Imagine my surprise when I saw the headline this week:

“DBS chief Piyush Gupta sells $3.4 million worth of shares in bank”

And this was the Straits Times mind you.

So I continued reading, and here’s what the article said (emphasis mine):

“DBS Group Holdings chief executive Piyush Gupta has sold 100,000 shares in the bank, netting him around $3.4 million, according to documents filed with the Singapore Exchange on Tuesday.

Mr Gupta sold 8,100 shares at $34.32 each and 91,900 shares at $34.2553 each in two separate open-market transactions on Friday.

Together, the shares sold accounted for 4.4 per cent of his DBS holdings.

He still owns 0.085 per cent, or 2,185,721, of the ordinary shares in DBS, under a trust arrangement.

Mr Gupta sold his shares a day after DBS trounced forecasts to announce a record $2.69 billion in net profit for the second quarter of 2023.”

Does Piyush Gupta selling his DBS Shares even mean anything?

I know what you’re going to say.

FH… hold your horses.

Piyush only sold 4.4% of his shares.

He still holds another 2,185,721, or 95.6% of his shares before he sold.

Worth a whopping $74 million.

Selling 4.4% frankly means nothing.

Okay… fair enough.

Piyush Gupta sold $3.3 million in DBS shares in 2022 as well

I dug a bit deeper, and it turns out Piyush Gupta also sold 100,000 DBS shares in 2022 (worth $3.3 million).

So it seems that Piyush has sold $3 million worth of DBS shares for 2 years in a row.

Perhaps he needs it to fund his personal expenses, I don’t know.

But that got me thinking.

Maybe I’m just being a paranoid horse.

But let’s play devil’s advocate here.

What might Piyush see about the future that we are not seeing?

DBS is firing on all cylinders here

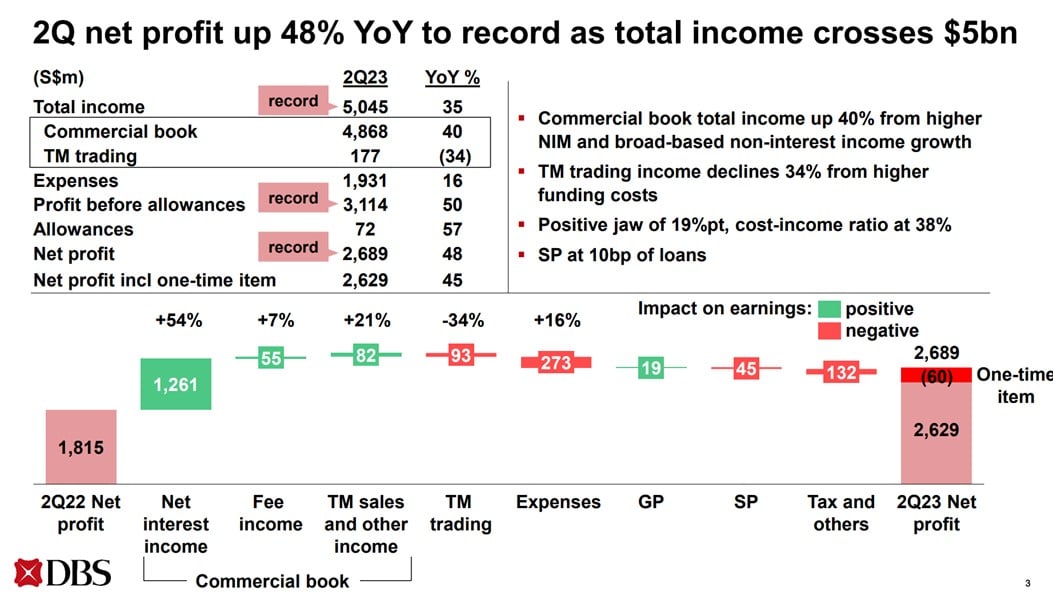

What’s even more striking is that Piyush sold his shares the day after DBS reported a blowout Q2 earnings.

