I received a very interesting question from a reader recently:

Hi FH

Thank you for your analysis of T-bills and REITs. I feel your analysis is grounded in reality as compared to other singaporean commentators who seem to be perpetually bullish, especially on when fed will start dropping rates.

I am curious, could you do an article on the Sreit leaders index? Forecast on where it will go in the next 2-3 years? I hold a significant position via syfe reit+ portfolio as i didnt want to dabble in individual reits. I should have pulled out when the interest rate hike started in late 2021 but i underestimated the drop on prices and am now sitting on a 10% loss.

Here is my view, what do you think?

- Fed rates will start coming down in h2 2024, if not later

- Dpus continue to be impacted as we have a high interest rate env for a few years now. Any refinance in the next 4 years will be at higher rates than before meaning we can expect debt to get costlier.

- Rentals have increased so there is some offset, but rentals in sg are already very high, they dont have much room to grow.

- There are some bright spots in sreit leaders index, but as an index it will still trend downwards for at least until 2024, then maybe range bound in 2025 and then start picking up in 2026. So its better to liquidate the reits position in sreit leaders index, and invest in specific reits u have analyzed… or just put it in sgbs..

What do you think?

What is the reader asking about REITs?

The more I thought about it – the more intrigued I got.

The reader is basically asking 3 questions:

- How will REIT prices play out over the next 2 – 3 years?

- What is the best way to invest in REITs for the next 2 – 3 years? Passive indexing or picking individual REITs?

- What could go wrong with investing in REITs now?

Obviously nobody has a crystal ball to answer this definitively.

But I figured I would share my views – and feel free to let me know if you disagree.

Basics: What is the S-REIT Leaders Index?

