I usually try to wait until the final prospectus for an IPO is out before I write on it.

But then I saw rave reviews from the other financial bloggers, and very excited comments from readers who reached out.

So I decided to make an exception this time around.

And boy, was I blown away.

5 minutes of reading the preliminary prospectus for Digital Core REIT and it was already clear this was going to be “THE REIT IPO of the year”.

Spoilers alert – Digital Core REIT comes with:

- Rock solid sponsor

- Hot asset class (data centres)

- Good valuations (both yield and Price/Book)

- Triple net lease with built in rental escalations

- Blue chip tenants with 100% occupancy

- Low gearing (27%)

And a list of cornerstone investors that reads like the who’s who in fund management.

There are a couple of unique points about Digital Core REIT worth discussing though, namely the potential conflict with the Sponsor.

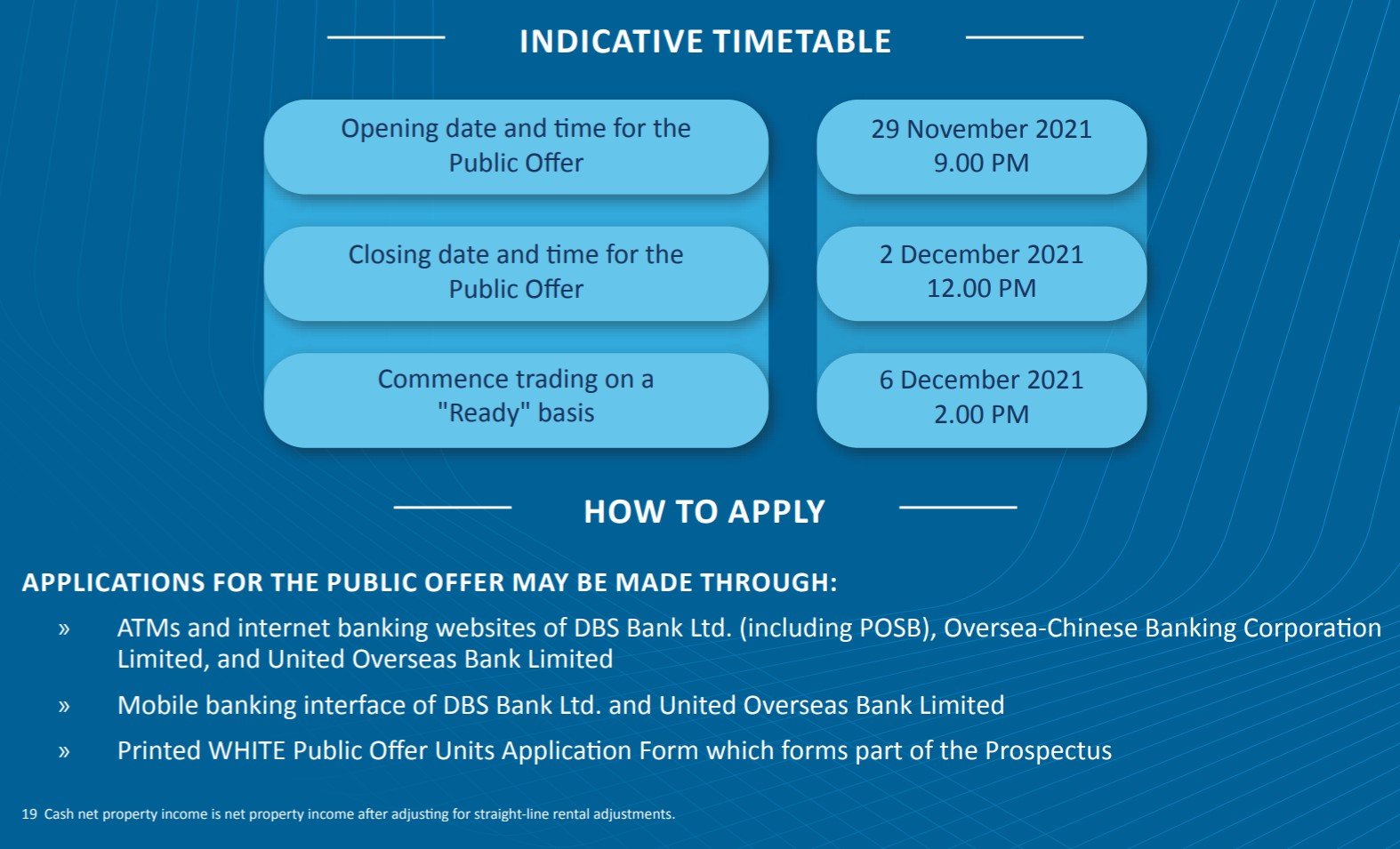

Update: Public Offer for Digital Core REIT IPO closes on 2 Dec 12pm

Just to update that the final prospectus for Digital Core REIT IPO is out.

The Public Offer opens at 9pm, 29 Nov, and closes at 12pm on Thursday, 2 December.

