Well… what a week!

For the first time in 2 years, it’s starting to feel like March 2020 again.

That indiscriminate selling across the board, people dumping anything they can get their hands on.

Yet as investors, times like this are what we live for.

These are the times where generational wealth is built.

That said – my personal view is that this market crash is very different from March 2020.

And calls for a very different playbook.

Lots that I want to share today, so lets get started.

The Carnage in Financial Markets

Stocks

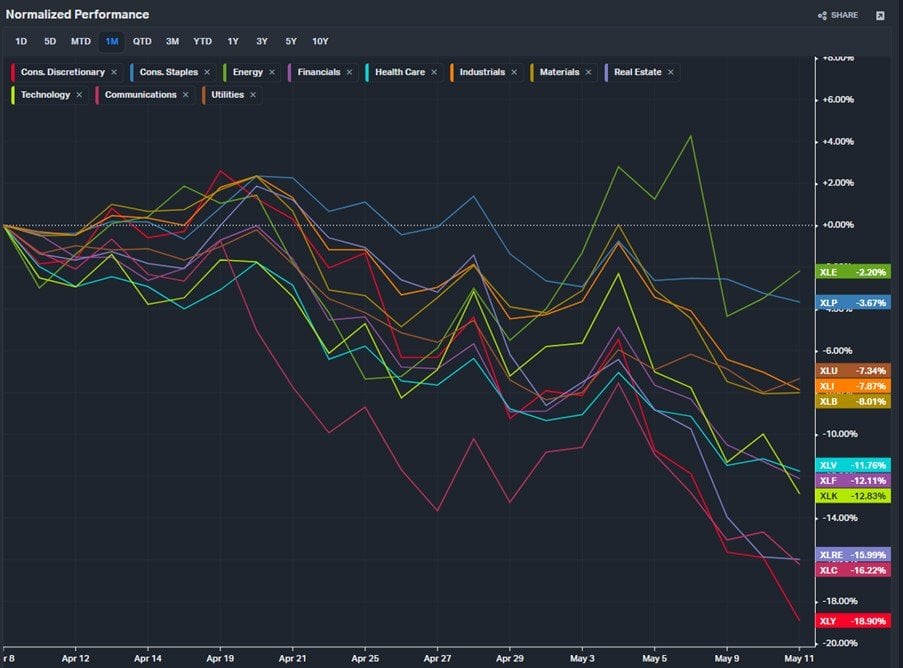

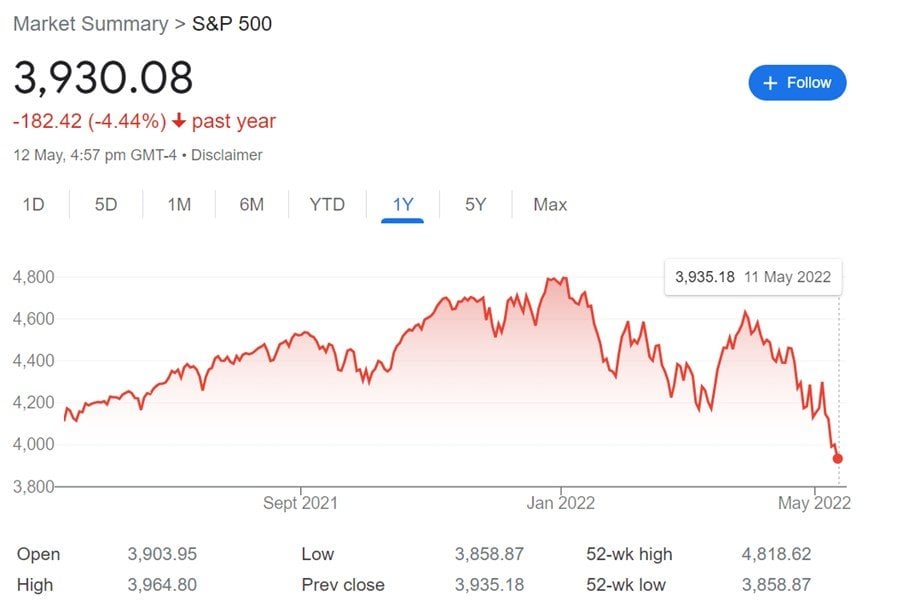

Over the past month, the S&P500 has dropped 12%, and the tech heavy NASDAQ is down 16%:

No sector has been spared.

