Singapore birth rates hit a record low in 2022.

We also see a trend of later marriages, and couples who choose not to have kids at all – DINK (double income, no kids).

Is cost really the predominant concern of declining birth rates? Let’s explore the cost of having a child in Singapore.

Useful checklists for parents-to-be below!

This post was written by a Financial Horse Contributor, with special thanks to Eleanor the Great.

Children no longer part of retirement planning + Rising costs

In response to queries on the declining birth rate, NUS sociologist Tan Ern Ser remarked that likely factors include:

Children increasingly not being seen as part of retirement planning.

At the same time, cost of raising them has risen in an increasingly Vuca (volatility, uncertainty, complexity and ambiguity) world.

More and more resources are necessary to bring up a child, which is also a constraint on the number of children a couple can afford.

Other factors according to Dr Tan include:

- the rise of dual income households, in part to make enough to maintain a middle-class lifestyle

- women’s late marriages

- priorities given to career

- and in turn the lack of work-life harmony in jobs which emphasise deliverables

What exactly are the costs involved?

It is clear that rising costs are a concern, but what exactly are the costs involved?

Let’s explore the details.

In this post, we’re narrowing the scope to the initial costs involving a child (0 – 1 years old), and the financial planning aspects to consider.

Pre-Conception

The pre-conception phase is not commonly discussed but worth planning for.

There are 3 main categories to think about:

- Fertility checks

- Health checks

- Insurance

- Life, Hospital, Maternity

Some additional costs for pre-conception include vitamins (folic acid is highly recommended).

In the pre-conception phase, it is advisable to undergo fertility & health checks. This is something that many young couples may not think about in their planning stage.

Fertility checks are often recommended to advise parents-to-be on the best course of action.

And health checks are useful to understand any underlying health conditions that may complicate pregnancy or birth, as well as genetic conditions to monitor.

At this stage, especially with the benefit of health checks, consider getting the appropriate insurances to protect your family.

This includes, life, hospital, maternity and even income insurance, according to your needs.

Post-Conception

In the post conception stage, these are the important planning considerations:

- Choice of birth plan (gynae, and hospital)

- Pre-natal testing

- Childbirth and childcare classes

- Cord blood banking

- Baby logistics preparation

- Will and CPF nomination

- Maternity / Baby hospitalization insurance

Let’s go through each category.

Choice of birth plan

The cost of giving birth in Singapore depends largely on your choice of gynae + hospital.

In general, private tends to be more expensive, but public hospitals also offer a comparable ‘private’ option.

With private gynaes/hospitals, you tend to get a better customer care experience.

With public hospitals, unless you opt to be a private A class ward patient, you can’t choose your gynae. There is also often long waiting times (even as a private patient).

That being said, Singapore public hospitals offer oustanding medical care and facilities, and you can certainly put your trust in them.

Take note that in any emergency, most hospitals are actually obliged to transfer the patient to KKH, as they have the best medical facilities and personnel for infants in Singapore.

Pre-natal testing

As a subset of the above, pre-natal testing is one of the larger costs during the pregnancy stage, as part of your gynae visits.

Some private gyanes offer a package, and you can consider if it is worth it for you.

Additionally, it is good to read up on pre-natal testings, and what is important for you. The most common one is the NIPT at around week 12 to screen for genetic issues and gender.

Childbirth and Childcare classes

These are optional classes. Consider also expanding your search to cheaper alternatives or just searching on the internet, as there are many useful resources available.

One important class to consider is baby CPR. There are also useful information on this online.

Cord blood banking

Cord blood banking is also optional, and something to think about.

The cost is generally around $5 – $10k. You can also choose to donate your cord blood for free!

Baby logistics

Baby logistics will probably be the major administrative category for parents-to-be. The list of purchases can be endless!

Big purchases include:

- crib

- stroller / baby carrier

- car seat

- changing table

- nursing chair

- optional but parents and their backs love them

and other baby consumables including:

- bottles

- clothes, towels, bedding

- diapers, wipes

- baby soap, shampoo, diaper cream, nail clipper, laundry detergent

- bottle sterilizer

- diaper bin

Maternity / Baby Insurance

Maternity insurance is optional, and can be useful for certain individuals. Do take a look at the specifics of what maternity insurance can cover. Also, generally it is advisable to buy maternity insurance early before any genetic testing results.

For baby hospitalization insurance, this is usually highly recommended, as you don’t want to be worrying about hospital bills if there is a scenario where your child needs to be hospitalized.

As post-birth is usually a very frantic time, now would be a good time to liaise with your insurance agent to consider getting the right baby hospitalization plan for you.

Once you have everything set up, you usually can finalize the plan around 2 weeks after the birth of your child. And get your agent to remind you!

Will and CPF Nomination

This aspect is often overlooked.