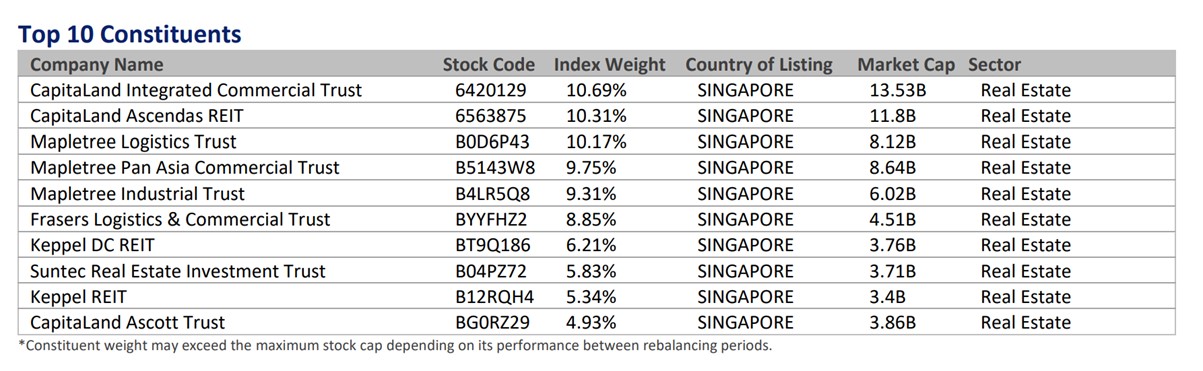

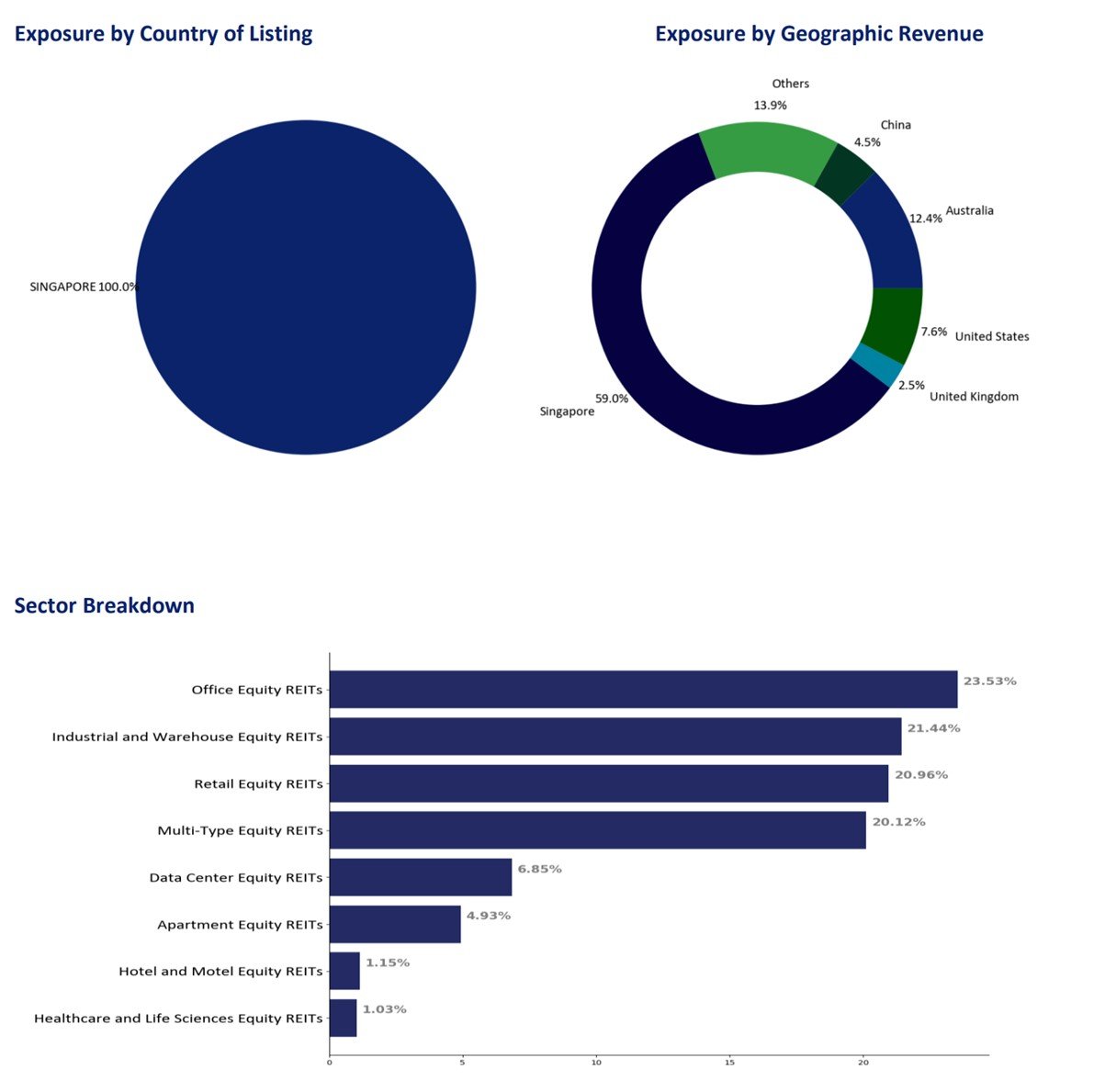

The iEdge S-REIT Leaders Index is a “free-float market capitalisation weighted index that measures the performance of the most liquid real estate investment trusts in Singapore in SGD.”

Basically, it’s an index of the blue chip REITs in Singapore.

Top 10 REITs are below, and its exactly as you would expect – CICT, Ascendas, MLT, MPACT etc:

Like the reader said – REIT prices peaked in late 2021 (before interest rates started going up).

REITs then bottomed out in late 2022 – followed by a small recovery in 1H 2023.

And recently it’s gone back down to 2022 levels again.

How will REIT prices play out over the next 2 – 3 years?

But that’s all in the past.

Where are REIT prices headed the next 3 years?

I’ve set out the reader views in bold below, and added on my comments.

