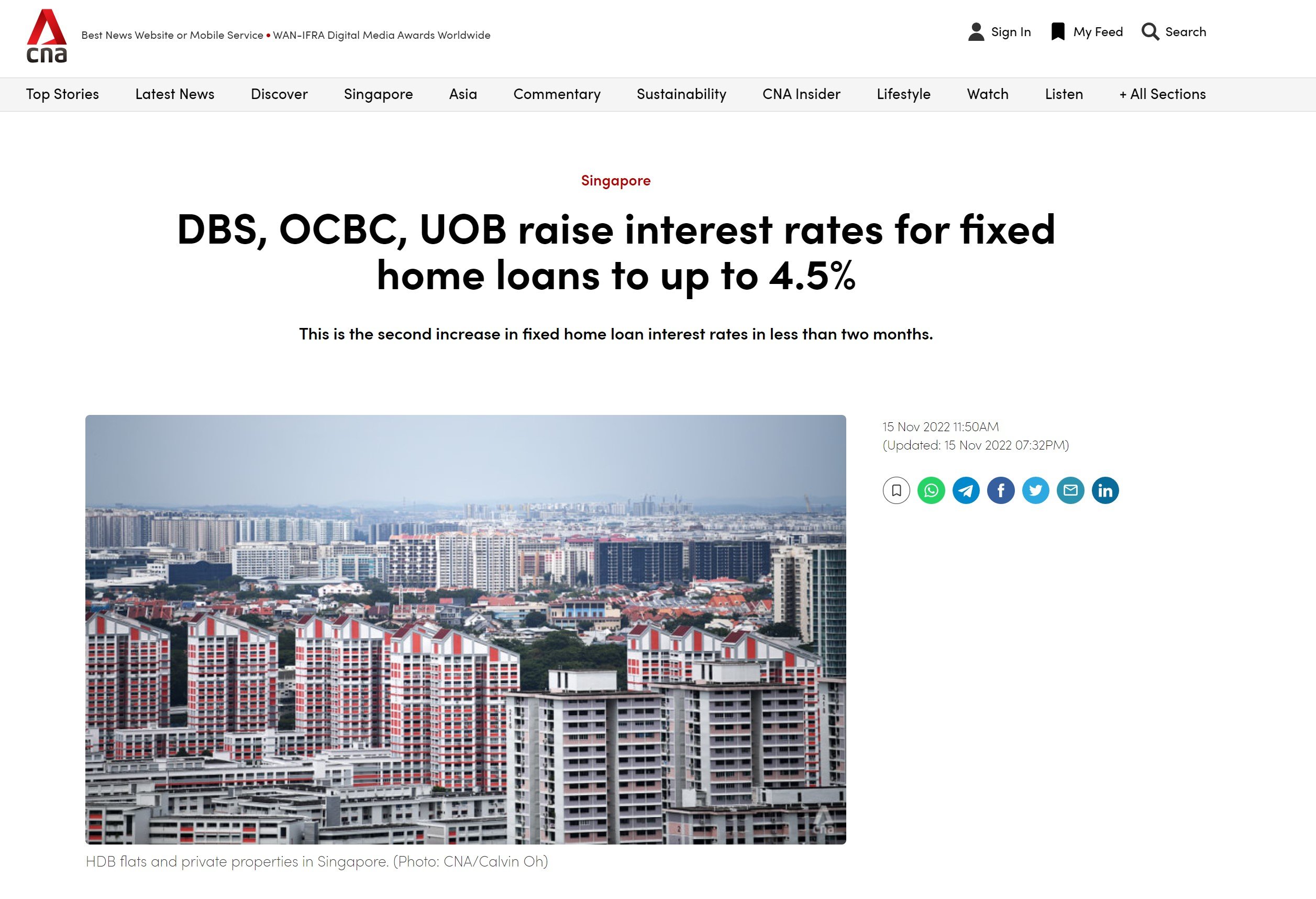

So I was reading this CNA article on DBS, OCBC and UOB Mortgage rates.

The title?

DBS, OCBC, UOB raise interest rates for fixed home loans to up to 4.5%

Massive rise in mortgage rates

To put things in perspective, this time last year you could easily get a 2 year fixed rate loan at 1.25%.

