I’ve been hearing a lot about the mythical 5-figure dividend portfolio recently.

The idea is simple – invest enough into dividend stocks / REITs, that you get a 5 figure dividend each year.

Once the dividend portfolio gets big enough… voila, you are free to quit your day job and live off the dividend income alone.

How much for a comfortable “5-figure dividend portfolio”?

At the same time, a Patron asked how to build a 5% yielding dividend portfolio.

Now that really got me thinking.

Let’s say one has $1 million stashed away.

Let’s say one then invests this $1 million, into a low – medium risk 5% yielding dividend portfolio.

That works out to a $50,000 annual dividend income.

Okay given how expensive things are in Singapore, that’s not exactly enough to live a high roller lifestyle.

But at $4,000 a month, it’s definitely more than enough to get by.

Rules for the 5% yield dividend portfolio

Portfolio 1 – Singapore only Portfolio

The rules for the dividend portfolio that I was asked to build by the Patron:

- Singapore dividend stocks / REITs only

- No more than 50% allocation to REITs (for diversification)

- 5% dividend yield

This is meant to be a low to medium risk portfolio, with dividend stability as the paramount goal.

When you plan to live off the dividend income, you don’t want to take unnecessary risks with it.

Portfolio 2 – No Rules Portfolio

But as I was building the dividend portfolio, I realized that there were a few notable shortcomings with the Singapore only Portfolio.

So… just for kicks, I also decided to build a no rules portfolio.

Rules (the irony) for the no rules portfolio are:

- 5% yield target

- No restriction on stocks / asset allocation

Stocks Masterclass Flash Promo ends tomorrow!

Learn how to build a portfolio of dividend and growth stocks, with a massive discount right now. Find out more here.

