I’ve been getting a lot of questions about using Endowus to invest CPF and SRS funds, so I figured let’s do a deep dive.

In this article, we’ll look at:

- What you can invest your CPF in?

- When should you invest your CPF?

- Does it outperform CPF’s 2.5%?

Endowus CPF Core Portfolios

The funds that you can invest CPF through Endowus Core portfolios are:

- Equity

- Vanguard-managed Infinity US 500 Stock Index Fund | Endowus Exclusive

- Vanguard-managed Infinity Global Stock Index Fund | Endowus Exclusive

- First State Dividend Advantage

- Schroder Global Emerging Market Opps Fund

- Bond (Fixed Income)

- Legg Mason WA Global Bond Trust

- UOB United SGD

- Eastspring INV UT Singapore Select Bd Fund

The 2 that caught my eye are the Vanguard US 500 (S&P500), and the Vanguard Global Stock Index fund (MSCI World Index).

As it stands, Endowus is the only platform that can access these 2 funds for CPF investment – S&P500 and the MSCI All World Index.

The reason is that CPF index funds must have a total expense ratio of less than 0.5%.

Endowus is able to achieve this because they rebate all trailer fees (kickback commissions paid by fund managers) to users, which reduces the total expense ratio.

Also, as part of their advised portfolio, you get First State Dividend Advantage, which is an Asia ex-Japan fund that invests primarily in blue chip, high dividend yield companies and Schroder Global Emerging Market Opps Fund which targets emerging markets globally.

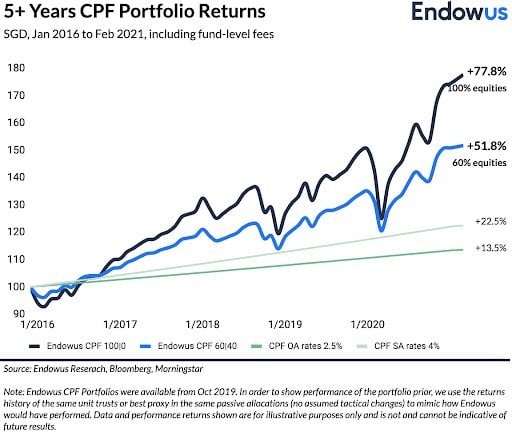

Historical Returns of Endowus CPF Portfolio

As you can imagine, stock markets have been very strong the past 5 to 10 years.

So historical returns are very strong compared to CPF-OA, which is stuck at 2.5%.

Benchmark of Endowus’s portfolio vs CPF-OA below, investing in stocks via Endowus blows away the return from CPF.

