We all know Singapore investors love banks stocks.

It’s been quite a while since my last article looking at the Singapore banks.

And we’ve had quite a few developments since:

- DBS announcing bonus shares

- Latest Q4 2023 earnings release

- Big changes in the macro space

So I wanted to take a refreshed look at the Singapore banks today.

DBS Bank pays a 7.0% dividend yield if you count the bonus shares – does that make DBS the best bank stock to buy today?

And how might the next 18 months play out for the banks?

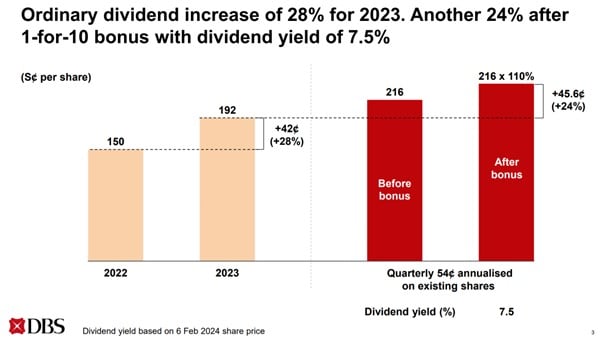

DBS Bank pays a 7.0% dividend yield after bonus shares – better than most REITs

In the latest Q4 2023 earnings result, DBS announced a bonus share issuance.

For every 10 shares an investor holds today, they will get 1 bonus share.

There’s been a lot of confusion over what exactly this means for existing investors, so I’ll try to clarify it here.

Does this affect DBS’s Share Price ?

Theoretically this does not affect DBS’s “share price”.

Think about it this way.

If DBS is worth $85 billion today, increasing the share capital by 10% doesn’t change that.

What it will change is the price of each share, which should theoretically go down after the bonus issue (to reflect the higher share count).

Does this affect DBS’s Dividend yield?

What it does change though, is the dividend yield.

DBS intends to maintain the dividend yield of $0.54 per share.

Which means that for existing investors, you are technically getting a 10% increase in dividend yield (because of the bonus shares).

Running the numbers.

Quarterly dividend of $0.54 * 4 * 110% = $2.376

$2.376 dividend – based on DBS’s latest stock price of 33.93 – works out to a 7.0% dividend yield.

Very attractive yield – higher than most blue chips REITs like Ascendas REIT (5.6%) or CapitaLand Integrated Commercial Trust (5.5%).

