I received a few queries from readers the past week:

Hi FH, I remember you were talking about the double dip in the stock market… do u still think it is going to happen?

Hi FH, what are your views on the current market conditions. Do you think this rally is sustainable (looking to add more positions), or is a bear market rally?

Great questions! I touched on this the past week, but I think this deserves a full article.

I’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, do consider – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything. Sign up below (you get a free guide when you sign up):

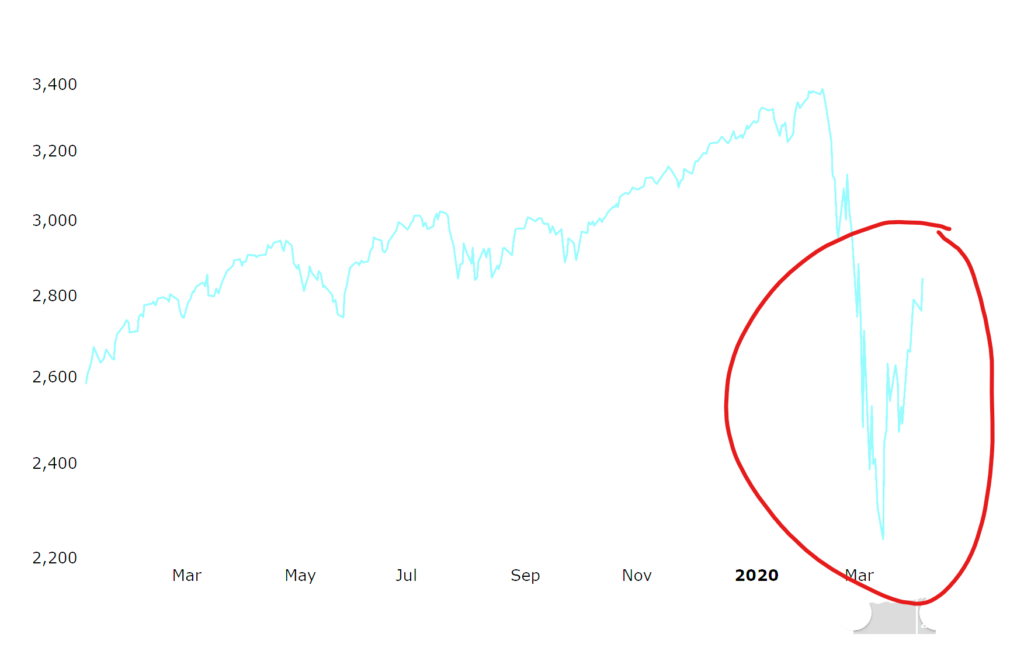

Basics: How have stocks performed so far

This chart gives you an idea of where the S&P500 has been so far. It was a 34% fall from the top, then about a 50%+ retrace of the fall, which is roughly where we are today.

And where do I think we will go going forward?

Now it’s important to note that predicting the future is not a science. This isn’t a math equation that if I solve it right, I know what happens next.

Instead – It’s all about shifting probabilities. If you think that there is a 60% probability something happens, and it doesn’t, it doesn’t mean you’re wrong. It just means the future that materialized wasn’t the high probability event.

Which is why in investing you never bet the house. When you bet on probabilities (like poker), one day you will be wrong. And if you bet the house, one day you’ll lose the house.

That’s important to understand.