As of today, you’re looking at:

UOB Bank – 4.5% a year for 2 year fixed interest rate mortgage

DBS Bank – 4.25% a year for 2 – 5 year fixed interest rate mortgage

OCBC – 4.3% a year for 1 – 2 year fixed interest rate mortgage

So… mortgage interest rates have gone from 1.25% to 4.25%, in the span of 12 months.

That’s ridiculous.

It’s one thing to get 4% on a T-Bill risk free.

It’s another thing to be paying 4.5% on your million dollar mortgage when it comes to refinancing time…

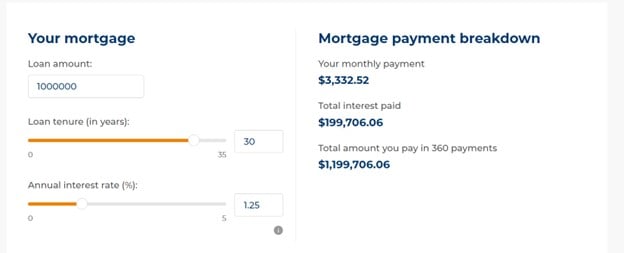

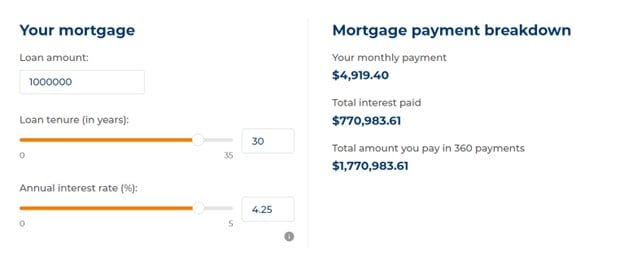

How much will monthly mortgage repayments go up?

Let’s put this into real world numbers.

Assume a borrower taking a $1 million 30 year loan to buy a $1.33 million property.

Last year he would be paying $3,332.5 a month in mortgage repayments.

Based on latest interest rates?

He would be paying $4919.4 a month.

That’s a 47.6% increase in monthly mortgage repayments, which is absolutely bonkers.

Will this crash the Singapore Residential property market?

As a real estate investor, there’s nothing that strikes fear into your heart like “rising interest rates”.

There’s a lot of chatter about how rapidly rising interest rates will crush the Singapore residential property market, just like it is starting to do with REITs and commercial real estate.

You see investors selling their homes to rent for the next 12 – 24 months, in the hopes of buying back cheaper down the road.

But… the world is seldom so simple…

But if there’s anything I’ve learned in my time investing, it is that the world is seldom so simple.

The narrative that rising interest rates will crash the Singapore residential property market is simple and sexy.

But the world rarely lends itself to such simplistic takes

3 points that I wanted to make:

- ABSD and TDSR means households are not overleveraged

- Rental Incomes are going up… a lot

- Government policy is a question mark

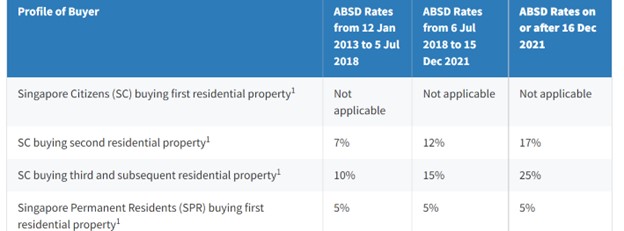

ABSD and TDSR means households are not overleveraged

Additional Buyers Stamp Duty (ABSD) has been in place in some form since 2013.

At latest rates, you’re looking at 17% for a second home.

So realistically, unless you’re a high roller who doesn’t mind paying ABSD, most Singapore households would not have more than 2 private properties (1 in each spouse’s name).

Sure, those who bought before 2013 may hold multiple properties, but if you bought before 2013 you’re so far up on the home value that interesting rates don’t even bother you anymore.

