I get a lot of questions on how to invest for dividend income.

Many investors aim to build an investment portfolio that generates stable monthly income.

So let’s explore how we can achieve this goal.

With a $1 million portfolio, how to earn $4,000 income a month?

Broadly speaking, there’s 2 main ways you can do it:

- Managed solution

- Do it yourself (DIY)

Syfe recently unveiled Syfe Income+, which would come under Option 1.

Regular monthly payout is 4.0 – 6.0% per annum.

Assuming one puts $1 million in, you could be looking at around $4,000 – $5,000 passive income each month.

How safe is this though?

Is this a good option to consider for income investing?

And how does it compare to DIY investing?

This article was sponsored by Syfe. All views and opinions expressed here are from Financial Horse.

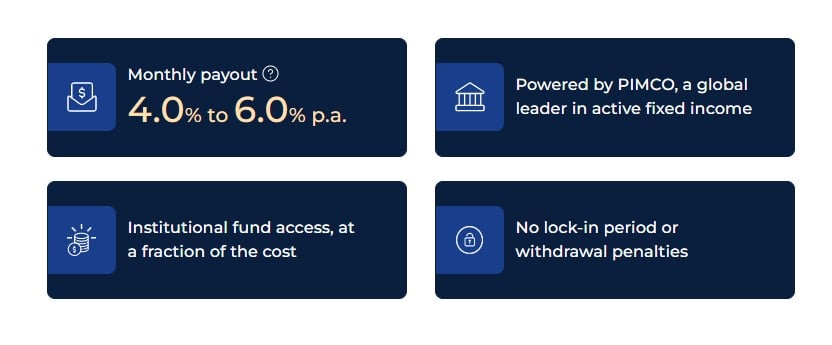

Syfe Income+ Key Features

I set out the key features of Syfe Income+ below:

- Regular monthly payouts at 4.0 – 6.0% p.a.

- Option to deposit to bank (free of charge) or reinvest

- Institutional grade solution (in partnership with PIMCO)

- High quality assets: Investment grade, high yield fixed income assets

- Lower fees for institutional funds, and 100% trailer fee rebates on retail funds

- SGD share class, hedged against FX risks

- Includes Semi Annual Rebalancing (you can choose to opt-in or out)