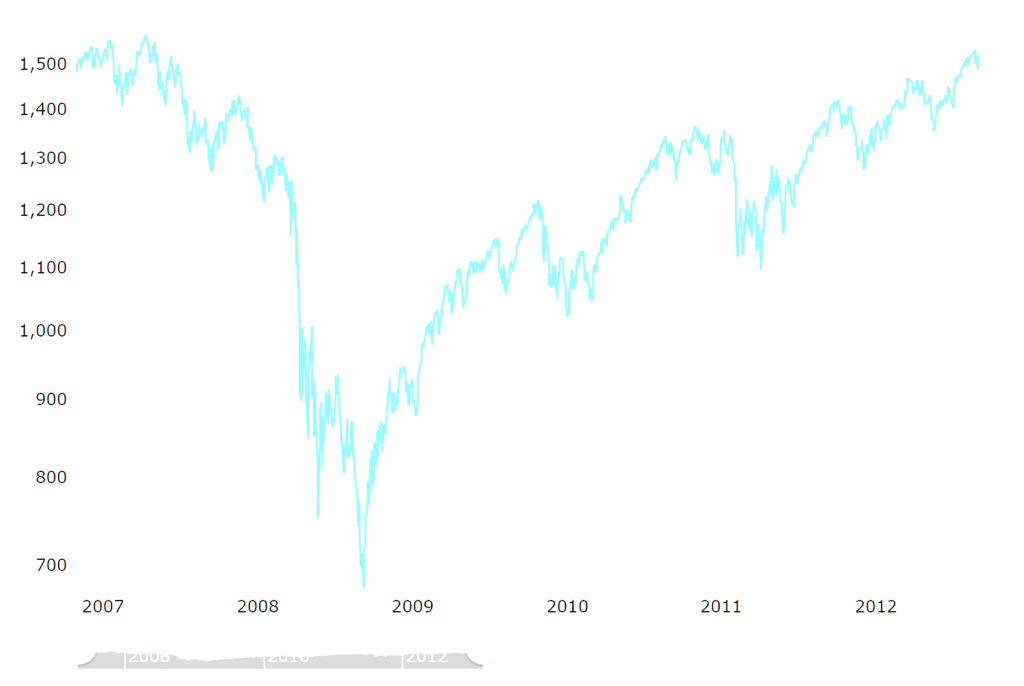

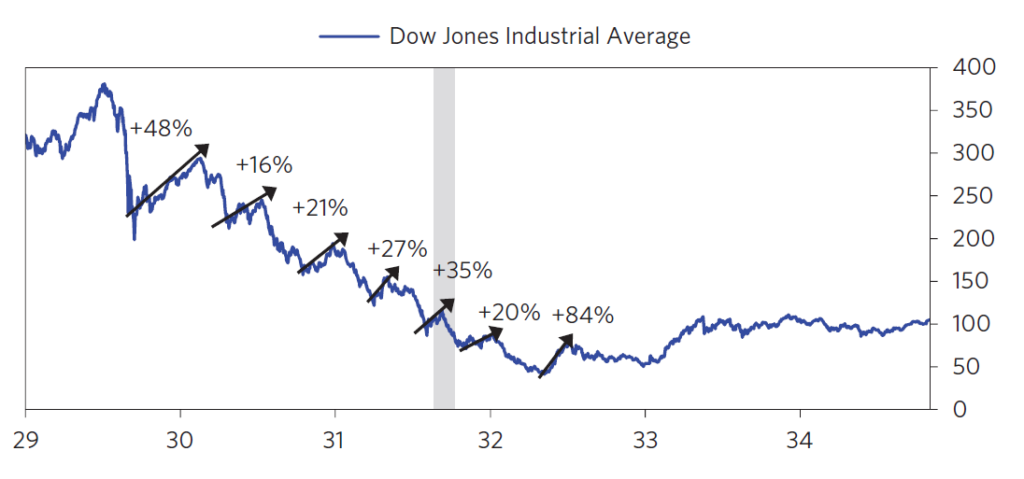

Historical Precedent – Why do stocks double dip / have a complex bottom?

I’ve set out the charts for 2008 (S&P500) and 1930s (Dow) above.

What is clear, is that stocks never bottom so quick. In 2008, the bottoming process took about 12 to 18 months depending on when you start counting. In 1930s it took about 3 years.

But the key lesson goes beyond the charts. The key lessons goes back to understanding – why did stocks take so long to bottom?

I’ve been reading up on the 1930s and 2008 recently. My thinking so far, is that it usually plays out like this:

- Step 1 – At the start, a lot of bad news happens, and there is a big fall in stocks. Then the monetary stimulus comes (interest rate cuts, easy liquidity etc), and investors think that stimulus will offset the economic impact. Stocks go up.

- Step 2 – As stocks go up, underlying economic data continues to deteriorate. At some point, investors recognize that the economy is not picking up, and stocks start going down again. Usually at this stage, we see mass unemployment, and corporate bankruptcies.

- Step 3 – Eventually, when things get bad enough, governments and central banks coordinate to unleash a gigantic fiscal + monetary stimulus via money printing to replace lost credit. When this happens (usually when stocks hit depressed valuations), that marks the bottom in stocks. From then on, the economy usually takes a few more months to bottom, but stocks have already bottomed.

This played out in 1930s, and it played out in 2008. Take a look at any other deflationary crisis and you will find that it plays out this way too.

Will 2020 be the same?

So let’s apply this to 2020.

