Now A LOT of you have asked me for my views on money market funds.

Higher yields than Fixed Deposit / T-Bills.

No lock-up period, free to withdraw any time.

What’s the catch right?

As should be obvious to you by now, there is no free lunch in investing.

When something is too good to be true, it almost always is.

Money Market Funds are quite a nuanced product and it’s not so easy to appreciate the pros / cons at first glance.

So I wanted to do a full article to discuss this.

Do note that there are many different types of money market funds out there

First off – there are many different money market funds on the market.

Some invest in fixed deposits, some invest in short term bonds and so on.

It’s always a trade off between yield, duration, and risk.

So each money market fund is different, and you need to analyse each of them on their own merits.

For today’s article though, I’m going to discuss the most popular money market fund out there – Fullerton SGD Cash Fund

With an Assets Under Management of $2.6 billion, this is one of the biggest SGD Money Market Funds today.

Basics: Fullerton SGD Cash Fund pays a 3.88% yield on cash – Better buy than T-Bills or Fixed Deposit? Are Money Market Funds a must buy?

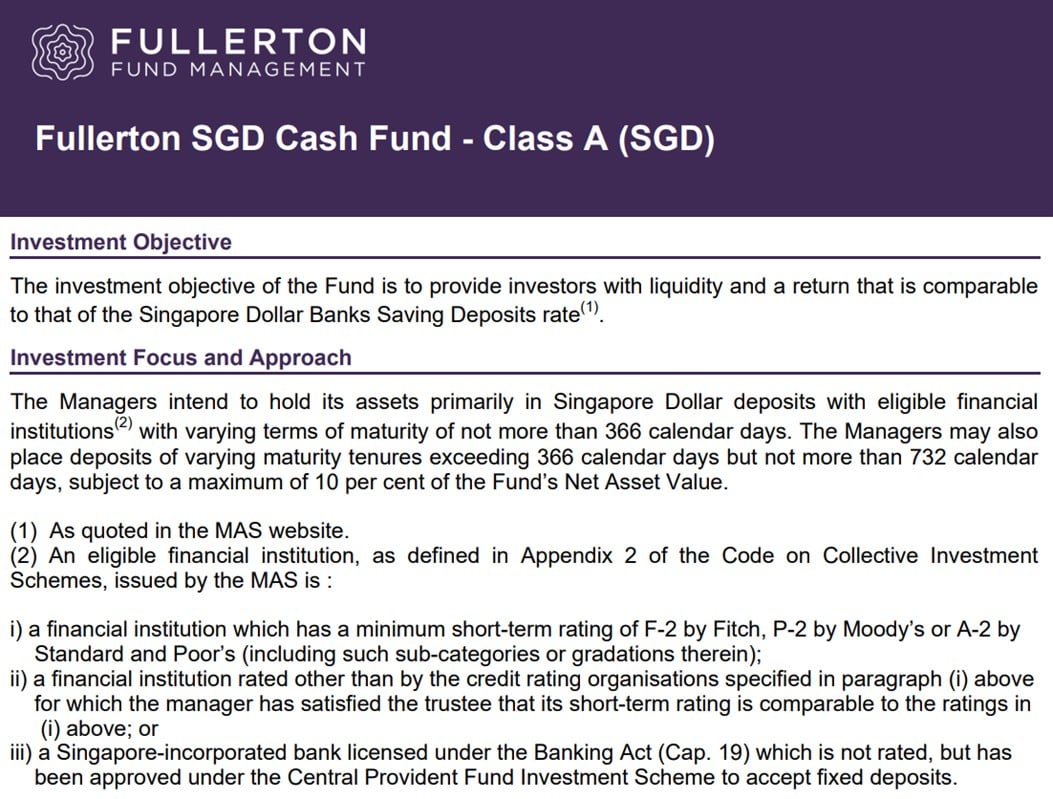

The investment objective of Fullerton SGD Cash Fund is:

to provide investors with liquidity and a return that is comparable to that of the Singapore Dollar Banks Saving Deposits rate

Or in plain English – they put the money into short term fixed deposits.

