What a month it’s been!

Since Jackson Hole in late Aug, the market has started to break.

This week, the US 10-year yield broke 4%.

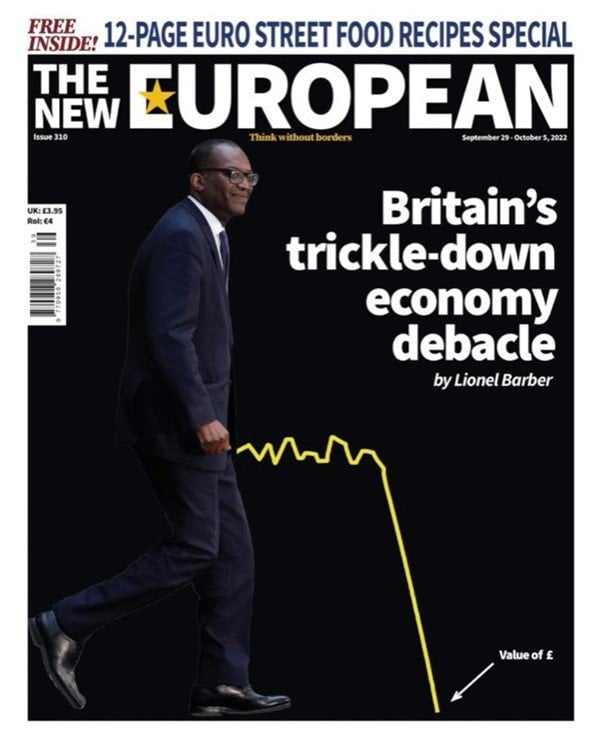

And don’t even get me started on the UK.

A very poor set of decisions by the new government led to chaos in the UK Gilt market.

That very nearly resulted in Lehman 2.0 in the UK, and forced the Bank of England to step in.

A lot of you have been asking for a macro post (which has now largely moved to Patreon), so here goes.

For ease of reading, I’m going to structure this as a series of Questions & Answers.

Has the Market Bottomed?

Short answer – No, I don’t think so.

The slightly longer answer, is that this is a very different market from March 2020.

March 2020 was unique, because the economy went from 100 to 0 due to COVID lockdowns, and then financial markets went from 0 to 100 due to supercharged Fed stimulus.

This time around, it plays out more like a classic bear market.

There are 4 stages of a bear market:

- Stage 1 – Market topping out, savvy investors start to sell

- Stage 2 – Market decline due to drop in valuation multiples. Damage is largely limited to financial markets.

- Stage 3 – Damage spreads to the real economy. Consumer cuts back on spending, corporate earnings drop, refinancing risk starts to play out.

- Stage 4 – Liquidity event and panic

Where are we now?

Rough ballpark, I think we are in the mid to later stages of Stage 2.

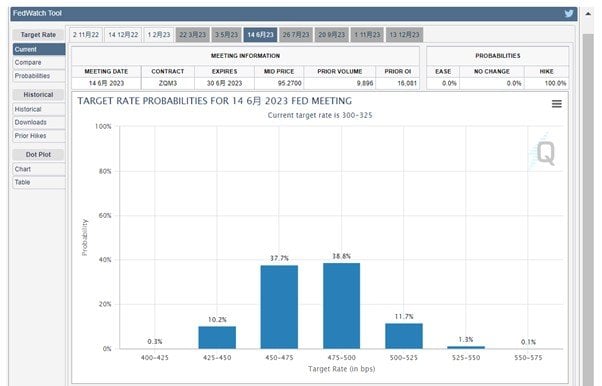

Previously I said that cycle peak for Fed Funds Rate may be close to 5% (with possible overshoot to 5.5%).

As of today – futures are now pricing in a terminal rate of 4.75% – 5.0% by June 2023:

There’s probably room to go slightly higher, especially if inflation is sticky.

But no denying that futures markets at least, are starting to price in the interest rate end game I’ve been talking about.