The key difference between this crisis and the previous ones, is that central banks and governments are very quick to respond with stimulus. It’s about 1 month into the crisis, and we’ve already seen the Feds unleash their entire 2008 playbook (and then some more). Congress has already passed a $2 trillion dollar stimulus. The ECB has restarted QE, in a big way. Even Singapore and Hong Kong have come out with stimulus packages that are a large % of our GDP.

In no other prior deflationary crisis – have governments and central banks responded this quick, this early into a recession.

That’s definitely unprecedented.

So the million dollar question now – is that will this be sufficient to shortcut the deleveraging process. Will we still have Step 2, or do we skip straight to Step 3?

There are 2 ways this plays out:

- Scenario 1 (Classical Economics) – The classic scenario. We go from Step 1 (now) to Step 2, and then Step 3. Stocks will either have a retest of prior lows, or stocks will break prior lows. This plays out maybe over a 12 month period or more.

- Scenario 2 (MMT Economics) – Modern Monetary Theory. This theory basically says that governments should print unlimited amounts of money, because they can. Under Scenario 2 we go from Step 1 to Step 3 immediately. Stocks only go higher from here, and they will never retest prior lows. The decline in stocks takes place over March to April 2020. This will be a stagflation style scenario.

Scenario 2 is quite widely accepted

Scenario 2 may seem stupid – but it’s actually not.

A lot of really smart people believe in Scenario 2 right now – and it’s a popular opinion on Wall Street.

Lots of top investment banks like Goldman Sachs and JP Morgan now adopt this thinking for US stocks.

People who believe in Scenario 2 believe that the Fed’s actions, and Trump’s actions, have signalled a willingness to do whatever it takes. The Fed’s power is theoretically unlimited, so if stocks continue falling, they’ll just print another $10 trillion dollars, and if that doesn’t work, another $10 trillion. Oh if that still doesn’t help, they’ll just buy stocks like the Bank of Japan.

It’s perfectly legitimate, and makes perfect sense. I wouldn’t rule this possibility out.

My Personal Opinion?

So what is my personal opinion?

Feel free to disagree with me on this. In fact I’m actively looking for people who disagree with me.

But my current thinking – and I could be wrong, is that we still see Scenario 1. I don’t see this time being different.

Why do I say this?

I think that this time around, the economic damage has been / will be too massive.

Economic Damage will be unprecedented

The latest IMF forecast is set out above. The numbers are staggering. -5.9% for the US in 2020, -7.5% in the Eurozone. -1.2% across Emerging Markets.

These numbers make 2008 look like a cakewalk, and the only historical precedent here is the 1930s Great Depression or World War II.

So we’re looking at unprecedented economic damage, and because of that, we need an unprecedented stimulus package.

Everything the Fed does so far looks massive, because what will come is massive. But my thinking is that as at right now, it’s probably still not enough to forestall the coming wave of insolvencies and unemployment.

Liquidity =/= Solvency.

I’ve been using this phrase a lot on Patron recently. And I think this will be the defining theme as we move into Phase II of this crisis.

Most of what central banks and governments have done so far is to solve liquidity issues. It is to solve the financial plumbing, and to keep money flowing.

What it doesn’t do, is stimulate underlying earnings or cash flow.

Think about it this way. Will interest rates at zero, the Feds buying junk bonds, a stimulus check in your account – Will that make you go out and watch a movie? Or dine at a fancy restaurant? Or buy a new car? Or buy a condo?

Probably not right? You’re worried about the virus. And you’re also worried about the coming recession. All the talk about layoffs and paycuts makes you worried.

Your spending is someone else’s income, so when you stop spending, someone else loses their income. That guy then needs to reduce his spending, which hurts someone else’s income.

That’s a demand shock, and the longer this drags on, the worse it gets.

And then we also have a supply shock.

Lots of producers can no longer get the parts they need for production. It’s a byproduct of decades of just in time manufacturing.

One story recently caught my attention. It was about this chicken farmer, who couldn’t get any delivery of chicken feed during the lockdown period. He couldn’t feed the young chicks, so he had to kill them all. About 100,000 young chicks.

Now every industry is slightly different of course – but imagine this playing out across the globe. The car manufacturer who can’t get the parts they need. The goldsmith who can’t get his gold shipment.

That’s a supply shock.

And that’s the impact to the underlying economy.

All the Feds are doing – is trying to flood the economy with enough cash so that the financial system doesn’t break. The farmer who had to kill all his chickens? The car manufacturer who can’t make cars? Their earnings are still gone.