Consumer discretionary has been hit the hardest, while energy and staples have fared the best (but still down).

Looks like the market is pricing in a stagflationary event (recession with inflation), which is not a good sign.

Crypto

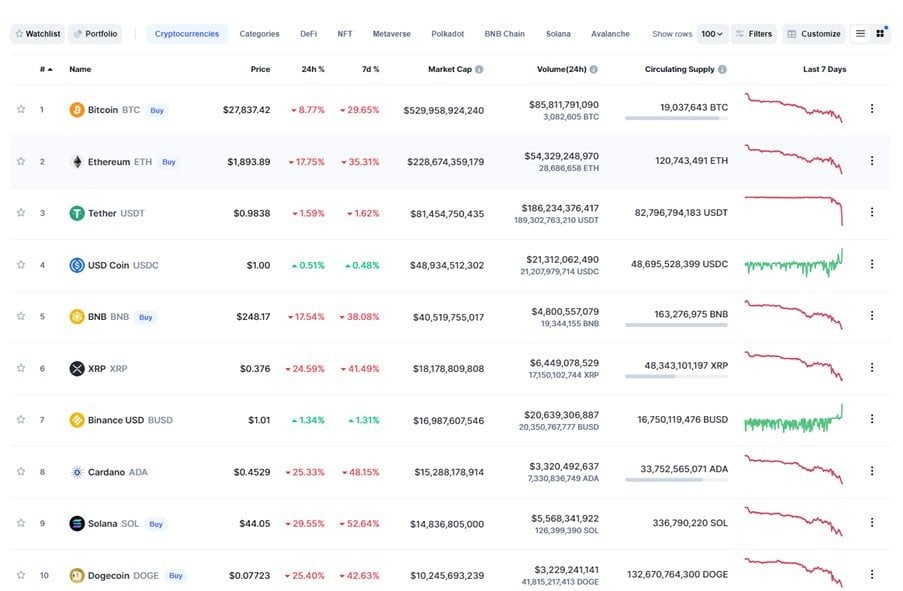

But the story of the week has to be crypto.

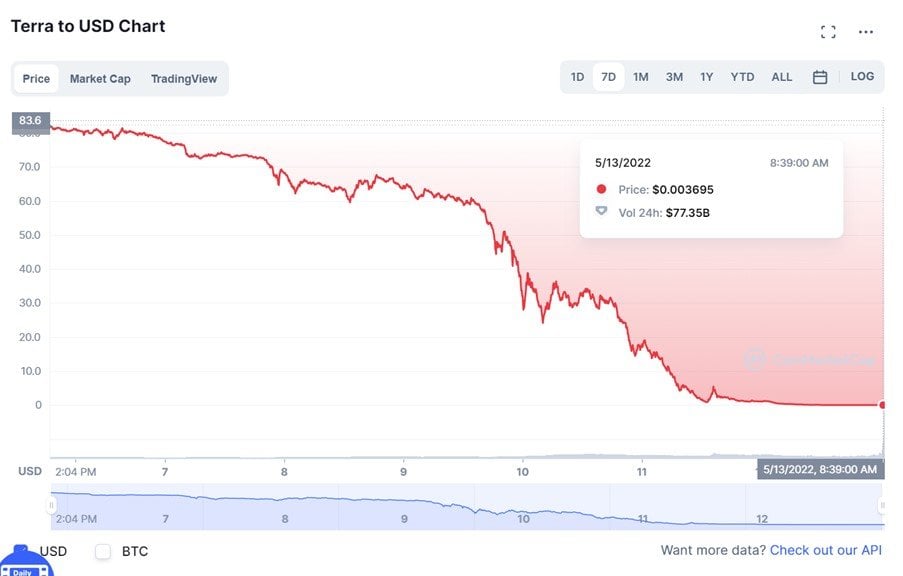

Luna, the fourth largest cryptocurrency just 1 month ago, has been absolutely obliterated.