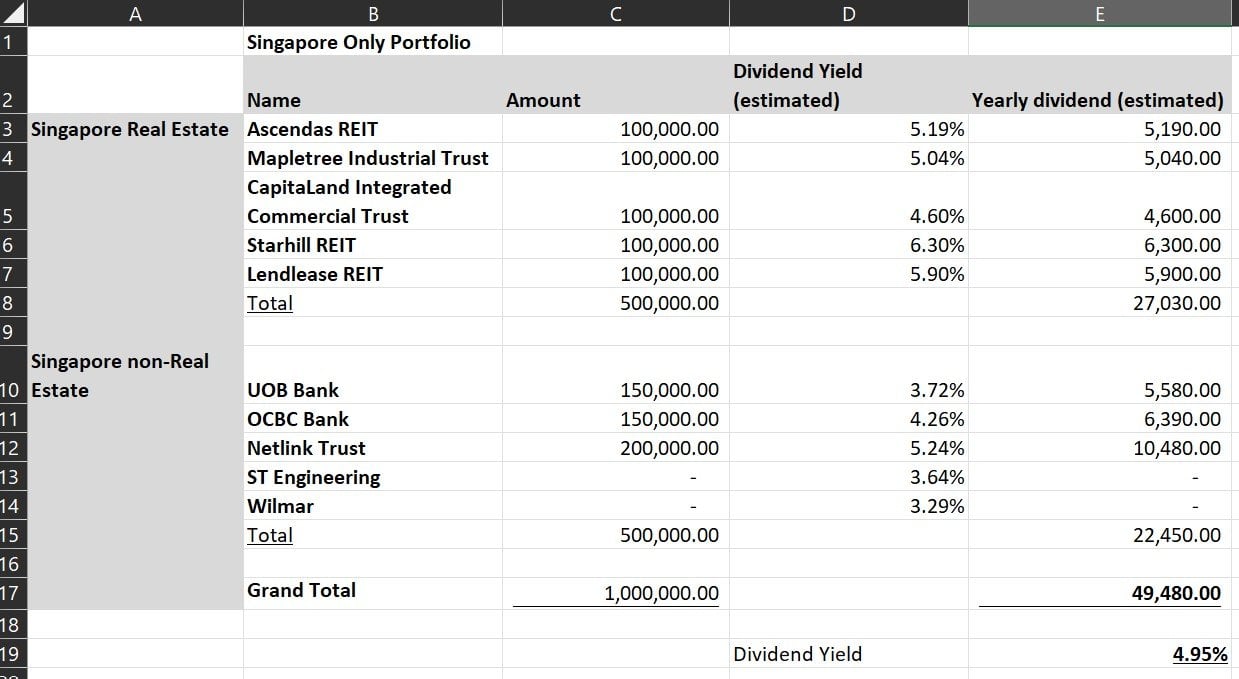

Portfolio 1 – Singapore Only Dividend Portfolio (4.95% yield)

The Singapore Only Portfolio is allocated:

- Singapore Real Estate ($500,000)

- Ascendas REIT – $100,000.00

- Mapletree Industrial Trust – $100,000.00

- CapitaLand Integrated Commercial Trust – $100,000.00

- Starhill REIT – $100,000.00

- Lendlease REIT – $100,000.00

- Singapore non-Real Estate ($500,000)

- UOB Bank – $150,000.00

- OCBC Bank – $150,000.00

- Netlink Trust – $200,000.00

The split is:

- 50% REITs (Singapore Real Estate)

- 30% Singapore Banks

- 20% Netlink

And the estimated yearly dividend is $49,480, which works out to a 4.95% dividend yield.

I’ve attached the excel for both portfolios here, so you can play around with the numbers if you want.

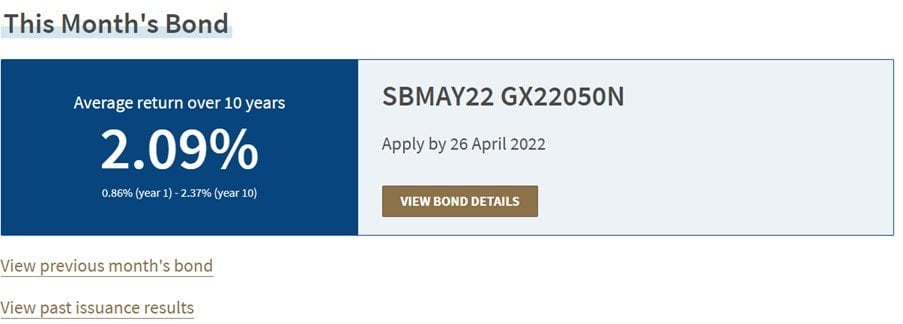

Is this Singapore only Dividend Portfolio risk free?

2 words – Absolutely not.

The latest Singapore Savings Bond pays 2.09% per annum.

If you want risk free, that’s the yield you need to accept.

With this dividend portfolio, we’re looking at almost a 3% yield higher than the risk free.

There’s no free lunch in this world, and this should give you an idea of the risk you’re taking on.