Reader Thinks: 1. Fed rates will start coming down in h2 2024, if not later

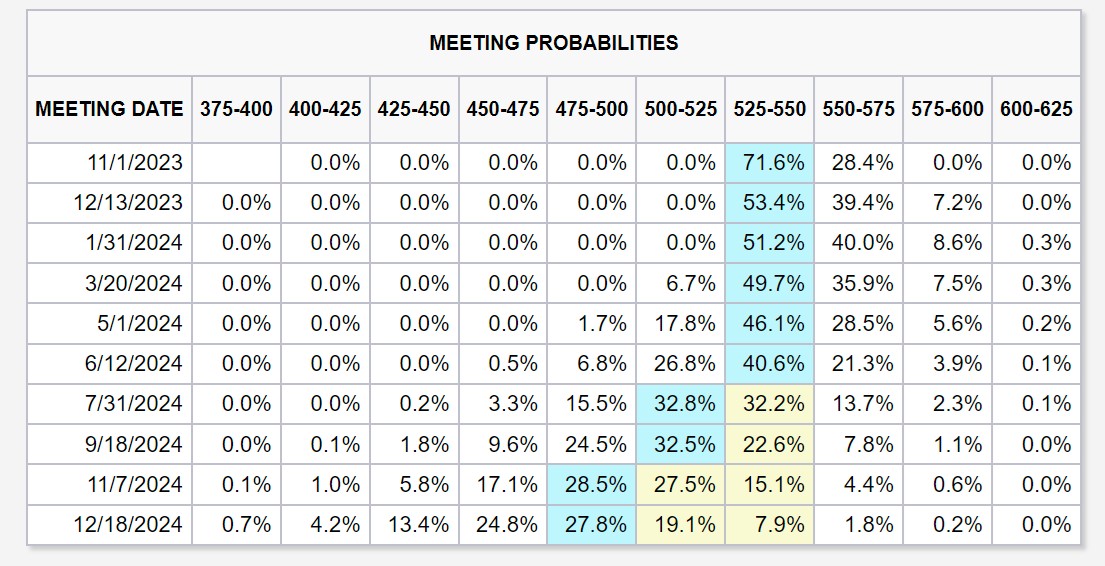

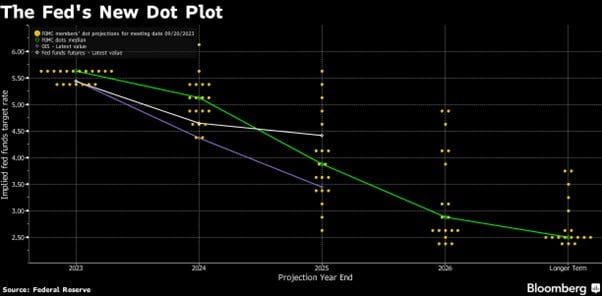

After this week’s FOMC – market is pricing in exactly the reader’s view.

Interest rates to stay flat until 2H 2024, followed by 2 interest rate cuts in 2024.

You guys know me.

For much of this cycle – I have been banging on and on about how interest rates need to go higher and stay there longer than what is priced in.

All that has played out.

Today, market thinks we stay at 5.5% interest rates until 2H2024, with only 2 rate cuts in 2024.

And I’m not so sure I agree with that view.

I think over the next 12 months, the risk is for economic growth (and unemployment) surprising to the downside.

I think there is a real risk that interest rates need to get cut faster, and deeper than what the market is pricing in.

And I don’t think this has been priced into REITs.

Reader Thinks: 2. Dpus continue to be impacted as we have a high interest rate env for a few years now. Any refinance in the next 4 years will be at higher rates than before meaning we can expect debt to get costlier. 3. Rentals have increased so there is some offset, but rentals in sg are already very high, they dont have much room to grow.

This statement by the reader is not wrong.

But this is also one of the biggest points that new investors get wrong.

You never look at the absolute level, you look at the rate of change.

This applies to earnings, it applies to economic growth, and it applies to interest rates.

Imagine that you are driving a car.

Market doesn’t really care what is the speed of the car.

It cares about how quickly the car is accelerating, or decelerating.

Now imagine that in 2024 the Feds instead of raising 75 bps a meeting, they are cutting 75 bps a meeting.

That could be very bullish for REITs from an interest rate perspective.

So it doesn’t really matter what level interest rates are at – if they are dropping quick enough, the market will price that in.

Reader Thinks: 4. There are some bright spots in sreit leaders index, but as an index it will still trend downwards for at least until 2024, then maybe range bound in 2025 and then start picking up in 2026. So its better to liquidate the reits position in sreit leaders index, and invest in specific reits u have analyzed… or just put it in sgbs..

Again, predicting moves with a high level of certainty is a fools errand.