So the next Phase of this crisis will be an economic one. The Feds hands are tied here because of legislation – they cannot lend directly, nor can they stimulate consumption. That requires actions from the government. We’ve seen snippets of it so far from the $2 trillion bill, and the Singapore stimulus package. But it will need to be far bigger in size.

Any small delay, and a lot of business owners could be in real trouble.

Everything goes back to the USD

The way I see it, everything goes back to the USD.

If you can tell me where the USD goes from here, I can tell you where stock prices go.

A lot of people think that after the massive $6 trillion USD stimulus, the USD is going lower from here.

I disagree. I still think that the USD is going higher before all this is over.

Why? It all goes back to the demand and supply shock.

The US economy is about 20% of the global economy. But about 50%+ of global trade and commerce, is transacted in USD. That’s what being a reserve currency means.

Let’s go back to the chicken farmer. In the good days he sells his chickens to a supermarket maybe in the US. The supermarket pays him in USD. The farmer takes this USD, and he pays for chicken feed, and he buys more chickens. Maybe he uses it to invest in another farm. Maybe he takes up a USD loan, to fuel his expansion.

Now times are bad. The chickens are dead, so he can’t sell them for USD. Even if he can, the supermarket no longer takes his shipment. But he still needs to repay his USD loan. And he needs USD to buy new chickens after all this is over.

Of course this is a very simplistic analysis. But on a certain level, it’s what I think will play out over the whole world in 2020.

The Feds know this, which is why they’ve extended USD swap lines and repo lines to central banks all around the world. But that swap line is to a CENTRAL BANK.

Let’s go back to the farmer. How the heck is the chicken farmer going to get a USD loan from the central bank? He needs to go to a normal bank right? And the normal bank looks at the farmer’s situation, and they don’t want to lend, because the farmer has no cash flow right. What if the farmer goes bankrupt? Then the bank would be on the hook for the loan. So banks are reluctant to lend, and without that lending, the farmer is in trouble.

2008 was a financial crisis. I think 2020 will be a main street, corporate default style crisis. So the swap lines that worked in 2008 are of less use here, because who really needs the USD, is the SMEs, the corporates. Central banks will need to find a way to solve this, fast, because this could play out at a rapid pace in the second half of 2020.

What if they can’t solve this?

Back to the farmer example – what happens if he can’t get his USD loan? The farmer will have to sell his farm to get cash, and convert the cash to USD, to repay the loan. Multiply this across the globe and you have a huge demand for USD globally, which will cause USD to go up. The more it goes up, the more local currency the farmer needs to repay the same loan.

Again – a very simplistic analysis. But to me, this will be a key part of the endgame. If the Feds cannot stop the USD from going up, then a strong USD will crush most global economies.

There are no old, bold pilots

There’s a saying I really like:

There are old pilots, and there are bold pilots. But there are no old, bold pilots.

Investing is the same.

In investing, we are betting on how the future will play out. And the future is uncertain.

If you bet the house on an uncertain outcome, and you do it often enough, one day you will lose the house.

So don’t be like that. Take measured risks.

Create scenarios that if you are right, you win a medium profit – but if you are wrong, you still win a small profit.

Avoid scenarios where if you are right, you win really big – but if you are wrong, you go bankrupt.

Create a heads I win, tails I win scenario

The same logic applies here. There are 2 possible scenarios set out above. I think Scenario 1 plays out, but Scenario 2 is not impossible too.

How do I set up my portfolio to benefit in both scenarios?

I create a balanced portfolio, split among stocks, bonds, cash, gold, and real estate.

I really like Gold at this stage of the investment cycle. I have about a 10 to 15% position in gold, and it’s gone up a fair bit the past year. Gold is one of those key components of a balanced portfolio, and I think it will continue to be a good hedge for my portfolio going forward.

Let’s say Scenario 1 plays out. It’s a deflationary cycle short term, so gold price goes down, but my cash and my bonds retain their value. That ok to me.

If Scenario 2 plays out, it’s an inflationary cycle, so my gold goes up a lot, but my cash and bonds lose their value. That’s not ideal, but at least the gold went up a lot and offsets my losses elsewhere.

That to me, is the essence of asset allocation.

Run this analysis across the rest of your asset allocation, and you can decide the appropriate asset allocation for your risk appetite.

Once you have your baseline, you can then decide how to tilt your portfolio based on your read of the situation. I think Scenario 1 is more likely, so I tilt to bonds and cash. But I also retain my equities / gold / real estate positions, to hedge against Scenario 2.

For those who are interested, my full portfolio breakdown is available on Patron.