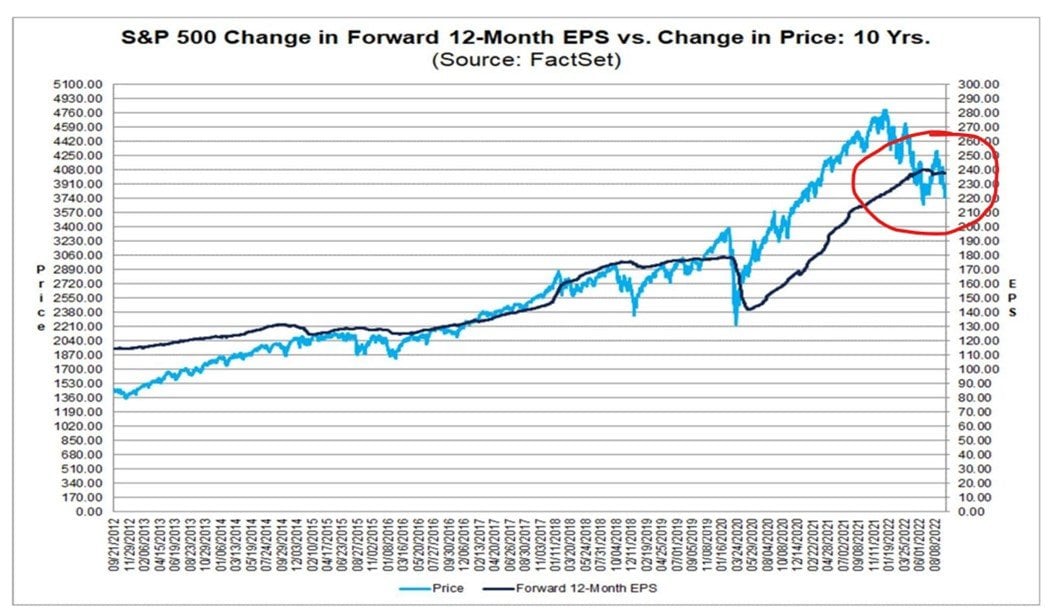

Market has not priced in earnings drop

But… look under the surface, and you’ll find that the market is currently pricing in almost no earnings drop.

In other words, the drop in the stock market to date, is entirely due to the rise in interest rates.

The market has not priced in any drop in corporate profits… yet.

The market is saying that the Feds will take us to 5.0% interest rates and stay there, and corporate profits are going to stay flat.

I don’t know about you, but I find that hard to believe.

I think at 5% interest rates, all sort of bad things are going to start happening in the economy.

In which case, this is not likely to be the bottom.

When will the Market bottom?

Short answer – I don’t know. Nobody does.

The slightly longer answer, is that before stocks can bottom, one of the following needs to happen:

- Feds start cutting interest rates (or at least pause rate hikes), OR

- Market prices in the drop in corporate profits

(2) has not happened yet. For it to happen, we need to see about a 15 – 20% drop in the market by my estimates.

3000 on the S&P500, just to hit fair value.

With possible overshoot due to liquidity panic.

It’s almost poetic justice right. If COVID stimulus caused excessive demand and inflation, shouldn’t the cure be to reset everyone to pre-COVID levels of wealth?

In any case, let’s not rest our hopes on (2) happening any time soon.

So let’s talk about (1).

When will the Feds start cutting interest rates (or at least pause rate hikes)?

A couple of months ago, I said that the market is wrong to price in a Fed Pivot so early.

A Fed pivot will come, but not as soon as the market is expecting.

A lot of people laughed at me back then, but now the market is starting to wake up to this new reality.

Now I hear people talking about King Dollar, and how US interest rates are going up and never coming down.

Source: Koyfin

And ironically, now that people are starting to say this, it means we are closer to the Fed pivot.

For the record, I think that Jerome Powell needs to talk tough on inflation, that is his job.

But if the higher interest rates result in (a) financial market contagion, or (b) a deep recession, he will eventually cut interest rates.

So FH.. when bottom?

So the question that literally every investor is asking now – How much pain does Jerome Powell need to see, before he cuts interest rates.

Really, that’s the only question you need to ask yourself for the next 12 – 18 months.

When does Powell cave?

Unfortunately, the answer is not so straight forward because it is path dependant.