You want to have a view, but you trade based off risk-reward.

It’s not so much about whether you are right or wrong.

It’s about how much you make when you are right, vs how much you lose when you are wrong.

But I don’t want to talk in riddles all the time, so let me answer this question straight.

My view, is that REITs will trade rangebound (or in a downtrend) until the Feds start cutting interest rates.

Once the Feds start cutting, the impact on REITs will depend on (a) why the Feds are cutting, and (b) how quickly they cut.

If Feds cut because of a bad recession, REITs won’t bottom until the economy starts to improve.

If Feds cut because inflation comes down and there is no recession, that could be the bottom for REITs right there (depending on how quickly they cut).

So… Buy REITs now or not?

If you recall, I was pretty bearish on REITs for most of 2022.

To me, investors were underestimating the impact of interest rates on (a) interest expense costs, and (b) property values.

All that has played out.

All the arguments I made last year, I see them parroted around in mainstream media today.

To the point where I would say much of these risks are priced in.

Markets are pricing in rates to stay high in 2024, with only 2 rate cuts.

And the way I see it – interest rate risk over the next 12 months is tilted to the downside. And current valuations are pretty juicy.

So I’m actually more bullish REITs today than I was last year.

What is the best way to invest in REITs for the next 2 – 3 years? Passive indexing or picking individual REITs?

Next question – index or pick individual names?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Passive REIT Investing – Buy the S-REIT Leaders Index (5%+ dividend yield)

The reader went down the passive path with Syfe REIT (tracking S-REIT Leaders Index).

This gave him broad exposure to the blue chip REITs in Singapore.

Blue chip REITs have not been as hard hit as the small-mid cap REITs – and this shows.

You’re looking at 20% declines for the index, vs about 40% declines for the small-mid cap REITs.

On the flipside though.

This also means that if conditions start to improve, you won’t see as big of a recovery.

So it really goes back to what you want.

Are you more concerned about not losing money if you’re wrong? In which case blue chips are probably safer due to the stronger balance sheet.

Or are you more concerned about making more money if you’re right? In which case the small-mid cap REITs probably offer greater upside because they are so beaten down.

Active REIT Investing – $100,000 at 7% dividend yield

If you gave me $100,000 and forced me to buy REITs today?

I’ll probably stock pick individual names.

Personally, I think the small-mid cap REITs offer better value now.

You’re looking at around 6-8% dividend yields, and most of these names are down 40-50% from highs which means they have more room to go up if there is a recovery.

Gun to my head, I might go with something like the following (not financial advice):

- Lendlease REIT (which I just did a deep dive on last week)– 8.1% yield

- Starhill REIT – 7.7% yield

- Keppel REIT – 6.6% yield

- MPACT (but HK play) – 5.8% yield

Assuming you equal weight them – that’s a 7.05% dividend yield that you are paid to wait for the next phase of interest rate cuts. And if (when) interest rates get cut, there could be pretty nice capital gains as well.

Whereas the S-REIT Leaders Index has a trailing dividend yield of 4.0%, but today you’re probably looking at 5ish% dividend yield.

So personally I prefer picking individual REITs here, but it’s really a personal call.

I’ll be updating the FH REIT watchlist this weekend with the list of REITs that I am keen to buy (with rough target pricing), so do sign up if you are keen.

Given this is not the bottom, you have to pick quality names and position size well, and look to hold for a 2 – 3 year horizon at least.

What could go wrong with investing in REITs now?

I just want to be absolutely clear though.

Even if my analysis above holds true.

This is probably NOT the bottom for REITs.

REITs are unlikely to have a sustained recovery until interest rates start going down meaningfully.

Why is this not the bottom for REITs?

Let’s game out the different ways that economic growth and inflation can play out in the next 12 – 18 months.

They can basically be split as follows:

|

|

Economic Growth |

Inflation |

Interest Rates |

REITs |

|

Scenario 1 |

Strong |

Strong |

More hikes |

Bad |

|

Scenario 2 |

Strong |

Weak |

Cut |

Good |

|

Scenario 3 |

Weak |

Strong |

Hold |

Bad |

|

Scenario 4 |

Weak |

Weak |

Cut |

Average |

Only Scenario 2 is outrightly good for REITs – economic growth stays strong, and inflation miraculously drops to 2%.