Closing Thoughts: Passive Investing may no longer have the same returns going forward

I wouldn’t say that this is the death of passive investing. What I will say – is that passive investing is probably less attractive going forward.

When you buy an index like the S&P500 now, you’re also buying into industrial, energy, retail, travel stocks. Not all of them are going to do so well in 2020.

Whereas when you active invest, you’re able to pick the winners, and avoid the losers. If you get that right, there’s a lot more money to be made.

I think 2020 will just be a stock pickers dream. A lot of old world industries are trading at fantastic valuations. If you can find those with a good balance sheet and resilient business model that will bounce back, there’s lots of money to be made.

But we’ll probably save that as a topic for another day. There’s just too much to cover. My advice is to not be too greedy. Optimize for survival, rather than gains. Pick companies that you think will not go bankrupt. Stay away from those with high leverage and weak cash flows, no matter how attractive they may look. The real secret to investing is to avoid losing money, rather than to focus on making big money. I know it seems counter-intuitive, but it’s correct. It’s why Warren Buffet has the rule: Rule No. 1, Never lose money. Rule No. 2, Never forget Rule No. 1.

Don’t forget this rule.

For now – My personal stock watch is available on Patron for those who are keen. This sets out the full list of stocks that I am monitoring on my watchlist.

What do you think? Is the bottom in stocks in? Share your comments below!

Support the site as a Patron and get market and stock watch updates.

Do like and follow our Facebook Page. We share great links and infographics there.

Join our Facebook Group to continue the discussion, we have a great community of investors who want to help each other become better investors. Everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Hi FH,

Very good insight analysis yet again. Thanks. Just wondering whether the general 6 months debt moratorium in the market now throw a spanner in your assessment of Scenario 1 since the farmer in your analogy is going to have a debt holiday for 6 months and indirectly kick the can down the road for everyone for another 6 months? Your thoughts?

That’s a really good question. I think the key here is that the moratorium is only Singapore. If it were a global moratorium, then everything would change.

So going back to the farmer analogy, maybe he tapped capital markets for USD bonds. These bonds will still be repayable, even though his loan to DBS may be frozen. That could still be problematic. And don’t forget that if the farmer is in Indonesia or Thailand etc, there is no such moratorium.

So it really goes back to how broad the policy response is, globally.

I agree that Main Street is in trouble. However, the big corporations are the ones who can access directly to central banks. Wouldn’t it be possible that economic conditions continue to deteriorate and the fed just need to print more money to pump up the big corporations? If enough money is printed, it doesn’t matter if Main Street is suffering and equities will keep going up? Of course there are political problems to that, but that’s for later.

Yes! Absolutely agree with this. This to me, plays out as a variation of Scenario 2.

I’m still leaning towards scenario 1 but I think scenario 2 is becoming increasing possible because of the unlimited money printing you mentioned. A huge portion of those in the US despite being unemployed, they are actually getting a higher pay now because the unemployment benefit exceeds their previous pay. There is also something similar in France. Those who are furloughed are still getting 90% or more of their pay (20% from the company and 70% from the govt) while working much less. And the France wage supplement scheme is available for 1 year! With all the programs introduced by so many countries that have the ability to just print money, these is much less demand shock this time round, unlike in previous crisis. For many workers in developed western nations, this period isn’t too bad for them all because they are getting paid for staying at home. There’s minimal loss of income, if any. The huge unemployment figures make things look bad but it’s not really that bad.

The unlimited money printing is also preventing companies from folding. 19 billion relief program was just rolled out for US farmers today. A program was already rolled out for airlines. There’s also a program for SMEs to get easy loans. There is low production/economic activity during this period. But, most companies are not going to fold if the govt continue to print more money and provide handouts.

I don’t disagree with you actually. Both Scenario 1 and 2 are possible in my books. I’m still leaning towards Scenario 1, but happy to be proven wrong in the coming months.

I agree that Main Street is going down. But big corporations will have better access to central banks. If the governments intend to keep them up, equities will still be going up regardless of fundamentals. What do you think are the signals we should be looking for if stagflation is on its way?

By the time it shows up in CPI it’s probably a bit too late, and one would have missed out the earlier part of the rallies. I would look at policy action, and price action in the markets. But yeah, it’s a tough call – all about shifting probabilities.

I am still wrapping my head around what are the future repercussion of unlimited quantitative easing, there must certainly be some sort of a cost to such methods?

Haha the cost is inflation. Happens all throughout history! A weaker currency and higher inflation, does amazing things for stocks.