Asset Allocation of Fullerton SGD Cash Fund – What are you buying?

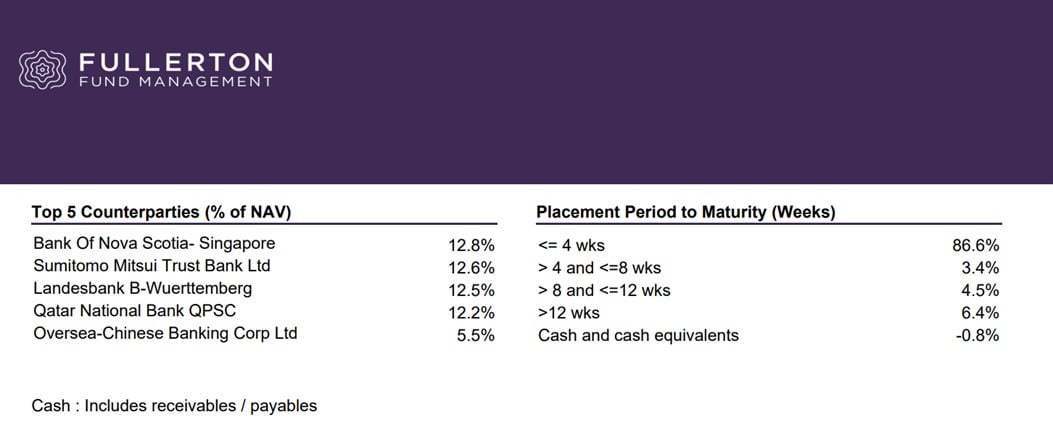

You can see the asset allocation of Fullerton SGD Cash Fund below.

The money is invested with fixed deposits with banks.

And 86% of the portfolio has a maturity period of less than 4 weeks.

This is quite different from the USD money market funds which tend to buy either T-Bills or Commercial Paper (short term debt issued by corporates).

This is because the markets for SGD Commercial Paper are not as deep and sophisticated as that for USD, so the SGD money market funds have to resort to putting the money into fixed deposits instead.

There are 3 key features of Fullerton SGD Cash Fund I want to talk about:

- What is the yield on Fullerton SGD Cash Fund?

- What is the default risk?

- Can you get your money back any time without a penalty?