- No lock-ins or holding periods

- Flexibility to deposit or withdraw any time

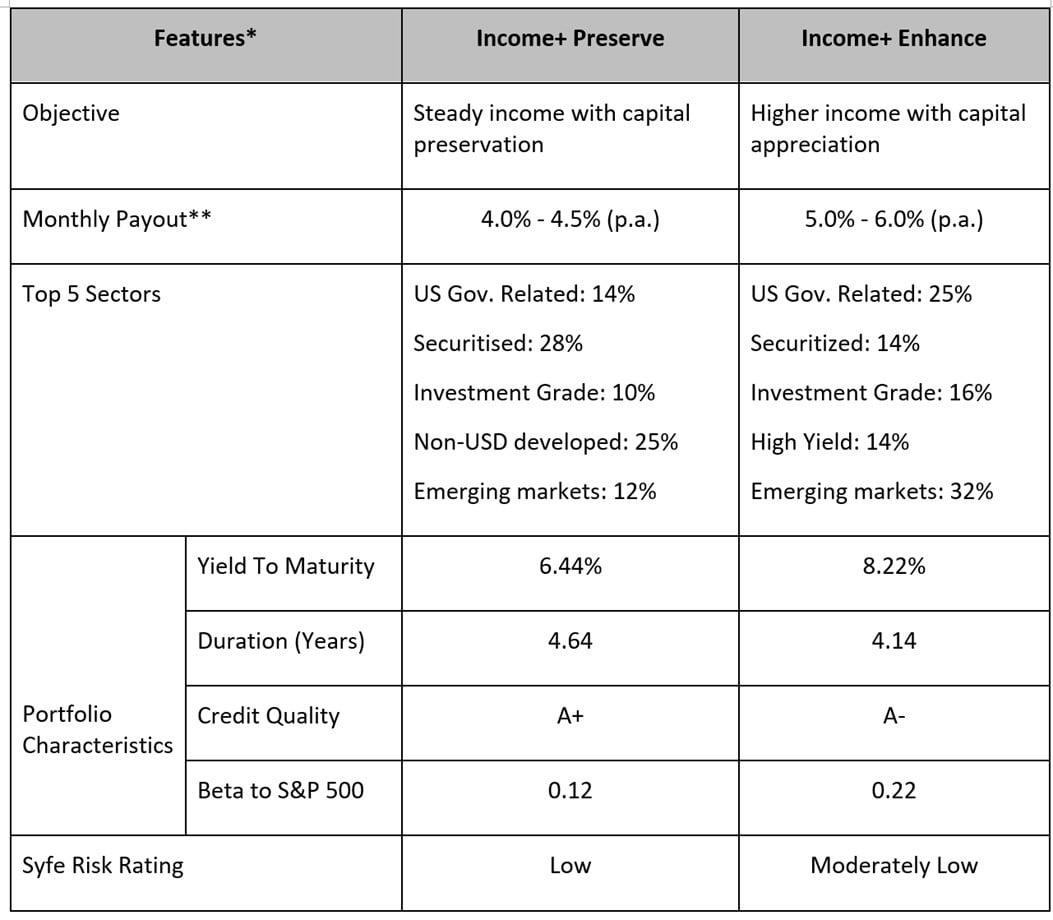

Syfe Income+ Preserve & Enhance – Low, and Moderate Risk

There are 2 different portfolios.

A lower risk Syfe Income+ Preserve, and a moderate risk Syfe Income+ Enhance.

You can see the high level details below:

Here’s the same in table form:

|

Features* |

Income+ Preserve |

Income+ Enhance |

|

|

Objective |

Steady income with capital preservation |

Higher income with capital appreciation |

|

|

Monthly Payout** |

4.0% – 4.5% (p.a.) |

5.0% – 6.0% (p.a.) |

|

|

Top 5 Sectors |

US Gov. Related: 14% Securitised: 28% Investment Grade: 10% Non-USD developed: 25% Emerging markets: 12% |

US Gov. Related: 25% Securitized: 14% Investment Grade: 16% High Yield: 14% Emerging markets: 32% |

|

|

Portfolio Characteristics |

Yield To Maturity |

6.44% |

8.22% |

|

Duration (Years) |

4.64 |

4.14 |

|

|

Credit Quality |

A+ |

A- |

|

|

Beta to S&P 500 |

0.12 |

0.22 |

|

|

Syfe Risk Rating |

Low |

Moderately Low |

|

Source: Syfe, PIMCO, fund factsheets. As of 28 Feb 2023. Statistics are based on the weighted fund allocation within each model portfolio.

* Refer to the Definitions section to understand these terms.

** Monthly payout ranges are computed based on the weighted average of the annualised historical distribution amount or dividend/distribution yield of the constituent funds from the latest three months. The upper and lower bounds of the range are rounded up to the higher 0.5% and down to the lower 0.5% respectively. The dividend amount or dividend rate/yield of the constituent funds is not guaranteed. Past distributions are not necessarily indicative of future trends, which may be lower. A positive monthly payout or distribution yield does not imply a positive return.

What I like about the Syfe Income+ Portfolio

Let me start by sharing what I like about the Syfe Income+ Portfolio.

Syfe Income+ Diversified Fixed Income Portfolio (not easy for retail investors to get such exposure)

At a high level, the Syfe Income+ Portfolio is basically a diversified bond portfolio that is hedged back to SGD (to remove Forex risk).

I like this part.

I’ve always said that as a retail investor in Singapore you will never be able to build a diversified bond portfolio by yourself.

You need to be an accredited investor to even access most of these bonds, and even then the minimum subscription amount of $250,000 is too large for most investors to diversify meaningfully.

Syfe Income+ solves that, by giving you exposure to a broadly diversified fixed income portion (via PIMCO bond funds), at a lower price point.

Even if you access these bonds through retail fund vehicles as a retail investor, you typically end up paying very high fees of 1.5% and above.

Whereas, Syfe Income+ invests primarily in the institutional share class, which reduces the fund level fees significantly up to 60%.

Syfe Income+ Simple and Fuss free

Syfe Income+ is simple and fuss free.

These are professionally managed funds, with semi-annual rebalancing.

Which means they are pretty much fuss free.

If you build your own portfolio via a mix of T-Bills, retail bonds, bond funds etc, you need to spend a fair bit of time researching and buying them.

