I’ve been getting quite a few questions about holding USD for yield recently.

As you all know, US interest rates sit at 5.5%.

Which means that you can just park your USD into 6 month T-Bills.

And earn that 5.5% yield completely risk free.

For what it’s worth, there actually isn’t a catch, you can literally get 5.5% risk free on USD these days because that’s where Fed Funds Rate sit.

But there’s some nuance on how to actually pull this off as a Singapore investor (and avoid withholding tax), so I wanted to discuss it further.

What are the options for USD yield? Very, very juicy yield…

I’ve set out the yields for the various SGD and USD instruments below.

You can see how across the board, USD just offers a higher yield even after the recent drop in interest rates.

|

Instrument |

Currency (FX) |

Risk Level |

Yield |

|

6-month T-Bills |

SGD |

No risk |

3.8% |

|

10 year Singapore Bond |

SGD |

No risk |

3.0% |

|

S-REITs (CICT or Ascendas REIT) |

SGD |

Low – Medium |

5.5% |

|

US 6 month T-Bills |

USD |

No risk (USD FX risk) |

5.4% |

|

US 2 year Treasuries |

USD |

No risk (USD FX risk) |

4.7% |

|

US 10 year Treasuries |

USD |

No risk (USD FX risk) |

4.3% |

US Government Bonds are backed by the US Government and risk-free

Now, US government bonds are backed by the full strength of the US government (and the most powerful military in the world).

This makes the US government bond as close to risk free as risk free gets in this world.

Don’t ignore USD/SGD FX Risk

That said.

If you’re a Singapore investor living in Singapore, and spending in SGD.

The biggest risk is of course USD/SGD FX risk.

The 5.5% USD yield is risk free, but the USD/SGD exchange rate is by no means guaranteed.

And in my view – this is the biggest catch of holding USD for the higher yield today.

Is USD FX Risk worth worrying about?

I’ve extracted the 15 year chart of the USD/SGD pair below.

In 2009, in the peak of the Lehman crisis, the USD went as high as 1.5 against the SGD.

After Fed money printing, it dropped as low as 1.2.

And ever since 2015 (the end of QE3), the USD has traded in a range of 1.30 – 1.44 against the USD.

Assuming this recent range holds, that’s about a 8% decline peak to trough, or about 1.5 years worth or dividends if you get the move wrong.

But will USD depreciate out of this range – below 1.3 vs SGD?

Not an easy answer.

My personal view, is that the only long term sustainable solution for the US deficit is for the Federal Reserve to resume buying of US Treasuries (ie. Resumption of QE, or a form of yield curve control).

I don’t think we get there without a big crisis, but I think we will get there eventually.

And when that move comes, that could spark a big depreciation in the USD.

So personal view – USD may remain rangebound vs SGD in the short term, but mid to longer term you want to be very careful about USD depreciation.

This “trick” is only worth doing if you know what you want to do with the USD

Because of that, I would say it’s not worth converting SGD to USD just for the higher yield.

This “trick” is only worth doing if you:

- Already have some USD lying around

- Need to use USD in the years ahead (for eg. To spend, or to buy US stocks)

How to earn 5.5% yield on USD?

Let’s dive into the actual mechanics.

At a high level, there are 3 ways of getting a higher yield on USD.

Ranked in terms of difficulty (easy to hard):

- USD Fixed Deposit (or brokers like IBKR)

- US Treasuries (direct or ETF)

- Money Market Funds

Buy US Treasuries or T-Bills (Moderate – Hard Difficulty)

Let’s start with Option 2 – buy US Treasuries / T-Bills.

There are 2 ways of doing this:

- Buy the actual US Treasury / T-Bill

- Buy an ETF

A quick note on terminology.

Just like Singapore government bonds – with US government bonds anything up to 1 year maturity is called T-Bills, anything with a maturity more than 10 years is called Treasuries.