This allows the Feds to cut interest rates rapidly, without a recession.

But c’mon, how likely is that to happen?

More likely is Scenario 1 or Scenario 3/4.

Scenario 1 – What market is pricing in

Scenario 1 is basically what is priced into markets today.

Economic growth stays strong, inflation stays strong.

Meaning we only get 2 interest rate cuts in 2024.

This is probably not pretty for REITs, and is roughly what is priced in today.

Which implies upside for REITs if the market is wrong on this.

Scenario 3 / 4 – the more likely outcome?

This is probably the more likely outcome.

Economic growth starts to weaken going forward.

Inflation comes down, but still remains around the 3% range.

In this scenario much will depend on what the Feds do.

And really, the jury is still out on that one.

Powell may talk tough about inflation today – but if the economy weakens, and unemployment ticks up.

He may sing a very different tune in an election year.

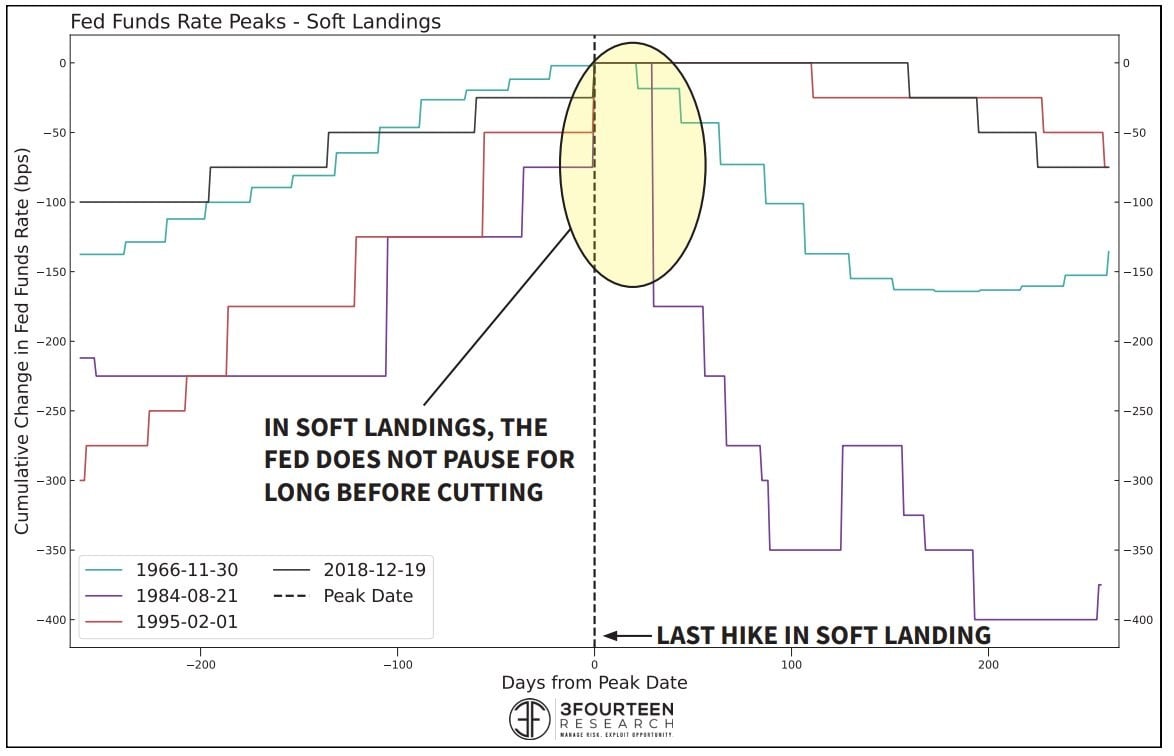

When rate cuts?

Historically speaking, the longest Fed “Pause” over the past 30 years lasted only 12 months.

While the longest “soft landing” pause only lasted 7 months.

Reason being that to truly achieve a “soft landing”, Feds need to act proactively and cut rates at the first sign of slowing growth.

The longer they hold rates high, the higher the chance of a hard landing style recession.

Assuming July’s FOMC was the last rate hike for the cycle, you might need to see rate cuts as early as 1H2024 to truly achieve a soft landing.