With Syfe Income+, all that is outsourced to a professional manager who handles all the work for you.

PIMCO is one of the biggest names in fixed income too (founded by Bill Gross, the so-called “Bond-King”).

On top of that, Syfe offers a semi-annual reoptimisation process to adapt the portfolio to market conditions.

Syfe uses forward-looking views from PIMCO, based on credit spreads, yields, economics forums, as well as Syfe’s proprietary optimization process to adjust the portfolio according to market conditions.

This semi-annual reoptimisation is entirely optional, so you can choose whether you want to accept or not.

There is also constant rebalancing at the bond level by PIMCO within the individual constituent funds of the portfolios.

For those who don’t like to spend too much time managing their money, this could be a good option.

What is the default risk? Syfe Income+ vs T-Bills

Okay let’s deal with the elephant in the room.

A 4.0% – 6.0% p.a. income payout is nice and all.

But in an era where you can get up to 4% risk free on T-Bills, how much extra risk are you taking on with this Syfe Income+ Portfolio?

How does Syfe Income+ compare to T-Bills?

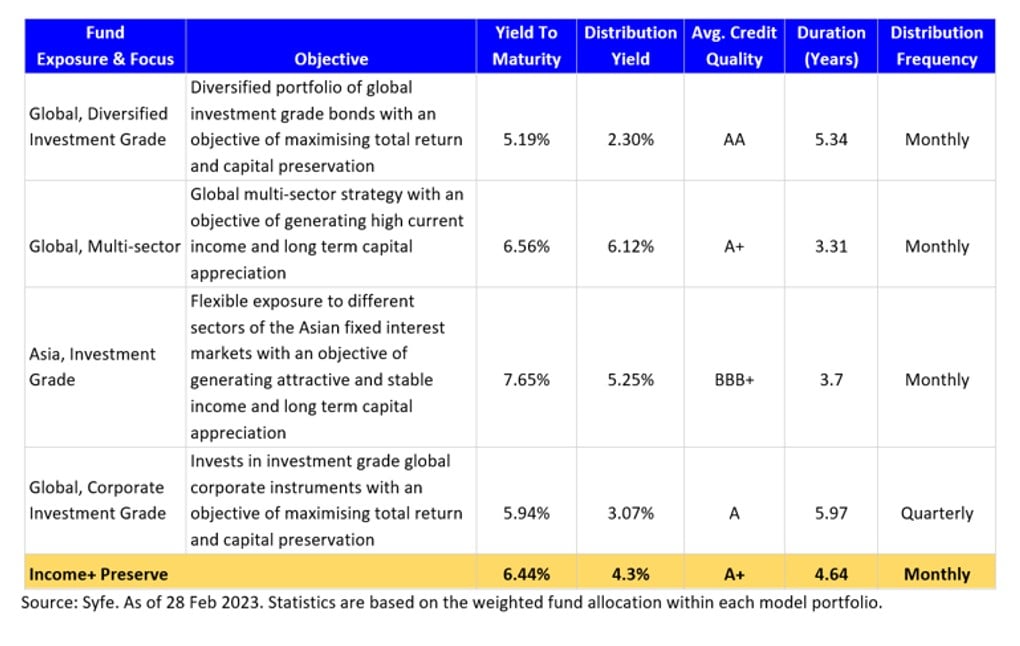

Syfe Income+ Preserve

Let’s look at the lower risk Syfe Income+ Preserve.

It’s made up with a mix of 4 different bond funds.