To put it simply – how quickly Powell caves, and accordingly how quickly the market bottoms, will depend on how quickly the rising interest rates break the financial system / economy.

Just look at the Bank of England the past week.

In the month they were supposed to start Quantitative Tightening (selling Gilts, which are UK Government Bonds), they ended up starting Quantitative Easing (buying Gilts) instead.

Could you have predicted a month ago that it would be Liz Truss and Kwarteng breaking the Gilt market that led to the Bank of England stepping in?

Doubt so.

But whatever the case, it’s obvious the risks in the system are starting to build.

In 2008 terms, the past week was Bear Stearns.

What happens when the Feds fold and cut interest rates?

Once the pain of fighting inflation gets too much to bear, central banks are going to fold.

And they are going to accept a higher rate of inflation (than the 2% target), and a lower rate of economic growth.

In other words – the next phase is inflationary.

After the market crash and the Feds pivot, the next phase will be debasement of fiat currency.

The value of money itself will drop.

And the value of everything else denominated in money – think stocks, real estate, commodities, oil, food etc, will go up.

So in the next phase, you don’t want to be holding too much cash, because real interest rates (inflation adjusted) are going to be negative.

The 3% yield on your T-Bills may look good, but if inflation rages at 5% for years, you’re losing 2% a year.

How should a Singapore Investor position in times like that?

But let’s not get ahead of ourselves.

That’s the mid term, 2 – 3 year outlook.

Your immediate concern, is to get through the current bear market.

You need to survive unscathed (as much as you can), until the market bottom.

If you are feeling adventurous, you can short the market.

But remember that the biggest rallies usually come in a bear market, so if you’re short, you need to be very careful with risk management.

If you are feeling less adventurous, then you just want to be in cash mostly.

Hold USD/SGD cash, earn the high yield in the short term (T-Bills yield 3.32% now risk free), and deploy that all into the market as close to the bottom as you can.

I’ve been saying this since Jan 2022

For the record, everything I’m sharing in this article is in line with the framework I’ve been sharing on Patreon, week after week.

So if you find this article helpful for you, please do consider signing up for the Patreon subscription. Most of the regular macro updates have moved there.

At S$15 a month you get the premium weekly market updates like this one.

At $25 a month you get my full stock and REIT watchlist, and at $40 a month you get my full personal portfolio.

Don’t be penny wise pound foolish.

Think about how much you may have lost this year.

And how much you will lose in the next 12 months if you start buying too early.

How I will invest $1 million in 2023’s market crash?

I spent a lot of time trying to explain the framework above, because I think this is important to understand for the months ahead.

Buy too early and you get crushed by rising rates.

Buy too late and you get crushed by inflation.

The game is this – I stay in cash as long as I can, until as close to the bottom as I can. Then I buy in size, and ride the next phase of inflation up.

To watch for the bottom, I watch for either (a) market pricing in corporate earnings decline, or (b) the Feds being forced to turn dovish.

(a) frankly is not likely. Even if it happens, you need to price in possible overshoot due to a liquidity crisis.

(b) is much more likely.

And for (b), this will happen if we get (1) financial market contagion, or (2) a deep recession where the pain is too much to bear.

I won’t be able to call ahead of time what’s the exact event that triggers (1) or (2).

But it will be fairly obvious when it happens (like the past week for the Bank of England).

How I will invest $1 million in 2022 / 2023?

For the record, I think it’s too early to buy long term positions, for the reasons set out above.

But I know many of you want my latest thinking of how to allocate capital when the time comes.

So with that caveat that I will likely change this allocation as the next few months play out, this is what’s on my watchlist right now (for latest watchlist and target prices, do check out Patreon):

REITs ($500,000)

- Industrial / Data Center REITs – $300,000

- Ascendas REIT

- Mapletree Logistics Trust

- Mapletree Industrial Trust

- Digital Core REIT

- Daiwa House REIT

- Keppel DC REIT

- Retail / Commercial REITs – $200,000

- Mapletree Commercial Trust

- CapitaLand Integrated Commercial Trust

- Lendlease Global REIT

- Keppel REIT

- CapitaLand China Trust

- Starhill Global Trust

Commodities / Precious Metals ($300,000)

- Oil (Exxon, ConocoPhillips, Shell)

- Copper Miners – COPX

- Gold Miners – GDX

Stocks ($200,000)

- Too early to call in my view, the sell-off is still playing out.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

We also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Thought Process for allocating the $1 million

Reasoning from first principles – what do I want to own in a world of higher interest rates, and higher inflation?