Sure, you may argue this cycle is different because of fiscal stimulus, fixed rates, strong consumer etc, and that’s definitely possible.

But history is not on the side of the Feds here.

So… why bother buying REITs now?

Which raises the question – why even bother buying REITs now, given all the uncertainty?

Why not just wait until the Feds start cutting, and then buy then?

I guess 2 points:

- Individual REITs may bottom out before the index as a whole

- I could be completely wrong on my analysis above

So while I don’t think REITs as a whole have bottomed out just yet from a macro perspective.

From a micro perspective – there are a lot of single name REITs that:

- Hold high quality properties

- Trading at prices down 40-50% from highs (some at COVID lows or worse)

- Paying 7-8% dividend yields

- Decent balance sheet

That’s attractive enough that I don’t mind buying some REITs here (while keeping enough cash to buy more down the road).

How much you make when you’re right, vs how much you lose when you’re wrong

I cannot repeat this enough.

In investing, it’s not about being right or wrong.

It’s how much you make when you’re right, vs how much you lose when you’re wrong.

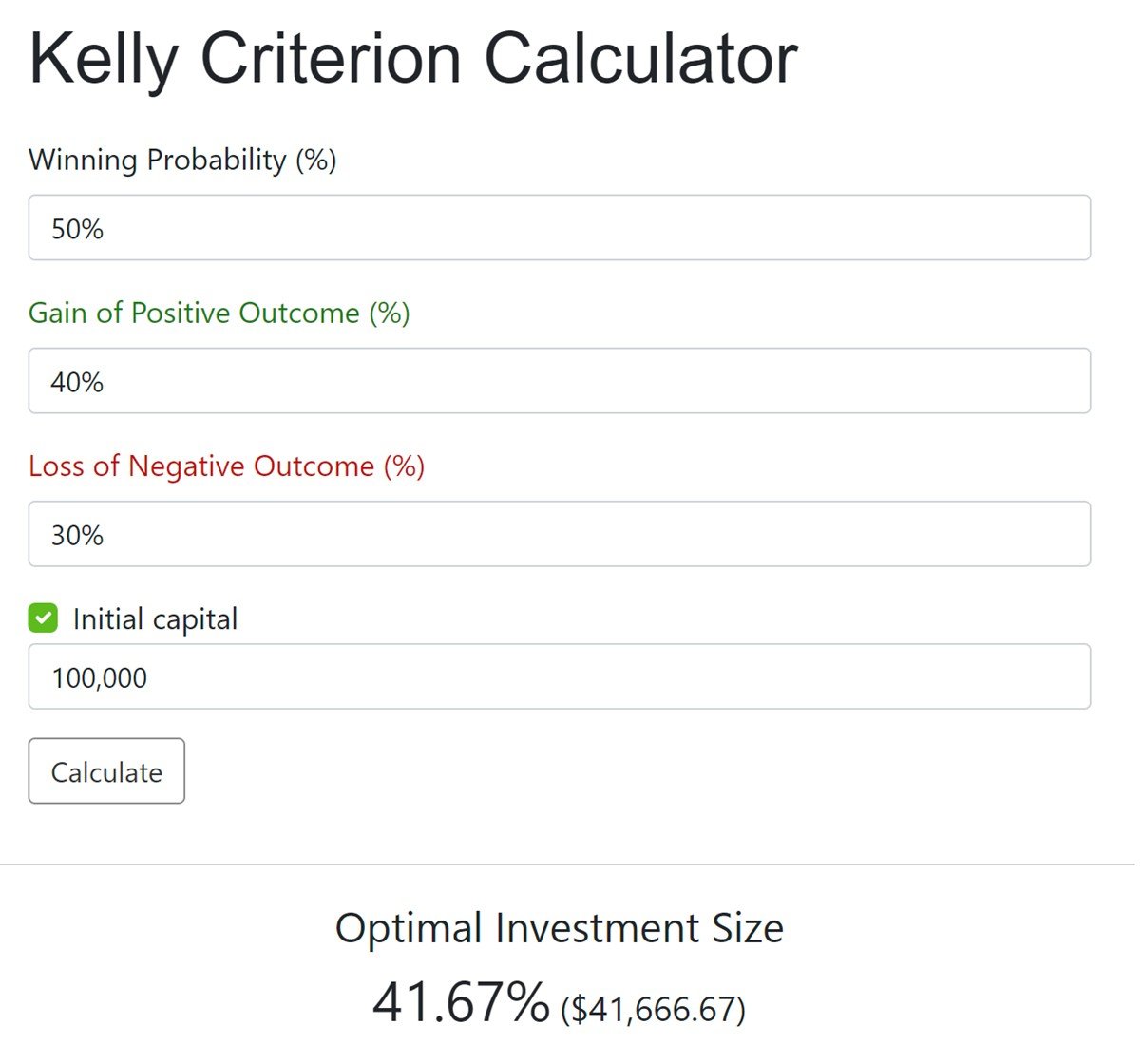

Let’s put it this way:

Assume I have a 50% chance of making money on REIT X, if I buy today and hold for a 3 year timeframe.

If I am right, I make 40% (15% capital gains + 3 years worth of dividend).

If I am wrong, I lose 30% (40-50% capital loss, offset by 3 years dividend).

You’ll probably agree these are very, very conservative numbers.

And Kelly Criterion (a method for sizing investments) says I can go ahead and bet 41% of my portfolio on this.

For obvious reasons the numbers above are approximate, and I would not be putting 41% of my portfolio into REITs today given my analysis above.

But the point is still clear.

This is a favourable trade that can be made, as long as you position size well, and recognise that you could be wrong (so don’t put money you cannot afford to lose).

Closing Thoughts

So this isn’t the bottom, but prices are attractive enough that I am slowly accumulating.

But I can’t stress this enough – focus on quality properties with strong sponsors / balance sheets.

And position size well – you dont know exactly how the next 12 months is going to play out.

With the latest FOMC promising interest rates to stay higher for longer, we’ve had a further sell-off in REITs that are exposing very interesting prices across the board.

I’ve shared above some of the REITs that look interesting to me and that I may add in the months ahead – but I will be refreshing the REIT (and stock) watchlist this weekend for Patreons to take into account latest pricing.