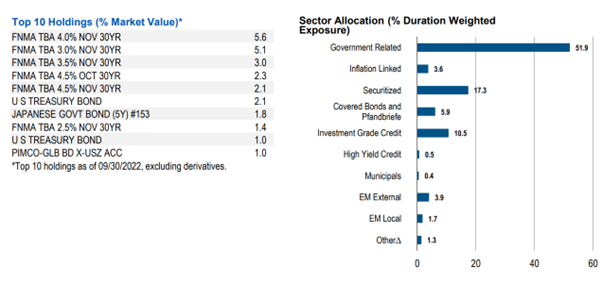

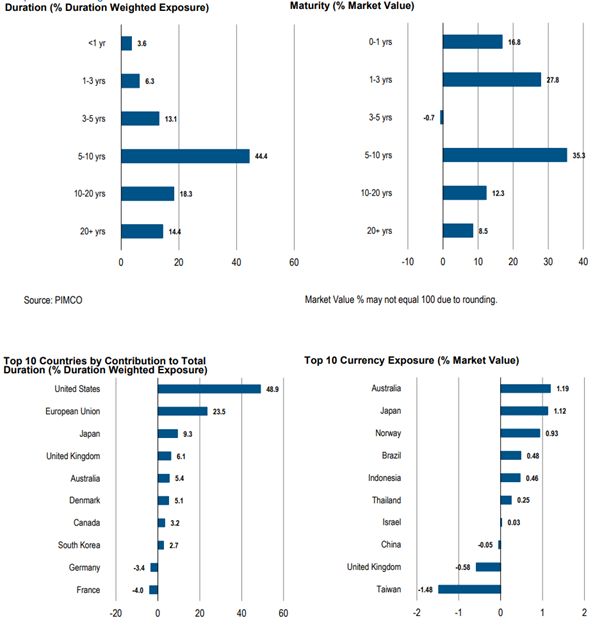

I extract the Top 5 sector allocations below for reference:

- US Gov. Related 14%

- Securitised 28%

- Investment Grade 10%

- Non-USD developed 25%

- Emerging markets 12%

For reference, here’s what goes into one of the underlying Pimco bond funds (you can access the full list after logging into your Syfe account).

Source: Pimco Fact Sheet, data accurate as of 31 January 2023

Source: Pimco Fact Sheet, data accurate as of 31 January 2023

What is the default risk of Syfe Income+ Preserve?

Basically, you’re investing in a mix of US Treasuries, mortgage-backed securities, and investment grade corporate credit.

Broadly speaking, I’m inclined to agree with Syfe that this is intended as a lower risk, lower return kind of portfolio.

Default risk should be low, but of course not zero.

Not to mention that a big part of the safety comes from diversification.

I know of many investors who loss a significant chunk of money because they had bought Credit Suisse’s AT1 bonds directly from their private banker.

With a more diversified approach like Syfe Income+, you get to diversify away the single issuer risk, and the risk you’re taking on is more of a macro, economy wide risk.

Syfe Income+ has one notable advantage over T-Bills – much longer duration

That being said, Syfe Income+ has one notable advantage over T-Bills.

It is the duration.

With T-Bills you are buying 6 month T-Bills.

This means you lock in the yield for 6 months only.

What interest rate you get after the T-Bills mature, is wholly dependent on where interest rates are in 6 months.

If interest rates are cut significantly in 6 months, you may not be able to maintain the 4% yield.

This is a pretty big risk, given the uncertainty over where interest rates will go the next 12 months.

Syfe Income+ Preserve locks in the interest rates for much longer

The difference with Syfe Income+ Preserve, is that the average duration is longer.

You’re looking at about 3 – 4 years duration across the board.

Which means that even if interest rates drop drastically, you are still protected because the yields are already locked in at the price you bought.

You still get to enjoy your 4.0 – 6.0% yield, as long as the underlying bonds don’t default.

In fact you may even see capital gains because bond prices go up when yields go down.

This is a pretty big advantage over T-Bills, especially if you are investing for the mid to longer term.

What concerns me about Syfe Income+ (potential risks)

There is a flip side to this though.

Duration Risk (this is a risk faced by all bond funds)

Because the average duration is higher than say T-Bills.

If interest rates go up, there is a chance of capital loss as bond prices go down.

This is called duration risk.

To be fair, this is not unique to Syfe Income+.

All long term bonds or bond funds have this problem (it was what got Silicon Valley Bank undone in their hold to maturity portfolio if you recall).

If you plan on holding the bonds long term this doesn’t affect you too much because you will still get the income payout.

Where does the cash go when the underlying bonds mature?

Sidenote here that when the bond coupons (dividends) are paid, you can choose to receive the monthly payouts (1) in cash or (2) to reinvest in the fund.

When the underlying bonds mature however, they are automatically reinvested by the fund manager into new bonds.

So this is unlike T-Bills where you can choose what you want to do with the maturing funds.

Again, this is not unique to Syfe Income+, and a feature of most other bond funds in the market.

But do note because this is a big difference from something like a Singapore Savings Bonds or Astrea Bonds where you can get the money back on maturity.

With Syfe Income+, the only way to get the money back is to sell the funds at the market price (this will be done by Syfe when you submit a redemption request).