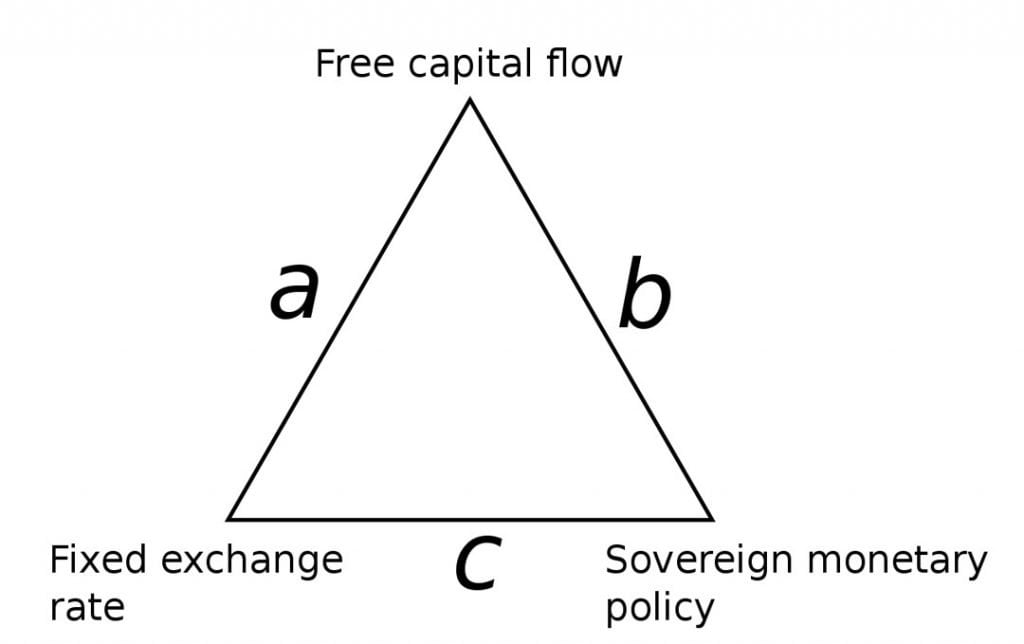

What is the main risk behind this dividend portfolio?

My view – Interest rate risk.

This portfolio is very vulnerable to changes in Singapore interest rates.

Singapore interest rates are basically tied to US interest rates because of the impossible trinity (by controlling SGD Forex and free movement of capital we give up control on interest rates).

If US interest rates go up, Singapore interest rates will go up.

Which means for this dividend portfolio, the worst thing that can happen is a prolonged period of the US Federal Reserve raising interest rates.

I did try to offset it by building in a 30% allocation to the Singapore banks, which should benefit if interest rates continue to march up.

But frankly, much depends on the inflation outlook here.

If inflation stays sticky, and the Feds keep on hiking, then at some point the banks will stop going up in price, and the REITs and Netlink trust may get crushed from higher rates.

Is this dividend portfolio too concentrated?

Yes, potentially.

I did consider names like ST Engineering, SGX, Wilmar, Singtel etc.

Just to diversify away from banks and real estate.

The main problem was that the yield there is usually in the 3% range.

So if you do want the diversification, in this market at least, it will have to come at the expense of dividend yield.

Only banks and real estate have the dividend level required to hit the 5% target.

Is there capital gains potential?

Another big drawback – I don’t think the potential for capital gains for this portfolio is very high.

In some ways, this portfolio sacrifices capital gains for a higher yield.

The REIT portion can probably have 1-2% long term capital gains potential.

But Netlink Trust not so much.

And the banks, at this point in the cycle you’re probably buying at the higher end of the valuations.

So it’s hard to see much capital gains too.

But enough talk – let’s move on to the No Rules Portfolio.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