You can see the financial results below.

Q2 profit up 48% year over year.

Net Interest margin has gone from 1.65% in early 2022, to 2.81% in the latest quarter.

That’s almost a doubling in net interest margin, which just goes to show you that banks make out like absolute bandits in a rising interest rate scenario.

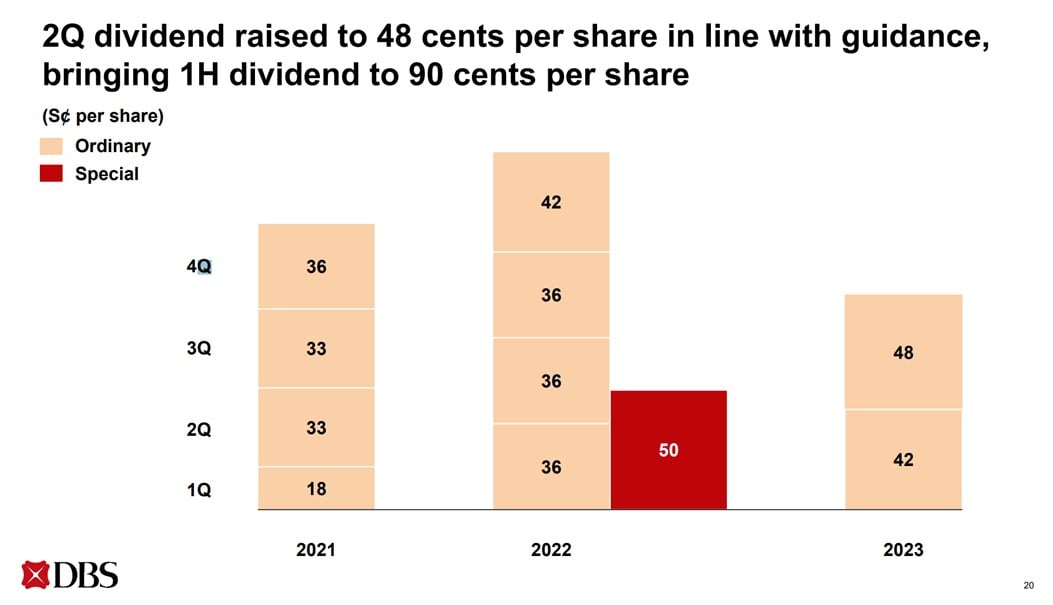

DBS raises dividend to 48 cents – 5.5% dividend rate

In fact DBS just announced a dividend raise (as did UOB and OCBC).

Q2 dividend is raised to 48 cents per share.

At current price of $34.3, that works out to a 5.5% dividend yield.

All good so far right?

As a DBS shareholder (which I am), what worries me most?

Full disclosure that I am a DBS and UOB shareholder.

Yes I have taken profit in both positions this cycle, but I still hold meaningful positions.

As a DBS shareholder – what worries me most about the next 12 – 18 months, hypothetically speaking?

Basically, it’s lower earnings from DBS’s core lending business.

Say what you want about diversifying the business – but the core lending business is still the bulk of the business at 67% of the income.

What could cause the core lending business to suffer?

It’s 2 things:

- Interest rates going down quickly – lower lending margins

- Recession – rising defaults

Okay, you can argue that they’re actually the same thing, because a recession will mean interest rates go down quickly, and interest rates will only go down quickly in a recession.

But you get what I mean.

Will Interest Rates go down quickly?