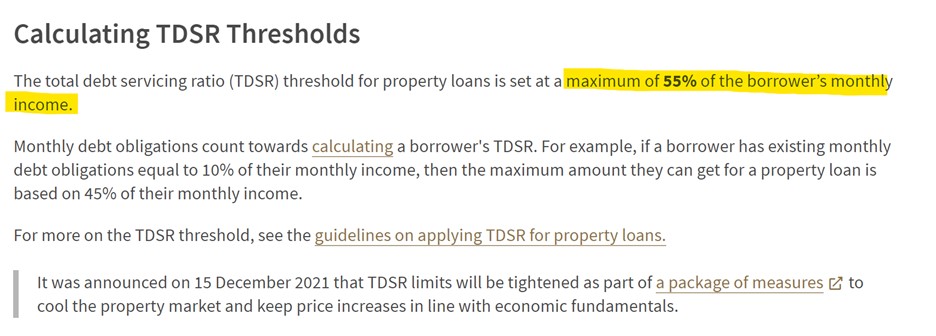

Now total debt servicing ratio (TDSR) ratios were changed recently in December 2021.

But even under the previous rules you are looking at mortgage repayments not crossing 60% of monthly income.

And don’t forget TDSR was calculated using 3.5% interest rates before this.

3.5% to 4.25% works out to about 10% increase in repayments.

Or in simple English – the guy that previously took up a mortgage that maxed out his TDSR? Will now have the monthly repayment go up to a max of 66% of his monthly income (assuming 4.25% mortgage).

That’s bad, but probably not bad to the point where we start seeing massive firesales just yet.

Problems with this analysis

Now you’re probably going to point out some problems with my analysis above.

Namely:

- Interest rate increases are not over

- What if you lose your job?

Let’s discuss each.

Interest rate increases are not over

I get it – mortgage rates have not peaked.

This is a fair point.

Market is pricing in a peak Fed Funds Rate of about 5%.

With fixed rate mortgages at 4.25% now, we could probably go higher, but we are getting very close to cycle peak.

Even if we assume a 5% peak, that would mean the same guy above will have mortgage repayments go to 72% of monthly income.

It’s tight, but probably not fire sales just yet.

What if you lose your job?

What would probably tip him over, is a loss of job.

A mortgage repayment of 72% of monthly income may be manageable… until he gets fired and the monthly income drops to zero.

For now at least, the labour market is very strong.

But you can see early signs that this is starting to turn.

Tech companies like Facebook, Sea, Amazon are laying off staff.

If interest rates stay at the 5% range, economic growth will slow further.

You can’t rule out job losses in 2023.

To respond to this, 2 points I wanted to make:

- Rental Incomes are going up… a lot

- Household balance sheets are strong

Rental Incomes are going up… a lot

Landlords (or tenants) will know what I’m talking about.

Rental rates are going up… a lot.

A simple example – the $1.3 million condo at the start of this article.

You could probably rent it out at $3,000 pre-COVID.

With a $3332 monthly mortgage, you’re out of pocket $332 a month.

Today?

You can probably lease it out at anywhere from $4,000 to $4,500.

Which means that while the mortgage payments went up a lot, the shortfall may not have increased that much because of higher rentals.

But not everyone leases out their home you say.

Some people live in them.

Let’s put it this way. If you lose your job, and you cannot pay the mortgage. And the market price of your home is well above its peak.

Are you going to firesale your home below market price?

Or will you rent out your home and find alternative accommodation, and wait for property prices to recover?

So higher rental rates offer a potential alternative, for those strapped for cash.

Household balance sheets are very strong

The funny thing is that despite all the pain caused by COVID, household net worth actually increased quite a bit after COVID.

Why exactly that is so is not very clear.

But ask around and you’ll probably find a number of people are better off financially today, than they were pre-COVID.

Which means that even with higher mortgage repayments, and even assuming job losses, it may take some time for households to eat through the cash buffers built up during COVID.

When you lose your job, and you need cash, you will sell your stocks and REITs, before you sell your house.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Government policy is a question mark

The final point I wanted to make, is government policy.

It’s fairly clear that government does not want undue speculation in property prices.

Once property prices start running away, you see cooling measures coming in to keep housing affordable.

If I were to venture a guess, this might work on the downside as well.

Given how much of the household balance sheet is tied to Singapore residential property, a plunge in real estate prices would be deeply unpopular, and may even have systemic risk for the economy.