I want to own (a) commodities, and (b) dividend stocks / value stocks.

Commodities

Commodities because they hold their value against a depreciating fiat currency.

Not to mention that structural demand-supply mismatches mean commodities can potentially go much higher.

This is a world after a decade of underinvestment into commodities, with higher geopolitical tensions and massive infrastructure investments moving forward (due to East-West decoupling and green energy transition).

Dividend / Value Stocks

Dividend stocks, because the right ones have pricing power, to pass on higher costs to consumers.

When a new factory costs $1 billion and 5 years to build, how much is your existing factory worth?

In a world where the price of goods go up 10% a year, every dividend company has growth built into it.

Remember – revenue growth due to inflation, and revenue growth due to good management, looks the same on a P&L.

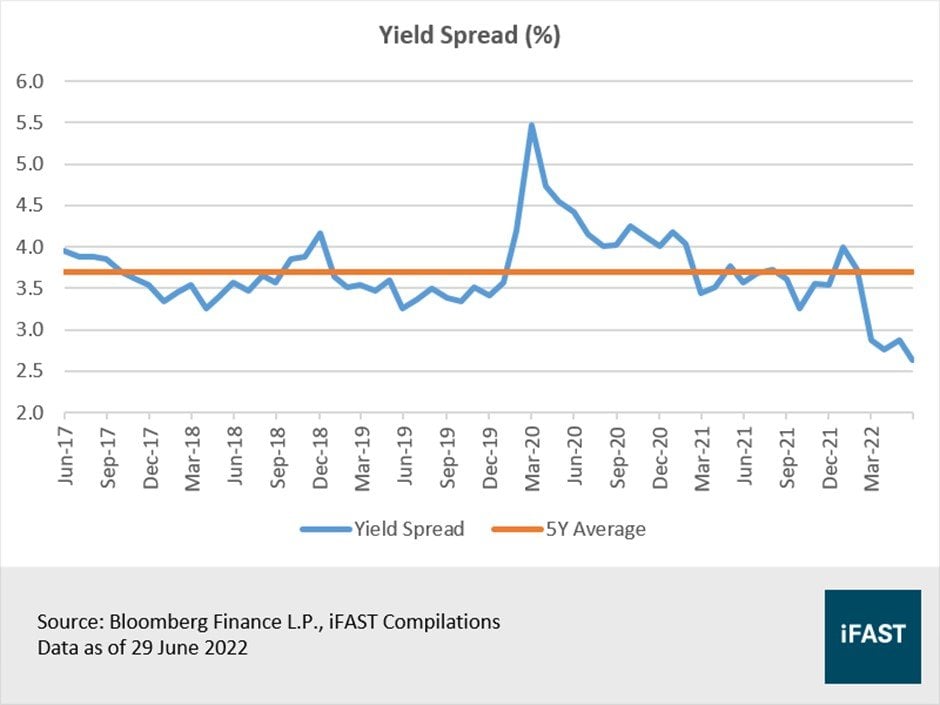

Will REITs underperform this decade?

If you look purely at yield spreads, REITs are the most overvalued they’ve been in 5 years.

Put another way – even after the big declines in REITs, they have (on average) yet to fully price in the rapid rise in interest rates.

Let’s reason from first principles.

REITs are a leveraged play on real estate.

With higher interest rates, higher inflation, and slower economic growth, how do REITs perform?

Higher interest rates will increase the interest expense, and increase real estate cap rates (lower valuations).

This is bad.

Slower economic growth will mean slower growth in rental income.

This is bad

Higher inflation, will mean higher real estate prices. This is good.

But that’s before you look at the demand-supply dynamics of each individual market.

My simple view, is that I think a lot of the secular tailwinds you had for REITs the past 10 years, are gone.