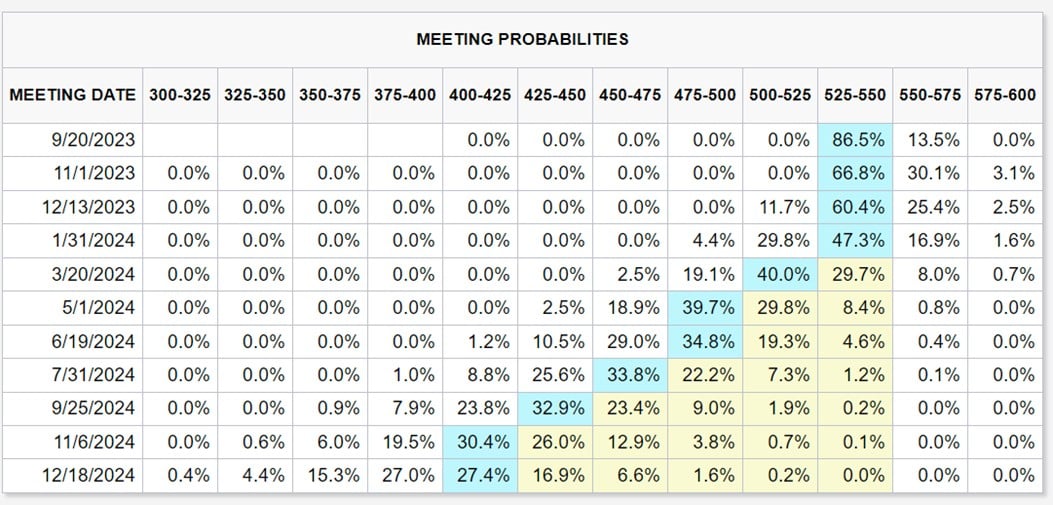

Here’s what’s priced into the futures market today.

Market thinks interest rates stay at current levels until Jan 2024.

Before 5 interest rate cuts in 2024.

If you believe this market pricing, then you’ll accept that we are close to peak interest rates today, and the only way for interest rates to move is down.

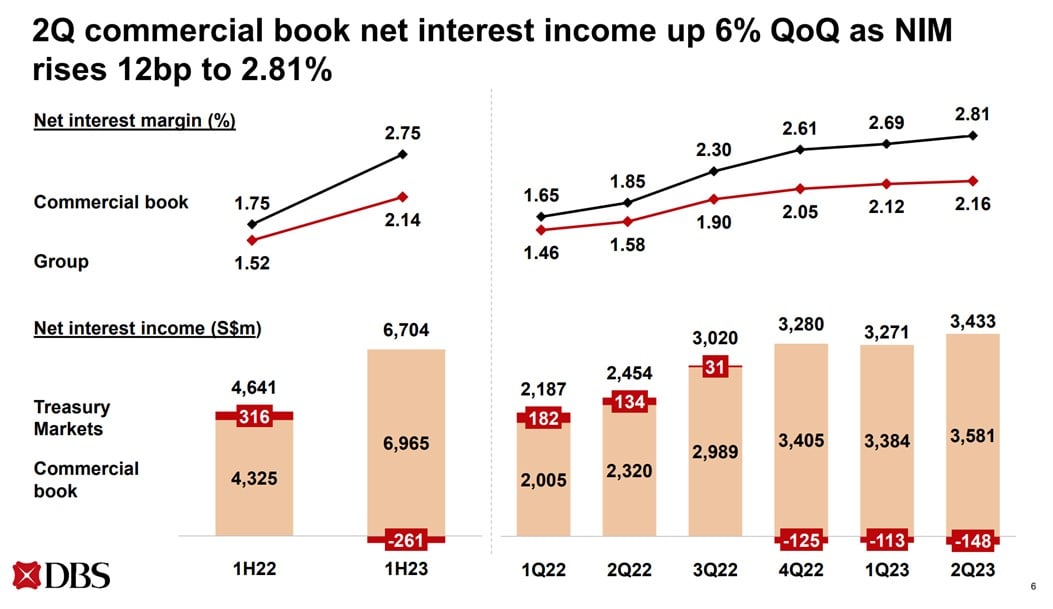

But… DBS has a huge deposit base to “borrow” from

Of course, headline interest rates is just one part of the story.