“ With all the programs introduced by so many countries that have the ability to just print money, these is much less demand shock this time round, unlike in previous crisis. For many workers in developed western nations, this period isn’t too bad for them all because they are getting paid for staying at home. ”

I disagree with this. Despite them getting paid, the velocity of movement of money is drastically reduced. Back to the chicken farmer, once he folded for good, it’s very hard to come back.

We also need to consider butterfly effects. What if government keep printing money to pump it up, what will happens to countries? This is a disaster of our lifetimes, some regimes will collapses. It’s a total devastation to economies.

Yeah. I actually do expect big geopolitical changes to the global world order after this.

I am in the scenario 1 camp as well. Two unrelated questions/comments:

1) within the universe of investible assets for SG retail investors, which segments are pricing in more of scenario 1 Vs scenario 2? I would think the downside upside skew would be better if we can identify these.

2) I don’t have data to back this up, but seems to me like the market structure is fundamentally different from 08/09. Given the moves down and then up are so rapid, it could be that the time line we have seen in past cycles becomes severely compressed. Not sure why this is so, but could be the increased prevalence of algo-based funds. So my worry is I’m too slow and I miss out on deploying capital, with the timeline now measured in days/ weeks vs months in decades prior.

Some quick thoughts:

1) The million dollar question! The Singapore market is too small – it’s basically 3 banks and a bunch of REITs + Temasek Cos. But if you look at the US companies, I think a lot of commodities players, materials, oil, cyclicals – they’re all still pricing in a Scenario 1. Even Treasuries are pricing in Scenario 1.

2) Yes. I agree with this. The clock speed of the world has increased dramatically.

“ I actually do expect big geopolitical changes to the global world order after this.”

Given how things evolve, it’s quite likely that regionalization will be the new globalization. Developing countries with underdeveloped healthcare systems aren’t going to get out of this easily. The developed countries will start to ring fence themselves. This break traditional supply chains and create new ones. Driving up inflation. Asia should be driving the next recovery since Asia countries have most fiscal tools at their disposal. Exciting times, we will probably see many enormous opportunities presenting themselves in the near future.

“ I would look at policy action, and price action in the markets. But yeah, it’s a tough call – all about shifting probabilities.”

I have recently come across your website and after reading through some of your articles, I am impressed by your sharpness. A few feedbacks:

1) I think you have provided very high quality qualitative analysis on world situation. It will be great if you can complement it with quantitative analysis. I for one, fail to fully appreciate the impact of 6 trillions stimulus on a 20 trillions economy or a 50 trillions worth of global usd trade. This involves the efficiency of the transmission of money, the velocity of money circulating in the economy and if the package is wide/deep enough. Looking at government policies, we probably need to go into the numbers to determine its impact.

2) I think in terms of asset allocation, we should probably allocate some high beta assets in times like this. In my view, this is important because 1) it helps to capture some values from the volatility 2) picking up nickels in front of a steam roller is dangerous.

3) we are living in exciting times, in my view, we should look beyond singapore for bigger opportunities out there, in view of the impending geopolitical shifts. 🙂

That’s a really interesting comment, thanks for sharing. My thoughts below:

1) Agreed on deglobalization. The era of globalisation is probably over now. What I’m trying to understand though, is how the US v China dynamic will play out over the next 10 to 20 years, and how the world will gather around them (how will the alliances be drawn), and how this interacts with the USD’s status as reserve currency (and how the US utilises the USD’s power during COVID19). If you have any thoughts on that, would absolutely welcome them.

2) Fair enough. I’ll see if I can include them, without any rubbish in rubbish out syndrome.

3) Interesting comment on high beta assets. Which classes are you thinking of in particular?

4) Absolutely agreed on looking beyond Singapore. In fact the current article is not targetted at Singapore assets, it’s written more assuming a Singapore retail investor with access to global investible assets. Singapore is far too small a market.

Thanks FH! I have couple of operational questions.

1) how do you get bond exposure in your portfolio? The TLT ETF in order to get capital gains from US treasuries?

2) for sg investors, we face an issue with buying US stocks where USD tends to be strong when US stocks are weak. How do you time your SGD conversion into USD?

3) Do you favor the use of put and call options to hedge risk from the market moving either way? So for eg. If you believe scenario 2 plays out and are overweight stocks, buy put options on the s n p 500 in the event you are wrong.