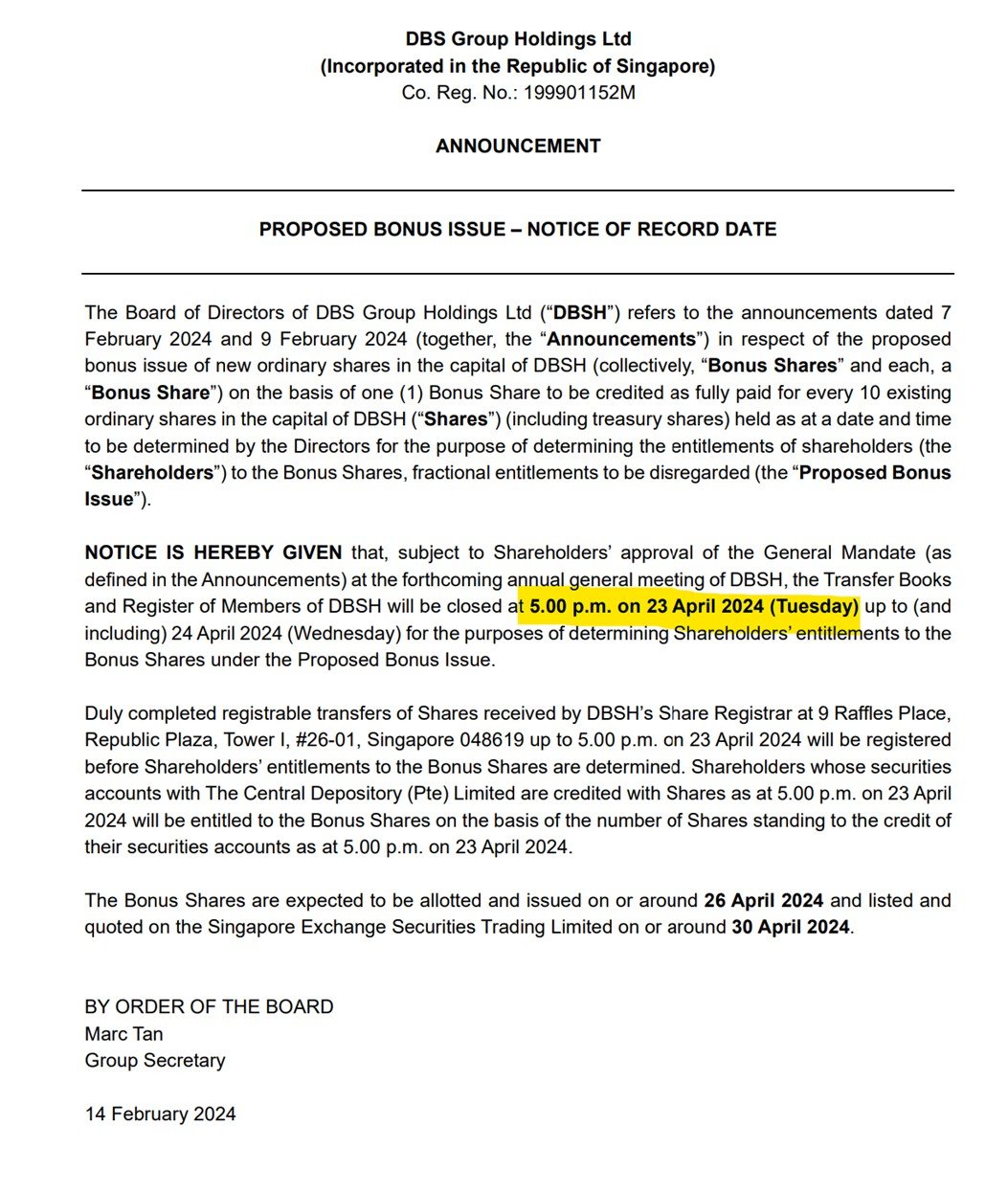

What is the cut-off date for the DBS Bonus shares issuance?

From the SGX Announcement:

the Transfer Books and Register of Members of DBSH will be closed at 5.00 p.m. on 23 April 2024 (Tuesday) up to (and including) 24 April 2024 (Wednesday) for the purposes of determining Shareholders’ entitlements to the Bonus Shares under the Proposed Bonus Issue.

This means that the DBS shares will trade ex bonus on 22 April 2024 (Monday).

In plain English, because of T+2 settlement – if you buy on or before 19 April (Friday) you will get the bonus shares, if you buy on or after 22 April (Monday) you will not get the bonus shares (and vice versa).

Dividend yield of DBS compared to OCBC and UOB Bank

Compared to the latest dividend yields for the other 3 banks:

|

Bank |

Dividend yield |

|

DBS |

7.0% |

|

UOB |

5.9% |

|

OCBC |

6.3% |

You can see how DBS’s dividend yield stands heads and shoulders above UOB and OCBC.

DBS Share price has outperformed OCBC and UOB this cycle

In fact if you look at DBS’s share price – it has been by far the strongest performer as well.

Including dividends, since Feb 2020 (right before the COVID crash):

- DBS Bank is up 64%

- OCBC Bank is up 47%

- UOB Bank is up 33%

There is no free lunch – what is the catch?

As my favourite saying goes – there’s no free lunch in investing.

Or – if something is too good to be true, it usually is.

Looking at the numbers above – DBS pays the highest dividend yield, and DBS’s share price has been performing the best since 2020.

By this logic DBS should be the “best” bank stock for investors to buy?

What’s the catch?

But – DBS’s Price/Book is much higher than OCBC / UOB

The catch I suppose – is that DBS is a lot more “expensive” than UOB and OCBC.

|

Bank |

Price/Book |

|

DBS |

1.49 |

|

UOB |

1.05 |

|

OCBC |

1.1 |

At 1.49x book value, you’re paying almost top dollar for the stock – close to the highs in the past decade.

Which means that if there is economic weakness, or if the bank executes poorly, there could be a long way to go on the downside.

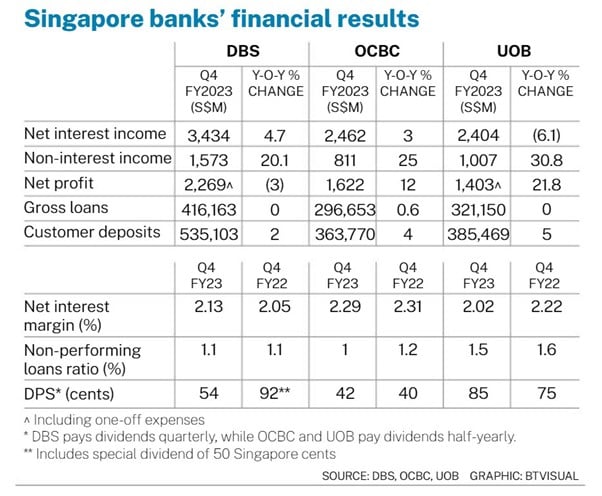

Comparing DBS’s financial results vs UOB and OCBC Bank

Let’s dive a bit deeper into the financial results of DBS vs UOB and OCBC Bank, to decide if this premium is worth it.