If you’re intending to welcome a child, you may wish to think about drawing up a will and also adjusting your CPF nomination to benefit your spouse/child.

Post-Birth

Post-birth costs can be broken down into 2 primary time frames.

0 – 4 months post

Major costs can include:

- post-partum recovery

- confinement arrangement

- helper

Confinement and post-partum

Confinement refers to the period post-birth where the mother engages in post-partum recovery.

In this time, many choose to employ a confinement nanny to guide them through the recovery process and learn the ropes of handling an infant.

There are major confinement agencies in Singapore that can be a reliable way to engage a nanny.

All of these agencies will provide nanny profiles and reviews, so you can browse to get a good fit.

The price ranges from 3.5k – 5k/month.

Most people engage nannies for a period of 4 – 6 weeks, but there are also longer-term options available (usually up to 4 months).

The benefit of going through an agency is that you are guaranteed a nanny, and the nannies usually undergo mandatory training and have some experience.

The agency also usually provides free substitution, so you may substitute the nanny with a replacement (which is super helpful if you find that you don’t get along for any reason).

Whereas, hiring freelance nannies tend to be cheaper, but comes at certain risk (difficult to switch, no guarantees), although some people prefer it if they have a reliable recommendation.

Alternatively, confinement centres are also available, where you and baby will stay full-board on location, with in-house staff supporting you.

The cost tends to range higher because of the baseline accomodation costs that are factored in (think of it as staying in a 4/5* hotel for a month). This means that prices can start from 10k+/month, with luxury offerings up to 30k++.

Confinement centres provide an all-in-one experience with a lot of institutional in-house support, including professional medical staff and relaxation perks like massages.

At the same time, as first-time parents, it may be that having an experienced nanny coming to your own house to help you with the entire set up and day-to-day of taking care of a newborn may actually be much more helpful in a practical sense.

You may also wish to budget for post-partum recovery, which may include rehabilitation exercises and therapy, and other medical costs.

Helper

Some households may also choose to engage a helper or part-time helpers to assist with housework and/or childcare.

Generally, you should start the search for a full-time helper 2 months before you need it.

In this case, you may wish to start while being pregnant, as there are certain administrative procedures involved, and you will also need some time to get to know and train your helper.

Cost of engaging a helper ranges from about $600 – $1k.

4 months (or when maternity leave ends) to 18 months

When maternity/paternity or flexible work arrangements come to an end, it would be necessary to line-up childcare arrangements.

These are the most common arrangements:

- infant care

- play group / pre-school

- stay-at-home parent

- grandparents or other familial assistance

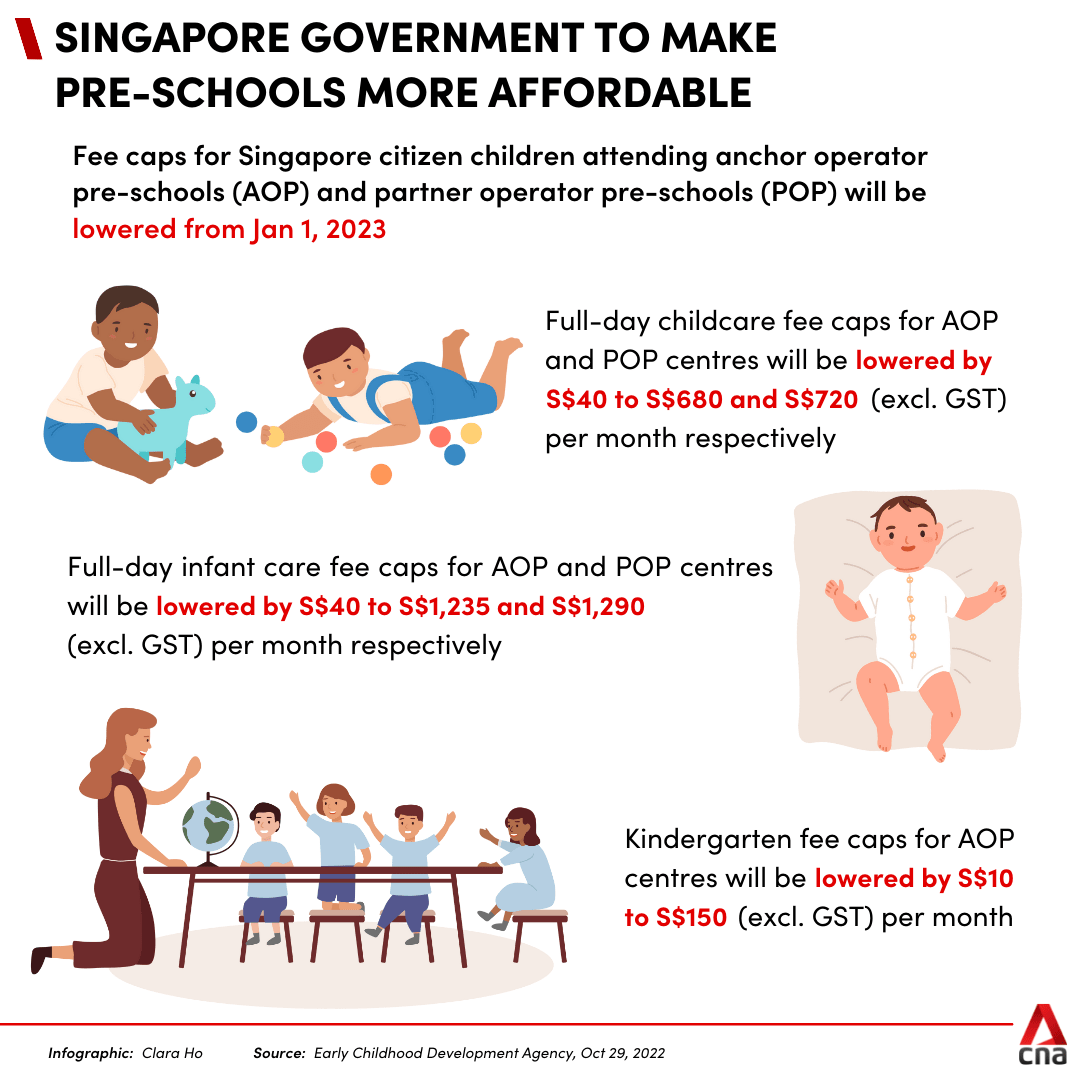

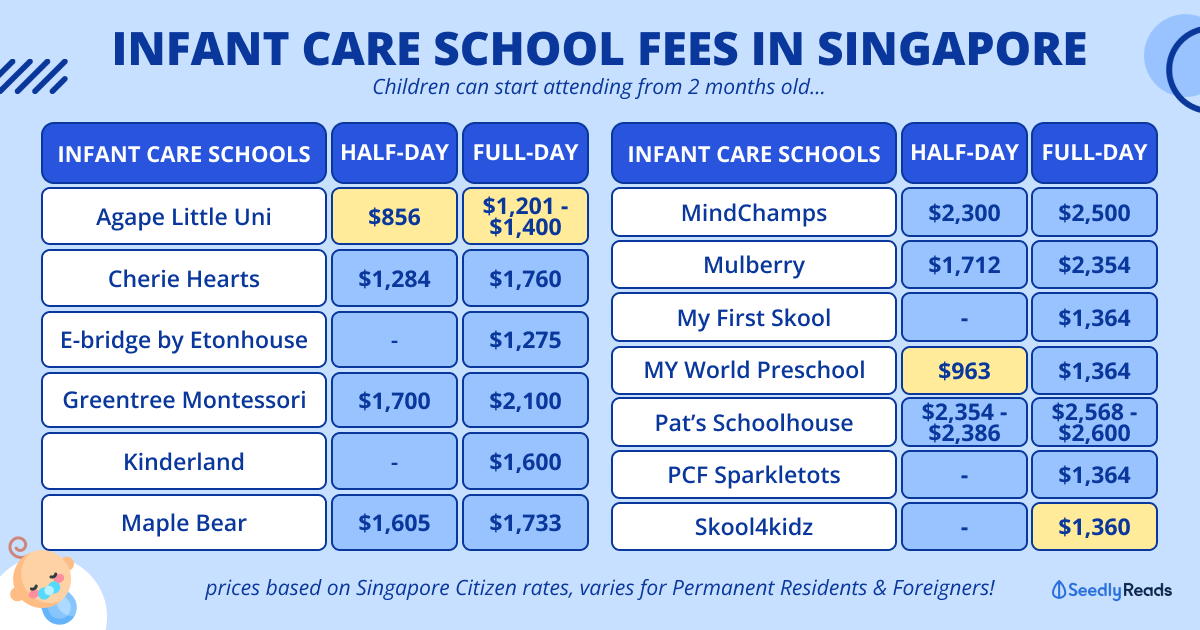

The biggest cost will be sending your child to a “school”, either infant care (<18 months) or playgroup / pre-school (18 months +).

Infant care in particular is very popular, so you do need to plan for this well ahead of time.

Especially if you live in a popular neighbourhood and wish to book government pre-schools, you may need to firm up your choice at least 6 months prior.

So do book school tours as early as possible!

If you have plans for non-centre related childcare arrangements, for instance, being a stay home parent or having grandparents help, this is also a good time to take stock of your financial situation.

This would be time to have a discussion with your spouse on the family’s financial situation, future career plans and any other logistical issues that may require budgeting for.