However, the benefit from this approach is diversification, in that you are not as exposed to single issuer risk like those investors who bought Hyflux perpetuals or Credit Suisse AT1 bonds.

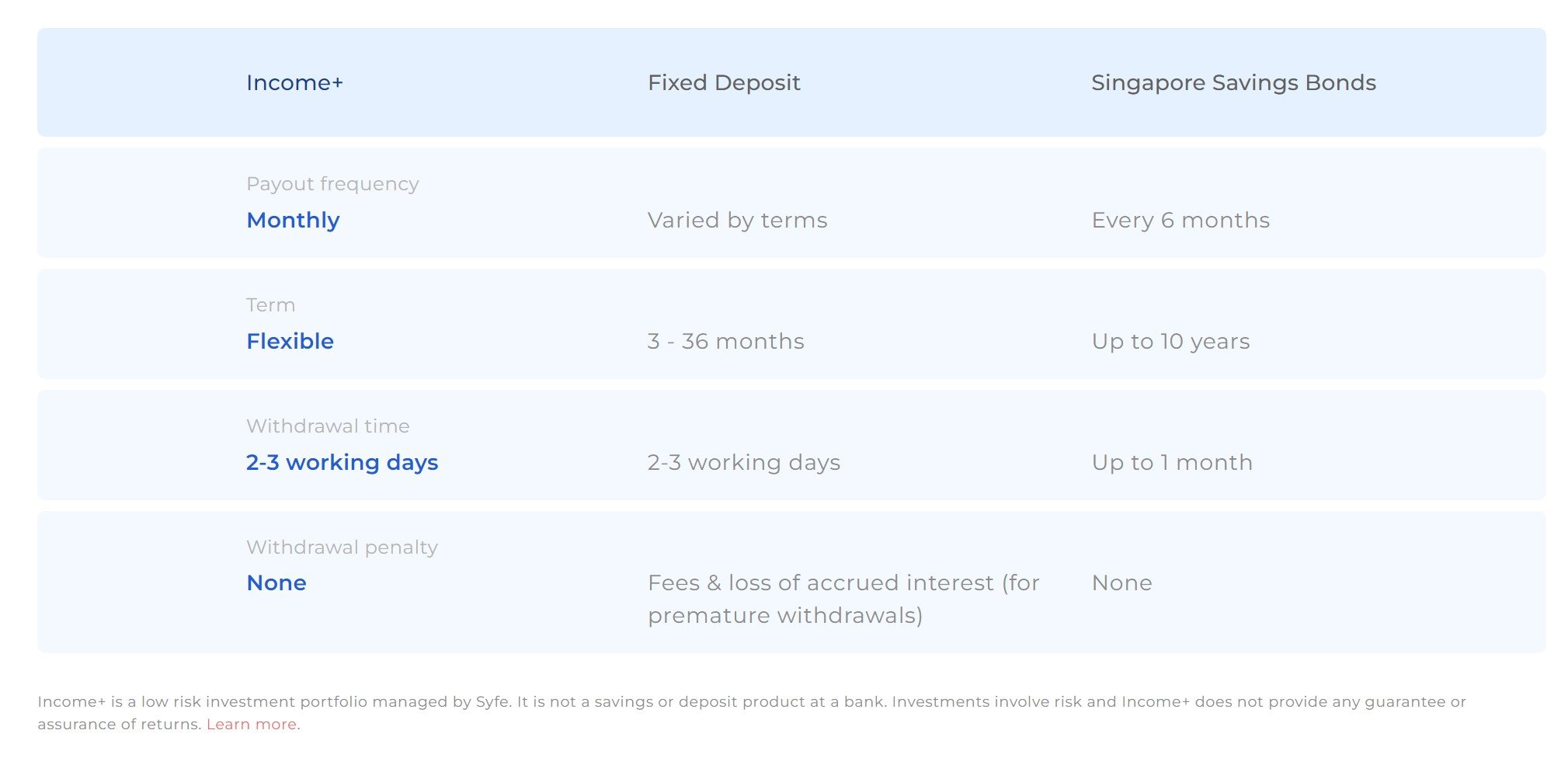

Syfe Income+ compared vs Singapore Savings Bonds or Fixed Deposit?

How does Syfe Income+ compare with Singapore Savings Bonds or Fixed Deposit?