Down from $100 to $0.003 on last count.

A 99% drop, for the fourth largest cryptocurrency.

And this has taken down the entire crypto sector, with BTC at $27,000 and Ethereum at $1800.

How I will invest $1 million in 2022’s Market Crash (as a Singapore Investor)

In times like this, cooler heads prevail.

2 big questions in my mind:

- When to buy?

- What to buy?

When to Buy REITs/Stocks in 2022?

I’ve been saying this since Jan.

To the point where I’m almost sick of repeating it.

But it’s important:

I do nothing until I see the Feds changing their mind.

And when the Feds change their mind, I buy the dip, in size.

Until the Feds change their mind, I see any big rallies as countertrend moves (in a broader decline).

And my clues for when the Feds change their mind are:

- Treasury (or credit) markets break

- Inflation goes away

- S&P500 melts down 20-30%

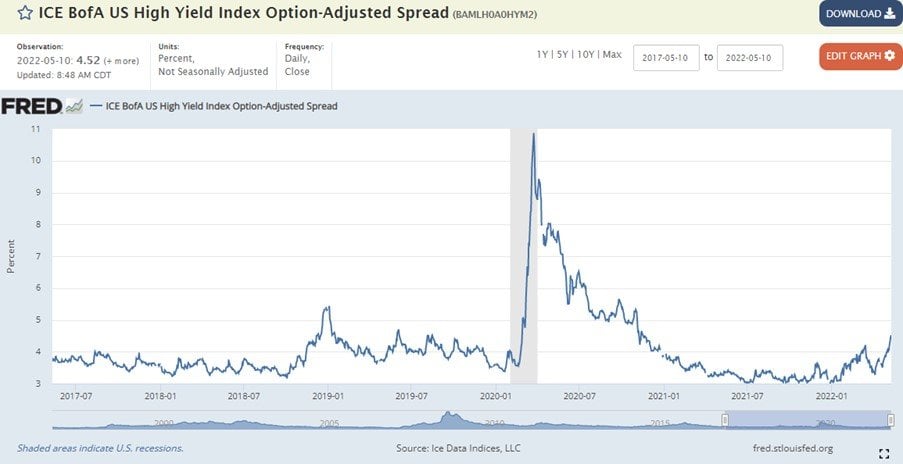

Treasury (or credit) markets break

Credit markets are actually holding up surprisingly well.

There are early signs of credit stress, but nowhere near the levels required for the Feds to turn dovish.

Don’t hold your breath just yet.

Inflation goes away

The latest US inflation report was… not good.

I’ll save you the details, but the key is that inflation is becoming more entrenched, and more broad based.

Inflation is shifting from goods into services, and core inflation is accelerating.

This is not the kind of report you want to see if you’re betting on the Feds turning dovish.

Feds will need to persist with rate hikes to prevent inflation from taking hold.

S&P500 melts down 20-30%

Interestingly it is this third factor that is the closest to being fulfilled.

The S&P500 at 3930 is now down 18% from it’s all time highs.

Will the Feds change their mind just because the S&P500 is down 30%?

Some of you have questioned this.

You think that the Feds only care about the real economy now.

As long as inflation stays high, and credit markets are functioning, the Feds will ignore equity markets pain.

My view is that all these factors are interconnected.

Unlike Singaporeans where most of our wealth is in real estate/CPF, Americans have a big chunk of their wealth in stocks.