Patreons will also have full access to my positions, and how much of my portfolio I am allocating to REITs.

I will be refreshing the REIT (and stock) watchlist this weekend for Patreons to take into account latest pricing. Do sign up as a Patreon if you are keen.

This article was written on 22 Sep 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

– Get up to USD 800 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 800 free fractional shares.

You just need to:

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Hi FH,

Love your analysis. I don’t think Reits have bottomed out either. In my humble opinion, Reits are likely to see higher funding costs & higher gearing ratios. This will hit their share price if gearing hits above 40% into 2024.

Cuz I suspect rates are gonna be more like table mountain than the matterhorn.

Hope we can discuss ideas, as the Fed’s latest are what I write about too at https://pugsandpennies.substack.com

Altho obv, nowhere as committed as you are. But investing from a gal’s POV is sometimes a different angle! I think. Lol.

Great blog! Love the sharing!

Love to discuss further ideas, feel free to reach out any time.

On REITs – short term I agree with you. But now that everyone is expecting a soft landing and rates to stay higher for longer. I can’t help but think the risk for rates is tilted to the downside.

When and how fast it breaks is the million dollar question, but if I were a betting horse (and I am), I would take the under on this trade.

Thanks FH! Really glad to hear that!

You at Financial Horse and the MileLion are my go-to financial reads. Lol… lion and horse. Just really good & witty.

It’s been great reading FH through the financial volatility of the past few years. Also really glad I went with Powell, not playground reviews. Tho… never say never.

To my mind retail and office REITs and are best avoided, even in Singapore. The tend to have shorter WALEs and are more vulnerable to economic conditions than industrial of healthcare REITs. That still leaves quite a few good choices. My own top picks (no particular order) are:

Mapletree Industrial REIT

Keppel DC REIT

CapitaLand Ascendas REIT

AIMS APAC REIT

Parkway Healthcare REIT

The valuations of these five (well run) companies are all depressed (compared to historical levels) at the moment, and the yields on offer range from 4% to just over 7%.

The chances of a meaningful drop in interest rates within the next 18 months seems remote. If it does happen and the borrowing costs of these REITs falls a bit we could see a nice bit of capital appreciation, but I wouldn’t bet the farm on it.