I’ve set out a table that compares the pros and cons.

Broadly speaking, Fixed Deposit and Singapore Savings Bonds are risk free (up to $75,000 for fixed deposit), but tends to have lower yields.

Fixed deposit duration doesn’t really go up beyond 1 – 2 years too.

While Syfe Income+ has much more flexibility on term and has higher yields, but is not risk free.

So it really goes back to what you prioritise as an investor, and whether you want to take measured risks for a higher yield.

Although that said it doesn’t need to be all or nothing.

You can mix in Syfe Income+ as another option for mid to longer term cash holdings, while still keeping money in Fixed Deposit and Singapore Savings Bonds.

How does Syfe Income+ compare to DIY investing (with a basket of dividend stocks / REITs)?

The more I look at Syfe Income+, the more I realise a comparison to DIY investing is not an apples to apples comparison.

For the simple reason that as a Singapore based retail investor, you will never be able to build a fixed income portfolio as diversified as what Syfe (or PIMCO) have done here.

I suppose you may ask how does compare to a basket of Singapore dividend stocks or REITs.

Well, the risk profile is fundamentally different.

With stocks / REITs you are taking on equity risk premium.

In a recession, there is a real risk of capital loss with stocks / REITs.

Whereas with a fixed income portfolio like Syfe Income+, there are potential hedging benefits because bond prices typically go up in a risk-off environment (when interest rates go down).

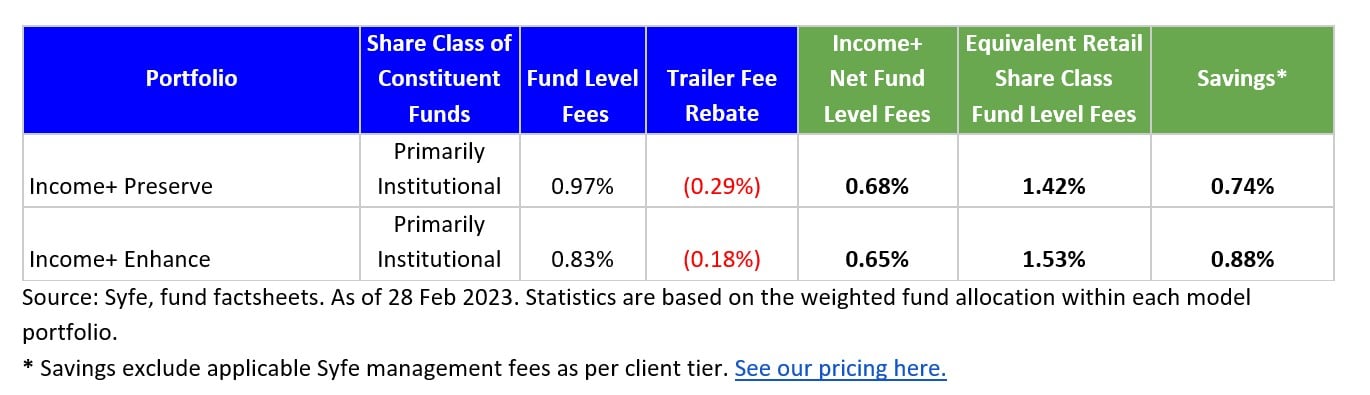

Fees of Syfe Income+

The fund level fees are set out below, but you get full trailer fee rebates which helps reduce the fees quite a bit (almost 60%) as compared to if you buy it as a retail investor.

Launch Promo Code!

Similar to Syfe’s other portfolios, Syfe’s fees start from 0.35% to 0.65% depending on membership tier.

There’s a special Launch Promo for Syfe Income+ clients!

For new Syfe users, use promo code “FINANCIALHORSE” to enjoy 3 months fee waiver.

Deposit a minimum of S$10,000 to enjoy the 3 months fee waiver, and fee waiver is available for up to S$50,000.

For existing Syfe users, enjoy fee rebate depending on the amount deposited:

S$10k: 3 months

S$50k: 4 months

S$100k: 6 months

Use promo code “FHRB” to enjoy this special promo.

- Promotion is applicable to fresh fund deposits only

- Minimum deposit amount must be completed by 31 May, 2023

Terms & Conditions apply.

Find out more here!

Who can consider buying Syfe Income+

The way I see it, there are 2 groups of investors who could benefit from Syfe Income+.