Hi MooMoo – thoughts below:

1) Really depends on what you want exposure to. TLT used to be great, but given that rates are now zero bound, I think TLT will have very limited capital gains going forward. TIPS could be another option too. SSBs, SGS, corp bonds, Astrea series etc, are all options. There’s no perfect one here for Singapore investors, I just cobble something together for my own portfolio.

2) I’m pretty bad at timing – and timing something as liquid as the USD FX market to me is tough, so I just don’t spend that much time on this.

3) I don’t use options personally, but yes – absolutely agreed that it could be another way to play this. Again, there are many ways to make money in this market, just stick with the one that works for you. 🙂

I have been focusing on researching how recovery will look like more than US vs China dynamics. I do agree that this dynamics has significant impacts on how our future world looks like, consequently our investment orientation.

20 years is probably too far out. I think that the US will be significantly weakened after this crisis. As of now, they have already flooded the market with 6 trillions, this is 30% of US GDP comparing to 10% of GDP in 2008. I suspect we are not any where the end of it. Maybe by the end of it, it will be 50%? What’s the impact when the economy eventually recovers? Cash is going to be trash. Rich poor divide is going to widen much faster than the previous decade. Nationalism will be on the rise. The US probably will face more domestic problems and accelerate its current process of engaging the world. Is it possible for the US to export their problems abroad? It’s possible. But I think they are going to pay a high price doing that in Asia. China is probably the best placed nation in the world right now. If we look at how China positions itself, they are gearing for Asia dominance both economically and militarily. I think Asia, especially East Asia will belong to China in the next 10 years. This is significant as I think Asia will lead the next recovery. I am also expecting that there will be defragmentation on the world reserve currency. Already, we are seeing China trying to reprice crude oil in RMB. We should not discount that dollar will no longer to the King comes next crisis (which I suspect will come from Asia). Short term, I think we should place our investment in Asia. I expect hot money to be flowing in.

“ Interesting comment on high beta assets. Which classes are you thinking of in particular?”

I invest in the most volatile class of assets which I think not suitable for everyone. ?

My point on high beta assets is that we probably need to consider beta in our asset allocation, even in sub-class like within equities. I usually trade and do not like holding for a long period of time. We can also argue beta varies over an equity lifespan. REIT that attracts investors because of its price stability, suddenly becomes very volatile recently. Some of the equities I am looking at are aviation companies. You may frown upon my choice because of the inherent business structure especially of airlines. I prefer to look at it another way: industries that are whacked the hardest can potentially give you the best possible returns in the short term. Risk management is key.

Moving forward, I think some regimes are going to collapse. Increasingly, common people who don’t invest in assets are going to suffer and lose faith in their systems. We call these people libertarians. I expect this group of people to increase. Digital finance will be an area of explosive growth. I think it’s something worth looking into.

Thank you. Very interesting thoughts, and appreciate the sincere sharing. Lots of food for thought for me as well. 🙂

I agree that USD will face challenges in the coming years, but for now, I just don’t see any alternative. RMB may get there eventually, but 5 or 10 years out, it would be tough. So yes – I’m actually inclined to agree with you on fragmentation. The world may gradually splinter into those who use the USD, and everyone else.

Correction: the US is going to accelerate its current process of de-engaging the world

An after thought: war is probably a good way to export the problem. Though that probability is low for now.

Haha, agree that war is a convenient solution for many of the global players. But like you, I too think of this as a low probability event.

We are heading into be a deep depression that will make the last depression look like a recession. Firstly there will be a second and third wave of the pandemic as Politicians worry about the political effects of the shutdown of the economy and scale down the lockdown measures too early. With a second and third waves of the virus, another prolong period(s) of lockdown will be necessary to bring the crisis under control. And we will have governments announcing emergency fiscal measures worth at least 10 percent of GDP again and put their countries under fiscal stress. Credit rating agency will downgrade these countries and there will be mass selling of sovereign bonds. Some countries like Italy and Spain will have trouble raising new debt to repay old debt. Sovereign are Ponzi scheme if they aren’t already. A massive sovereign debt crisis is looming. And since banks hold a quarter of sovereign debt in Europe, most will become insolvent and no one can bail them out because Germany won’t come to the rescue of its profligate club Med neighbours. Banks are gonna failings we will have a banking crisis in TOP of a sovereign debt crisis. If Greece can cause such a crisis a decade ago, imagine what an Italian and Spanish sovereign debt crisis will do. All these money printing/quantitative easing will also make people lose faith in currencies as it is debased and governments like the fed can print ad much as they want. Soon we will have hyperinflation like in Germany during the 1920s. Money will also flow out of emerging markets because they can’t print money to finance their emergency measures as they are not the world reserve currencies and their economies will crash because they can’t borrow in international markets because their currencies have just crashed.. Investors are rushing for the exits from emerging markets. So what we have here is a pandemic, an economic depression, a Global financial crisis, an Asian financial crisis, a Greek sovereign debt default all rolled into one. And for what you know, the EU common currency may collapse as fiscally responsible countries like Germany will refuse to bail out the profligates like Italy and Spain. And there is a possibility of world war three as western powers fail to contain the pandemic and blame China for their predicament. China is the scrap goat. And some counties will sue China for compensation to repair their fiscal damage. Already attacks on Chinese in western democracies has started with people getting injured. The nationalist CCP will not lay down and they will defend their national pride. They will first started a trade war and then sell down their holdings of euro and dollar sovereign debt and start a sovereign debt crisis. Then Europe and America will retaliate by starting a war with China. And that will lead to World War three. Good luck everybody.