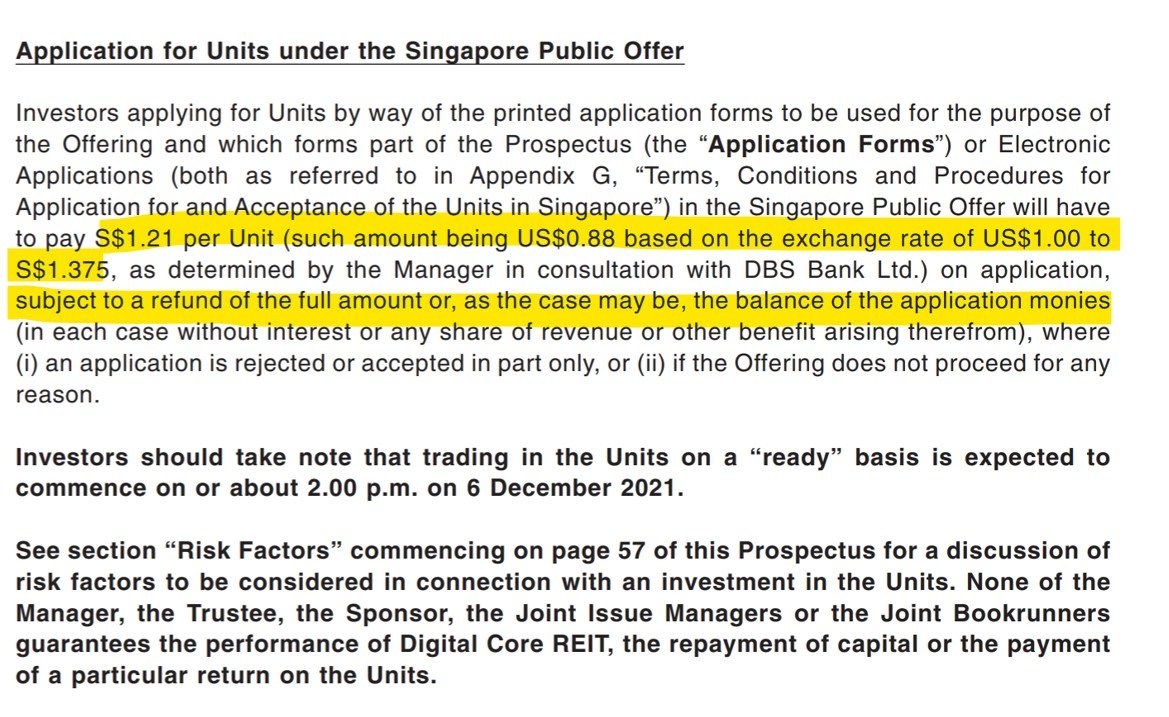

The FX roundtripping issue also has been addressed by DBS, because the Public Offer will be in SGD and not USD.

Public offer will be at S$1.21 per unit. This uses an exchange rate of US$1.00 to S$1.375 which is not an amazing FX spread, but at least it solves the problem where you pay FX fees twice if you don’t get an allocation.

This way if you don’t get an allocation, you just get refunded in SGD. 🙂

Basics: What is Digital Core REIT?

From the prospectus (emphasis mine):

Digital Core REIT is a Singapore REIT (“S-REIT”) established with the principal investment strategy of investing, directly or indirectly, in a diversified portfolio of stabilised income-producing real estate assets located globally which are used primarily for data centre purposes, as well as assets necessary to support the digital economy.

Digital Core REIT seeks to create long-term, sustainable value for all stakeholders through ownership and operation of a stabilised and diversified portfolio of mission-critical data centre facilities concentrated in select global markets. Digital Core REIT will be the exclusive S-REIT vehicle sponsored by Digital Realty, the largest global provider of cloud- and carrier-neutral data centre, colocation and interconnection solutions.

Basically, a data centre REIT, sponsored by Digital Realty, a US listed REIT.

You read that right.

A REIT, sponsored by a REIT. This has some interesting implications on conflicts of interest that we’ll discuss later.

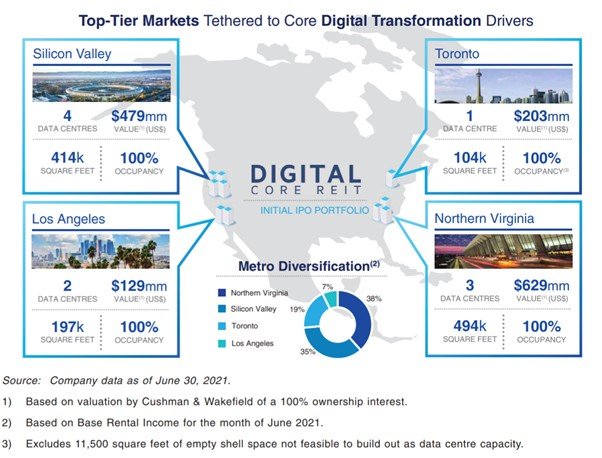

This is the initial portfolio, 10 freehold data centres:

Units will be offered at $0.88 per unit, working out to a market cap of US$1 billion on listing.

Sponsor: Digital Realty – a Mega US Data centre REIT

The Sponsor of Digital Core REIT is Digital Realty Trust, a US listed REIT.

Digital Realty Trust is one of the largest data centre providers in the world:

As at 30 June 2021, the Sponsor is the largest global owner and operator of data centres with a total of 291 data centres with NRSF of approximately 35.8 million square feet, excluding approximately 7.6 million square feet of space under active development and 2.0 million square feet of space held for future development, in 47 metros across the Americas, EMEA and Asia Pacific, of which a sizeable portion will become suitable for potential injection into Digital Core REIT over time.