If we see a plunge in property prices, you probably cannot rule out loosening of cooling measures to support the market.

I am not saying that Singapore property prices will go up…

Now don’t get me wrong, I am not saying that Singapore residential property prices will go up in the face of higher interest rates.

I am saying that the world is not as simple as that…

All I’m saying, is that the world does not lend itself to such simplistic analysis.

Rising Interest Rates -> Falling House Prices is a simplistic analysis that only takes into account the immediate impacts of interest rates.

I encourage you think about the second and third order effects.

Why are interest rates going up so drastically?

What will happen if the consequences of higher interest rates start to play out?

My personal view on Singapore’s Residential Property Market?

The way I see it, Singapore’s residential property market is tightly controlled by government policy, both on the demand side (ABSD, TDSR etc) and supply side (land sales).

As investors – how do you invest in a market that is tightly controlled by one party?

Take oil for example – where OPEC+ has outsized control on oil prices.

How do you invest in a market like that?

Answer – unless you have inside info or a special edge, you don’t bet on short term price movements.

I’ve been burnt by OPEC too many times in the past, that I have this lesson seared in my psyche.

In markets like that, stay away from short term positions, and take long term positions.

Short Term (1 – 2 years)

And really, that’s my view on Singapore real estate.

Where prices go in the short term, I frankly have no clue.

I have listed out some of the potential factors to consider above, including the possibility of government intervention.

Trying to predict how all this will play out, is a fool’s errand.

So for all the investors selling their home and renting, in the hopes of buying back cheaper 12 – 24 months later.

That’s a short real estate position, and who knows it might pay off.

But I’m not a fan of such trades as shared above.

Longer Term (10 – 20 years)

Longer term, the goal (as I see it) is to have houses for living in, not for speculation.

So expecting a 7% real return compounded on Singapore residential property over the next 20 years is probably a tad optimistic.

This isn’t 1960, and Singapore is not going from third world nation to first world.

But will Singapore residential property deliver negative real returns over the next 20 years? That could be tricky too, given how much of the household balance sheet is Singapore real estate.

If that happens, it’s probably bad news for all Singapore assets in general.

So base case – probably low single digit real returns in the long term, broadly tracking economic growth.

But that’s the long term.

As for the short term, I frankly have no strong views.

This analysis above is only for Singapore Residential Property

Been getting some questions, and I just want to clarify that this analysis above only applies to Singapore Residential real estate.

Commercial or Industrial real estate have a very different analysis, because things like ABSD and TDSR don’t apply – creating fundamentally different industry dynamics.

And technically even within Singapore residential property, you need to be differentiate between HDB, Condos and landed in the analysis.

If you find this article helpful for you, please do consider signing up for the Patreon subscription. Most of the regular macro updates and changes to my portfolio positioning have moved there.

At S$15 a month you get the premium weekly market updates.

At $25 a month you get my full stock and REIT watchlist, and at $40 a month you get updates on changes to my portfolio positioning.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

To labor the point on how much we don’t know about second and third order effects:

-who knew home prices would shoot through the roof during Covid? Conventional wisdom was that unemployment would rise and people would be forced to fire sale their homes.

-our parents who bought in the 60s and 70s took a leap of faith that Singapore would grow from third world to first. It wasn’t obvious back then!

-with the issues in Hong Kong and China we are seeing an influx of wealth and talent into Singapore. Govt is wary of giving official numbers but I’ve heard enough anecdotes. What does this do to property prices at the top end and how does this spill over to houses for the masses (Resale HDB, Condo)?

Exactly right! It is tempting to break investing down into simple cause effect analysis, but the reality is that the world is incredibly complex with a lot of moving parts, and it is not so straightforward to predict the outcomes of a certain action. Without fully considering the second and third order effects, it is very tough to call what will happen.

Like you said, who would have expected that home prices would shoot through the roof during COVID!

A healthy dose of humility is required in investing.

For lots of people sake, let’s hope there’s no property market crash. It’s not the kind of scenario that’s nice to even observe

Agreed! Although on the flip side, I can think of many buyers / renters who wouldn’t mind one!