If DBS lends out at a lower rate, they can still make money if they borrow from you at an even lower rate.

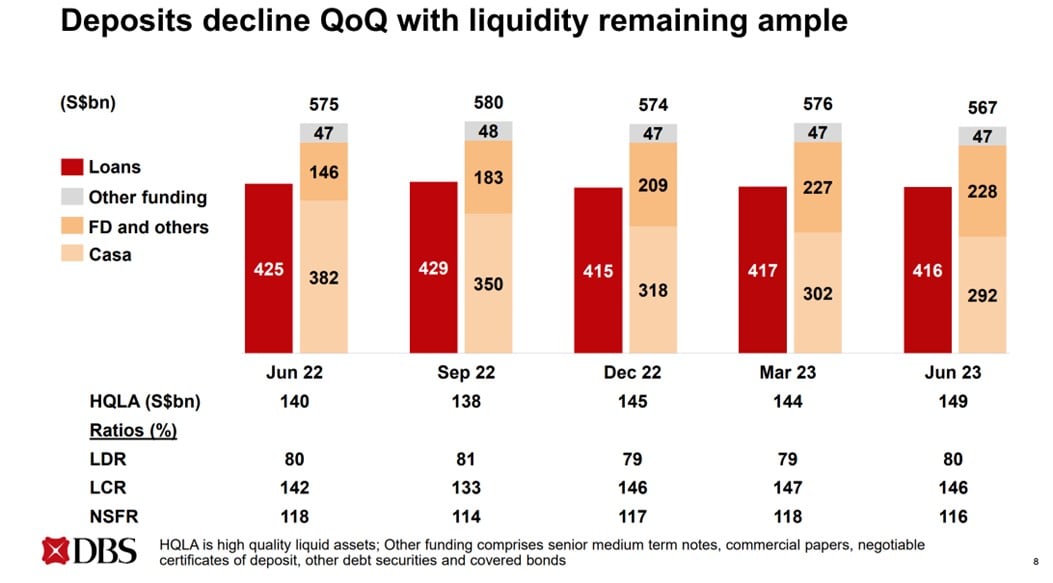

And you can see DBS’s deposit base below.

Yes it did decline by 1.6% this quarter.

But by and large DBS still has a rock solid deposit base to “borrow” from.

And c’mon, all us fixed deposit junkies will know that DBS pays one of the worst Fixed Deposit rates out there, and yet their deposit base is still massive.

This means that DBS’s borrowing costs is much lower than the other banks, which could given them a huge competitive advantage even if interest rates were to go down in 2024.

Will we see a Recession?

What about a recession?

If we have a recession and loan growth slows, or loans start to default, that could really wreck DBS’s earnings.

Let’s see what DBS themselves have to say on this.