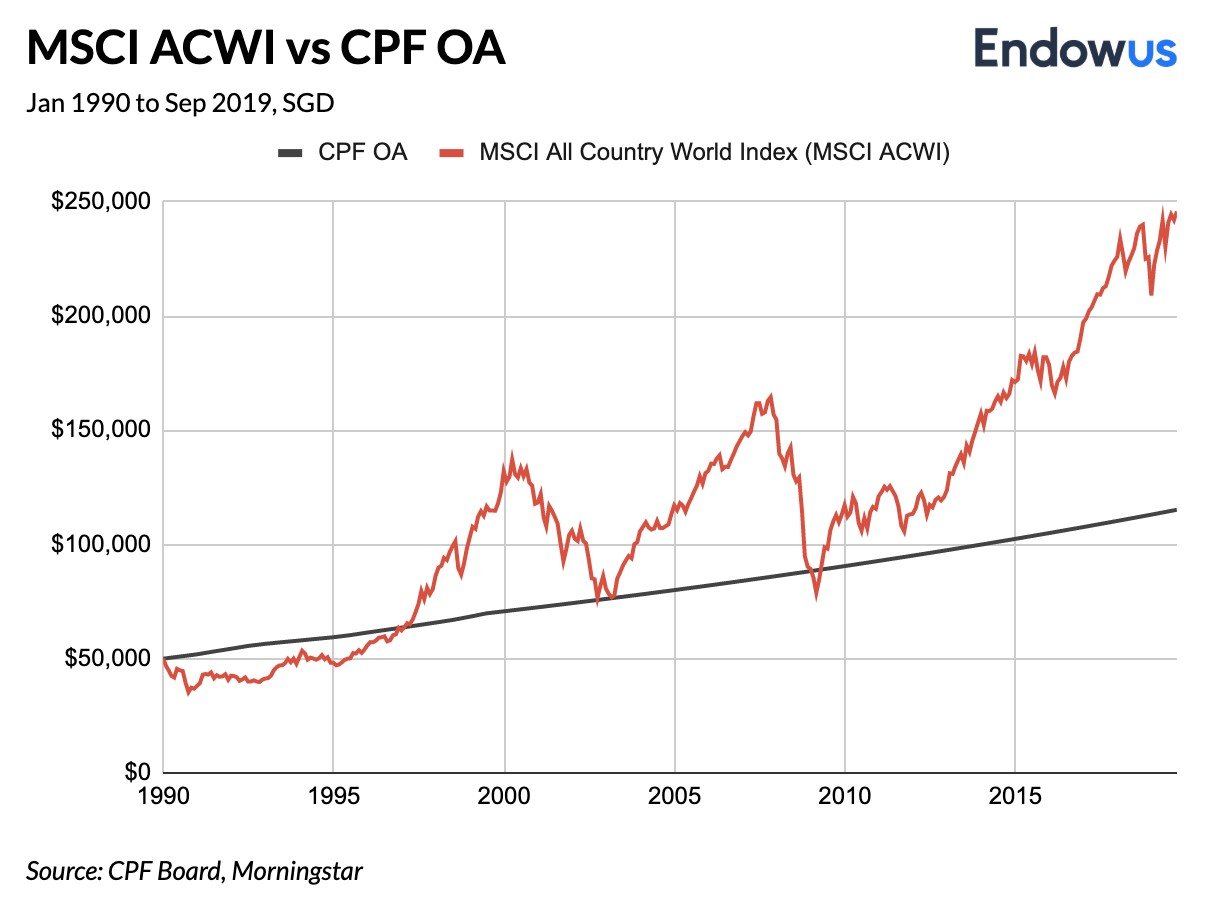

Likewise for the MSCI All Country World Index, it handily outperforms CPF-OA over a 30 year period (392% vs CPF’s 130%).

The long story short – if you take a long enough timeframe, such that you can ride out short term volatility, equity markets will almost always outperform CPF-OA which is fixed at 2.5%.

Future returns for Endowus CPF?

But that’s all in the past – what will we see going forward?

I’ve shared a lot of my macro views here in the past, and to sum it up I think the coming decade may potentially be an inflationary one.

Governments and central banks are going to be pumping a lot of money into the economy in the years to come, and at some point in time, that could prove to be inflationary.

Gun to my head, I would say that over the next 10 – 20 years, money invested in the S&P500 / All Country World Index is *probably* going to do better than 2.5% a year.

If stocks underperform, will CPF rules change?

The other thing to note, is that these matters are not mutually exclusive.

CPF-OA funds need to be invested somewhere too, to be able to pay the 2.5% interest.

If we have a 20 – 30 year period where global stock market and risk assets are unable to achieve a 2.5% return, I find it hard to believe the CPF redemption rules would not be affected. Where would the money come from?

So it’s not a zero sum game here, the 2 issues are intimately linked.

Longer term, putting money into stocks via Endowus could be a great way to juice returns, if you want something higher than the CPF 2.5%.

What if you need the CPF money short term?

The big caveat I would add, is that the money needs to go in for a long enough period, such that you can ride out short term volatility.

The chart below shows this well.

If you invested at the worst possible 20 year period – buying in at the Dot Com boom in 1999, there are a couple of periods where you would be underwater, and underperforming CPF-OA’s 2.5%.

But as long as you keep holding, at some point in time, stocks eventually recover against CPF.

So investing time frame is really important.

And if you dollar cost average when markets decline, the performance will be significantly better than in the chart shown above, which is pure lumpsum investing.

Endowus CPF Fees

You pay a 0.4% fee per annum to Endowus + the underlying fund level fee.

If you choose to invest only in the S&P500 fund through Endowus Fund Smart, the fund level fee, nett of trailer fee rebates is 0.395%, so the total fee is 0.4 + 0.395 = 0.795%.

Frankly, there’s no benchmark to this, because there is literally no other player on the market that allows you to access the S&P500 with your CPF money.

The other ways are usually via an actively managed unit trust, with all-in fees of 1.5% and above.

Safety – Custodian Structure via UOB

All funds that you deploy with Endowus are held via a segregated custodian structure with UOB Kay Hian, so there’s no worry about Endowus’s insolvency risk.

If Endowus goes under, the money is held in UOB Kay Hian, in your name.

You even get monthly account statements from UOB Kay Hian, which is a pretty nice touch.

How much of your CPF-OA can you use?

With CPF-OA, you can invest anything in excess of the first S$20,000 with Endowus.

So if you have $100,000 in CPF-OA, up to $80,000 can go into Endowus’ funds.

How would I use Endowus for CPF-OA?

Personal view – if I were going to invest CPF-OA monies long term, I would just chuck it all into a S&P500 / MSCI World Index fund, and hold it long term. For those who want an advised solution, they can also consider using the Endowus advised portfolio, given that they are working with the fund managers to add in new funds that will improve on the advised portfolio.

I think that over a 20 – 30 year period, the stock index is just going to beat CPF-OA’s 2.5% hands down.