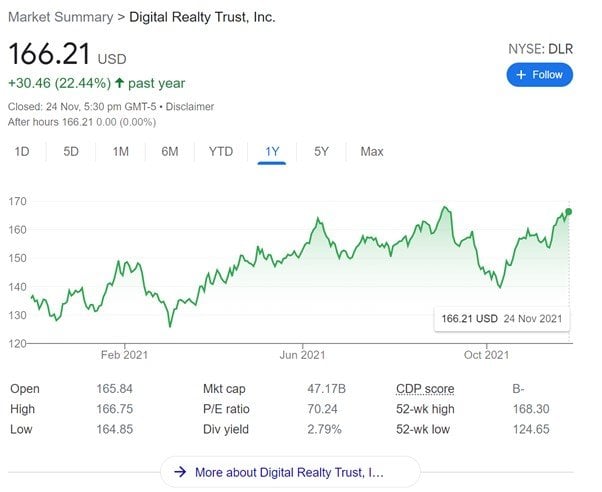

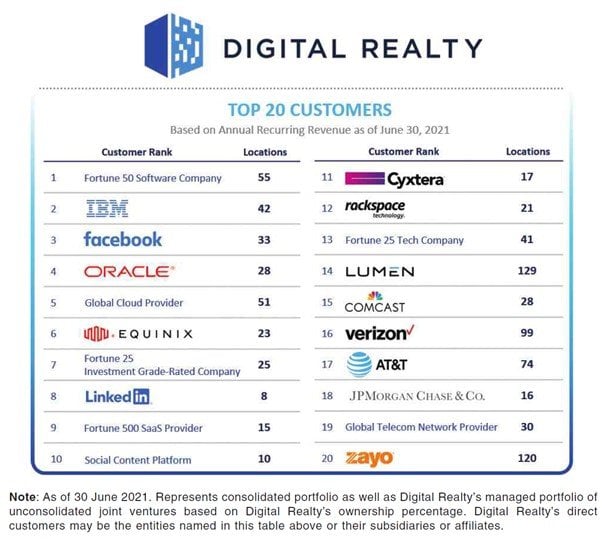

Digital Realty is a really big boy – US$47 billion market cap, 2.79% yield.

With a list of Top 20 Customers that is as solid as it gets in the data centre space.

Conflict of Interest? – REIT sponsoring a REIT?

The problem then – a mega US data centre REIT, sponsoring a much smaller Singapore listed REIT.

If not properly managed, there could be a potential for conflicts of interest.

Thankfully, there are quite a few safeguards built into place:

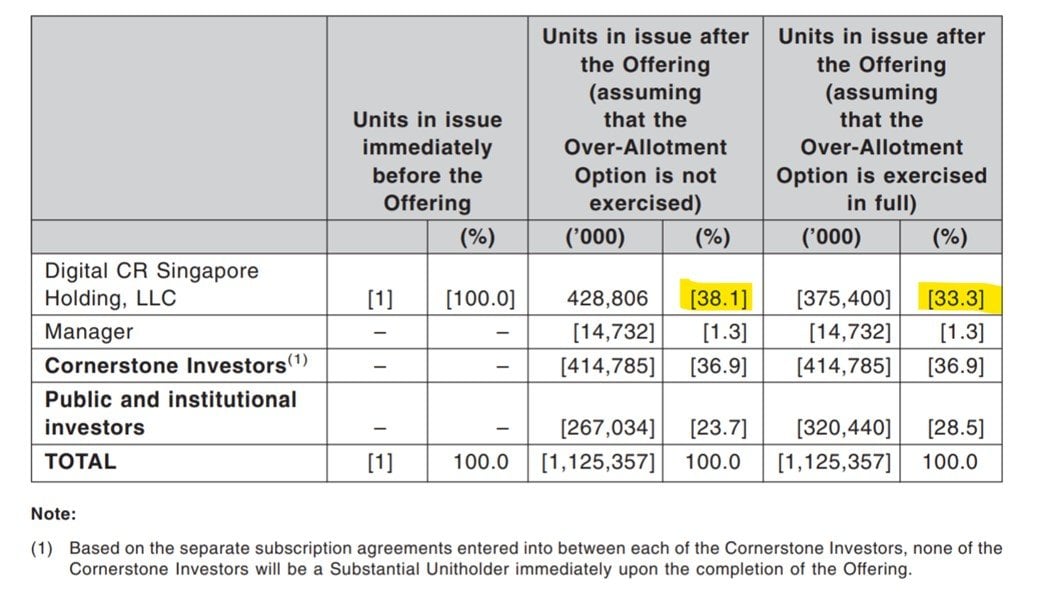

- Sponsor will hold 39% interest in Digital Core REIT (assuming over-allotment not exercised)

- Right of First Refusal (ROFR) from Sponsor to Digital Core REIT

- Reverse ROFR over any assets Digital Core REIT sells

- Co-Investment by Sponsor

This is probably the most important part of Digital Core REIT IPO, so it’s worth spending some time to discuss this.

Sponsor will hold 39% interest in Digital Core REIT Post IPO

Digital Realty Trust will hold a 39% interest in Digital Core REIT post IPO, assuming the overallotment is not exercised.

If exercised, then Digital Realty’s stake will drop to 33.3%.

What I did not like about Daiwa House Logistics Trust was that the sponsor held a small 10% stake post listing.

I much prefer 30%+ ownership stakes, exactly what we get here.

30%+ is in line with the CapitaLand/Mapletree/Frasers REITs, in terms of Sponsor stake.