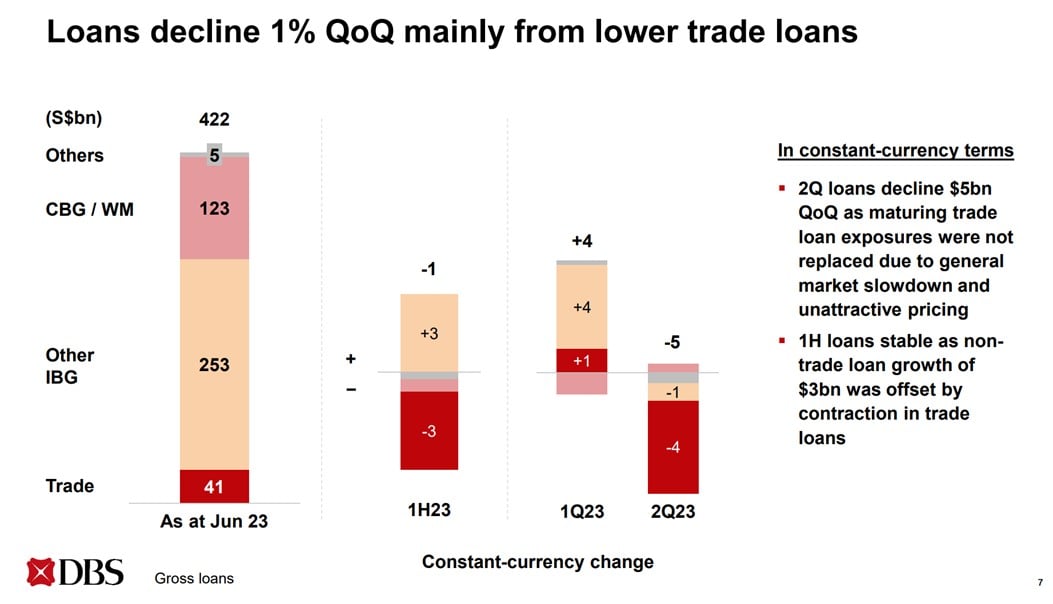

Loan growth is slowing?

Per DBS’s own words:

2Q loans decline $5bn QoQ as maturing trade loan exposures were not replaced due to general market slowdown and unattractive pricing

An analyst posed this question to Piyush on the earnings call:

“Q: On loan growth, where are the pressure points? Is it Hong Kong because of the higher rate environment than you initially assumed? Is it the mortgage market in Singapore?”

Here was Piyush’s response, emphasis mine:

On loan growth, it is all of the above.

In the second quarter, the trade book shrank by $4 billion due to a general slowdown and low pricing.

For the non-trade book, we got $3- $4 billion of loan growth everywhere else, but lost $3 billion from the shift from Hong Kong to China.

In Singapore, mortgages will be slower than we expected. I was hoping they would grow about $1 billion this year, but we will probably wind up at $500 million-750 million.

My estimate now is that we should have about $5 billion of overall loan growth in the second half, resulting in 1-2% of loan growth for the full year.

Loan growth appears to be slowing

I’ve been talking to people in the market generally, and what I’m hearing is that loan growth is slowing.

Banks are becoming less keen to lend despite higher interest rates.

Because they are afraid that the borrowers will not be able to repay the loans.

This is very big if true, because a drying up of bank credit means less credit creation means less economic activity.

So I went to double check against the latest quarterly earnings of all 3 local banks.