The US stock market has an important signalling effect for the US consumer and business.

If the US stock market is down, it will affect consumer sentiment and business spending. Stock based compensation will collapse.

It’s a vicious cycle that feeds on itself, which will eventually hit inflation and credit.

We saw this in 2000 when the bursting of the Dot Com bubble triggered a recession.

Stock markets crash, and very soon earnings start to follow, then layoffs.

At what level of pain will the Feds step in?

Where I disagree with the dip buyers, is the level of pain required before Jerome Powell steps in.

I don’t think we’re there yet.

You must understand, collapsing equity prices, crushing speculative SPAC and crypto bubbles – this is exactly what the Fed wants.

This is working as intended.

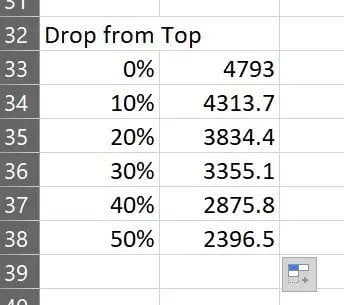

I would be looking for a close to 30% drop in the S&P500 before this is over. 3500 on the S&P500 would be a key level to watch for me.

This is different from March 2020

I think the key difference with March 2020, is that back in 2020 we had the Feds on our side.

Markets plunged, the Feds came in with unlimited liquidity, and you just bought the dip.

This time around, because of inflation, Feds cannot come in so quick.

And without the Feds coming in, how long do equity markets take to bottom?

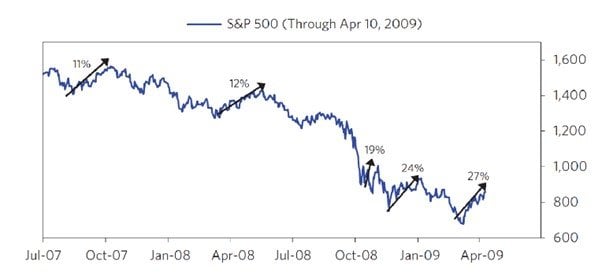

What happened in 2008?

2008 offers some clues, and it’s not pretty.

In 2008, the S&P500 declined almost 50% over 18 months, with multiple bear market rallies of more than 20% on the way down:

Of course I’m not saying 2008 will repeat.

I’m saying that if the Feds don’t come in and markets are left to play out by themselves, the bottoming out is a very vicious process.

Basically… don’t buy the dip yet…

Long story short – I still don’t think we are at the bottom.

Short term bottom maybe given the oversold sentiment, but the bottom for this credit cycle?

I don’t think we’re there yet.

I’m happy to start nibbling here and there, but I’m still saving the heavy firepower for later in the year, closer to the Fed pivot.

When it is time to buy though, I will be sharing on Financial Horse so do stay tuned.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Should I Dollar Cost Average?

A lot of you have been asking me whether dollar cost averaging is the right move.

And frankly that’s a personal question only you can answer.

If you have a lot of cash on the sidelines, and you don’t want to time the market, then yeah DCA is a good choice.

For me personally though, I want to maximise my returns, and I’m happy to time the markets.

But frankly I also spend all my waking hours tracking financial markets.

It works for me, but it might not work for you.

What REITs/Stocks will I buy in 2022? As a Singapore Investor…

With timing out of the way, the next question is what to buy.

Buy Opportunistically based on prices

The problem with coming up with a fixed list of stocks to buy, is that you are closing your mind off to other possibilities.

It’s like going into a pasar malam with a shopping list.

I mean sure it works, but then you miss the discarded gem worth $100 going for $1.

It’s not possible to anticipate ahead of time what sells off and what doesn’t.

Of course, you need to do your homework and prepare as best as you can.

But when the time comes, be flexible.

How I will invest $1 million in 2022’s Market Crash

So what I would do is to compile a broad list of REITs / stocks that I am keen to buy.