ROFR from Digital Realty to Digital Core REIT

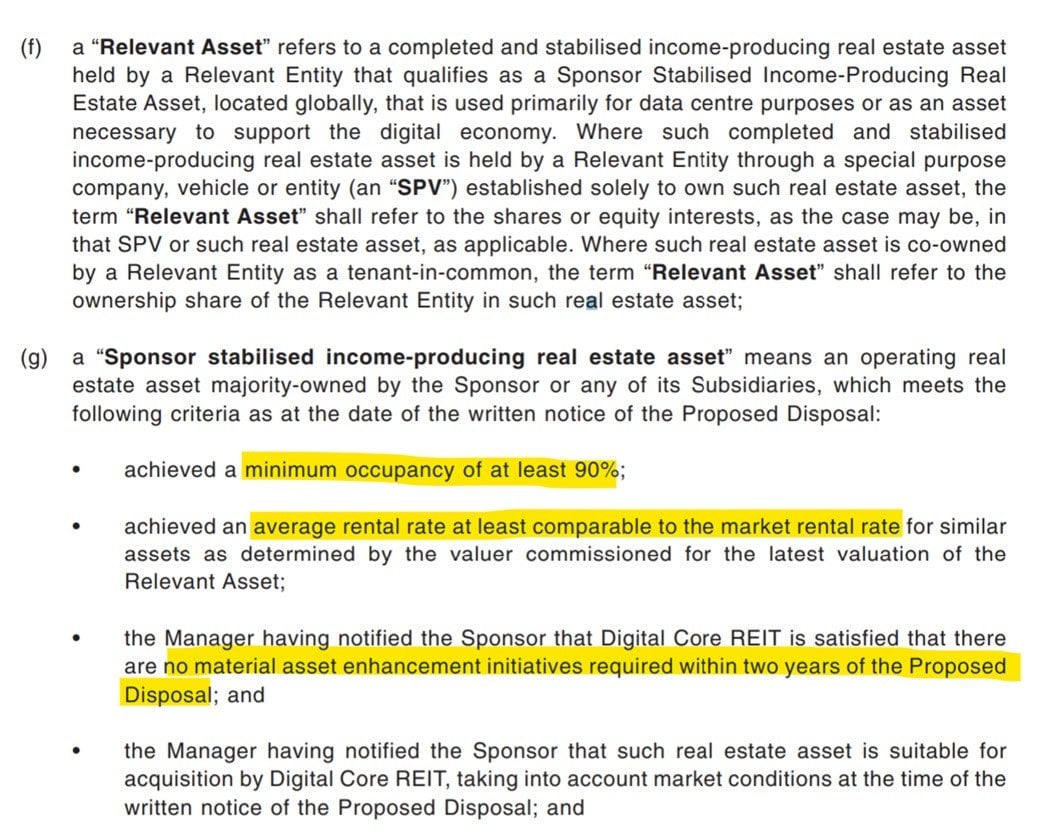

Digital Realty (Sponsor) will grant a right of first refusal (ROFR) to Digital Core REIT over any stabilised income producing data centre.

This means that before Digital Realty sells such a data centre, they first need to offer it to Digital Core REIT.

What is a “stabilised income producing data centre” you ask?

It is a data centre with:

- At least 90% occupancy

- Average rental comparable to market rental

- No material AEIs required within 2 years

This is very interesting and gives us hints as to the purpose of Digital Core REIT – which could be a vehicle for Digital Realty to offload mature, stabilised data centres, into an Asian listed vehicle that can more easily tap Asian capital.

There, I said it.

Agree or disagree – let me know in the comments below.

Reverse ROFR if Digital Core REIT sells any data centre

At the same time, there is a reverse ROFR if Digital Core REIT sells any asset, so the sponsor Digital Realty has the right to buy it back.

For now it’s not going to mean much since Digital Core REIT is so small, but it’s a nice touch.

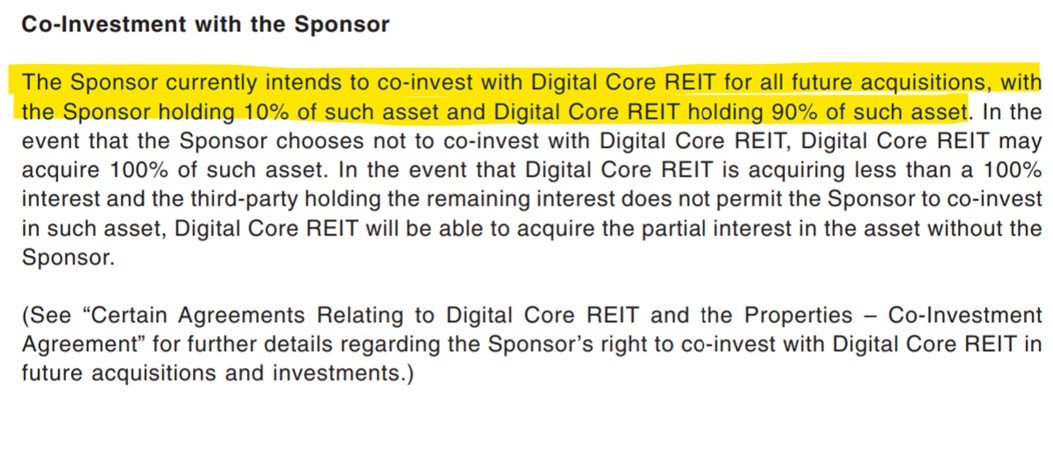

Co-investment agreement with Sponsor

There is also a co-investment agreement, where the Sponsor has the right to take a 10% stake in anything Digital Core REIT is buying.

Quite a nice touch to address the conflict of interest between the 2 REITs.

Why is Digital Realty listing a REIT in Singapore?

I know a lot of investors always ask “If it’s so good, why do they need to come all the way to Singapore to list?”.

If I were to venture a guess – it would be to tap Asian capital, and provide a vehicle to recycle the mature data centre assets.