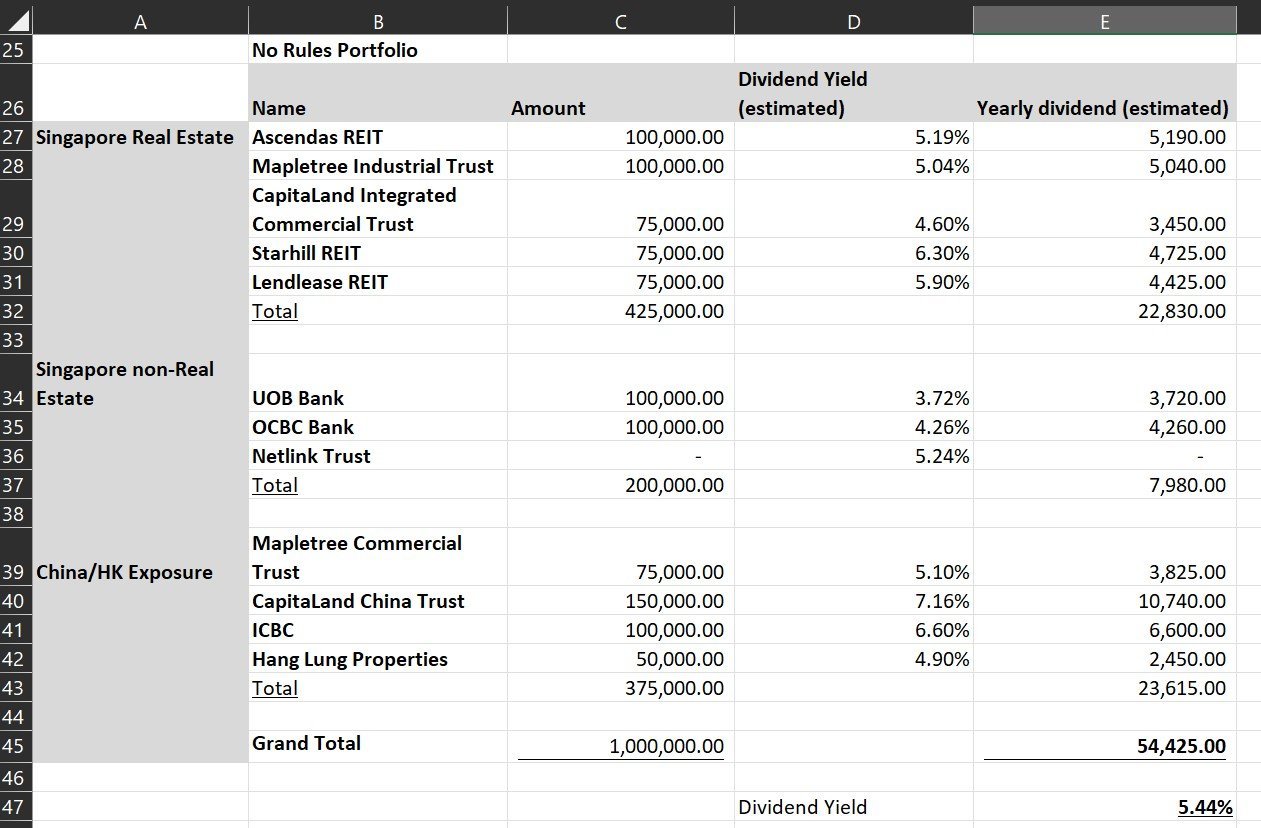

Portfolio 2 – No Rules Dividend Portfolio (5.44% yield)

For this portfolio – anything goes.

Do anything to hit 5% yield, without taking on stupid risks.

This was the allocation I used:

- Singapore Real Estate ($425,000)

- Ascendas REIT – $100,000.00

- Mapletree Industrial Trust – $100,000.00

- CapitaLand Integrated Commercial Trust – $75,000.00

- Starhill REIT – $75,000.00

- Lendlease REIT – $75,000.00

- Singapore non-Real Estate ($200,000)

- UOB Bank – $100,000.00

- OCBC Bank – $100,000.00

- China/HK Exposure ($375,000)

- Mapletree Commercial Trust – $75,000.00

- CapitaLand China Trust – $150,000.00

- ICBC – $100,000.00

- Hang Lung Properties – $50,000.00

Asset allocation is:

- 25% REITs (Singapore Real Estate)

- 20% Singapore Banks

- 75% REITs (HK/China Real Estate)

- 10% China Banks

Geographical exposure is:

- 67% Singapore exposure

- 33% China exposure

And the estimated yearly dividend is $54,425, which works out to a 5.44% dividend yield.

Why no US stocks?

Simple answer – 30% dividend withholding tax on US stocks kills any dividend portfolio.

To achieve a 5% dividend using US stocks, you effectively need to buy stocks with a 7% dividend.

That requires you to take on a very real risk of capital loss.

Risk-reward doesn’t make sense to me.

Why not buy US stocks for capital gains?

Remember the idea of this portfolio is to live off the dividend income.

With capital gains, at some point you need to sell the stocks to harvest the gains – to fund living expenses.

That brings up questions about timing.