And as 2022 plays out, I buy what sells-off the most relative to fair value

For now, my broad allocation would be:

- $500,000 REITs

- $500,000 Stocks

FYI the $1 million is a hypothetical number. Feel free to adjust accordingly based on the amounts of funds set aside.

REITs (6% yield is my target)

With REITs my target price is about 6% yields on the blue chips like Ascendas and Mapletree Industrial.

This indicates a price about 10% below current prices.

Frankly I don’t know if we’ll get there, so I’m happy to nibble along the way as I see bargains emerge (just in case I’m wrong).

That said, we haven’t had that kind of liquidity event like March 2020 yet where investors panic sell everything and margin calls are pouring in.

So… there is still time for this to play out.

In an case, the REITs on my watchlist are:

- Industrial / Data Center REITs – $300,000

- Ascendas REIT

- Mapletree Logistics Trust

- Mapletree Industrial Trust

- Digital Core REIT

- Daiwa House REIT

- Keppel DC REIT

- Retail / Commercial REITs – $200,000

- Mapletree Commercial Trust

- CapitaLand Integrated Commercial Trust

- Lendlease Global REIT

- Keppel REIT

- CapitaLand China Trust

- Starhill Global Trust

For full stock watchlist and my target prices, you can check out Patreon.

Stocks

Stocks are a little more tricky.

The universe of stocks is so much broader than S-REITs, and it is very hard to anticipate in advance how the price for each sector will play out.

For now, my preliminary views are:

- S&P500 – $100,000

- Commodities – $100,000

- Gold Miners – GDX

- Oil (Exxon, ConocoPhillips)

- Discretionary Stock Picks – $300,000

- US Growth

- Cloudflare

- Crowdstrike

- Semiconductors

- AMD

- Intel

- Micron

- Value

- Disney

- DBS/UOB/OCBC

- JP Morgan

- US Growth

Some key questions that I wanted to address:

Why $300,000 unallocated?

In the previous version of this article, the $500,000 was broadly split among value stocks.

Then a Patron pointed out that the allocation is too value heavy.

And the more I thought about it, the more I realised he was absolutely right.

There is already a growth to value rotation playing out right now. Investors are dumping growth stocks, and buying value stocks.

This means that as 2022 goes on, if I do absolutely nothing, my allocation to value will go up, and my allocation to growth will go down, simply due to market movements.

If I then add another 1 million to value, I would be very heavily overweight value.

Will Value outperform Growth this decade?

Now this really is the million dollar question.

I’m hearing from institutional fund managers that all the “smart” money is moving from growth into value.

And when institutional money moves like that, it usually plays out over years, not months.

The added complexity, is that even though the S&P500 may bottom out when the Feds turn dovish, growth stocks may not necessarily bottom out.

You see the S&P500 is made up of 500 stocks. If the increase in the value portion of the S&P500 outperforms the decrease in the growth portion, then the index as a whole may bottom, but individual growth names may not bottom out just yet.

The macro backs it up too, because if this decade is indeed a higher rates / inflation volatility regime, then value should outperform growth.

Whatever the case, I dont think there is a need to decide now.

Let things play out, and reassess in Q3/Q4 this year.

Watch if inflation is sticky, if interest rates will come down. Then make the value vs growth decision.

Hence I left this $300,000 open for now, but I included some names that I am keen on.

If you are keen you can view my updated stock watchlist and price targets on Patron.

Why buy Commodities – Aren’t commodities at a high?

My view is that by the end of this short term cycle, we’ll see commodities prices come down as well as global economic growth slows and inflation comes down.

But in the mid term, all that underinvestment into capex and emphasis on ESG will come back and haunt us.

Setting us up for further shortages as this decade plays out.

In other words – I would buy the dip in commodities. If we get one.

Why Gold?

Gold is a bit of a hunch for me.

You can read my full views on gold here.

But the long and short is that in March 2022 when the US confiscated Russia’s USD foreign reserves, the whole world sat up and took notice.