Business Times has a great table summarising the Q4 2023 financial results for the 3 banks:

2 key takeaways from me:

- Loan growth is slow for all 3 banks (flat vs last year)

- Net interest margin is going down

Loan growth is slow for all 3 banks (flat vs last year)

Loan growth for all 3 banks is flat vs 2022.

Quarter on quarter – DBS and OCBC’s loan book fell by 1%, while UOB rose by 1%.

Both OCBC and UOB expect low single-digit loan growth in 2024, “reflecting low appetite for new loans in a higher interest rate environment”.

It’s interesting that the reason OCBC/UOB gave for slow loan growth is low demand.

From what I’ve been hearing in the market, banks are not super keen to extend loans too, especially to weaker borrowers (due to fears they cannot be repaid).

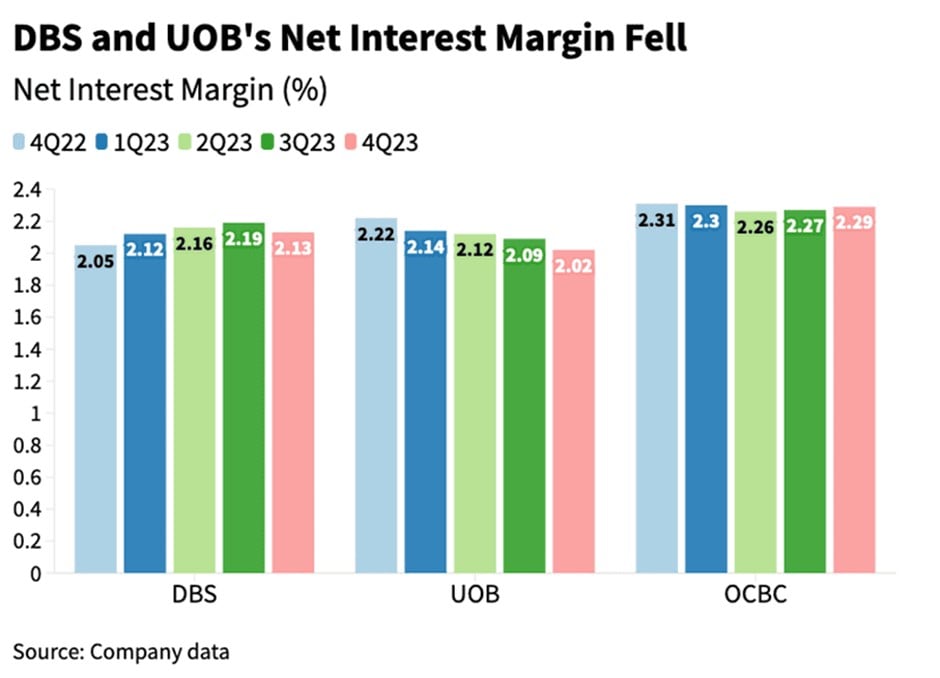

Net interest margin going down

I’ve summarized the quarter on quarter net interest margin for the 3 banks below.

Flat at best (OCBC), down low single digits at worst (DBS and UOB).

Beansprout has a chart plotting net interest margin over the past 5 quarters – generally flat / down.

In terms of forecast – all three banks are expecting slightly weaker net interest margins in 2024.

DBS expects net interest margin in 2024 to be slightly below the fourth quarter margin of 2.13%.

OCBC expects its net interest margin in 2024 to be in the range of 2.20% to 2.25%, below the net interest margin of 2.29% in the fourth quarter.

UOB’s net interest margin guidance for 2024 has also been lowered to about 2.0%, based on the margin it was able to achieve in the fourth quarter.

What does this all mean for DBS Bank stock (or UOB or OCBC Bank)?

If you take the banks’ forecast at face value.

They are expecting flat loan growth, and net interest margins to come down slightly.

This means profits to stay around current levels, without a big move up or down.

If so, you would probably expect share price to stay rangebound around current levels, but of course there is a juicy 7.0% dividend yield to go with it.

For what it’s worth – this is in line with analyst expectations on the Singapore bank stocks – flat, with a juicy dividend yield.

But… can the bank’s own forecast be wrong?

That said – if you are an active investor.

There is no money to be made by accepting the market view.

The real money is made if you think the market is pricing in x view, whereas you think in reality y is going to happen.

So the question we want to ask – is how can the bank’s own forecast be wrong?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

What is the outlook for interest rates / economic growth?

To understand how banks share price moves, you need a view on 2 things:

- Interest rates – which affects net interest margin above

- Economic growth – which affects loan growth / loan default rate

High interest rates, strong economic growth, is the holy grail for banks.