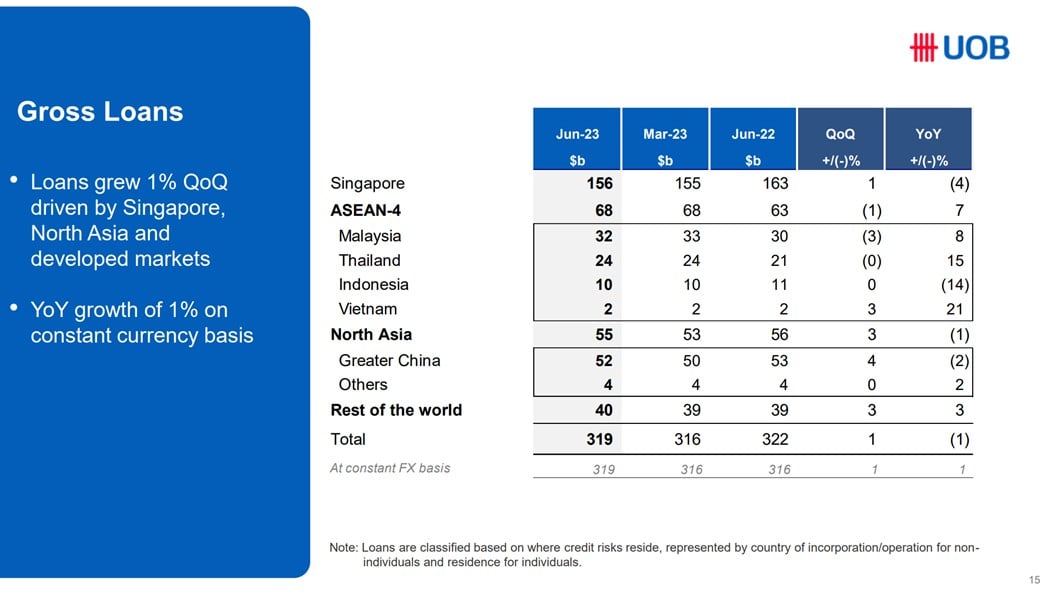

UOB is showing 1% quarter on quarter increase in its loan book (down 4% year on year).

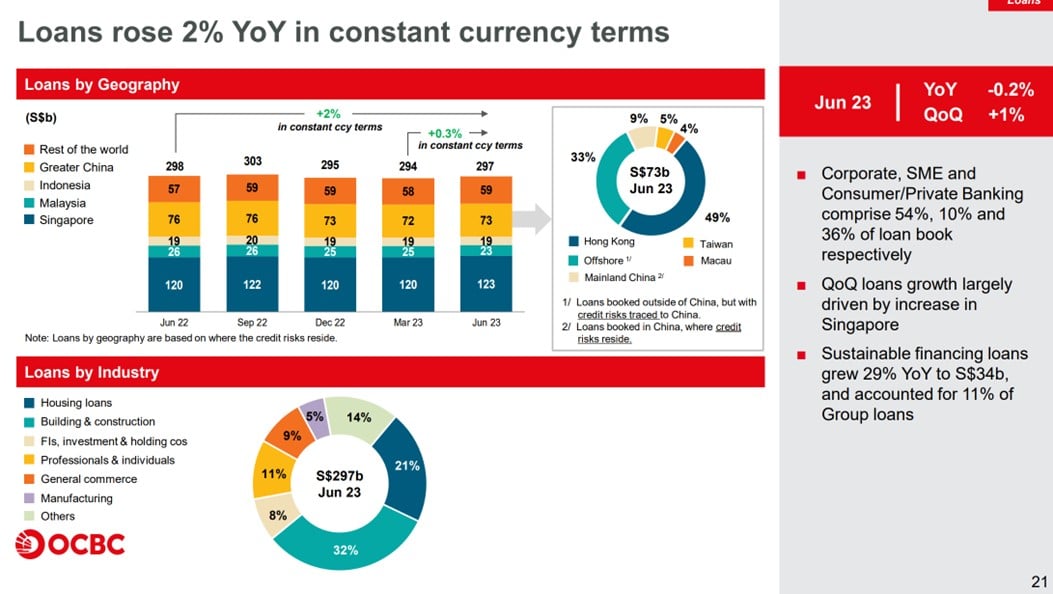

OCBC is showing 0.3% quarter on quarter increase in its loan book (up 2% year on year).

While DBS itself, is showing 1% quarter on quarter decrease in its loan book (up 2% year on year).

So.. Q2 loan book growth is about flat to slightly negative depending on the bank.

Indeed, it does look like loan growth has slowed, but the big question mark is whether it will stabilize or continue to slow further.

Piyush himself is forecasting 1% full year loan growth for 2023:

“My estimate now is that we should have about $5 billion of overall loan growth in the second half, resulting in 1-2% of loan growth for the full year.”

What does this all mean?

Now banks are fair weather friends.

Business owners will know what I mean.

When you don’t need money, the banks are eager to lend you money.

When you actually need money, no bank will touch you regardless of how high interest rates are (because you know… possibility of default).

So banks are a powerful pro-cyclical factor – and watching banks’ loan books offers you powerful insights into the economy.

When the economy booms, banks lend a lot, driving the economy up even higher.

When the economy slows, banks pull back on lending, slowing the economy even further.

It’s a bit of chicken and egg I know, but I generally holds true.