Singapore is the largest REIT market in Asia ex Japan, so Singapore is the natural option.

Us Singaporeans need to have a bit more faith in ourselves, sometimes people come here because we are good.

I like this trend though, it’s a very positive trend for Singapore.

We saw Daiwa House do the same last week with Daiwa House Logistics Trust, and I hope we see more of such REITs going forward.

Makes me a very happy horse.

Are the conflicts properly managed for Digital Core REIT?

As to whether the conflicts are properly managed – it’s not an easy question to answer.

You can have all the protections in place, but if people choose not to follow it in practice there’s not much you can do. With conflicts of interest, getting people to abide by the spirit of the law is more important than the letter of the law. There are many ways around a ROFR if you are crafty enough.

What I would say though, is that I like the gesture from the Sponsor Digital Realty by giving the ROFR, Co-Investment Agreement, and reverse ROFR. And I really like the 30%+ ownership, which is in line with the CapitaLand/Mapletree REITs.

I’m willing to give them the benefit of the doubt here, but as to how it actually plays out in reality, we do need to see the track record over time.

It’s not immediately obvious to me what kind of data centres would be held by the Sponsor Digital Realty, and what would be injected into Digital Core REIT. Will Sponsor keep the best data centres for themselves?

This is probably the biggest question mark about Digital Core REIT.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

IPO Portfolio of Digital Core REIT

The portfolio of Digital Core REIT is pretty decent stuff:

The Digital Core REIT IPO Portfolio is comprised of 10 institutional quality, 100% freehold data centres concentrated within top-tier markets in the U.S. and Canada with an aggregate Appraised Valuation of US$1.4 billion.

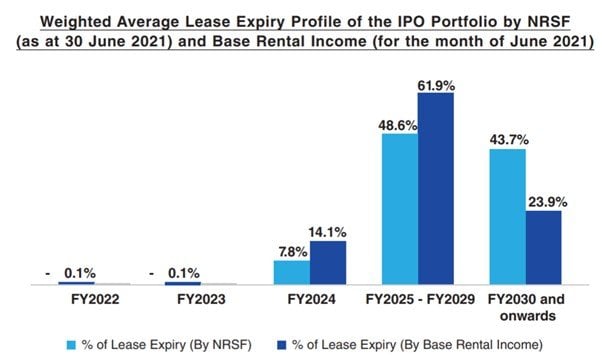

The IPO Portfolio totals 1.2 million NRSF as at 30 June 2021 and is 100% leased to a roster of blue-chip customers, each with numerous deployments across the Sponsor’s global platform.

The weighted-average remaining lease term is over six years and 100% of the lease agreements contain contractual annual cash rental rate escalations ranging from 1.0% to 3.0%, with a weighted average of approximately 2% by Base Rental Income for the month of June 2021.

In addition, approximately 85% of the IPO Portfolio based on NRSF as at 30 June 2021 is leased on a triple-net lease structure, providing additional insulation against operating expense growth.

Why Virginia

The bulk of the data centres are located in Northern Virginia.

Shoutout to Investment Moats who brought this article to my attention, explaining why Virgina is so popular as a data centre hub.

Basically:

- Location – Virgina is right in the middle of the Eastern seaboard, and just 30 minutes from Washington DC. This gives it short latency to the major population hubs.

- Reliable Energy – Energy supply is consistent and well managed by the local operator (Dominion Power).

- Tax Incentives – Favourable tax incentives for data centres.

- Infrastructure – Few natural disasters, easy availability of land. Fibre connections are abundant, as is a skilled data centre workforce.

Digital Core REIT’s IPO Portfolio

Back to the IPO portfolio, you get:

- Blue chip Tenants

- 6.2 years WALE (Weighted Average Lease Expiry – average lease tenure for the portfolio)

- Built in rental escalations of 1-3% per year

- Triple Net Lease

- 100% Occupancy

- 100% Freehold properties

With a triple net lease (NNN), the tenant agrees to pay the property expenses such as real estate taxes, building insurance, and maintenance in addition to rent and utilities.

This provides low risk, steady income – basically a good thing.

Some of the Properties are quite old

The one potential problem is that some of the properties are quite old, dating back to the 1970s.

But frankly these are data centres and not retail malls or offices.

So the age of the building doesn’t matter so much as the servers in them.

As long as the lights (power supply) and aircon (cooling) stays on, the age of the building doesn’t matter that much.

Valuation of Digital Core REIT

Average cap rate for the portfolio is 4.25% which is fair for US based data centre assets.

Book value for Digital Core REIT is US$0.85, so at IPO price of $0.88 you’re buying in at 1.04x book value.

Considering how most of the other data centre REITs like Mapletree Industrial Trust and Keppel DC REIT trade at a premium to book, this looks really good.