Buy the actual US Treasury / T-Bill

The exact process will vary depending on your broker.

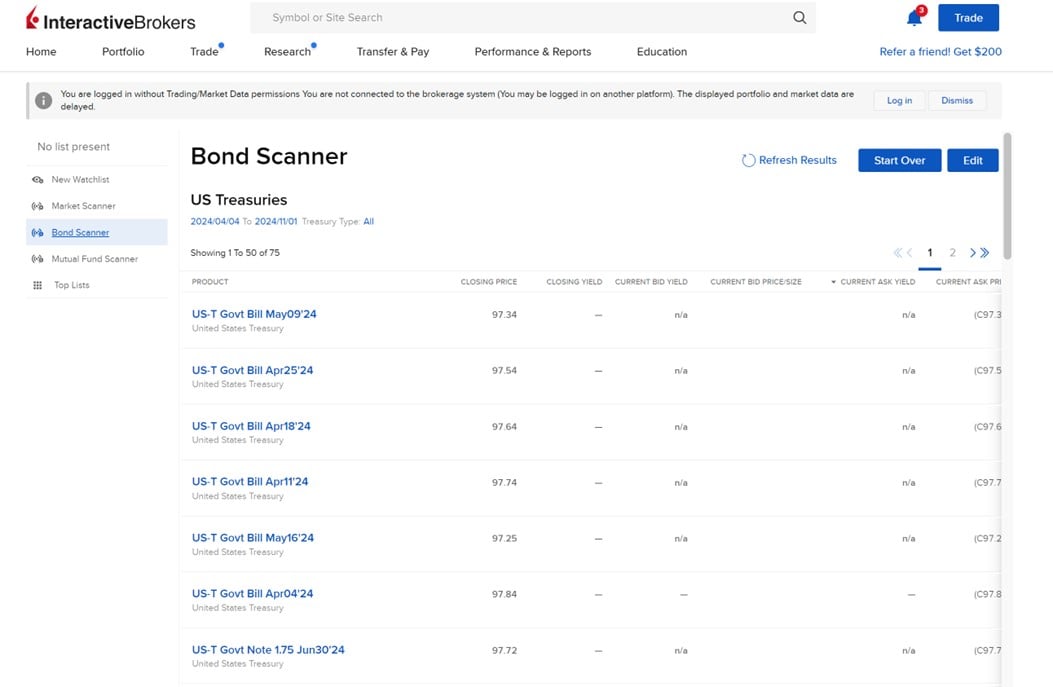

If you’re an , you can go to Bond Scanner and do a search for the bonds that you want:

And once you find the bond that you want, you just place a buy order.

So for example the T-Bill expiring in April 2024 will pay a 5.466% yield, which is very close to market yields today.

Does the “yield” trigger US withholding tax?

The problem with buying US government bonds directly as a Singapore investor is how withholding tax is handled.

Withholding tax is 30% on US dividends, so it’s a very big deal if you get hit.

Do you pay withholding tax on US T-Bills?

T-Bills (up to 1 year maturity) are straightforward.

T-Bills are issued at a discount, and do not pay a coupon (same as Singapore T-Bills).

So there is no “dividend”, and consequently no withholding tax to worry about for T-Bills.

The 5.46% yield is money in your pocket, no tricks there.

What about US Treasuries?

It gets a bit more tricky with US Treasuries though.

Now officially, US Treasuries are exempt from US withholding tax. Here’s the disclosure from Charles Schwab (emphasis mine):

Interest: Interest earned on bonds and commercial paper issued by U.S. companies, by the U.S. Treasury and by U.S. government agencies is generally exempt from U.S. tax withholding if the interest qualifies as portfolio interest and the original issue date of any such debt instrument is after July 18, 1984. For debt instruments issued after March 18, 2012, portfolio interest does not include interest paid on debt that is not in registered form, except for interest paid on foreign-targeted registered debt instruments issued before January 1, 2016 (see IRS Publication 515 for more information). However, even though generally no U.S. tax is to be withheld on interest earned on bonds issued by U.S. companies, the U.S. Treasury or U.S. government agencies, the interest earned on such U.S. securities must be reported to the IRS by us on our annual report on Form 1042-S as U.S. source income. See the “U.S. Tax Reporting” section of this document.