And don’t forget if your stocks drop but you need the cash, you’re forced to sell a bigger proportion of the stocks than you normally would.

Given the whole point of this is to free up time to focus on other things in live, a capital gains portfolio requires too much active management to work.

How does this solve interest rate risk?

Well, not directly.

The key thing to note is that China’s economy operates on a different monetary cycle from the west.

2022 is a good example – going forward the US Federal Reserve and European Central bank will be forced to raise interest rates to combat inflation.

While the People’s Bank of China will instead be cutting interest rates to stimulate growth.

So by increasing exposure to China dividend stocks, you’re reducing your sensitivity to the US interest rate cycle.

With this portfolio, 33% is China exposure, 20% is Singapore banks.

So that’s almost 50% of the portfolio that is not so vulnerable to rising interest rates.

But… you are taking on China risk…

Of course – there is no free lunch in this world.

While you do swap out US Fed rate hike risk, you’re taking on Xi Jinping risk.

I know many of you have strong views on whether China is “uninvestible”, or whether China is the next global power.

For me personally, I am a long term China bull, but a realistic one at that.

The path forward for China is paved with real uncertainty and obstacle. They need to navigate COVID zero, soaring commodity prices, slowing growth, all while a real estate bubble is bursting.

But I do think that as this century continues to play out, China’s influence will gradually increase.

But I mean, I could be wrong here.

If you’re not comfortable with China risk, you can stick with the Singapore only portfolio.

Why no energy or commodities stocks? Inflation risk?

I actually really agreed with this.

In a world where central banks can print money at will, where governments can inject fiscal stimulus to offset any recession – what is the material constraint?

It is the stuff that we cannot print –gas, oil, commodities.

The more I think about it, the more I think the path forward may lie with commodity shortages, and higher interest rates.

Which is why I was so concerned with interest rate risk with this dividend portfolio.

After a 40 year period of declining interest rates, investors are conditioned to think that interest rates can only stay at zero.

What if that’s no longer true?

What if 5 years from now, the long term neutral interest rate is now 3% instead? What about 4%?

Will real estate or tech stocks still perform so well?

The problem though, is that energy or commodities (at current prices) don’t deliver the 5% yield required.

So I couldn’t find a way to make the portfolio work with energy/commodities, while still hitting the yield targets.

And this is a very big risk to note.

The million dollar question – is it feasible to retire off this dividend portfolio?

Most financial advisors will tell you that a “safe” drawdown is 3-4%.

This means that if you have a $1 million portfolio, you can drawdown 3-4% a year long term, into perpetuity. Without risk of the capital running out.

And building this dividend portfolio, I’m inclined to agree with that.

By forcing a 5% yield into these portfolio, I was effectively taking on higher risks.

I was either taking on concentration risk, or interest rate risk, or China risk, or giving up capital gains potential.

So… is it feasible to retire off this dividend portfolio?

I think it works in the short term.

But if the plan is to rely on this for the next 20 – 30 years, there are real risks in play.

A prolonged period of inflation and rising interest rates will absolutely crush this portfolio.

Not only would you be hit by rising cost of living, rising interest rates may also crush the real estate portion of the portfolio.

So a pure passive approach may not be possible here. Some active intervention may be required to avoid significant capital loss, in the event that inflation stays high.

Other options to consider – CPF or Rental Income

Practically speaking – most investors will not rely solely on their dividend portfolio.

Most people will have either CPF to fall back on, or perhaps an investment property for rental.

CPF actually is a very strong option here.

With the right options CPF can provide a recurring stream of cash flow every month, risk free.

Closing Thoughts – Inflation is your biggest enemy

Is it a coincidence that the FIRE movement (Financial Independence, Retire Early) arose in a decade of record low interest rates, low inflation, and soaring stock prices?

Building these 2 dividend portfolio has taught me a key lesson.

Once you throw inflation into the mix, almost every single assumption investors have relied on the past few decades no longer works.