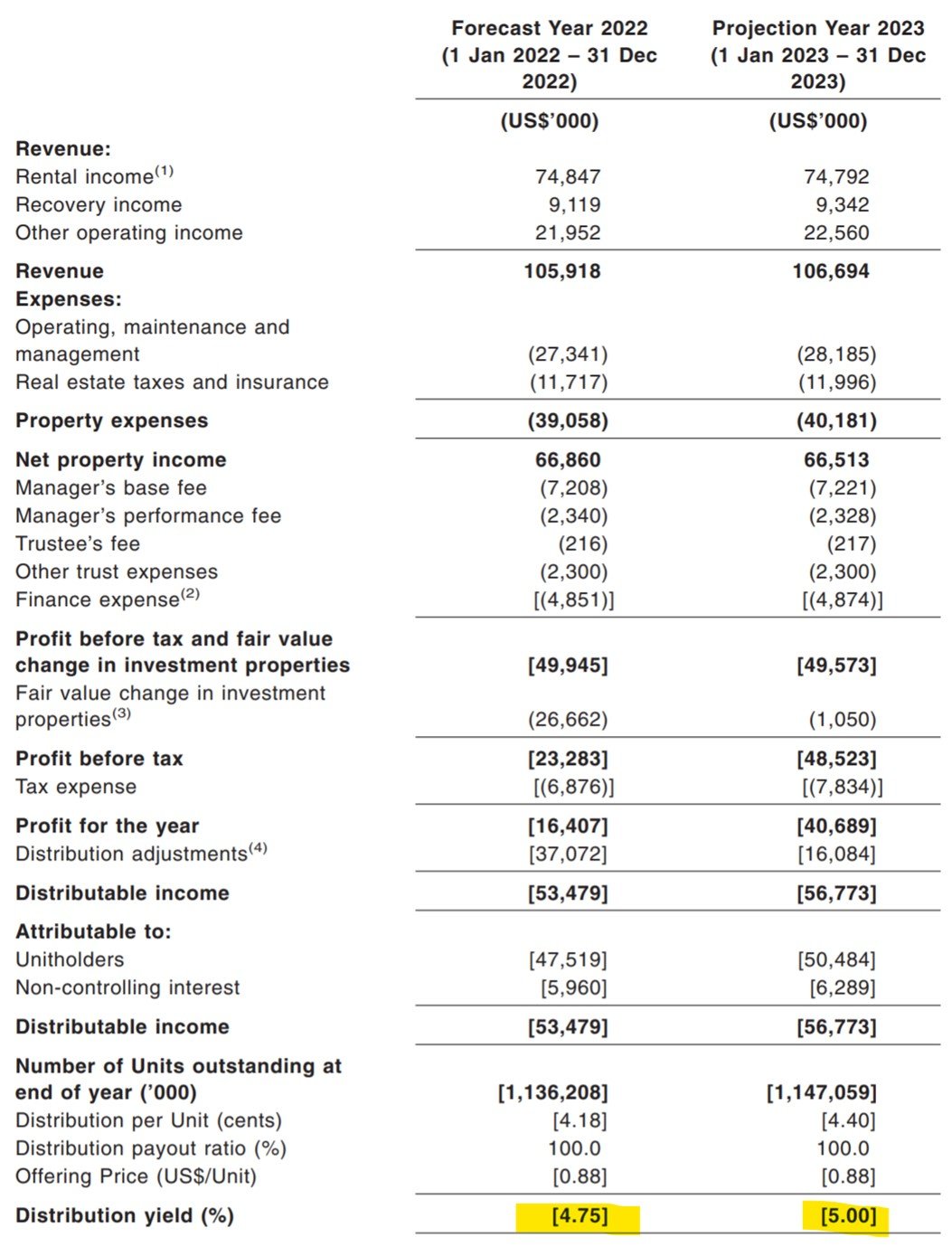

Yield of Digital Core REIT

Forecast yield for Digital Core REIT is 4.75% for FY2022, and 5.0% for FY2023.

By contrast, here are the yields for some other Singapore listed data centres:

- Keppel DC REIT (100% data centres): 4.0%

- Mapletree Industrial Trust (53% data centres): 4.9%

- Ascendas REIT (10% data centres): 4.99%

- Digital Realty Trust (the Sponsor): 2.79% yield

So both book value and yield of Digital Core REIT looks very solid compared to market prices.

Gearing / Leverage of Digital Core REIT

The icing on the cake is that Digital Core REIT achieves this 4.75% yield with just 27% gearing.

Most of the other REITs are pulling 30%+ gearing, so this is a really, really nice touch.

With such low gearing, you can actually add on some leverage of your own and juice returns up to 7-8% for quite low risk.

Cornerstones for Digital Core REIT IPO

On to the Cornerstones.

I mean this just looks like Xmas came early.

You have:

- AEW

- AIA Investment

- Blackrock

- DBS Bank (not on behalf of the wealth management clients)

- Eastspring

- Fullerton

- Jane Street

- Lion Global

- Nikko AM

- Segantii

Full list of cornerstones below:

If you’re slightly newer to the investment space, all you need to know is that the guys listed above are really big boys.

And they are all crowding into Digital Core REIT’s IPO, which is a very strong show of confidence.

Public Offer is miniscule – US$10.68 million

If there is one problem with Digital Core REIT’s IPO, it is the miniscule public offer.

13,352,000 units are being offered, which is a tiny US$10.68 million.

Given the insane demand I would expect for Digital Core REIT IPO, the chances of getting any are very slim.

When is Public Offer open?

Public offer is not open yet, we need to wait for the final prospectus to be out.

Will release an update article once it’s out.

Potential roundtripping of FX Fees?

One point to note is that the IPO units for Digital Core REIT are in USD.

If you apply for the IPO, the bank you use (eg. DBS) needs to deduct USD from your account, incurring Forex Fees.

Which means if you don’t get an allocation, DBS may refund you in SGD, causing you to incur Forex Fees twice.

If anyone has experience with this do let me know in the comments below – is there any way around this? Or do we just need to eat the FX fees if we want to punt this IPO?

What is my take on Digital Core REIT?

Frankly it doesn’t matter what I write about Digital Core REIT, because this IPO is going to be red hot regardless.

The cornerstones are already locked in, and the placement is probably going to be red hot too.