Interesting – appreciate the sharing.

I suppose that is why the industrial names (esp thoe you cited) trade at a premium valuation vs retail/office.

Great article horse, well balanced with different perspectives. I get the feeling you’re in the soft landing camp more than the hard landing camp?

It’s funny because every day that goes by without a recession more people are in the soft landing camp. But the way I see it, the longer the Feds stay high, the higher the probability of a hard landing.

For what it’s worth, I’m in the hard landing camp, but I’m not dogmatic enough to insist on my view.

The data over the next 6 months will tell us who is right, and really it’s always about how much you make when you’re right, vs how much you lose when you’re wrong.

If I’m wrong, I’ll just take the loss and move on.

Dear FH

Thanks for this

You might recall Oct 22, when I posted that I invested in SG REITS taking the risk

Although prices are slightly lower by 4-5% for well run REITS in Sep this year as compared to then, the dividends made up for this

I am slowly accumulating and averaging down again this month and will continue to keep doing this at dips

With due respect, no one can predict the Fed and subsequently the bottom

The fed will blink faster than what they posture and any credit event and or signs of sharp slowdown will weaken their resolve and they will cut

It is very difficult to invest very big amounts to make meaningful returns waiting for “ the bottom” – for me the best strategy is to accumulate gradually and cash in dividends and wait for this cycle to turn

Possibly after 2-3 years, I will make a double digit annualised return!

Regards

Garudadri

Hi Garudadri,

Appreciate the sharing as always.

Fair enough – if you buy when great real estate when prices are attractive, it will probably turn out to be a great investment in the longer run!

Good morning FH,

I am no expert of Sg, that’s why I read you.

I believe the long term interest rates go up for many years to come until some kind of gold backing will stop it (see Alasdair Macleod). This should mean price pressure for everything beside bread and water (at least in real terms).

In history were situations in which real estate went worthless. Doug Casey bought his HK PH, when energy was missing and the elevator not running.

The advantage for Sg is the island – space is limited which makes it more stable. But commercial real estate is a sure troublemaker and the Sg REITS invested overseas as well. The rents people pay in Sg are very high and Forest City is so close.

And what is with debt in these REITS, do they have to refinance?

And the many AirBNBs are expected to flood the markets – price pressure in many places will be contagious. Could Sg decouple herself from that?

So from my Latinamerica point of view I would not touch them.

I rent a somewhat run-down ex-luxury 400m2 ap with view over town for 1k USD. Venezuela had it’s time and is possibly bottoming out. Some came back home and bought, but lots of vacancy anyway. No sale signs – many owners gave already up.

This is possible everywhere. People cannot imagine… and they do not read history.

Pistol to my head: I would prefer Sg REITS which are free of western assets and very well financed.

Another view FH, I am sure you don’t mind.

First of all, forget about Forest City. Depending on the day of the week and time of day it can often take hours to cross the border (either at Tuas or Woodlands). There’s almost no public transport there either, so property looks destined to become a stranded asset unless something changes.

Secondly, there is no AirBnB in Singapore as short-term residential letting is illegal. The authorities have actually prosecuted and jailed several people for breaking these local laws.

Housing supply in Singapore seems likely to remain quite tightly controlled for the forseeable future. Maybe too tight, but it is what it is.

Fantastic points, and appreciate very much the different point of view.

I agree with Jonathan that the local real estate market in Singapore has certain nuances.

A few points I would make:

1. Yes, that’s the story with Forest City being so close. And yet demand for SG real estate remains high, while demand for Forest City is non-existent. Why is that the case?

Just like with China, you can build real estate close enough to key population centers, but it doesn’t necessarily mean people will want to buy them.

And here Malaysia is a very different country vs Singapore!

2. Singapore does not allow short term rentals of less than 3 months on Airbnb. So supply side it is very regulated, unlike other countries where Airbnb is a problem.

In time to come the supply issue will balance out, but I dont think we’ll see a flood of supply crashing property prices.

That said – agree that between the two, I would favour SG REITs focussing exclusively on SG real estate. Would expect SG real estate to weather the storm better than other countries.

If real estate prices correct though, then the value proposition might be very different.