The secular tailwinds for this asset class have reversed.

To perform with REITs in this decade, you need to be more selective about:

- What kind of real estate you are buying (geography and asset class)

- What price you are buying at

A lot of investors are still valuing REITs based on 0% interest rates and thinking they are cheap at current prices.

I encourage you to rerun your valuations using a 4% risk free rate.

Why did I overweight REITs in that case?

Simple answer – of all the asset classes out there, I am most familiar with REITs.

When the time comes, when S*** hits the fan, it will not be easy to deploy capital in size unless you are familiar with what you’re buying.

And of all the asset classes, I am most confident in my ability to identify value, and allocate capital in a big way to REITs.

That said I don’t think REITs will do spectacularly this decade, so I will not buy until I see them at good value.

Rough ballpark, that may actually work out to >6.5% yields on the blue-chip REITs, just to account for the rapid rise in risk free rates.

You can check out my target prices for the each of the REITs on my watchlist on Patreon.

Asian Financial Crisis 2.0 and Sovereign Debt Crisis brewing?

I’ve tried my best to summarise my entire macro thinking into 2000 words, but frankly it’s not easy.

Apart from what I covered today, there are 2 big economic crises worth keeping on eye on: (1) Asian Financial Crisis 2.0 and (2) Sovereign Debt Crisis.

Asian Financial Crisis 2.0

When I say AFC 2.0, I mean it in the context of a currency crisis.

Just pull up the charts of the Japanese Yen, the Chinese Yuan, and the Korean Won.

And you’ll start to appreciate the kind of mess we are in right now.

Big one to watch.

Sovereign Debt Crisis

Another huge one – is Europe.

2022 has shown what happens when a G7 country fixes interest rates at 0.25% and floors the fiscal pedal (Japan).

The past week has shown the way for another G7 country (UK).

And that’s even before we talk about Europe.

Europe is going to experience a deep recession this winter, they will be forced to subsidize energy prices for consumers, and they are going to pay for that by issuing more debt into rapidly rising euro interest rates.

Mario Draghi managed to avert the crisis in 2012 with “whatever it takes”.

This time around, fates may not be so kind.

Closing Thoughts: Don’t fight yesterday’s battles

My fear is that when the time comes to buy, investors will invest like it’s 2012.

They will invest for a decade of zero interest rates, and inflation below 2%.

But if my thinking above is correct, we are never going back into the pre-COVID world.

This will be a world of higher interest rates, and higher inflation.

Think a decade of Core CPI in the 3-4% range, and interest rates bouncing around from 2-4%.

The implications for investing, are game changing.

As always, this article is written on 30 Sep 2022 and will not be updated going forward.

Weekly macro updates and market commentary are available on Patreon.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- Whole bunch of freebies – A free packet of rice (1kg), a free Kopitiam Kaya Toast set, a $1.99 Double Mushroom Swiss at Burger King, and 50% off KFC Zinger Set just to name a few.

- 1.0% base interest on your first $50,000 (up to 1.4%)

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Thanks FH, insightful post as usual. What’s your take on bank stocks?

Well rising interest rates are good for the NIM (net interest margin).

So the key question for the banks is how bad is this recession going to get. And don’t forget, if the recession gets bad enough, governments may step in with massive fiscal stimulus (like we saw in 2020), to offset the pain.

As at right now, it’s not very clear how bad the loan defaults are going to get, which is why you see the SG bank stocks still holding up well.

Always appreciate your insights FH, been very helpful in stress testing / validating my thinking. Just a couple of questions:

I’m inclined to think the HK market follows a slightly different dynamic (timeline) from what you mentioned, since the factors affecting the Chinese economy are different (Covid lockdowns, real estate crisis). At the same time, I think the prices are going to be influenced by the multiples vs US stocks. If US stock multiples get hit in a bad way, I’m inclined to think there will be a corresponding impact in Chinese stock valuations as well. That said:

1. What are your thoughts on the stage of the HK markets in the cycle, and what is your estimation of when the lockdowns and real estate crisis will start to ease?

2. Given the competing factors of the China economy starting to open up vs US stock multiples being compressed, how do you see the impact on HK market prices?