What is the Yield on Fullerton SGD Cash Fund – Money Market Fund

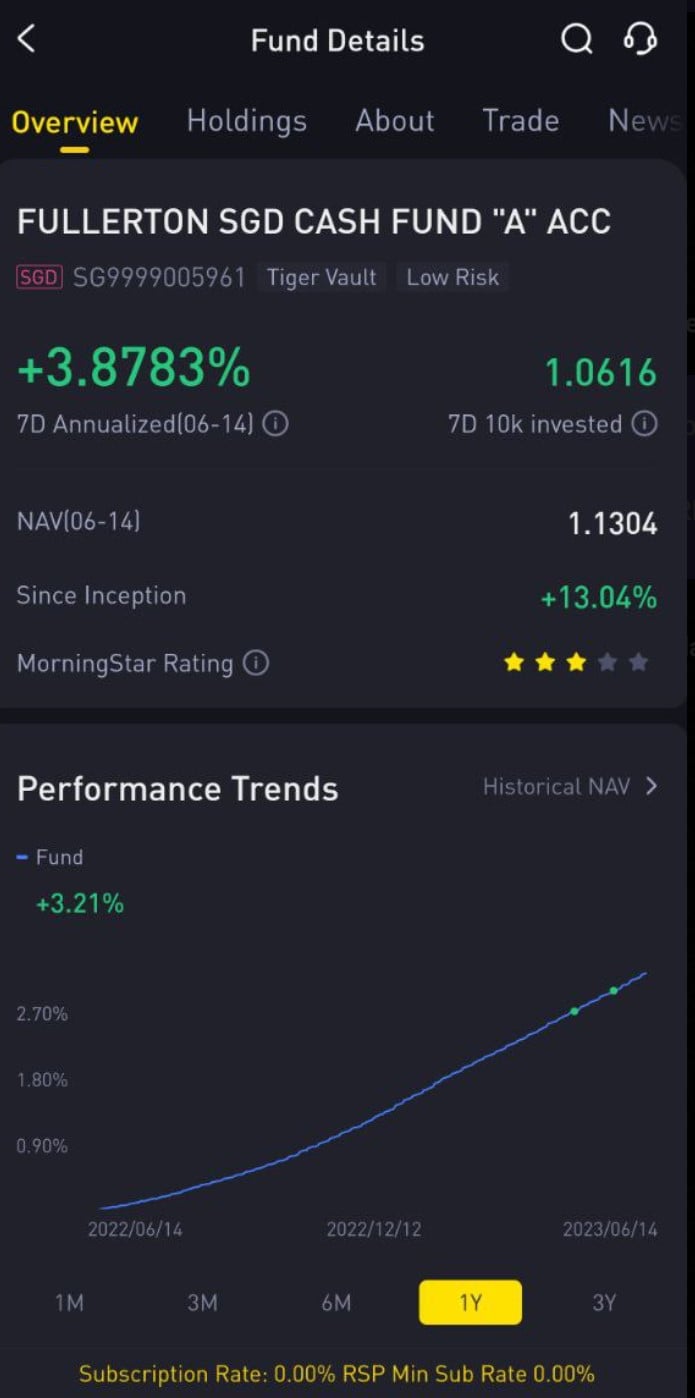

Now the 7 day annualised yield is 3.88%.

But… the yield is “floating”

But here is where things get tricky.

If you recall – 86% of Fullerton SGD Cash Fund’s assets are placed in fixed deposits with a maturity of less than 4 weeks.

Let’s put it this way.

Imagine that you have $1 million cash, and $860,000 of that is continually rolled over in a 4 week fixed deposits.

What yield would you get over the next 12 months?

This has exactly the implication you would think it has.

So unless you can predict what the bank fixed deposit rates will be over the next 12 months – nobody can tell you the anticipated yield on the Fullerton SGD Cash Fund.