With a dividend portfolio like this, you need to think about whether your dividends can rise fast enough to keep pace with price increases.

Sure $4000 a month is more than enough now, but what if the price of food in NTUC continues their relentless march up? As does petrol? And electricity?

And if inflation stays high, interest rates are going to stay high.

What would a period of higher interest rates do to a dividend portfolio like this?

Stocks Masterclass Flash Promo ends tomorrow!

Learn how to build a portfolio of dividend and growth stocks, with a massive discount right now. Find out more here.

As always, this article is written on 2 April 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patreon.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Shopee share (worth $160), zero commission trades & more, if you’re new to MooMoo and fund $2700.

Get 1 free SoFi stock, zero commission trades & more, when you open a new account with Tiger Brokers and fund $2000.

Special account opening bonus for Saxo Brokers too (drop an email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Just buy the higher income portfolio from Endowus for greater global diversification will do.

Underlying risk is the same though – interest rate risk.

And with an 80% allocation to fixed income, it’s arguable the risk for capital loss may be even higher, without the upside that equities have.

Interest rates up bond prices down, the Endowus income bond portfolio like how they over promise their cash smart portfolio will drop until u got no eye to see haha..good luck with endowus

Yes – exactly my concern with fixed income portfolios in this climate. The yield looks good, but capital losses can be very real.

Q1: Why no HKEX listed REITs?

Q2: Though new, can also explore China REITs.

Hi MSFlyer,

1. Any REITs in mind? Names like Link REIT are sub 5% yield, so I used MCT/CLCT/Hang Lung to replace the China/HK real estate exposure. But no issues if you prefer HKEX listed REITs.

2. By China REITs you mean the onshore listed names right? They’re all part of the new pilot program, infra assets and trading at 3% yields last I checked. Doesn’t really work for a dividend portfolio like this, best to use the offshore listed China names and arbitrage the capital controls (onshore listed names always trade at a premium due to capital controls).

Hi FH,

Great article as usual. A few thoughts on my end.

1. Be wary of home market bias – in a world of ever increasing uncertainty, diversification probably means across geographies, sectors and currencies. Having a 100% Singapore/China portfolio comes across as too concentrated from both a risk and opportunity standpoint. For example, my comment on European banks previously. I picked up some Lloyds at 40p during the crash which is 5% on current dividend yield and 7.5% on pre-Covid dividend yield. It has already provided 20% capital gains in 2 weeks. Credit Agricole also hit 9 Euros when its declared dividend policy for next 2 years is 1 Euro per year.

Similarly, the best performing REIT in Asia has historically been Link REIT. This was also available just couple weeks back at 5% yield, highest in years, when it was trading at $60. Link has increased DPU every year for more than a decade and have never had to raise capital from investors from dilutive rights issues.

There are many bargains to be had if we scan the globe and do not restrict ourselves to just Asian markets.

2. It may be more fruitful to have an exercise of how you would allocate a $1M portfolio based on your ideal portfolio mix rather than actual current prices. That is, what is your all weather dividend portfolio? For me, I try to balance REITS with Banks and Commodities so that it works in rising interest rate and inflationary environments and also when the opposite is true. Then once you have identified your target portfolio allocation, have to be opportunistic about the right time to buy. E.g. China banks few months back, some banking and REITs couple of weeks back during the war crash, oil stocks during the Covid crash etc. Over time, you will then get a long-term resilient portfolio with the required yield. What is important is to know what your target portfolio looks like but you don’t need to get it all in place immediately if you want to buy-in cost effectively. Maybe you can consider such an exercise as an article?

3. I am more optimistic about resilience of REITS in inflationary environments – as shown by your previous chart of performance of different assets under different environments. While there may be a short-term hit to share prices and DPUs, in the mid-term the underlying value of the properties will rise and rents will re-adjust so they will likely recover.

Oh CMC, you have outdone yourself with the comment this time. Absolutely fantastic thoughts.