3. Would you have any further input on any factors I may have missed out?

Yup, agreed, and great points that you raised.

To be clear, the analysis in my article mainly applies to global stocks ex China. China operates on a different credit cycle from the west, so the analysis is different like you rightly pointed out.

Some thoughts from me:

1. China is more advanced in the short term cycle than the West. And earlier in the long term debt crisis. So they have more policy levers they can pull, as compared to the US/EU.

When lockdowns/real estate crisis will lift is a political question, and not easy to guess. I would watch the upcoming Party Congress and the post-Congress movements closely.

2. China is more advanced in the short term cycle than the US (they are easing monetary policy as the west is tightening monetary policy). So stock valuations are more attractive than the US. But with China you do need to price in geopolitical risk from the possibility of US sanctions.

3. Geopolitical risk is a big one. Everyone has their own views on whether China will invade Taiwan. My own view is that the risk is low, but I can’t rule it out. If it happens expect Russia style sanctions on China.

Political risk too. Xi is not an easy man to read, there are few in this world that know what he is truly thinking.

So China stocks rightly should trade with a geopolitical risk premium.

That said, China banks trade at almost a 9% dividend yield today. Is that sufficient margin of safety? Ultimately a question each investor needs to answer for themself.

What kind of sanctions on China do you expect besides targeted ones like semi chips? We have seen how sanctions on Russia have backfired. How the trade war led to US consumer paying more for goods and increase inflation. Sanctions are definitely lose-lose. Question is who lose more?

China is still the de facto world’s factory even after many companies have setup factories elsewhere. Many components come from there. Nowadays it’s very difficult to manufacture a product (machineries, electronics) without a single component coming from China . How do you sanction? No other country can absorb the mass manufacturing capability and infra that China has. The sheer scale and “China speed” which leads to cost effectiveness in manufacturing cannot be replicated elsewhere. Which other country has the sheer labor force and infra to do all these? Not even India.

Trade deficit with China is rising non stop despite trade war and decoupling etc lol. How do you sanction? I really don’t understand. Can we all think on a deeper level instead of just say “sanction”? Further I’d say this Great Decoupling will eventually cause US to lose more in the long term since US corps have been riding on China’s growth for past 20 years. With China becoming more self-sufficient, more revenue will go towards domestic companies. Imports from US will go down. Trade deficit will widen. China can export its cheaper products to BRI countries to displace US products. All in all, US is in a more worse situation in the longer term

US dollar is slowly but surely losing its appeal. It’s status as global reserve currency is gradually eroded. Long-term wise does not bode well. Countries are diversifying their assets. Western Europe is in deep shit, with deep recession with high national debt. The west might not hang on for a few more decades. If a crisis happen every 10 years, they will eventually go down, they cannot take the damage for so long and they don’t even “heal” themselves, unlike China which has been focusing on solving domestic problems relentlessly, tackling property bubble , corruption etc. China EVs may eventually replace the ubiquitous Japan cars we see on the road. My prediction is all these developed countries suffer from too many problems that have been snowballing for the past several decades and they don’t fix those problems. Eventually they will be doomed.

One prime example is UK. The sun is indeed setting on this once-glorious empire. The pound is losing its value rapidly. A few more crisis and that’s it. The leaders are morons. There are also many separatists (Scotland) calling for independence. First is Brexit, second, I predict UK will break up then later on EU no more. Japan is probably doomed as well. And lastly the US. This Ukraine war is just the beginning of a new world order indeed.

Actually US has a lot of debt as well, see https://www.usdebtclock.org/

And it has significant hidden debts in the form of “money that is supposed to be spent but not spent “ eg rebuilding infra will take 3 trillions at least. Investing in healthcare, education, social systems, etc. all these are hidden debts. Every aspect of their system is dying and rotting. Only the Big Tech and elites are thriving , albeit on a bedrock of quick sand. At some point they have to invest all these money but their hands are tied. Too slow and too little funding to solve these problems. 10% of their federal budget go towards paying debt interest . Will definitely be higher in the future, maybe 25% I won’t be surprised. Then they have to print even more to pay the debt. Eventually will become banana money

I suppose the analogy is UK in the Post WWI period, dealing with a rapidly rising US.