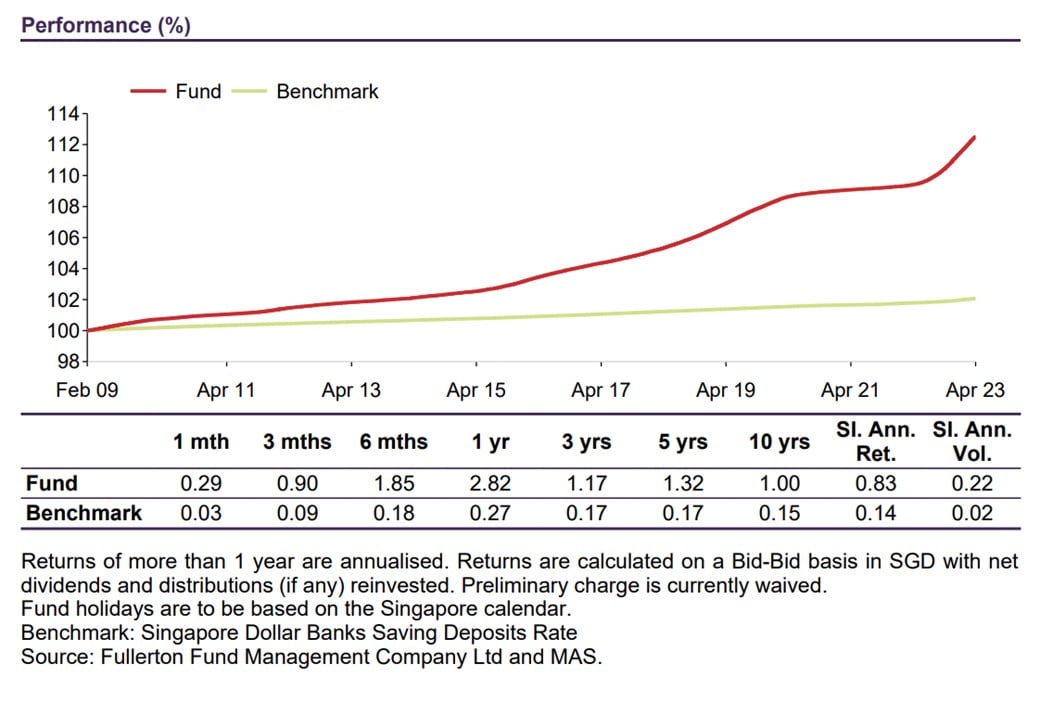

What about the historical yield on Fullerton SGD Cash Fund?

You can see this in the historical yield.

If you annualise the 1 month return you’re looking at a 3.48% return.

If you annualise the 3 months return you’re looking at a 3.6% return.

If you annualise the 6 months return you’re looking at a 3.7% return

If you take the 1 year return you’re looking at a 2.82% return – because fixed deposit rates were very low 1 year ago if you remember.

And if you annualise the 7 day return, you’re looking at a 3.88% return.

Long story short – the yield moves around a lot, depending on where bank fixed deposit rates are at that point in time.

Effectively, Fullerton SGD Cash Fund is a “floating” interest rate Money Market Fund

So you can think of Fullerton SGD Cash Fund as a money market fund that will give you the yield paid on bank fixed deposits.

If bank fixed deposits are high (like it was in late 2022 or early 2023), you will get a good yield.

If bank fixed deposits go down (like they are right now), you may not get such a good yield.

This is an important distinction vs the usual T-Bills or Fixed Deposit or Singapore Savings Bonds you may be used to.

With those, you know exactly the yield you get upfront.

If you’re buying a 3.55% fixed deposit for 12 months, that’s the yield you’re going to get.

No surprises.

With a money market fund like Fullerton SGD Cash Fund, you’re effectively repricing your interest rate every 4 weeks.

FH… Can you estimate the yield on Fullerton SGD Cash Fund going forward?

As you can imagine, it is really, really tough to estimate the yields going forward.

You may have noticed that most banks have been repricing their fixed deposit rates down aggressively the past month or two.

Whether this will continue the next 12 months is anyone’s guess.

So the returns over the past 6 months were about 3.5 – 3.8%.

After 0.15% fees (charged by the fund) you’re probably looking at about 3.4 – 3.7% ish yields.

And I think as a general note, that’s probably the kind of yields you might see going forward.

3.4 – 3.7% ish yields

Default Risk of Fullerton SGD Cash Fund – Money Market Fund?

What about default risk?

Is there any chance you can lose your money?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Please note that Money Market Funds are NOT SDIC Insured – not risk free

Here I want to make an important distinction.

Money Market Funds like Fullerton SGD Cash Fund are NOT SDIC insured.

This is unlike a fixed deposit where if the bank goes under, all amounts up to $75,000 are insured.

Or unlike T-Bills or Singapore Savings Bonds which are backed by the Singapore government.

With a money market fund, if the underlying assets default, you could be looking at capital losses.

What is the default risk on Fullerton SGD Cash Fund?

You can see the top 5 counterparties below.

Mostly globally systemically important banks.

What is the chance of an underlying default by one of these banks?

Incredibly low I would say.

But I would not say it is zero risk, unlike a T-Bill or a Fixed Deposit under $75,000.

This is important to note.

Money Market Funds like Fullerton SGD Cash Fund can be redeemed any time – T+1 Liquidity

The big advantage of money market funds like Fullerton SGD Cash Fund though.

Is that they can be withdrawn any time, without any penalty.

The usual settlement is T+1.

Which means that if you submit a redemption request today, you can get your money back by tomorrow.

If you submit the request before 12pm, you may even be able to get the money back the same day (see the summary from Tiger Vault below):

This is unlike Fixed Deposits where breaking early will cost you your interest.