That’s bleak 🙁

“for sg investors, we face an issue with buying US stocks where USD tends to be strong when US stocks are weak. How do you time your SGD conversion into USD?”

You can consider shorting USD to hedge your position. I think that current usd rate is not going to maintain in the long run. And you can decide on a suitable time to release your shorts in the future.

Sure. Please let me know if you have any thoughts on these in the future. Glad to learn from you.

“RMB may get there eventually, but 5 or 10 years out, it would be tough.”

I agree. I don’t think its going to happen in 5-10 years + there is inherent distrust on the Chinese among nations that’s not going to go away in 5-10 years. Just making the point that fragmentation is going to happen moving forward. I guess we don’t disagree with each other. 🙂

On the European anaysis I agree with you, as an italian/spanish who escaped to singapore years ago…?

agree also with FH that this scenario is too bleak, the US/China war possibility is very low, due to economic interdependece.

A question for FH: I am recently wrapping my head around the Silver, as it has both coinage and industrial values…i believe that its current price already reflect partially scenario 1, specially from the gold/silver ratio at all time highs. Any views on silver?

Unfortunately I don’t follow silver, so not able to comment. I do agree though, that the current gold/silver ratio is interesting, but I haven’t done any in depth research as to why that could be the case. 🙂

I think people can be divided into two groups, old school believing in scenario 1 and new school believing in scenario 2. If the numbers in both school is 50 50 then selling will be well absorbed. When the old school noticed market is stable and up trending they will buy back and the market gets more upthrust. What we get is stock market decouples from it’s fundamental in short term. The global financial keepers are buying time for the real economy to get back on its feet and preventing financial market meltdown. According to the global growth projection all countries will get back to positive growth in year 2021. The question is can the financial stability keepers trick the market until the world get back to positive growth?

Yes I agree with this. Only time will tell. 🙂

And I thought I had dark thoughts ?

I am just thinking for Scenario 2 – what will be the side effects or unintended consequences from arising from the unlimited money? Probably inflation risks…?

Then assuming the money does get trickled down to the farmer in some other ways (such as a more effective way like maybe the government doing a direct financing…?)…

Then:

Q: What are the chances of these smaller SMEs surviving? And if they do, then I assume economy will recover. But what if not?

Q: What are the repercussions if they fail despite with the financing help – government ending with huge sovereign debt? Increased taxes? Increased austerity measures? Then the economy will be bleak again, somewhat like Greece?

A poster mentioned something about Italy and Spain. I am just thinking if it will be extended to any other countries say in SEA, and not only limited to Europe.

Yeah those are the right questions to be asking. And those are the questions no one has answers to right now.

On side effects for Scenario 2 – most likely consequence is inflation and rising inequality. 🙂

For the rest, only time will tell.

All the stimulus and handouts sound really good for large corporations but how about SMEs? Would small business owners be inclined to take up additional loans to pay off racked up debt or would they just declare bankrupt and start over when all is better? Also the stigma of bankruptcy in US isn’t as much as those in Asia. Is my idea a bit far-fetched?

Not far fetched at all. Unfortunately though – I genuinely do not know the answer to this. But these are the right questions to be asking.

Seems like everyone is distracted by Covid19. We are currently in an oil crisis – levels are lower than in 2015.

Hi FH, can you please share ways to invest in gold at lowest cost possible? Thank you.

You can look at GLD if you’re ok with paper gold. For physical gold – look at gold accounts from banks or just buying a bar from a shop like Bullionstar.

?