It is only natural for the incumbent to want to take moves to surpress the rise of the challenger. While the challenger will do everything they can not to be surpressed.

How exactly it evolves day to day is not easy to predict, but it is fair to expect more conflicts between the 2 as China continues its rise.

Can you comment on why the A shares market is more stable than H shares? Seem like Hk stocks are dominated by western investors who are fearful of China Covid policy and slowing growth and sanctions.

Because of capital controls.

Like you pointed out, A shares are dominated by onshore investors who cannot move their money out easily. H shares are dominated by western investors (or instis), who can, and do. Which is why A shares consistently trade at a premium to H shares.

Xi’s plan is simple: to make China great again. I just focus on his goal of doubling GDP by 2035. As an investor I will buy stocks that are relatively immune from sanctions and geopolitics and can grow in tandem with the GDP. I will invest overweight in China and will continue to hold for the long term. I believe the tech ‘crackdown’ has many goals: to tame the big tech, control them, push them to innovate harder(chips, expansion overseas) . The so-called “common prosperity fund “ is just corporate social responsibility which many other western companies do. See baba is now trying to expand aggressively overseas instead of isolating itself within China and strangling domestic competitors . And Jack Ma is not the charismatic angel that most people know of. He has scheming ideas . I think ccp did the right thing although too aggressively. But can’t blame them as mainstream media likes to exaggerate china moves and spread fear.

Interesting comments, appreciate the sharing.

Nice read, FH! Thumbs up.

One more scary thing. Prospect of a wider war driven by a madman. Russia might have attacked NATO assets in the form of Nordstream.

Also about financial instability. Lael Brainard, Fed dep gov, warned yesterday they were closely monitoring US financial event risks like what happened in the UK last week. But she went on very hawkishly that the Fed would not stop inflation fighting prematurely. This might be a very long bear (not just ending in 2023). There are a multitude of ways the Fed can do emergency measures to stop a negative financial event without actually easing rates. No one wants to be Arthur Burns.

Thanks! Glad you find it useful.

Agree with this. There is a possibility that this bear may last beyond 2023.

It probably won’t be my base case, but it is worth being at least alive to the possibility.

Funnily enough, I’m not so sure if I believe the Russians blew up Nordstream. They can easily turn off the tap, what’s the incentive to blow it up? The better question might be – who stands to benefit the most from the blowing up of Nordstream?

Haha, that’s a good conspiracy theory! ????But I think it’s Putin, to say there are long term ramifications about Russia not supplying natural gas to Europe even after the war.

Hi FH love your work. Keep it up.

Thanks! Appreciate the support!

SG reits, are taking a beating right now,

So FH, those SG reits that you bought in 2020, and 2021, or even 2019,

Are you still holding them right now ? Or sold all of them already ?

Most of the non-core REIT positions I sold in late 2021 / early 2022.

The remaining are core positions that I continue to hold. That said, I have significant cash on the sidelines that I intend to deploy in line with the thinking set out in this article.

Dear FH

Thanks for this. Although I agree broadly with your opinion, the fact is that we are now going to be led by Q3 earnings and the next CPI data coming out in the second week of October, just preceding the earnings season

If either and more worryingly both disappoint, we will see the SPY go from the current 3580 quickly within a couple of weeks to 3200 and then 3000. The latter will reflect a baked in moderate recession at 15 times 2023 earnings at 200$ for the SPY

Current 16 is still overstretched if earnings fall. The recent earnings mostly have been followed by significant drawdowns for the likes of FED NKE MU etc etc

With an unrelenting USD, earnings will fall plus associated guarded outlook will trigger

We will touch 3200 if not 3000, there will be sheer overwhelming negativity and if the PCE plus CPI at least fall, the Fed will pivot and the markets will start to poise themselves for the slightest trigger to rally, anticipating a softer Fed

The SG market as of today is already lower then its 20 and 50 DMA and the RSI showing nearly oversold conditions. I have started nibbling at the REITS plus adding to the banks and will do so as these serve as a natural hedge to each other in these treacherous conditions

Am surprised that your hypothetical 1 m SGD allocation had nothing for the banks

The SG banks will have much lower NPA and bad loans as compared to the rest and the fed linked transmission of rates will shore up their NIM that will more than compensate the downside risk posed by poor loan growth and higher NPA losses

Regards

Garudadri

Banks are interesting, but not yet cheap. DBS is at 1.5x BV, with BVs set to drop with higher rates. OCBC and UOB are cheaper at 1x PBV. Credit liquidity events may centre around banks and FIs a la Lehman.