So flattish loan book growth for the banks is never a good sign.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

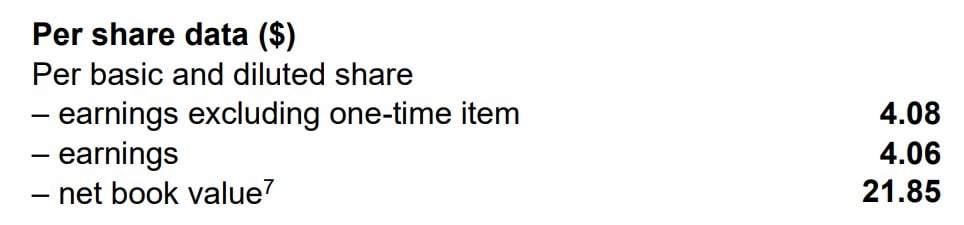

What is priced in? DBS Book Value is $21.85

In times like that, it’s helpful to understand what is priced in.

DBS’s book value is $21.85.

At current share price of $34.3, that works out to 1.56x book value.

Boy… that’s pricing in a lot of growth right there, for a bank that is growing its loan book at 1-2% this year, and where the market is pricing in 5 interest rate cuts next year.

You can see the 20 year Price/Book chart for DBS below.

At 1.56x you’re getting close to 2019 levels, although still healthily below 2007 levels of 1.9x book value (thankfully).

My Personal View on DBS?

As shared above, I am a DBS and UOB shareholder.

I have taken profit in both positions this cycle, but I still hold onto the remaining positions.

Will I sell my remaining DBS / UOB shares?

Probably not.

Who knows DBS might soar to 2.0x book value like in 2007, and I would look very silly with no position at all (like I did with NVIDIA).

So whatever position I have in DBS currently, I think I’ll continue to hold.

Will I buy more DBS Bank Stock?

The tricky question is whether I will buy more DBS Bank Stock.

Regular readers will know that I am not married to any of my positions, and I have no problems changing my mind.

I can be convinced DBS is going to $20 today, and tomorrow I might buy $50,000 worth of DBS if I think I was wrong.

Patreons get latest updates on my portfolio moves and thinking, so do sign up if you are keen.

Will I buy more DBS Bank Stock today?

I really don’t think so.

I can’t help but shake the feeling that the way the economy is set up.

The risk to banks is more tilted to the downside than the upside here.

At 1.56x book value, you basically need a soft landing with mild interest rate cuts in 2024 to justify the price.

But if you’re wrong – and you get a bigger economic slowdown than priced in, or faster than expected interest rate cuts, that 1.56x book value starts looking very pricey.

Just to be clear – I’m not saying DBS share price is going to go down.

I’m just saying that at this price, risk-reward doesn’t look that great.

I see better opportunities elsewhere

The way I see it.

At this point in the cycle.

I want to start thinking about playing the reversal in interest rates.

I want to buy asset classes that do well if interest rates go down.

I wrote about Treasuries for Patreons this week, as a potential play I am buying.

REITs, maybe tech, those are interesting to me as well, and you can see how I am positioned and what I am keen to buy on Patreon.

But DBS at 1.56x book value?

Sure, I will hold what positions I have, but I’m not sure if I will add new money here.

Closing Thoughts: I know a lot of you dividend investors love DBS… don’t let me stop you

I know a lot of you long term dividend investors love DBS, UOB and OCBC.

When you get paid a higher dividend to put your money in the bank stock than in that bank’s fixed deposit, yeah I get why you guys feel this way.

If you’re a long term dividend investor, don’t let anything I say above change your mind.

I’m more of an active macro investor so perhaps my style is different from yours.

If your plan is to buy DBS and hold it for the next 20 years through rain or shine, it’s a completely different story.

Over a timeframe like that, you’re basically just playing Singapore’s economic growth, and anything that happens in the next 2 – 3 years is just short term noise.