For what it’s worth though, I like:

- Rock solid sponsor

- Hot asset class (data centres)

- Good valuations (both yield and Price/Book)

- Triple net lease with built in rental escalations

- Blue chip tenants with 100% occupancy

- Low gearing (27%)

The only potential problem is how to manage the conflicts of interest with the Sponsor Digital Realty, but I think they’ve done a decent enough job, at least at IPO stage.

Will I be subscribing for Digital Core REIT?

The chances of getting any on the public offer are very small, given how tiny the public offer is.

Having to incur FX fees twice just to subscribe is a bit of a bummer too, so if anyone has experience on this do let me know.

If I can solve the FX issue I would hands down subscribe, if I can’t I might just save myself the FX fees and wait for Digital Core REIT to trade on the open market post IPO.

I applied for Daiwa House Logistics Trust and got a grand total of zero units, so given that it was a 50% chance, maybe I just don’t have luck with such things.

Why is Digital Core REIT better than Keppel DC / Mapletree Industrial Trust?

Update: Some of you have asked me why I like Digital Core REIT over Keppel DC REIT or Mapletree Industrial Trust.

And I think the main reason why is (1) pricing and (2) sponsor.

The problem is that neither Keppel nor Mapletree has the kind of size that Digital Realty (the sponsor) has. So they lack the pipeline and expertise in data centres, and the big growth can only come by acquiring assets from a third party. So to pay a premium over book valuation doesn’t make a lot of sense to me for those REITs.

With Digital Core REIT there is backing from Digital Realty which is one of the largest data centre players in the world, that’s real expertise and pipeline there.

And valuations are arguably even better than Keppel DC / MIT, and it looks like the sponsor left some money on the table here to build goodwill with investors.

Main worry like I said, is whether the Sponsor will treat the REIT well going forward, or will they keep the best assets for themselves and spin off the subpar assets at a high valuation into Digital Core REIT.

We can only speculate at this stage, but from a long term perspective Digital Realty will make a lot more money by treating Digital Core REIT well. Investors are once bitten twice shy – all you need is to mistreat the REIT once and investors will sell out.

So I’m willing to give them the benefit of doubt, and it seems like most of the big cornerstones taking similar views.

But only way we’ll know for sure is to see how this does post-IPO.

Do expect lots of fundraisings and acquisitions going forward though, the whole point of Digital Core REIT is the growth and pipeline. If you don’t want a REIT with aggressive capital calls and fundraises then probably best to stay away.

Closing Thoughts: THE REIT IPO of the year – Digital Core REIT IPO

At current IPO price, I do think they are leaving money on the table, and I do expect price to pop on day one.

There are longer term problems such as the potential conflicts of interest, growth path post IPO etc, but for these we just need to let it play out and watch the track record post listing.

Markets are panicking over the new Omicron (B.1.1.529) Variant, causing a big risk-off yesterday.

But data centres are practically immune from COVID, and any delay in rate hikes will bode well for REITs.

So yeah… 5 Horse Rating from me, at least for the short term trading.

Mid to longer term though, you’ll want to consider the risks I raised above.

Love to hear what you think!

Digital Core REIT – FH Rating

As always, this article is written on 27 Nov 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with and fund $2000.

Get 1 free Apple share (worth $200) you’re new to and fund $2700.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Thanks FH. Can we apply directly from a USD account to save on FX. And can the refund come directly into USD account. Basically fund the FX account using Interactive Brokers low cost conversion.

I recall when subscribing via the ESA function of DBS there isn’t such an option available. Let me know if you manage to do it.

Appreciate if this option is available.. Called DBS seems like they are not familiar on this

What do you mean? The public offer is priced in SGD so there’s no FX issue.

I thought it was denominated in USD. And the purchase price is in USD right?

Yes this is a USD counter. 🙂

Hi there FH. Great right up.

Will this reit be denominated in and traded in USD?

If the sponsor is also a REIT, where does the sponsor get its properties from?

Thanks much!

Yes, denominated in USD.

REITs are allowed to develop properties too, under Singapore CIS code up to 10% of the REIT’s asset base can be used for development. Can’t recall the exact numbers for US regulations, but the concept is similar.

if Sponsor’s Reit yield is 2.79% and their SG Reit is 4.75%, doesn’t it means that they’re making a lost when moving their assets from their US Reit to SG Reit? If the assets are not from the US Reit but from 3rd parties, can understand why their US Reit don’t acquire them ‘cos with their lower yields, they can create more value to their US Reit shareholders when the spread is higher; is this another potential conflict-of-interest issue?

Technically no because they book the asset on their books at book value, so they are not divesting at a loss. But yes – once you go down this line of reasoning it is obvious there are many possibilities for conflict. Hence it’s important to see how the sponsor will treat the REIT going forward.

But I do think there is more to be gained by treating Digital Core REIT well, Digital Realty already has a good reputation – no point muddying it just to make a quick buck.

Hi FH, thanks for your analysis.

On a separate note, can you check the programming of the ads on your page? For this and the last few articles, the ads are programmed to autoplay with sound on. At times more than 1 ad is playing as well, and I couldn’t locate the ad where the sound is playing.

Nowadays the default for ads should be “sound off”, as a lot of us are surfing in situations or places where it’s inappropriate to have the audio come on. For the previous articles I ended up just closing the article quickly as I couldn’t find the ad that was playing loudly.

Thanks for raising this to me. I have just raised this to my ad provider, will get them to check on the technical issue. The ads are supposed to be muted.

Apologies for the inconvenience.

Hi MBev,

Have identified the ad in question and reported to the ad publisher.

Thanks again for raising this.