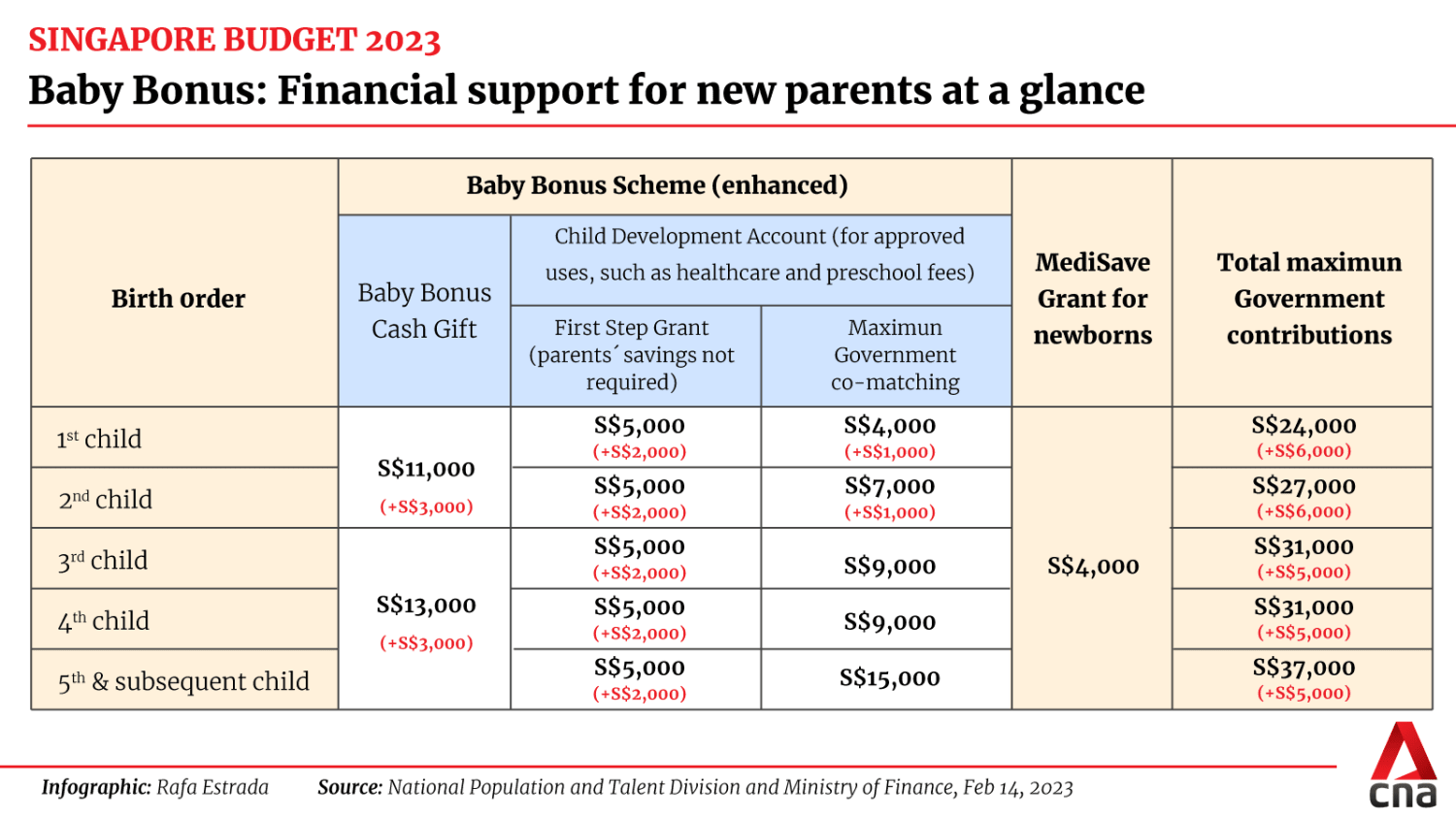

Don’t forget your baby bonus!

If you’re reading this and feeling worried, do know that you are entitled to support from the government.

Baby bonus and other childcare subsidies are available to help support you.

Check out our guide on baby bonus and parenthood tax rebates!

Concluding thoughts

As earlier mentioned mentioned, couples who choose to have kids, increasingly do so without the thought of kids being part of their retirement planning.

In other words, modern day parents are very mindful of their choices.

Fears around the costs involved in having a child should not be overplayed, but carefully understood and budgeted for.

In fact, there is also a saying that kids bring wealth to the household.

There is some evidence to back this up, chiefly that families tend to commit to a larger home, and hence accumulate a larger real estate asset, and also that there is more motivation to be financially prudent.

So embracing a future with kids if you choose to do so, can be very rewarding in more ways than one.

Parents, do you have any budgeting advice for those planning to have a kid? Share your experience in the comments below!