My thoughts:

1. Congrats on the Euro banks call btw – Absolutely fantastic, 20% capital gains across the board in 2 weeks on the Euro bank names. Fantastic trade.

2. Yes good point on the home market bias, I do admit there is home bias in both portfolios. The Singapore only one can’t be helped because the reader wanted a SG only portfolio, but for the no rules portfolio I agree more some more global exposure would make sense.

3. Yes, the problem with this portfolio is that I was constrained by how prices are trading at today. I would have dearly loved to add commodities and energy, but at current yields I would not have been able to hit the 5% yield target.

Good point about the all weather. Will look into it, but it may look like my own personal portfolio now, with a broad mix of real estate, equities, commodities, precious metals etc.

4. I like REITs in inflation. The only concern is that if interest rates stay high for a while, at some point that will flow back into real estate cap rates and valuations. And whether we have sustained high interest rates will depend on the inflation outlook, which at this point is not so easy to call. Interest rates can only kill demand, they cannot solve supply side issues. And with things like oil/commodities, it’s not like you can build a new mine and have the supply come online by Christmas 2022. The capex will take years to bear fruit, and companies are very reluctant to invest in new names because of the whole ESG push.

Interest rates will go up because of high inflation. But with higher interest rates, economy will slow down. With the inverted yield curve this week, the recession warning signs are flashing and we’re probably on a countdown now. Do you think the Fed will be forced to reverse course to either pause or reverse rate hikes to support the economy when/if the recession hits?

I think the answer to this depends on the terminal inflation outlook.

Let’s say we are in early 2023, and the Fed Funds Rate is at 2%. Does inflation stay at above 5%? Does it drop to 4%? Does it drop below 2%?

The way I see it, only 2 things that will break this hiking cycle:

1. Market breaks (stocks plunge, or treasury/fixed income market blows up)

2. Inflation goes away

So to answer your question, we need to see either inflation going away, or a big break in markets before the Feds change course. For now at least, markets are holding up very well, and inflation is not showing any signs of going away.

But like you said, all the warnings signs are already flashing, and we’re almost certain to head into an economic slowdown. But will the slowdown be sufficient to tame inflation, when so much of the causes are supply side?

I think CMC raises really good points!

Fully agree that it takes time to set up the desired portfolio. With a long enough time horizon. You want to be investing counter cyclically. Picking up the out of favor sectors and waiting for the eventual turn.

On diversification beyond REITs and banks, and beyond Singapore / China, I think there still remains opportunities among the commodity players despite the massive run up in prices. The London Stock Exchange is a good hunting ground for some of the largest commodity producers in the world. For Oil & Gas, Shell or BP. For miners, Rio Tinto or BHP. If we are indeed in a super cycle, then these commodity players could pay elevated dividends for years to come. Final point also is that we are not seeing much by way of capex, which leaves more cash to be paid out as dividends for shareholders.

Agree, fantastic points from both yourself and CMC.

I do agree that commodities/energy could turn out to be the stealth winner this decade. With soaring demand from the ESG push, and a decade of underinvestment into capex, and companies still reluctant to invest into new mines now because of ESG, this shortage could be here to stay.

And on the countercyclical point, funnily enough, despite all that talk about commodities, commodity names are still very underinvested in. Just look at the proportion of energy/commodities as a percentage of the S&P500, or as a percentage of institutional holdings!

So yes, agree that commodities could hold good value. LSE is good hunting ground, and the withholding tax treatment is great. There are some listed in Canada as well (TSX).

Hi FH

Thanks for this

CMC has made a very important observation regarding avoiding home bias and geographical diversification along with sectoral diversification

I did the same like the other reader and bought LLOY HSBA during the pandemic phase locking into yields that will likely go higher on cost with the uptick in the interest rate cycle

Loading up on oil and commodities means buying at the LSE, which I regularly do, as you get the full dividends . The miners are posed delicately and certainly are more risky just like the oil majors NOW. There is a small currency downside risk with the £ performance being uninspiring and therefore this needs to be factored in for SG investors

Finally, although we lose out on dividends, the US stocks can be TRADED and the profits cycled into SG REITS and other dividend stocks as well- something I have done all the time

The growth in capital is essential as a buffer for the inflation factor that you pointed out at the end.