But…

The problem though is that most brokers (like IBKR) will deduct a 30% withholding tax on dividend.

Which is then refunded in the first 6 weeks of the following year.

So US Treasuries are not subject to withholding tax, but 30% of the dividend is delayed and you only get it the next year.

The exact procedure depends on your broker, so do check with your broker to be sure.

But this is the practice for .

Buy an Irish domiciled ETF instead?

There is a way to get around this though.

For investors who don’t want to bother with all the withholding tax mechanics, or finding individual Treasuries / T-Bills to buy.

You can just buy an Irish domiciled Treasury ETF, and let the fund manager handle all of it for you.

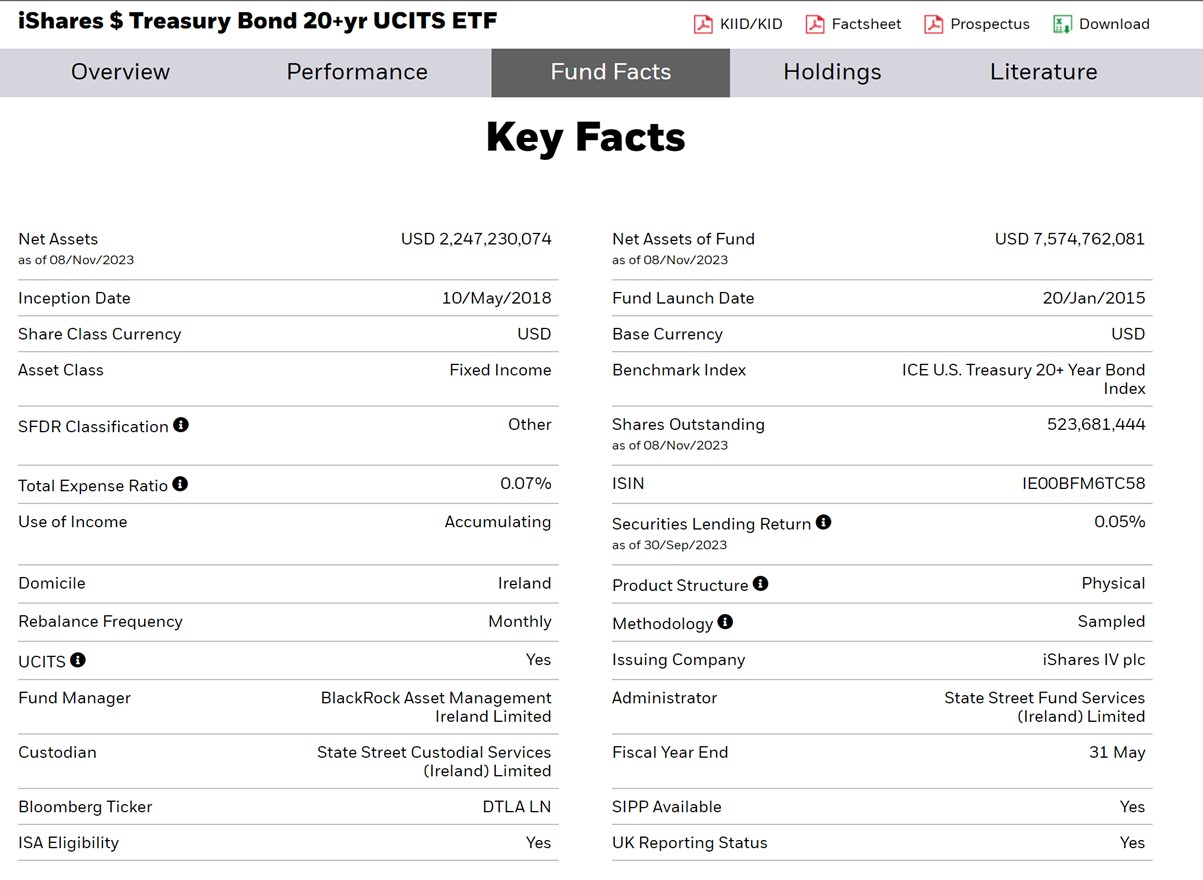

iShares $ Treasury Bond 20+yr UCITS ETF

The DTLA, or the iShares $ Treasury Bond 20+yr UCITS ETF.

This ETF holds primarily 20 year+ Treasuries, which is the Irish version of TLT.

Note that when you buy such long duration Treasuries you are implicitly making a bet on where interest rates will go, so do be careful with instruments like that.

There is both a distribution (yield paid out) and accumulating (yield is reinvested) version, depending on which you prefer.

But with long term US Treasuries (>10 years duration), you have to understand you are taking on real duration risk.

So I would say don’t touch US Treasuries unless you know what you are doing, and you are prepared to take a position on where interest rates will go in the years ahead.

Here’s the price of the US Treasury ETF since 2020 – it’s down 45% just due to interest rate increase alone.

So this is a good way to bet on a reversal in interest rates, but if interest rates march up, you could see further capital losses.

