move the needle meaningfully here.

Not when the west is hellbent on “decoupling” with China and “friendshoring” supply chains.

And (5) Don’t replace real estate.

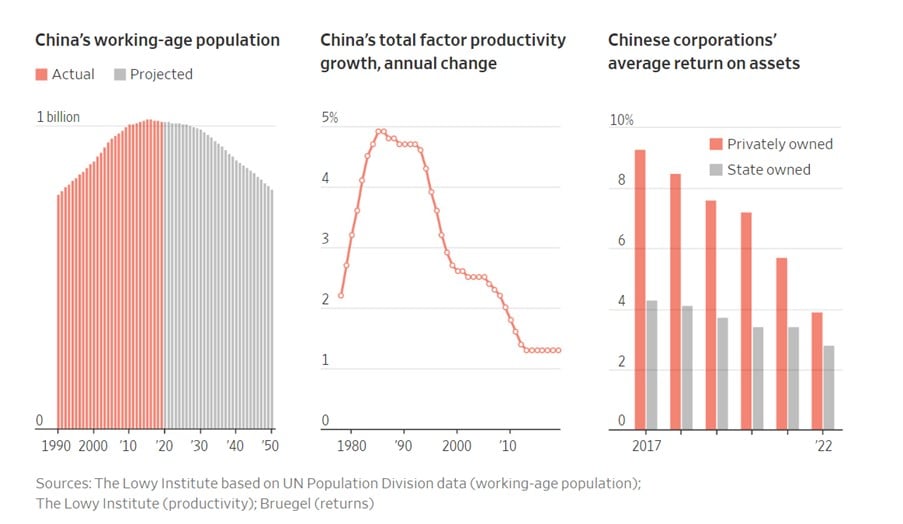

Real estate in China makes up close to 30% of the GDP.

If you let it blow up, it’s going to make 2008 look like child’s play, and I’m not even exaggerating here when you consider the debt levels in play.

At 250% of GDP, China has even more debt than the US.

Realistically though – only 2 and 3 are the real solutions.

Realistically – China only has 2 solutions.

They have to replace real estate, with (a) domestic consumption and (b) new areas of productive investments.

Each has its own problems.

Boost Domestic Consumption

Domestic consumption – the underlying problem is China’s financial repression (income inequality).

Simply put – salaries are too low.

This is great for business profits, but terrible for workers.

If you want to boost domestic consumption, you need to boost middle class income.

That means higher salaries, which means lower profits, higher costs, less competitive exports.

But this is the only sustainable solution – a redistribution of wealth, hurting the rich, but benefitting everyone else.

New Areas of productive investment

About 30% of China’s GDP is real estate/infrastructure.

This cannot be replaced overnight.

China is definitely doing this though – via semiconductors, electric vehicles, green energy etc.

But there’s just simply not enough productive investments out there to fully replace real estate.

This will be unpopular with the existing establishment – hence the crackdowns?

In any case – both policies above will be unfavourable to the existing real estate tycoons or existing businesses generally.

So you start getting some sense on why the crackdowns are required.

What does this all mean for China?

If you understand the solutions above, you’ll realise these solutions take years to effect.

Which means that the Inevitable conclusion is that China need a period of below trend growth in the years ahead as they rebalance the economy towards (a) domestic consumption and (b) new areas of growth.

Ie. More pain will come.

What are the immediate options available to China?

What about the short term though?

Let’s discuss the 3 immediate solutions China can use:

- Conventional Monetary Policy (cut interest rates)

- QE (printing money to buy assets)

- Fiscal Stimulus (giving money to consumers)

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Conventional Monetary Policy

Options here are to cut interest rates, or depreciate the yuan.

China cut interest rates by 0.1% this week, and has generally been reluctant to depreciate the yuan so far.

My view is that both will be of limited use here.

If you depreciate the Yuan, exports will do well. But importers (households) will suffer. So a depreciation of the Yuan effectively boosts exports at the expense of domestic demand, which is not what you want to see when you are trying to boost domestic demand.

Because of this China has (rightly) in my view, been reluctant to depreciate the Yuan in a big way.

Cutting interest rates – this will hurt the banks.

And it doesn’t change incentive to lend in any case, because in China the banks will lend to whoever the central government asks them to lend to.

So cutting interest rates simply hurts bank profitability without any real benefit.

QE (printing money)

QE basically is printing money to fill the real estate bubble.

This works, but it merely reinflates the real estate bubble.

Fiscal Stimulus (giving money to consumers)

Now fiscal stimulus will absolutely work.

If China prints a trillion RMB and hands it out to consumers to spend (like the US did), I don’t doubt that the economy will roar to life.

The problem is whether there is the political will to do this.

As of today that is not clear, but if we see this happening on a big enough scale I think that would mark the bottom.

This is important to watch for.

But there will be no “Lehman” moment?

That being said, China is China.

Everything that happens, happens because it is allowed to happen.

So for the commentators calling for a doomsday Lehman style bankruptcy that takes the entire economy down.

I’m not so sure we will see that happening.

Sure – maybe 5% – 10% probability.

But base case – I think China will manage the drawdown.

It will be a long, drawn out economic slowdown as China reduces its over-reliance on non-productive investment without a commensurate rise in consumption.