Or T-Bills where it is really tough to sell your T-Bills prior to maturity.

This is a big advantage of Money Market Funds like Fullerton SGD Cash Fund.

And arguably the main reason why you should even consider putting your money here instead of T-Bills or Fixed Deposits.

The redemption is paid for directly using the fund’s assets, which means you don’t need to worry about trading liquidity (as compared to instruments that are listed on a stock exchange).

There is a small catch though… that you may suffer capital losses

There is a small catch though.

In that when you submit the redemption request to get your money back, you don’t actually know how much you’re going to get back.

The amount you get back will be based on the price of the fund.

In plain English, let’s say you submit your redemption request at 1pm on Monday.

The amount you get back will be tied to the Fund’s NAV, which will only be updated at 15:30.

So it is theoretically possible that you can submit your redemption request to get your money back.

On that day itself something goes really wrong with the underlying assets that forces a markdown in NAV.

And the amount you actually get back may suffer capital losses.

What is the chance of this happening?

Yes, it is a slim chance I know.

But the details do matter, especially when you’re parking cash in somewhere you think is supposed to be safe.

And especially when your alternative is risk-free like Fixed Deposits or T-Bills.

99.99% of the time the details like this don’t matter.

But the 0.01% of the time it matters – think 2008 or March 2020, it really matters.

How to buy Fullerton SGD Cash Fund – Money Market Fund?

There are 2 ways you can buy money market funds like Fullerton SGD Cash Fund:

- Traditional Fund Management Platform

- Stock Brokers

Buy via Traditional Fund Management Platform

The first is to buy it via a traditional fund management platform – think Endowus, FSMOne, DBS etc.

The problem with this approach, is that you have to pay fees to the fund management platform.

However if you use Endowus, their fund management fee is 0.05%, and there is a trailer fee rebate of 0.05%, so effectively you’re not paying any platform fees.

Liquidity will be T+1 though.

Buy via Stock Brokers

That said – the best way to access Fullerton SGD Cash Fund might actually be via the stock brokers – Moomoo, Tiger Brokers, Webull etc.

There’s 2 major benefits with buying via a stock broker:

- No platform fees

- Instant liquidity

No Platform Fees

Here’s Moomoo Cash Plus, which allows you to invest your cash in Moomoo with Fullerton SGD Cash Fund.

They charge no subscription, redemption, or platform fees.

Instant Liquidity

And the best part – any funds invested in Fullerton SGD Cash Fund (via Moomoo Cash Plus) can be used to buy stocks instantly.

You don’t need to wait for T+1 (until the money hits your account) to buy stocks.

How this works is that Moomoo is effectively giving you a bridging loan to fill the gap between the time when you submit the redemption request, and the time Moomoo actually gets the money back from Fullerton SGD Cash Fund.

This only applies if you are buying stocks though, if you want to withdraw the cash you still need to wait for the redemption request to complete.

So like I said, funnily enough the best way to access Fullerton SGD Cash Fund might be via the stock brokers.

You don’t pay platform fees, and you get instant liquidity to buy stocks.

Do note counterparty risk

That said, I do appreciate that not everyone may be comfortable putting their life savings in a stock broker just to access a money market fund at lower fees.

Unlike with a traditional platform like Endowus or FSMOne where the asset holding structure is clear (that the assets are held in your name).

With some of these brokers I couldn’t really confirm how the assets are held, and what would happen in the event of insolvency.

If this worries you you can also consider using Endowus or MoneyOwl, which effectively don’t charge platform fees for Fullerton SGD Cash Fund.

But you won’t get the instant liquidity you get with the stock brokers though.

Money Market Funds are more complex instruments – Intended for institutional investors to park cash

As you can see from the discussion above.

Money Market Funds are a much more complex instrument vs your usual T-Bills or Fixed Deposits:

- Interest rates are “floating” – both good and bad

- Can be withdrawn any time

- Not SDIC insured or risk free (but low risk)

They are generally intended as a place for institutional investors or corporates to park cash short term to earn a higher yield, with a good liquidity profile.