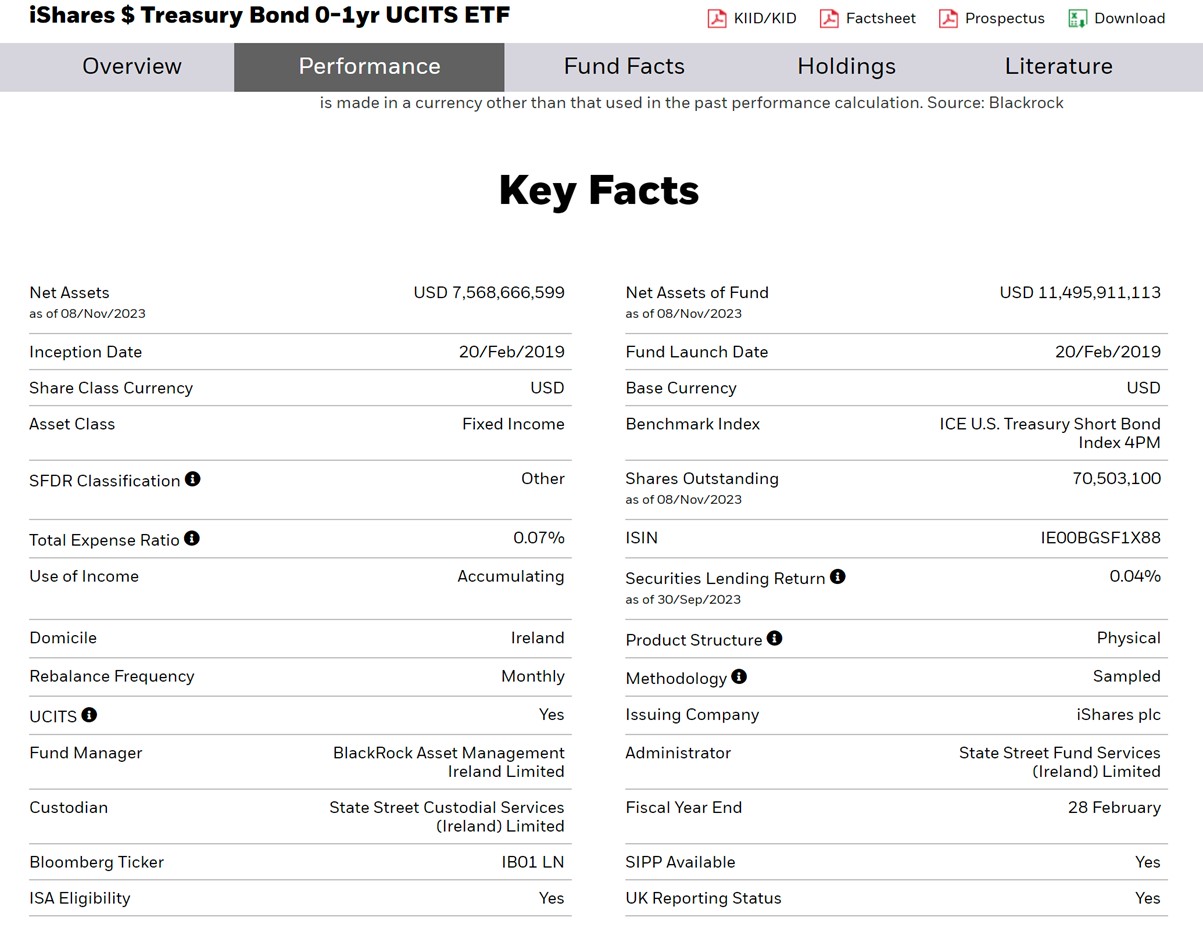

Short Term Treasury ETF – iShares $ Treasury Bond 0-1yr UCITS ETF

If you want to do the same with T-Bills, the equivalent is the iShares $ Treasury Bond 0-1yr UCITS ETF.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

USD Fixed Deposit (Easiest)

If you don’t want to bother with all the complexity above.

Then an easier option may be to just place the USD into a fixed deposit account with a local bank.