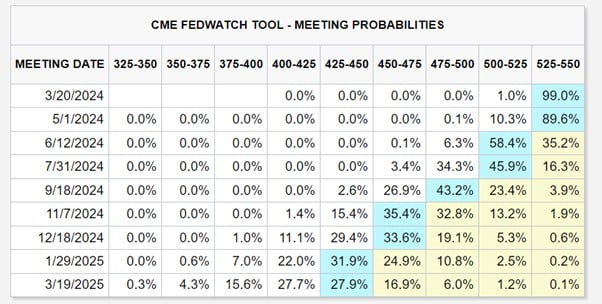

Interest Rates Outlook?

Latest US inflation data this week is showing US inflation stabilizing around current levels (3-4% year on year).

Month on month inflation is no longer going down and starting to trend up.

The market reaction to the hot US inflation print this week was very instructive.

And what was the market reaction?

Stocks, commodities, gold, bitcoin all went up.

If you recall – there was a time in this cycle where hot inflation prints were bad news for the market – as they meant higher interest rates from the Feds.

Well, that time is gone.

The market is calling Jerome Powell’s bluff at this point.

US inflation is going to stabilise at the 3-4%, and stop going down (unlikely to hit the Fed’s 2% target).

BUT – the Feds are going to cut interest rates anyway, because it’s an election year.

The market is pricing in 3 interest rate cuts in 2024:

On the face of it, this would not be good for banks.

Economic Growth outlook

That said – the other piece of the puzzle is economic growth.

Let’s put it this way.

Inflation hasn’t been tamed for good, economic growth is resilient, and the Feds are going to cut interest rates. All while the US government is running a record budget deficit.

I don’t need a PhD in economics to figure out what happens next.

Now you can see why cyclicals, commodities, gold, bitcoin – all went up this week.

This actually makes me nervous about a potential repeat of the 1970s.

Every time the Feds ease, inflation comes back, requiring a second tightening cycle – that played out over a whole decade.

Based on what we’re seeing today, there is a decent chance this may happen.

But hey – this would be bullish risk assets in the short term.

And it won’t be bad for banks I suppose, as it means stronger economic growth in the short term, offsetting the lower interest rates.

Technical Analysis of DBS Bank Stock – potential break out this week?

DBS’s share price has been generally range bound since 2022 and the start of this interest rate hike cycle.

This past week though – we saw a potential breakout from the current trading range since 2023.

Is the market seeing what I’m seeing too?

Would I buy DBS bank stock?

If you would recall, I flipped to being neutral on the Singapore banks early this year.

My thinking then was that the Feds would cut interest rates into an election year, leading to a potential resurgence in economic growth / inflation.

However, I never bought the Singapore banks in the end, because I figured if I was right on this – stuff like Commodities, Gold, Bitcoin, US momentum stocks – they’re going to jump more than the Singapore banks (you can see my full portfolio breakdown on FH Premium).

What we’re seeing so far, seems to confirm this general macro view.

What is the risk-reward for DBS Bank stock at this price?

But let’s relook the risk-reward for DBS Bank stock.

Long term Price/Book of DBS Bank is set out below.

Let’s say best case P/B goes back to 1.7x.

That’s 14% capital gains.

Throw in the 7% dividend yield, it’s potentially around a 20% return in a year.

That’s pretty decent, but of course this is quite an optimistic best case scenario.

The downside of course is if we have a recession / rapid interest rate cuts.

So far at least, data isn’t pointing at that.

But I would not rule it out.

Let’s say there is a mild recession, P/B goes to 1.2x.

That’s about a 20% capital loss.

So this is probably the downside case.

Will I buy Singapore banks in 2024?

In Jan 2024 I said that I was keen to pick up a position in OCBC bank.

And yet I never did – I bought a mix of commodities and Bitcoin and US tech / AI stocks instead.

All of which have done much better than the Singapore banks to date.

Does that change today?

I’m inclined to just pick up a small position in DBS bank or OCBC bank just to anchor the price psychologically.

But I find it hard to pull the trigger and open a big position in the Singapore banks today.

If I am right on the cyclical upswing – there’s way bigger money to be made in stuff like commodities / Bitcoin / US Tech (you can see my full watchlist and price targets on FH Premium).

If I’m wrong on the cyclical upswing – the bank stocks are going to be rangebound at best, in which case the 7% yield is only a 3%+ yield spread vs risk free T-Bills.

While if we do get a recession / rapid interest rate cuts, there could be a fair bit of downside risk for the banks.

So that’s my view as of today, but I reserve the right to change my mind any time if facts change.

As always – I share latest updated macro views on FH Premium.

This article was written on 15 March 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

– Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

certainly like your website but you need to take a look at the spelling on quite a few of your posts Many of them are rife with spelling problems and I find it very troublesome to inform the reality nevertheless I will definitely come back again

Thanks – will proofread more closely going forward.