But it will be a controlled one – instead of a big bang.

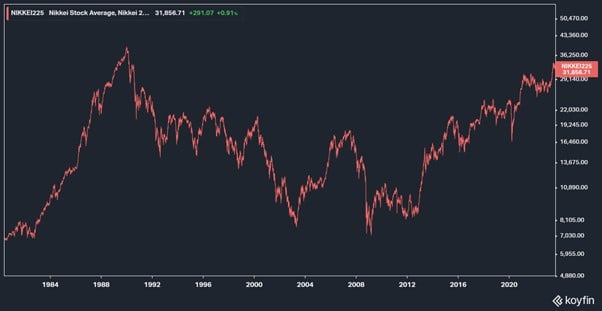

China’s lost decade?

After Japan’s real estate bubble burst.

Japan went through a lost decade.

The Nikkei went on a downtrend from 1989 to 2003, more than a decade.

It has never recovered to 1989 highs, not even today, 34 years later.

If my analysis above holds true, will we see the same for China?

FH… So how do I make money from this?

That’s nice and all.

But let’s get to the important part.

How do we make money from this?

My base case is that we will not see a singular “Lehman” moment for China.

But we will see a long, drawn out period of slow(er) economic growth for China.

In which case there are 2 ways investors can play this:

- Trade – buy when oversold, sell at the top of the range

- Buy dividend stock –ignore price fluctuations, but collect the dividend

If you want to trade China, you’re probably going to get unbelievable volatility, which means plenty of opportunities for aspiring traders.

What would I do? Buy dividend stocks?

The other way I suppose, is to buy dividend stocks.

But like I shared above – the economy is no doubt in a controlled drawdown mode, so you want to be very careful about what stocks you buy.

You want to find stocks where the underlying cash flow is sound, and where the dividend is high enough to compensate for the risk.

You can find names paying 8-10% yields today, which as long as the dividend doesn’t get cut, looks very much like a high yield junk bond.

And you just collect the dividend, while ignoring the day to day fluctuations.

Have I started buying?

I’ve started buying small amounts, but nothing in size just yet.

With the events of the past week, valuations are starting to get very interesting though.

Here is Link REIT – plunged to 2014 prices.

Trading at a 50% discount to book (book value $73), and a 7.2% dividend yield.

This isn’t some small cap REIT mind you, this is Asia’s largest REIT by asset size.

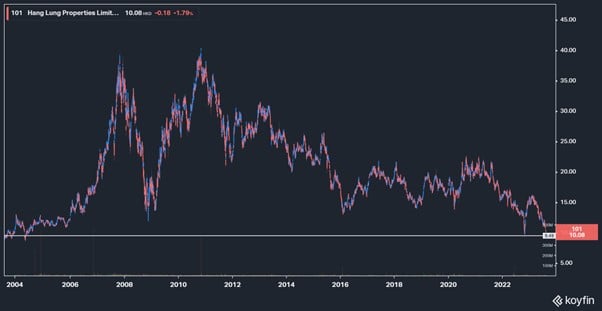

Here’s Hang Lung, a Hong Kong developer.

65% discount to book, and a 7.4% dividend yield.

Here’s ICBC, one of the world’s largest bank and bigger than JP Morgan by asset size.

Trading at 2008 prices – last hit during the depths of the Financial Crisis.

A 9.6% dividend yield at these levels.

Valuations are attractive, and you’re basically looking at decades long support levels here.

So who knows, I may buy bigger positions in the months ahead, depending on how things play out.

As always, I will share fuller thoughts on what stocks I am keen to buy, and when I am buying, with Patreons.

Closing Thoughts: With China, don’t ignore Geopolitical risk

One final risk I need to highlight though – is geopolitical risk.

Let’s say there is a tiny, 2% chance of a China-Taiwan war in the next 10 years.

And let’s say in the unlikely event of a China-Taiwan war, there is a 50% chance of US sanctions against China (similar to what we saw against Russia).

That’s a 1% chance of catastrophic loss in your China portfolio.

So yes, the risk may be miniscule.

But the very presence of this risk, means that you MUST position size well.

As should be the case with any investment – never put in more than you can afford to lose.

I recently updated the REIT & Stock Watchlist on Patreon – that sets out the China related REITs / Stocks I am keen to purchase, and approximate price targets.

Some pretty crazy valuations out there for China and Hong Kong related counters.

Do sign up if you are keen.

This article was written on 25 August 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

– Get up to USD 580 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 580 free fractional shares.

You just need to:

- and fund $300 SGD

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Dear FH,

Another great article. Will you consider sharing a list of big cap, China High dividend stock that is worth looking into?

Thank you

Thanks for the kind words!

It’s shared on the Stock watch on Patreon, there is a China section: https://www.patreon.com/financialhorse

As to whether I’ll do one on the public version of FH, maybe. Let’s see how things play out in the months ahead, and where prices go.

Cheers.

May I ask what you think about ping an?

Pretty similar views to the Big 4 banks.

Investors need to be comfortable with China risk, and the huge black hole on their balance sheets (from real estate debt).

But if you can get comfortable with that, and position size well, then the implicit belief has always been that the SOEs would not cut their dividend.

I’m sure this will be tested in the months/years ahead though, so it’s going to be a bumpy ride to say the least!