Firstly, those who have a sum of money that they will probably need in a few years time, that they don’t want to take too much risk on.

For example money saved up for a BTO or marriage, that they don’t want to put into equity markets given the volatility.

For these investors, Syfe Income+ can be considered as an alternative to the usual T-Bills / Singapore Savings Bonds / Fixed Deposit.

You take on a bit more risk, but you get a higher dividend payout in exchange (on a monthly basis).

Don’t underestimate the monthly payment, this can be very helpful for some investors (especially those that need to spend the income).

Alternatively, those who want to put some money into a lower risk income portfolio for the mid-term.

T-Bills have significant interest rate risk because you need to roll the bills every 6 months. While Singapore Savings Bonds only offer about 3% yields.

Syfe Income+ can be an alternative with the higher yields, higher duration that you’re locking in, and you also get the benefit of monthly dividend payouts.

Follow up questions on Syfe Income+ (updated 10 May 2023)

Following up on this piece, a lot of readers wrote in with questions on CPF-OA, SRS and Withholding Tax.

So I wrote in to Syfe to clarify these points.

You can see my questions to them, and Syfe’s replies below:

1. Are there any plans to allow CPF-OA or SRS Funds to be used to purchase Syfe Income+?

Syfe: Yes, this is something we are working towards. We could see this in the near future.

2. Is the dividend payout be subject to any withholding tax? Is the projected 4 – 4.5% payout before withholding tax (and fees)?

Syfe: This is a good question, so let me clarify. I assume there are two parts to this question:

- How are our fees calculated?

Syfe’s platform fees are separately calculated based on the overall AUM of the account, inclusive of other wealth portfolios.The fees are charged on the net asset value (NAV) and not taken from the monthly payouts.

- Is the dividend payout subject to any withholding tax?

The 4-6% payouts are not subject to any withholding tax. In addition, the funds are all domiciled in ireland which makes them much more tax efficient compared to US listed funds/ETFs which can result in up to 30% dividend withholding taxes.

Check out Syfe Income+ here!

Don’t forget to use the promo code FINANCIALHORSE (new Syfe users) or FHRB (existing Syfe users) to enjoy a rebate on fees!

Find out more at Syfe’s live webinar on 11 May 2023!

Register for free here!

Disclaimers:

The information contained herein is provided for general information only, and should not be used as a basis for making any investment or business decisions. All return figures shown are presented for informational purposes only and are not indications, predictions, forecasts, nor guarantees of future performance results, or the quality of an investment, are subject to change without notice and may differ or be contrary to opinions expressed by others. All projections are made in good faith and reasonable effort is made in the calculations, but Syfe does not take responsibility for the calculation of assumed target returns, no representation or warranty is given as to the adequacy or reasonableness of the methodologies or assumptions used in calculating assumed target returns, and no reliance should be placed on any assumed target return.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Is this available to invest using CPF or SRS monies? Seems like this product would be quite suitable for CPF/SRS investment purposes.

Unfortunately I don’t believe Syfe Income+ can be used for CPF or SRS yet. Let me confirm with Syfe if they will be getting approval for this.

I think the indicative yield for the income+ is before the 15% witholding tax. So, net yield is lower

That’s an interesting point. Let me confirm with Syfe if their numbers are before or after withholding tax, and if so what level of withholding tax is payable.

Total expense ratio would be at least 1.3% if we take platform fees into consideration.

Can you compare this to EndowUs bond fund offerings? I believe they are quite similar.

Endowus does have platform fees as well though, may not necessarily be cheaper: https://endowus.com/pricing

Endowus’s offering has a slightly different mix of funds too, so not really an apples to apples comparison.

FH, interest rates are quite high now, hence the syfe income+ portfolios are able to provide relatively high rates.

what happens when the interest rates start falling again? and goes to low rate environment, are they still able to dish out 4-6%? would it be sustainable?

Technically speaking if interest rates go down the bond funds will go up (capital gains). So this is even better for the funds in the short term.

But let’s say rates stay low for another 4 years though, then the fund will be forced to reinvest the maturing proceeds into new bonds at much lower interest rates, which will bring down the yield over time.

But if you look at how inflation is playing out, it’s questionable if interest rates will stay low for an extended period this decade. Short term maybe if we get a recession, but what happens after that if inflation returns?