This article was written on 11 August 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

WeBull Account – Get up to USD 580 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 580 free fractional shares.

You just need to:

- Sign up here and fund $300 SGD

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

A timely piece of analysis; I’ve been trying to get more info ever since I saw this piece of news. I think what really struck me more was the timing; he sold off those shares pretty much just before the Ex-Date, considering that the dividend was at $0.48 per share.

Although I’m a long term dividend investor, I don’t disagree with you at all:

1) Definitely holding onto my bank stocks but for sure I’m not adding more for now &,

2) It’s actually a good opportunity to slowly load up on good quality REITs.

Pretty similar views to you on this really.

At this point in the cycle, interest rate risk looks tilted to the downside over the next 12 – 18 months.

Sure, it might go higher short term, but the higher it goes short term, the more it needs to go down when the time comes (in my view at least).

It would be good if you can study his past transactions of DBS shares. I was told by someone that Piyush ‘trades’ DBS shares, buying them at multi-year lows and sells at high valuation.

Yes, that is what I have heard as well.

I only looked at his transactions the past few years for this article, but yes agree a fuller analysis may be required. Unfortunately I dont have any easy access to the data source for this (short of trawling through SGX announcements, you need a professional data subscription for the compiled data).

If you have access to the full transaction history for Piyush, would greatly appreciate the share.

My personal views on the 3 main issues you raised are as follows:

1. CEO paring down his holdings. I think the number of shares he sold is small and there could be many reasons for him doing sold with none of which concerning DBS

2. The book value of (especially) DBS since the FED started its rate hike regime have been negatively effected by the hikes. This is because DBS have huge investments in non SGD denominated debt instruments issued by foreign entities. As a result it incurred substantial losses thru FVOCI, as the yields on fixed rates instruments move in opposite direction to their prices. So much so that in a couple of recent quarters, despite its record profits, after payments of dividends, DBS book value declined! When interest rates fall, the reverse will likely be the case. I made a couple of posts on FB that highlighted this also that these losses are unrealised losses and if the bank holds the instruments till maturity they will be redeemed at par values, probably without loss!

3. The 3rd point is that in the US the FED dictates the interest rate that will prevail. All banks will adjust their rates accordingly. But in SG the MAS does not dictate interest rates but of course the banks will bend to the market. Yet the 3’SG banks will adjust their rates according at each bank’s discretion, to each its own! And they do not have to adjust the loan and deposit rates at the same time or by the same extent. So it is possible that NIM may not be negatively impacted immediately.

I believe that for FY24, DBS will beat my own expectation for Net Profit to exceed $10 billion. Based on the 1HFY23 result it looks like exceeding even $11billion, or over $4.10ps. DBS itself extrapolates it at over $4.20ps. If dividend is at 50% we may see total distribution for FY23 of $2.10ps.

So for me I will hold till next year!

Great comment, appreciate the insights. You may well be right on this, it comes down to probabilities and risk-reward.

For what it’s worth, my thoughts on the 3 points you raised:

1. Yes, absolutely agree with this. He could well be selling to fund a new swimming pool for all we know.

2. Very interesting point. I did not consider this. Do you have any compiled research on this, on what is the impact to their book value – for eg. if you adjust this away as hold to maturity, what is the adjusted book value?

3. The Feds only control the Fed Funds Rate, which is the short term rates. Exactly what rates the banks choose to lend at is entirely up to them, as is the long end of the curve.

MAS does not control interest rates but controls FX, which accordingly to the impossible trinity means that we adopt global interest rates – of which the biggest player is the US. Hence US monetary policy has an outsized impact on SG monetary policy.

There are no details of the debt instruments and investments in their reports. At best, only group totals are discernible from the Other Comphrensive Income and details of Shareholders Equity.

I sent you an email but notice it is addressed to ‘donotreply’

Understand, thanks for the share.

You can email me at [email protected]