Including a whole bunch of countries that may not necessarily be fully aligned with the US foreign policy.

The previously unthinkable red line in the sand was crossed, and this is not something you put back in the bottle.

In a decade of deglobalisation and lack of trust between countries, what is the true neutral asset?

Gold, commodities, and maybe Bitcoin.

But it doesn’t need to be one or the other.

All 3 can potentially benefit.

In any case, rising real rates are not going to be good for gold in the short term, so I can patient with this one.

If I am right this will be a decade long play.

What about China stocks?

What I will say, is that China is on a completely different credit cycle from the west.

The analysis above applies for everything outside of China, but very much less so for China.

For China, it all goes back to the CCP’s policy.

They’ve talked a lot about easing and stimulating the economy, but so far we’ve only had a trickle of liquidity.

Actions talk, so the time to buy for China is when the real fiscal / monetary stimulus starts.

Some may argue that the stimulus is never coming, because the CCP is afraid of inflation.

If so, then the decline will be a painful one and it is not a buying opportunity.

I’m a bit more sanguine, and I think we’ll start to see some easing as we head closer to the Party Congress. Whatever the case, will share views on Financial Horse as and when I see the signals play out.

These are momentous times in markets… but it is just money

After the recent collapse in Luna prices, there are a lot of talk about people wanting to take their lives.

Now this goes without saying, but money, is just money.

No amount of money is worth taking your life over.

Live to fight another day, and you can always build back stronger.

If you feel too stressed, just log off, and take a walk.

Come back a few days later after you’ve cleared your head.

Closing Thoughts: Will Fundamental Stock Picking work? Macro is King?

A lot of you have asked if fundamental stock picking works in times like this.

Personal view – Yes, a time will come for stock picking.

But for now, macro is king.

When the Feds are raising 50 bps each meeting and QT is starting next month, you really just want to stand aside and let things play out.

Play defensive, preserve capital.

When the time comes, then stock pick.

If you are keen, you can see my full portfolio breakdown and how I am positioned, as well as my REIT/stock watchlist with target prices on Patreon.

As always, this article is written on 14 May 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patreon.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to MooMoo and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with Tiger Brokers and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Dear FH,

Great article. Thanks also for doing the earlier article I suggested on how you would allocate given the chance to buy gradually at cost effective prices. Very useful.

A few comments on my end

1. I do not believe the Fed will step in with 30% S&P decline if inflation stays at 8% and credit markets do not break. While participation in US equity markets is much higher as you say, it is still skewed more towards the upper middle classes and wealthy. If the less wealthy is finding it difficult to pay for food because of inflation, the Fed will not risk riots and protests to support the stock market. Furthermore, if you look at long term trend lines, even with current drop, both S&P and Nasdaq are still considerably above these. I think this will likely be closer to the 2008 in your chart. In fact, the closer corollary is 2001 dotcom bust. I lived through that and am seeing many parallels to what is happening with Nasdaq. However, inflation may come down because of the stronger USD and in this case, the Fed could slow earlier.

2. I wonder if bonds should also have a role in your portfolio. If the bond bust continues as it will if the Fed keeps raising, at some time, it becomes a big reset of the decades long bond bull market and bonds become attractive to hold again. TLT is already at 5 yr lows. If it drops further into the 80s, it will provide 5+ yield and regain its role as a ballast against stock instability which is its historical role. The 60-40 portfolio will be resurrected.

3. Gold – this is very interesting. China will certainly be looking for ways to move away from Western fiat currency reserves and Gold and Commodities seem to be the only alternatives. They do not believe in Crypto. Already, Russia is looking at a gold and commodity backed Rouble and perhaps we will see a gold and commodity backed Yuan eventually, so back to the gold standard. This will obviously not happen quickly but even if it happens over a decade or more, the role of gold could change and the potential impact tremendous.