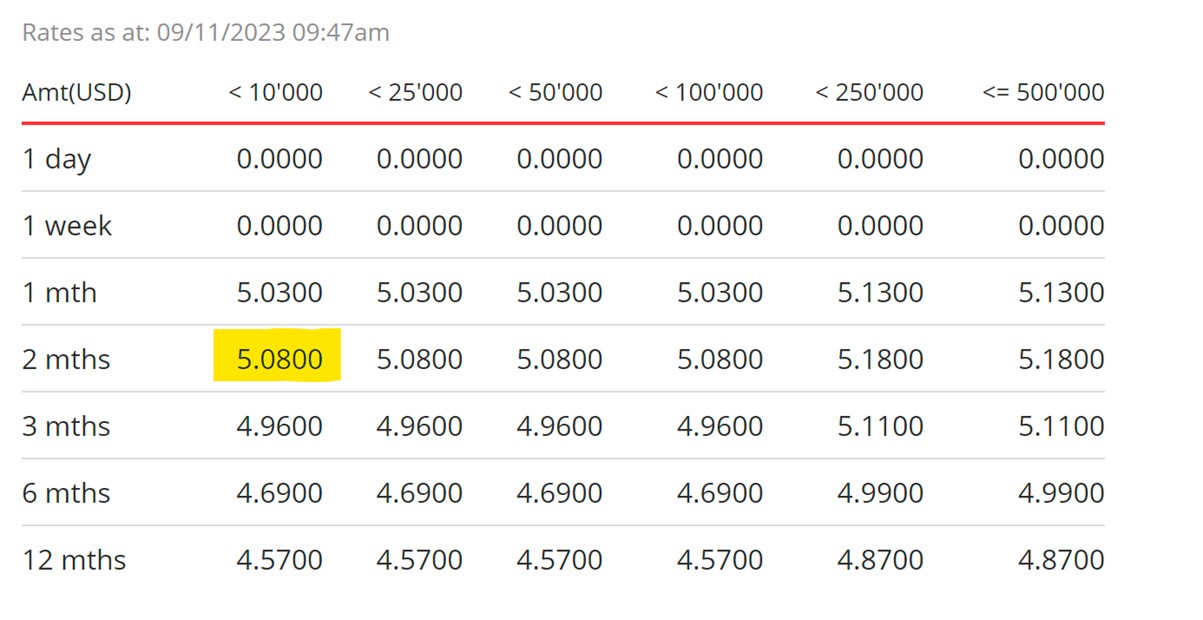

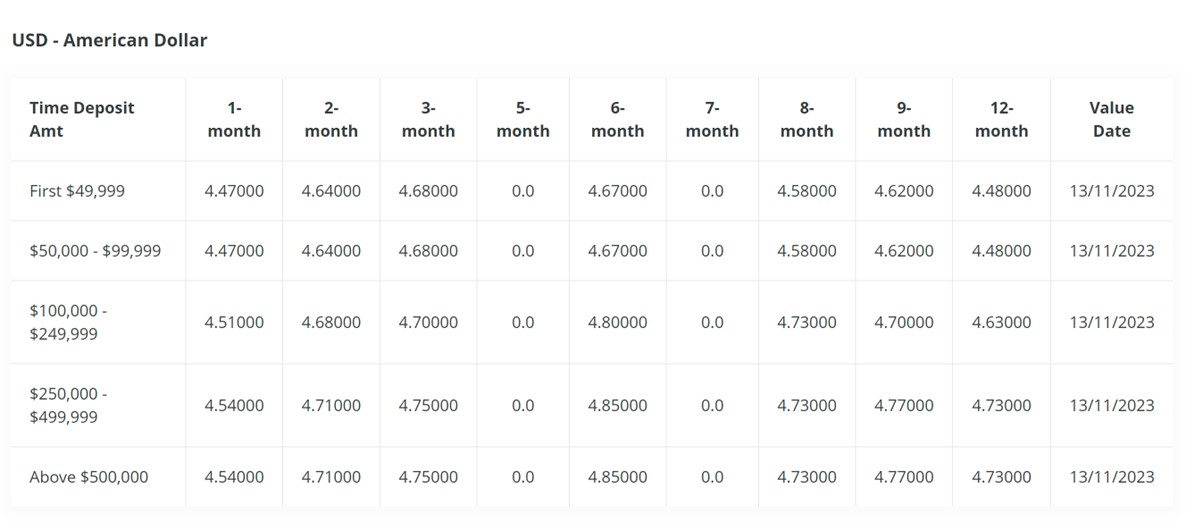

For example you can just deposit USD into a multi-currency account with DBS Bank.

And DBS bank will pay you 5.08% on your USD, with a 2 month lockup:

It’s literally as simple as that, doesn’t take more than a few minutes (can be done online).

You can also use OCBC or UOB bank, but based on my checks DBS offers the best interest rates.

OCBC offers 4.8% for 6-months (minimum $100,000):

While UOB offers 4.85% for 3 months (below $50,000):