Our famous passive income stalwarts AK, STE etc have done this judiciously and they are our local inspiration as far as high yield investing is concerned

Regards

Garudadri

AK I know of, who is STE? I should also read his blog…

He is my friend who retired a few years after me. Good guy.

Hi Garudadri,

Fantastic comment as always. Really enjoyed reading your comment, and yes – I agree with the points that you raised.

Btw – congrats on the Euro banks pickup! Fantastic trade. Although I suppose these are long term holdings for the dividend, and so you don’t plan to sell it anytime soon?

Yes

LLOY HSBA are my Long term holds and though both are significantly down on my buy price average over the past decade, their dividends – except recent cut associated loss, have helped me recoup paper losses

With the upcoming interest rates upcycle, they will hopefully hike dividends and do well

Understand – appreciate the sharing.

$4k/mth go Malaysia become $12.5k liao, more than enough to rent a nice condo and live comfortably haha

Haha, indeed!

what about 2800:hk @ ~3% that tracks the hsi index, 2 weeks ago it was at 18000ish.

current level is at 22000+/- , the average should be somewhat between 25000-28000 when it fully recover, that would ramp the dividend to above 3% and literally risk free with potential upside.

Well I wouldn’t say the HSI is risk free haha, but I do get what you mean. I didnt want to go with this approach because the dividend yield at 3% is much lower than 5% which was what the reader asked for. If one is able to accept a 3% yield, then the simple solution is to just buy HSI and STI ETF, get a 3% dividend, with capital gains potential.

Hi FH,

Love reading your articles. I have few questions below

1) How about Kep Infra Trust? The infrastructure trust is similar to Netlink Trust

2) How do you think of SG stocks with other countries besides China/HK exposure. Stocks like UtdhampshReit and Frasers L&C Trust

3) Also, are stocks of quarterly payout better options than those that gave out in semi-annual and annual basis? If so, should we consider DBS and Mapletree Log Trust instead if they ever reach good buying price level ?

Hi Ed,

Thanks for the support!

My replies below:

1) Yeah quite a few have asked about KIT. Simple answer is that I have not looked into it closely, so I cannot comment on the yield stability as compared to Netlink.

2) Real estate is a local business. I am not familiar with Aussie or US real estate, so I dont invest in those REITs. For investors who are familiar, feel free to go ahead.

3) This one is a personal choice. Those who rely on the dividends for cash flow might like quarterly payouts. For me frankly it doesnt make a difference. DBS and MLT are good counters, but I didn’t include them because I think they are on the pricey side, and their yields would be a drag on this portfolio which is trying to hit a 5% average yield.

I just sold it a few days ago. Look at their propose new fees structure before buying…

I like how you balance out the interest rate risk by including local banks.

Simple and effective.

However, I’m not keen on netlink trust currently. Almost no room to go up. Should the market break and we see a sell-off then yeah definitely.

Agreed that capital gains potential for Netlink is limited here. But with the pace of rate hikes and QT to come, who knows what will happen next 😉

its hard to catch bottom but if one had an average buy price at 18000-20000 and assuming the dividend payout stays at 3% when it recovers to the 28000-30000 level, you will be sitting on huge capital gain and if one decides not to sell, the return based on the low entry price is somewhere between 4-5% dividend payout

is this a viable strategy?

Yeah get what you mean. It’s basically buy and hold right?

My apologies, speaking as an American living in Sg – is the tax on US dividends you mention specific to Singaporeans? Otherwise, qualified dividends and capital gains in the required income range you are mentioning would be taxed at 15% max, and likely at 0%.

Yes that’s right. This is intended for Singapore investors investing in US, not for Americans.