Central banks and governments are going to inject a lot of money into markets in the coming decade.

BUT – these must be funds that I do not need to use short term.

If I’m saving up my CPF-OA to buy a house, or to build up a cash buffer, then I’m not going to be taking any risks with it, and the 2.5% is pretty attractive compared to cash accounts which yield 1% these days.

Invest your SRS with Endowus?

You can also use Endowus to invest SRS Funds.

Whether to use SRS is a whole topic in itself, that I discussed in a previous article.

The benefit is that it gives you tax benefits (no tax on the amount that goes into SRS), but the drawback is that the money is locked up until 62.

It will make sense only if your income bracket is above a certain level such that you’re paying serious amounts of tax (11.5% to me is the range where SRS is worth considering – after the first $80,000 of chargeable income).

What can you buy with SRS Funds?

The list of SRS funds in the Endowus Core Portfolios are set out below, and again it is made up of different funds for diversification.

Equity

- Dimensional Global Core Equity

- Vanguard-managed Infinity US 500 Stock Index Fund

- Dimensional Emerging Markets Large Cap Core Equity

- Dimensional Pac Basin Small Companies

Bond (Fixed Income)

- PIMCO GIS Global Bond Fund

- PIMCO GIS Income Fund

- Dimensional Global Core Fixed Income Fund

- PIMCO GIS Emerging Markets Bond Fund

Dimensional Funds are included – which are this series of well-known funds with a tilt towards value.

Value has been doing very well since the start of 2021, and if inflation is going to emerge in the years ahead, could continue to do very well going forward.

But if you want something more straightforward, choosing the US S&P500 through Endowus Fund Smart is also an option.

When to use Endowus to invest SRS?

Because of how SRS works (long term lockup, hard to deposit funds in), I think the ideal investment for SRS is a growth stock that you can just park funds in, and hold for a 20 – 30 year period.

The problem with the banks / REITs is that they pay good dividends (never thought this would be a problem), which creates a lot of cash stuck in SRS over time. You will need to manually reinvest that money each year. And sometimes the REITs will do a rights issue, which is tricky if there’s no cash in your SRS at that time.

The Singapore listed ETFs (eg. OCBC Hang Seng Tech) are a decent option, but they come with poor liquidity, and expense ratios are usually quite high.

So frankly, the funds from Endowus – S&P500, MSCI all world, or Dimensional funds are all great choices for SRS.

Responses from Endowus team

Endowus was kind enough to volunteer to answer any of my queries, so I posed a couple to them below.

My questions, and their responses below:

Why does Endowus uses unit trusts which have higher fees than ETFs?

Endowus: Unit trust and ETFs are both pooled investment products that can offer low cost, diversified exposure to equities and bonds. For many of us, we have only come across unit trusts that are high cost because of

- complex structures and fees because they are part of an ILP structure

- high sales charges (1-5%) and platform fees (1-2% p.a.) from bank relationship managers or financial advisors

- high total expense ratios (up to 2% p.a)

At Endowus, you can get unit trusts that are not wrapped by complex structures, without paying sales charges, and pay a low platform fee for it. The unit trusts that we use are low cost as well, with a broad based, developer market unit trust going as low as 0.26% p.a. for its total expense ratio.

How does Endowus’s offering stand out from other Robos like StashAway or Syfe?

Endowus: Our entire tech stack and how our clients’ assets are custodied to the most stringent standards.

We worked closely with our broker partner, UOB Kay Hian, to keep all our clients’ assets in a personalised custodian account. Even though this setup is tedious and more resource intensive to maintain, it allows us to scale our tech stack to accommodate not just cash investments but CPF and SRS monies.

Other robos have built their platforms around pooling and co-mingling clients’ monies in a single custodian account, which means that they are acting as a fund manager rather than an advisor. There are very stringent criteria to be onboarded as a CPFIS approved fund manager, which includes investment track record, low fees.