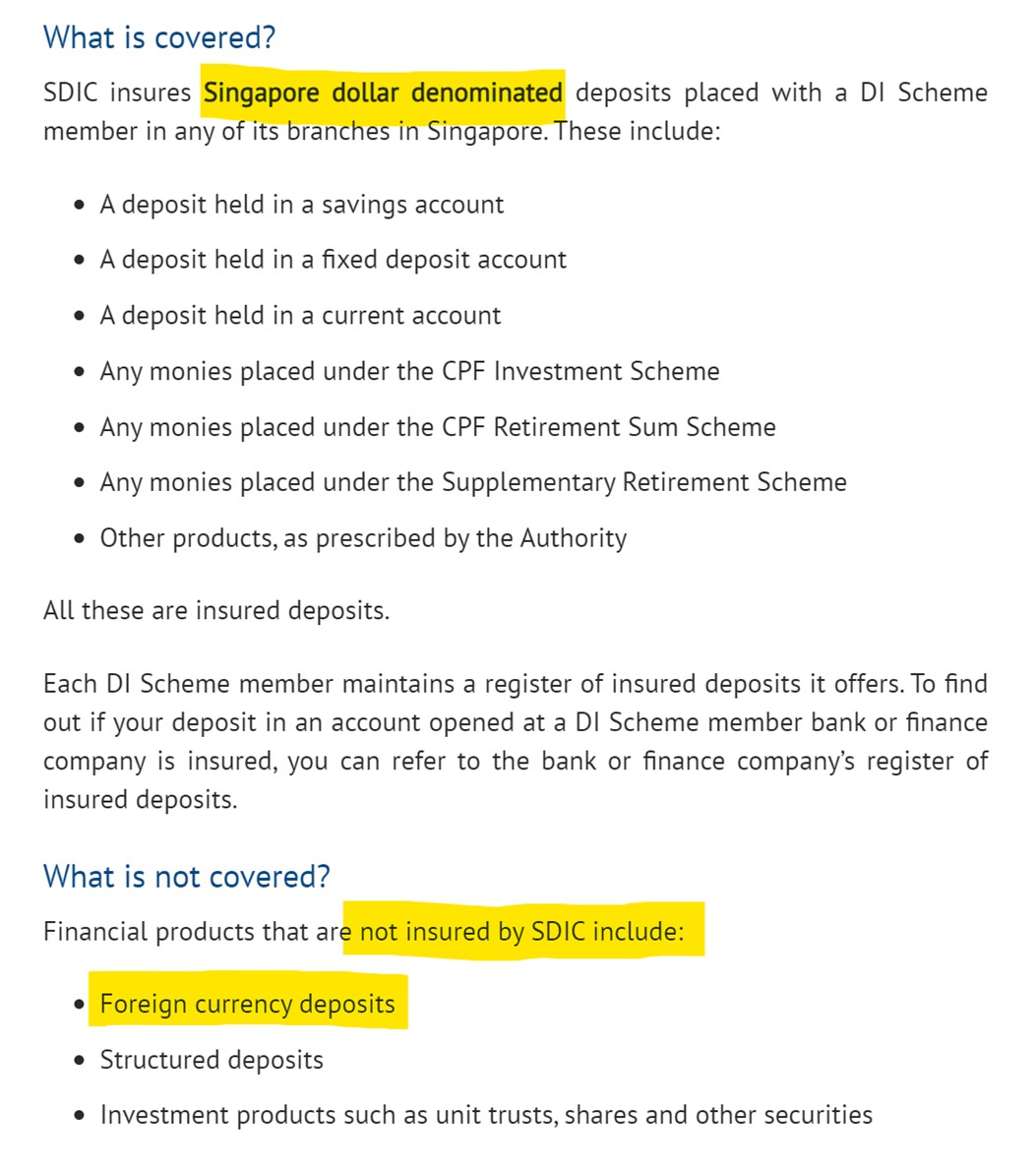

Is this risk-free? NOT SDIC insured

Note that USD deposits with a Singapore bank are not covered by SDIC insurance.

SDIC only covers SGD deposits.

This is made very clear on the SDIC website, which I extract below:

So you do want to be careful with the bank you choose if you do this.

But as long as you stick to one of the 3 local banks (DBS, UOB, OCBC), the risk should be low.