If you encounter this again in future you can assist to get them blocked by reporting the ad. I’ve extracted the steps below:

“The best way to get these blocked is to report the ad using the ad reporter so that all the identifying information is sent to our Ad Operations team to track the advertiser and get that blocked for you.

On the Universal Player, the ad reporter is at the bottom left-hand corner right beside the volume button and looks like the Mediavine logo:

Once you click on that icon, you’ll then be able to click on the Report Ad button and send that information to the team:

At that point, we should be able to track the advertiser and block their ads from your site.”

Hi FH. Thanks for your response as always!

Interested to know your macro thoughts on data centers as a whole. I noticed KDC and MINT have corrected quite significantly since their highs reached in June. Is this more of a cyclical rotation going on? Would you view present valuations as compelling enough to jump back into the data center reit sector?

Also, in terms of competitiveness, would it be fair to say that Digital Realty is way more competitive than Keppel / Mapletree in the data center game? More scale, better geographical reach, more A-List clients? For the A-List clients with multiple offices around the world, I can see why it would make sense to stick with a particular provider (digital realty) due to familiarity and predictability. So perhaps those customer relationships are stickier and harder to displace?

Biggest downside I see is lack of inflation protection. 1-3% annual increases with 6 year WALE. US inflation has been over 5% for the past 6 months, and is expected to be high, because residential rent is increasing (see the chart in https://www.bloomberg.com/news/articles/2021-07-06/soaring-u-s-rents-are-the-sticky-inflation-with-staying-power). Owners-equivalent-rent is a large part of the CPI, so higher rents give higher inflation.

The second risk is that we don’t know the property cycles: when data centers in different US cities start to become oversupplied.

But overall, good combination of yield and growth.

Nice writeup. Agree that at IPO valuation and yield it’s a no brainer. I think the bigger question for me is – say you don’t get allocated any at all (I’m presuming I won’t thanks to all the rave reviews and 5 horse ratings haha). Would you still buy it at say 1.3x P/B (which works out to be 3.6% yield for at least the next 2 years) if prices stabilize at that range post IPO? It becomes a much closer decision vs MIT’s 5.0% at that range. I like the better, bigger sponsor, but it’s to some extent countered by the worry that they’ll keep the best for themselves. Thoughts?

Yes fantastic question. Just personal view, but at 3.6% yield I will probably skip it. At that kind of price the risk-reward no longer looks amazing, and I would want to see some clarity on the longer term roadmap for the REIT + what kind of assets are spun off into the REIT.

I respectfully disagree with the conclusion. My biggest concern is how independent is the REIT from its parent? As of today, CEO of the REIT, Mr. John Stewart is still listed as SVP, Investor Relation. I don’t believe that senior management can “wear” 2 hats, be senior management of 2 listed companies. Yes, it’s good to have all the contractual arrangements but this is not good enough. Can the REIT make its own acquisition without consulting Digital Realty, or even get the blessing of Digital Realty? If there were new data centers where both the REIT and Digital Realty were interested in, can the REIT make its own decision?

Yes, I completely understand where you’re coming from. This would be my biggest concern for Digital Core REIT as well.

You could make the same argument for all the REITs with a listed Sponsor as well, eg. CapitaLand? How does sponsor balance their own interests versus that of the REIT is a very tricky question, that is seldom black/white in practice.

If after looking at the facts you think it will be an issue, just skip the REIT.

Great write up! I have more of a logistical question and this might be useful to address in future posts as well – how do u actually sign up for allocation pre-ipo?

You need to get access to the placement tranche. Best bet is to ask your private banker or stock broker if they can give you an allocation. But the hottest IPOs will usually be reserved for their favourite clients (ie. if you give them a lot of business).

Hi FH, thanks for the writeup.

Can you explain the intuition behind how the ROFR, reverse ROFR and co-investment agreement act as a protection against potential conflict of interest and Digital Realty offloading poor quality assets to Digital Core REIT?

Haha ok technically speaking they don’t. Like I said, if the sponsor has evil intentions, no amount of legal protections will protect you because things are not black/white in reality. So if the sponsor wants to screw over the REIT, chances are they will still be able to do it.

But looking at it holistically, with the Sponsor’s size and reputation, the legal agreements in place, the stake in the REIT, the cornerstones they lined up – these suggest to me the Sponsor is serious about Digital Core REIT as a long term vehicle.

Of course things can change down the road, but at least for now that’s my view.

Hi FH,

Are you still as bullish on this? Given this has corrected to 0.95 now, maybe a good entry point?

One thing that concerns me is rental reversions are only 1-3%, far below inflation. Thoughts?

Well the fundamental analysis remains the same, what’s changed is the macro backdrop.

Given the rise in yields, I wouldn’t be keen to pick this up at IPO price anymore, as there are much more attractive investments out there. If it goes back down to below IPO prices, then that’s a different story.

Hi FH,

Your wish is granted! Significantly below IPO price now. All the positives you mention in the post remain. What changes is rising inflation and interest rates with low rental reversions built in. Under such circumstances, what would be the target price you are looking to buy in?

Looking increasingly interesting. Thanks!

6% yield could be interesting for me, which is a 3% yield spread vs the 10 year Treasury.

That’s the same spread they IPO-ed at, as the 10 year was back at 1.5% back in Dec (vs 4.75% IPO yield).

Works out to a price in the low 70s. Don’t know if we get there, but let’s see how this plays out.

Thanks. I am with you, am waiting for all the quality Reits like MIT, Ascendas etc. to hit 6% as well. MIT almost got there then recovered strongly in last few days.