4. Data center Reits – I am starting to wonder if these are actually risky in an inflationary environment. They have very long term leases and in some cases built in rental escalations of only 2-3% as these were signed in a low inflation environment so rentals could lag inflation for a long time. Conversely, hospitality Reits work well in inflation as room rates vary every day.

This is a great comment CMC. I add my views below:

1. Yes I understand your point on the 30% drop in S&P500. What I might add is that the speed of decline matters too. Let’s say the S&P500 drops another 15% the next 5 days, I think that’s a big enough move that credit may start to break and we see signs of systemic stress. If it drops 15% over the next 12 months, then maybe the market can absorb it no problem. But in any case there is no need to make this call ahead of time, one can watch the impact on credit/inflation as the stock market decline plays out.

2. Okay on TLT – my view is that it is ok as a tactical timing tool, but not as a strategic long term holding. If one is buying it to trade the eventual Fed rate cuts / Recession, that probably fine. But as a 5 – 10 year holding, I would really think twice. It is increasingly looking like there will be significant rates/inflation volatility this decade, which means bonds may underperform after adjusting for inflation. I think the 60/40 or risk parity is dead. Replace the Treasuries with cash to survive the volatility, and the rest goes into risk assets.

3. Yeah whatever way you spin it, for a country like China, there are only 3 big asset classes to hold reserves in that are politically neutral – (1) Gold, (2) Commodities, (3) Bitcoin (or other digital asset). (2) has storage issues, (3) we all know the problems, and (1) there is insufficient supply if China were to buy in size. Which leads to a conclusion that China will still have to hold USD assets, but over time may start to diversify into a mix of these 3. So I think there is an argument to be made that all 3 can benefit.

4. Frankly I never understood the appeal of DC REITs. It’s a building, with a bunch of data centres. Where is the moat? The real value comes from the guy making the semiconductors, or the guy who owns the data. Not the guy who owns the building that stores the computers. That said, DC REITs are selling off very strongly, and if they cross the 5% yield point they’re probably a decent add.

Thanks for the reply, FH.

1. Agree with you on speed. The quandary will come if credit markets start to creak but inflation is still sky high. There will be no way out of the mess they created with unlimited money printing.

2. Interesting you think that risk-cash is the new portfolio. In this case, what proportion will you keep in cash vs equity?

Hi CMC,

Interesting points.

1. Credit breaking but inflation not going down is a nightmare scenario. One wonders how likely it is though. Credit breaking is a 2008 level kind of event, consumer demand will crash. If inflation doesnt come down it indicates an equally big supply disruption, in which case we might be looking at a 1970s kind of depression. In which case the only real hedges are stagflation hedges – hard assets like gold/oil. I think it’s a low probability outcome for now.

2. I think this has to be a personal decision. Whatever % that helps one to sleep at night. For some it might be as low as 5%, for others it could go up to 40%. Will need to depend on age + risk appetite + income status.

Hi CMC,

Which article were you referring to?

“Thanks also for doing the earlier article I suggested on how you would allocate given the chance to buy gradually at cost effective prices. Very useful.”

Would like to read it if I missed it. Thanks!

Before the China tech crackdown, you were bullish China. In past “Where I Will Invest” articles, you had advocated 2801 ETF

Alibaba, Tencent and even Luckin. Presumably they are significantly under water now.

You may wish to write article on how you deal with your China holdings? Cut and take losses – and how? Hold – and why?

Well as investors, one must be flexible. When the facts change, don’t be afraid to change your mind.

That said – my apologies because while I have been doing China updates on Patron, I dont think they were released on the public site. Will find the time to do a post to round up latest views on China.

For now, my view is that with China one should watch for real policy moves, instead of just talk. So far there’s been lots of talk about dialling back the regulatory crackdowns and impending fiscal/monetary stimulus – but no action to back it up.

Cheers.