Everyone seems to be gunning for 3000. Would be careful if it is a common sentiment around that level.

Hi Garudadri,

Am actually curious for your views on the banks.

My simple view is that while rising rates mean stronger NIM for the banks, much will depend on the level of bad debt going forward. This will depend on (a) how deep a recession we go into next year, and also on (b) how much fiscal stimulus governments decide to pump in when the time comes. Whatever the case, if cycle bottom for the banks is going to be 1.5x book value on DBS, then I probably just hold my existing bank positions and allocate cash elsewhere.

The 200k allocated to stocks was designed for this. If the banks sell-off, definitely I add. If they don’t sell-off, maybe because govts unleash huge fiscal stimulus again, then I allocate elsewhere.

Agree that fair value probably lies around the 3k range. Although I would caution against placing too much reliance on valuations in this market, which is primarily driven by liquidity and flows. If we do break to 3000 in a couple of weeks, I would expect other things to start breaking elsewhere. The magnitude of the move and the velocity of the move cannot be separated, especially given how tight liquidity is at the moment.

Hi FH! Great post! However, what are your thoughts on DCA-ing through this bear market instead of timing the Fed pivot?

Well there are 2 ways to invest: (1) DCA into a diversified portfolio regardless of market conditions and (2) market time to try to outperform the market.

Both are acceptable ways to invest, there is no right or wrong.

This article was written more from the perspective of those trying to do (2)! 🙂

I like how you accurately describe the big sh*t we are currently in and round it off with recommending a credit card that comes with free rice as sign up gift 🙂 Tough times!

Haha thanks for the light hearted comment. I chuckled to myself when I saw this! 😉

2018, 2022 is a monetary tightening or a hawkish stance adopted by G20 nations in this normal business cycle. The difference in 1997, 2009 is unforseen financial crises. As it implies a financial crises is the inablitiy to repay loans at the national and household level. When an economy is overleveraged, household and national debt is over 60% of income in 2009 is characterized by bank failures. Consumer banks are guaranteed by the gov and are required to have a certain amount of capital or minimum fixed deposits with the central bank to dispense loans. To maintain the minimum capital they depend on consumer deposits. The interbank lending mechanism banks to banks lending is used to maintain the minimum required amount of capital. When an economy slow down in 2022 due to inflationary pressures pushing UP prices of everything from grocery, fuel, electricty to the prices of homes to unsustainable level, the hawkish stance breaks the bubble. Bubble simply means that. The higer interest rates should slows everything down. Gov and Business revenues start to fall. Gov and corporations might default. The income pyramid crumbles when the bottom is in difficulties. Debt is is omnipresent. Corporations and govs normally runs on debts in its policies. With the exception of Germany’s Angela Merkel the swabian housewife policy. Gov debt, is with the IMF and World Bank. Thats where all the countries globally sets aside a certain sum of money. In effect its Country A is lending -to Country B. Whoever has the highest says. Local bank A loans with bank B. A-B, A-B , A-B will all be in an “inter-lending” commitment. The thing to watch out for is when these failures (2009) which starts at the bottom cascades into banking failures at every level. When income plummets starting from businesses, next Tom, Dick, Harry, then at the national level. A cannot repay B cannot repay C defaults in a interconnected crises. At the apex of the pyramid IMF and World Bank comes to the rescue at the national level. Bailouts at the expense of debt restructuring. Simply a new larger amount with a longer time frame with new interest rates. Zambia recently. The thing of interest is Just “how leveraged” are household and national debt to note when interest rates starts to rise in this business cycle in 2022.