Think of a company with $10 million set aside for an M&A deal, and they want to park it somewhere until completion.

Or a company who just received $500,000 from a customer, and is parking it somewhere until it gets paid out to suppliers.

Will I buy Fullerton SGD Cash Fund vs T-Bills or Fixed Deposits?

Full disclosure that I do have some funds parked in Fullerton SGD Cash Fund.

But this is primarily spare cash that I hold in Moomoo or Tiger Brokers or Webull, that I have not invested in markets yet.

I see this as the primary use of money market funds like Fullerton SGD Cash Fund – as a place to park short term cash, until they can be deployed for other purposes.

The bulk of my cash is still held via a mix of:

- High yield savings accounts – like UOB One or UOB Stash Account

- T-Bills

- Singapore Savings Bonds

- Fixed Deposit

I would buy T-Bills over money market funds like Fullerton SGD Cash Fund today

As of today, I still prefer T-Bills over money market funds.

With yields of 3.84%, T-Bills have very competitive yields vs money market funds.

Given how things are playing out, I do think there is a risk that bank fixed deposit rates may be cut further in the months ahead.

So I like the ability to lock in 3.84% for a 6 months period.

T-Bills are also risk free.

No doubt the risk on Fullerton SGD Cash Fund is very low, but when I can get risk free at 3.84% why do I need to bother with low risk?

I don’t deny the lack of liquidity (for T-Bills) is a problem.

Because of that I do need to maintain some cash in high yield savings accounts and Singapore Savings Bonds come in for me – to provide a healthy pool of cash I can draw on if I need urgent funds.

But for the right kind of investor, I think money market funds like Fullerton SGD Cash Fund can have a real place in your portfolio.

The risk is low, and you’re getting very competitive yields with fixed deposits, and you have T+1 liquidity.

Closing Thoughts: This is just the basics of money market funds, you can take on more risk / duration for a higher yield

There are a whole bunch of other options like EndowUs Cash Smart which mixes and matches money market funds to achieve higher yields (by taking on a longer duration and higher risk).

Generally speaking though, the analysis above holds true.

There’s really no free lunch in this world.

It is up to each investor to decide the right balance between yield, risk, duration and liquidity.

Money Market Funds do offer much better liquidity, but that can come at the cost of yield and risk.

This article was written on 16 June 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

– Get up to USD 500 worth of fractional shares (expires 30 June)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- and fund $100 SGD

- Maintain for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

When your treasury bills bought using CPF reach their maturity dates 6 or 12 months later, there is usually a gap of around 14 days or longer before you can purchase new treasury bills. In the meantime, you will get very low interest rate offered by the CPF agent bank. Will you purchase Nikko AM Shenton Short Term Bond SGD using CPF first and redeem them in time to participate in the auction for the next treasury bills? Nikko AM Shenton Short Term Bond SGD 6 months return is 1.98% which is 3.96% annualized. I wish you could write an article on the best action to do when treasury bills bought using CPF reach their maturity date as there is no automatic roll-over mechanism and the gap of 14 days or longer will significant hit the actual returns for retail investors using CPF to purchase treasury bills.

T-Bills are risk free though. All the other options like bond funds entail risk.

When CPF T-Bills mature, just roll them over into the next available T-Bills. Or if T-Bills rates are not attractive at that point in time, just withdraw back to CPF-OA. 🙂

Hi FH; apologies, a dumb question. When I look on apps like Apple Stocks and FSM, each one does not provide any yield data for the Fullerton SGD Cash A Fund. On the Fullerton web site it has “N” (meaning I think No) next to “Distribution” in the description of this fund (“share class A). In share class C the indicated distribution is “Every yeti months). However I can’t find that share class in any of my platforms. Do you know which is the actual yield paying fund and how to tell which one you are dealing with?

Thanks in advance

The most accurate is to pull up the actual fact sheet / historical data from the Fund website itself.

Alternatively Endowus/FSMOne’s website usually has fairly good data tracking on this.