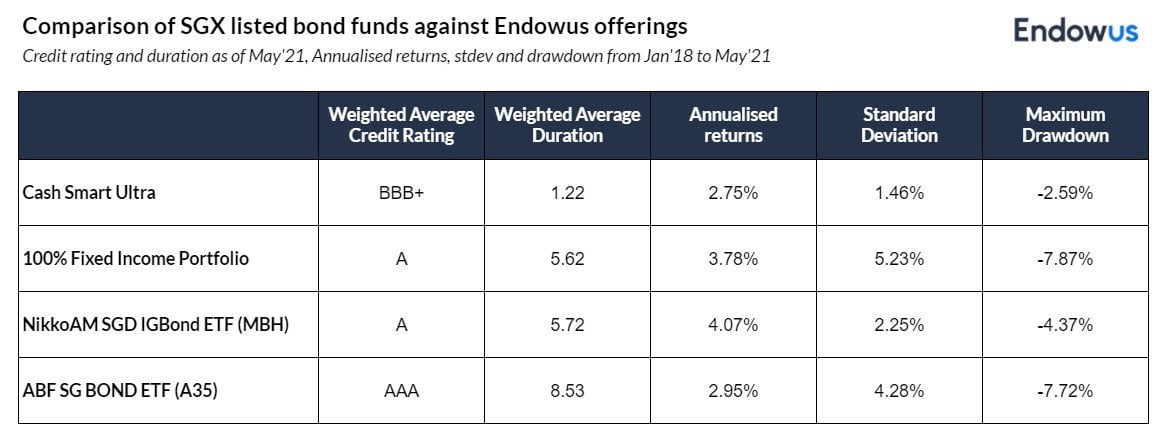

What do you think about Cash Smart Ultra as an alternative to bond ETFs like MBH and A35?

Endowus: The SGX listed bond funds, such as MBH and A35, are generally high credit quality (A and AAA) funds but have long weighted average duration (5.68 years and 6.25 years). This means that the funds are susceptible to greater interest rate risk, which is a concern in this low interest rate environment. This might be a concern if they invested in these bond ETFs with the expectation that there would be low volatility.

As you can see from the table above, while there is better credit rating for the two bond ETFs, the funds’ standard deviation and maximum drawdown are higher than that of Endowus Cash Smart Ultra.

As an investment advisor, we recommend that you have a more diversified allocation in fixed income beyond just a few companies or even geographies.

Top holdings of MBH

If you are looking to keep your money in a lower duration risk portfolio, cash smart ultra is a great choice, else our 100% core portfolio is also another option that you can choose in place of a SGD-hedged fixed income exposure.

Endowus Promo Code / Referral Link

When you create your account from this promo code / referral link, you will get S$10,000 managed free for 6 months ($20 equivalent). So don’t forget to use it.

Referral Link: https://endowus.com/r?code=FH_XOKU9GZMTJ

Closing Thoughts

Frankly, the ideal place to park CPF and SRS funds are low cost index funds, and just leave them there until retirement.

That wasn’t possible in the past, but Endowus now offers that optionality, which I think is absolutely fantastic.

The fees are not as low as if you’re investing directly with cash, but it’s still way better than the other options available.

So if your funds are sitting around in CPF-OA / SRS doing nothing, and you plan to invest for multi decade periods, I think Endowus CPF / SRS is a really solid option worth checking out.

Love to hear what you think though!

Note: This post was sponsored by Endowus. All views and opinions expressed in this post are from Financial Horse.

Hello Finance horse,

Thanks for the article. Quick question, if we invest in this Endowus S&P500 and the MSCI All World Index product. Does thee product have certain guideline or rule that they will pay out dividend on regular interval? Or these products are more like buy now when their price is low and wait for 20 to 30 years later and hope that these product price will shoot up and sell it off for one time profit.

Thanks

That’s a great question. These look to be acumulating funds – so the dividends will be reinvested into the underlying stocks.

So the gains will be capital gains – buy now and wait 20/30 year to use your example. 🙂

More details here:

https://endowus.com/support/360000618721-fund-rationale:-lion-global-infinity-us-500-stock-index-fund/?utm_source=affiliate&utm_medium=financialhorse&utm_campaign=sponsored&utm_content=july21CPFSRSarticle

Hi FH,

Does Endowus allow investing in just one of the funds (e.g. US 500), instead of the entire core portfolio?

Yup possible – just use your CPF or SRS and customize your own solution via Fund Smart: https://endowus.com/fund-smart

Hi FH, thanks for the comprehensive article! I know it’s an old article, but I would still like to ask a question. If you are dumping the whole money in SRS to index fund, why not just do it yourself instead of paying the extra fee to Endowus? I’m wondering if you calculated if the tax benefit is more than the platform fee in the long term. Thanks again!

Also, you could get a much lower fund fee if you invest it yourself e.g. 0.07% for CSPX (S&P500)

Sorry not quite sure if I understand the question. With SRS funds you will not be able to use it to invest in an offshore ETF if I am not wrong? Hence Endowus was the workaround rather than using a local ETF which has high fees as well and poor liquidity.

That said the more efficient way is to probably use SRS to buy Singapore stocks, and use cash to buy the offshore ETFs to optimise the fee structure.

Hi FH, would like to seek your views on another option that I am thinking about. How about investing in the Lion-Infinity Global index fund AGD Class C (which aims to replicate the MSCI All World index) using FSM RSP. No sale charges. For CPF, there is no platform charges. You just pay the expense ratio which I think is now 0.46%? You do not need to pay the 0.3% Access fees that Endowus charges. Wouldn’t this be cheaper?

Hi J – I have not double checked your numbers. But if you’ve done the research and the numbers check out, then yeah I would agree with you!