Hi FH,

Can you share the entry plan/criteria for US growth stocks if possible… e.g. how do you value loss-making growth companies…

Thanks,

KK

Oh… that is an entire stocks masterclass right there. Will see what I can do, but not sure if it can be condensed into 1 article. Valuing and picking growth stocks, and then timing the purchase requires quite a deep understanding of the business/valuation techniques/macro.

100k each…chop chop 60k/yr tax free income 🙂

1398.HK

3988.HK

DBS

UOB

OCBC

HKL

Wilmar

Sabana

HPHT

MIT/MLT

Nice – appreciate the sharing.

(June 2022) Seas of reds finally except FTSE, KOSPI & Shanghai Index. Major indices has been going in a downward trend since the US Fed announced its intention to curb its highest inflationary level in America not seen in 40 yrs. I researched 3 main causes contributed to it

1.) surging fuel prices (Brent & WTI) as a result of the recent pandemic imbalance

2.) increased international shipping & logistics costs due to ports shutdown, labour shortage, containers shortages from being left in the wrong places, shipping companies skipping major routes altogther

3.) Ukraine (Russia decimation) is a major producers of crops and livestock feeds Europe & Americas

The imbalance has caused a food security concern in many countries. Exporters are reluctant to export / Importers faces exogenous shocks

Prices of poultry and cattle will skyrocket.

In my opinion inflationary pressure is seen as a positive sign. Prices usually transmit across different price chains. E-commerce delivery time will escalate due to the surge in vehicle fuel prices, international shipping costs, labour reduction when delivery companies try to breakeven costs. Profit & Markets should be going up. b FH explains the red flags on major indices today. TQ

(June 2022) Seas of reds finally except FTSE, KOSPI & Shanghai Index. Major indices has in a downward trend since Oct 2021 when the US Fed announced its intention to curb its highest inflationary level in America not seen in 40 yrs. I researched the 3 main causes contributing to it

1.) surging fuel prices (Brent & WTI) as a result of the recent pandemic imbalance

2.) increased international shipping & logistics costs due to ports shutdown, labour shortage, containers shortages from being left in the wrong places, shipping companies skipping major routes altogther

3.) Ukraine (Russia decimation) is a major producers of crops and livestock feeds Europe & Americas

The imbalance has broke down the food supply chain and caused a food security concern in many countries. Exporters are reluctant to export / Importers faces exogenous shocks. Prices of poultry and cattle will skyrocket.

In my opinion inflationary pressure is seen as a positive sign. Prices usually transmit across economies. International Cargoes, E-commerce delivery time will be delayed to the surge in vehicle fuel prices, international shipping costs, labour reduction when delivery companies try to breakeven costs. Profit & Markets should be going up. Will FH explains the red flags on major indices today. TQ

(June 2022) Seas of reds finally except FTSE, KOSPI & Shanghai Index. Major indices has in a downward trend since Oct 2021 when the US Fed announced its intention to curb its highest inflationary level in America not seen in 40 yrs. I researched the 3 main causes contributing to it

1.) surging fuel prices (Brent & WTI) as a result of the recent pandemic imbalance

2.) increased international shipping & logistics costs due to ports shutdown, labour shortage, containers shortages from being left in the wrong places, shipping companies skipping major routes altogther

3.) Ukraine (Russia decimation) is a major producers of crops and livestock feeds Europe & Americas

The imbalance has broke down the food supply chain and caused a food security concern in many countries. Exporters are reluctant to export / Importers faces exogenous shocks. Prices of poultry and cattle will skyrocket.

In my opinion inflationary pressure is seen as a positive sign. Prices usually transmit across economies. International Cargoes, E-commerce delivery time is delayed to the surge in vehicle fuel prices, international shipping costs, labour reduction when delivery companies try to breakeven costs. Profit & Markets should be going up. Will FH explains the red flags on major indices today. TQ

Haha, thanks for sharing your views! Yes, you have identified the key factors driving the current inflationary pressures.

The million dollar question – will these go away, or are they here to stay?