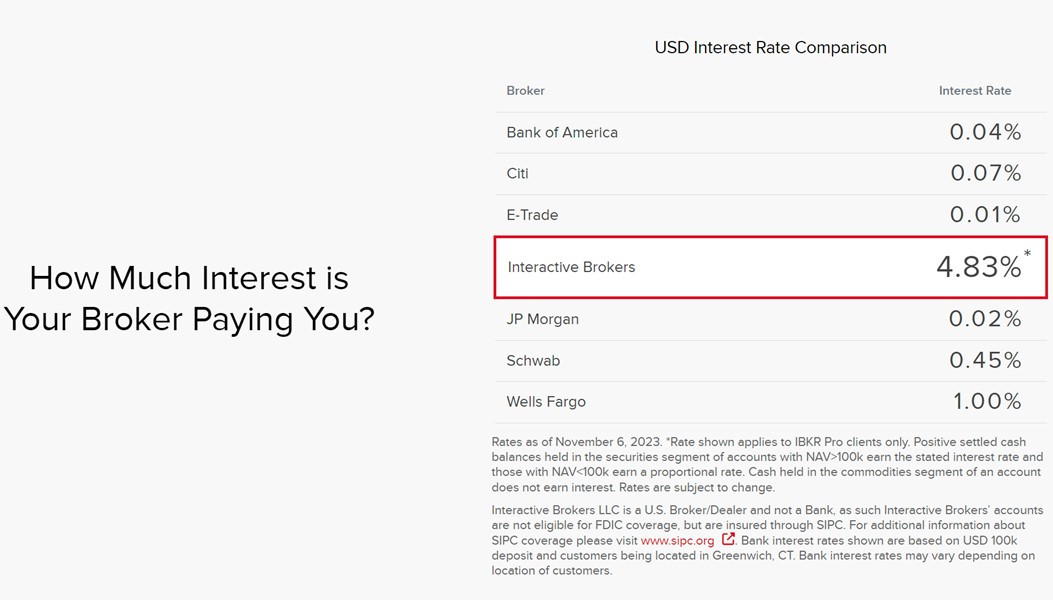

pays 4.83% on USD cash balances above $10,000

Alternatively, if you have an .

You can just park the USD cash with IBKR.

And any USD balances above $10,000 earn 4.83% just sitting there.

Credit risk with this option is the risk of going under, which while probably low, is not zero.

So if you want to earn some good yield on USD cash for very little risk, the easy options are above.

USD Money Market Fund?

The last option is to use a USD money market fund.

The problem with this approach is that you need to be careful which money market fund you use, and what kind of instruments the money market fund invests in.

Some money market funds are not subject to withholding tax for Singapore investors, while some are.

And based on the instruments the money market fund invests in, you may be exposed to varying levels of risk.

It’s definitely a viable option, just that the universe of money market funds is so big that it is not possible to generalise.

If you get it right, yields can go into the 5%+ range, above USD bank fixed deposits.

How do I do it? Yield on my USD cash?

For what it’s worth, I have a fair bit of USD cash in a DBS multi-currency account.

And I’ve simply been rolling them over every few months at the 5.08% offered by DBS.

No doubt I can get a higher yield by buying US T-Bills, but I guess I’m lazy like that.

I do hold long term US Treasuries as a bet on interest rate movements though.

I have been playing this primarily via call options, but at a certain point in this cycle if the trend starts to move.

I may start buying a Treasury ETF using USD cash as well.

How best to earn USD yield? For retail investors?

But really, there’s no right or wrong here.

The options available when it comes to USD yield is absolutely massive.

This is the biggest and deepest funding market in the world, and the options available for USD will dwarf anything available for SGD.

If you’re a retail investor who has some spare USD lying around and want a higher yield – I would say the USD fixed deposit or options are the easiest.

If you’re more sophisticated, you can look into buying US T-Bills.

But with long term US Treasuries (>10 years duration), you have to understand you are taking on real duration risk.

So I would say don’t touch US Treasuries unless you know what you are doing, and you are prepared to take a position on where interest rates will go in the years ahead (if interest rates go up, you could be sitting on pretty hefty capital losses).

So there you have it!

How to earn 5.5% yield on USD, risk free.

Where are you parking your USD right now?

Love to hear what you think!

This article was written on 1 Dec 2023 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

– Get up to USD 5000 worth of shares (Best promo of 2023)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now (Best Promo of 2023)

You can get up to USD 5000 free shares.

You just need to:

- Fund any amount (get 5 free shares)

- Hold for 30 days (get 5 free shares)

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.